Andriy Onufriyenko/Moment via Getty Images

Andriy Onufriyenko/Moment via Getty Images

Ionis Pharmaceuticals, Inc. (NASDAQ:IONS), the Carlsbad, California-based, commercial stage pharmaceutical company, announced its Q4 and full-year 2023 earnings on Wednesday after the market close.

Ionis stock presently trades at around a value of $45.5 per share, and the market appears to have been largely unmoved by this latest earnings report, although, this month, a bull run that lasted throughout 2023, carrying the share price from ~$35 in March, to ~$54 at the end of December - a gain of >50%, ended abruptly, with shares falling >15% in value.

I find it hard to explain this drop, and see it as an advantageous opportunity to buy Ionis stock, as I will explain in this earnings review.

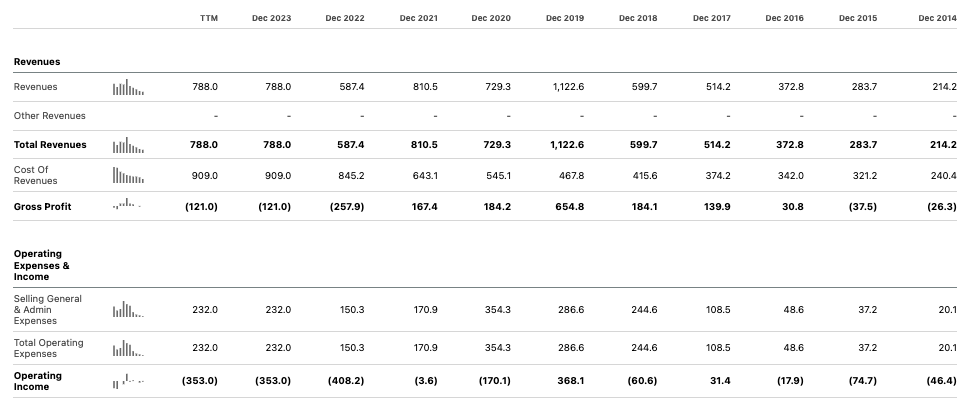

From a financial perspective, the headline figures show Ionis' revenues in the fourth quarter of 2023 more than doubled year-on-year, to $325m, and the company made a narrow loss from operations of $(6m), compared to a loss of $(208m) in Q4 2022.

With that said, the performance of Ionis' 4 commercially approved drugs - excepting Wainua, which was only approved in December (and which I will discuss in more depth later) - QALSODY, SPINRAZA, TEGSEDI and WAYLIVRA - indicated for superoxide dismutase 1 amyotrophic lateral sclerosis ("SOD1-ALS"), spinal muscular atrophy, polyneuropathy caused by transthyretin amyloidosis with polyneuropathy ("ATTRv-PN"), and genetically confirmed familial chylomicronemia syndrome ("FCS") - was a little underwhelming.

Firstly, lets discount QALSODY, since Biogen now owns all rights to commercial revenues from the drug. Spinraza royalties - Biogen (BIIB) is responsible for marketing and selling the drug, with Ionis earning tiered royalties up to the mid-teens percentages - came to $62m in Q4, down slightly from the $67m earned in Q4 2022. Tegsedi and Waylivra revenue came to just $9m, however, up from $7m in the prior year period, with an additional $8m from licensing and royalty revenues.

Across the full year, Spinraza earned $240m of royalty revenues, Tegsedi and Waylivra $35m, with an additional $34m contribution from licensing and royalty revenues. The total of $309m earned compares to $303m earned in 2022.

Additionally, Ionis earned $125m in the form of amortization from upfront payments - up 80% year-on-year - $101m of milestone payments, $117m of license fees, and $10m from "other services," for a total of $353m from "collaborative agreement revenue" - up 71% year-on-year.

Finally, joint development revenue in relation to newly approved Wainua - from Ionis' co-development partner AstraZeneca (AZN) - came to $126m, meaning Ionis earned total revenues of $788m - up 34% year-on-year. Ultimately, Ionis beat its own revenue guidance for 2023 by >$200m.

Overall, this can be considered a good performance from a company whose revenues are often unpredictable in nature, due to the one-off nature of milestone payments from Ionis' various partners - including Biogen, AstraZeneca, Novartis (NVS), Roche (OTCQX:OTCQX:RHHBY) and GSK (GSK) - however, turning to the bottom line, Ionis remains a heavily loss-making company.

Ionis income statement historical (Seeking Alpha)

As we can see above, however, Ionis posted an operating loss of $(353m) for the year, following from a loss of $(408.2m) in 2022. The company's net income, working back from 2023, has been $(366m), $(270m), $(29m), and $(480m) in 2020.

This is not necessarily a problem for Ionis, given it reported a cash position of $2.33bn as of the end of 2023, but in order to grow its market cap valuation, and reward shareholders with a rising share price, at some stage, the company will need to show it can turn a profit, as well as developing groundbreaking new drugs.

Ionis management is guiding for revenue of $575m in 2024, down 27% year-on-year, while operating loss is forecast to be <$475m, resulting in a forecast cash position at the end of 2024 of ~$1.7bn.

As such, there is little change to the pattern of heavy spending, and unpredictable revenue performance, offset by a more than healthy cash position.

The main revenue driver will once again be Spinraza royalties, according to management - on the Q4 earnings call, Ionis' Chief Financial Officer ("CFO") Beth Hougen commented that:

Our total expected revenue for 2024 includes a sizeable base of commercial revenue with SPINRAZA as the cornerstone. We expect the resilience SPINRAZA has demonstrated to continue at our royalties to reflect that.

Biogen reported revenues for Spinraza of $610.5m in 2023, up from $600.2m in 2022. Although there may have been a small uplift, the fact that revenues barely grew may imply that the drug's sales have hit a ceiling, and it should also be noted that in January 2023, Ionis agreed to sell a 25% portion of its royalties due from sales of the therapy to Royalty Pharma (RPRX). That portion will rise to 45% after 2028, for a total consideration of $1.1bn, which also entitles Royalty to receive 25% any royalties earned from Ionis' drug candidate pelacarsen, which it is co-developing with Novartis.

As such, long-term, Ionis' earnings from Spinraza do seem likely to decrease. With that said, the December approval of Wainua, in the indication of polyneuropathy of hereditary transthyretin-mediated amyloidosis ("hATTR"), is significant. The rare disease apparently affects ~50k patients worldwide, although the figure in the U.S. - the only territory in which Wainua has been approved to date - is likely closer to 13k.

Rival RNA-interference drug developer Alnylam (ALNY) has commercialised two drugs - Onpattro (patisiran), and next-generation Amvuttra (vutisiran) - in the indication of hATTR, which earned respectively $355m, and $558m in 2023, meaning the franchise earned >$900m of revenues. Being available in auto-injectable form, Wainua may have a critical edge over Alnylam's drugs, which must be administered subcutaneously at a Physician's office - that will help it gain market share.

Analysts have previously speculated that Wainua could achieve peak revenues of ~$1.3bn, although in order to achieve that kind of revenue number, the therapy may need to secure a follow-on approval in cardiomyopathy - a 400k - 500k patient population. The class-leading drugs in that indication are Pfizer's (PFE) Vyndamax and Vyndaqel, which earned >$3.3bn in 2023.

By the terms of its agreement with AstraZeneca, Ionis will split Wainua revenues in the U.S. 50/50 with its partner AstraZeneca, and may receive up to $485 million in development and approval milestones, and up to $2.9 billion in sales-related milestone payments.

While Ionis' forecast for the top and bottom line in 2024 may not give shareholders or Wall Street much encouragement, Wainua is an exciting prospect, and when we consider the current state of play with Ionis' pipeline - the overall picture becomes even more encouraging.

In its 2022 10K submission / annual report, Ionis discusses its clinical pipeline as follows:

All of the medicines currently in our clinical pipeline use our antisense technology — an innovative platform for discovering first-in-class and/or best-in-class medicines. Antisense medicines target RNA, the intermediary that conveys genetic information from a gene to the protein synthesis machinery in the cell.

By targeting RNA instead of proteins, we can use antisense technology to increase, decrease or alter the production of specific proteins. Most of our antisense medicines are designed to bind to mRNAs and inhibit the production of disease-causing proteins.

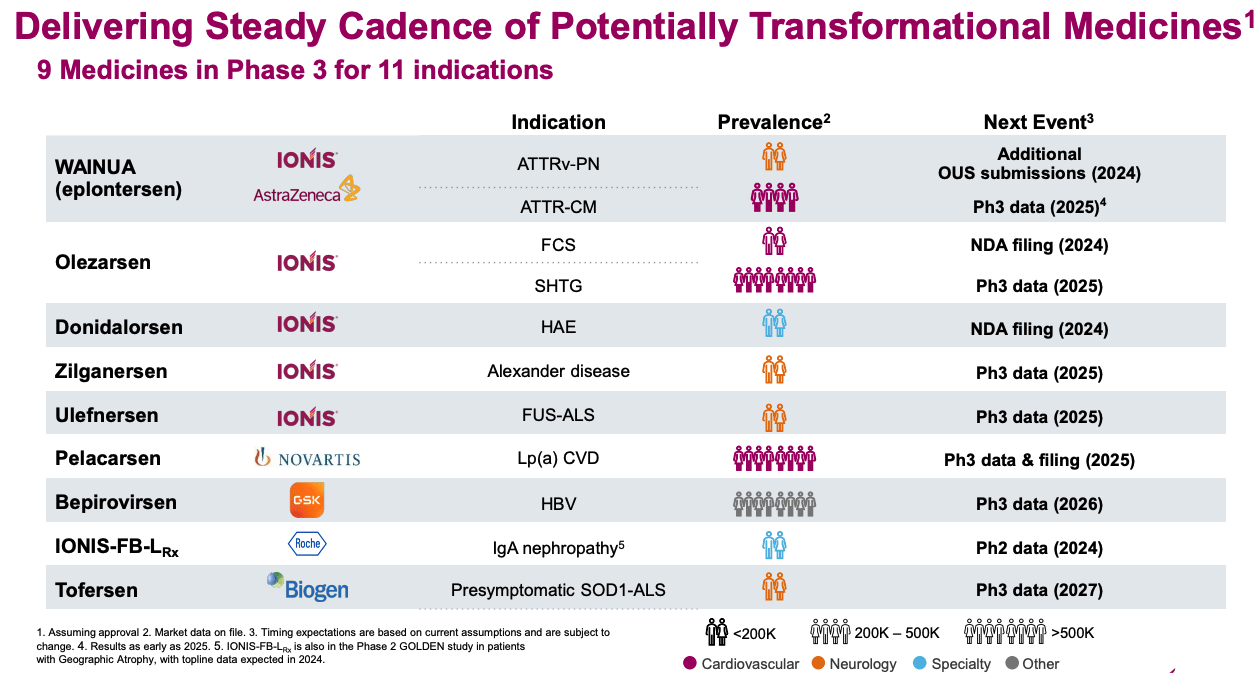

As we can see below, as of the beginning of 2024, Ionis is guiding 9 different medicines through Phase 3 studies targeting 11 different indications:

Ionis late stage pipeline (Q4 earnings presentation)

We have already discussed the strong promise of Wainua, although it is worth noting an important data catalyst upcoming in 2025 - Phase 3 data in cardiomyopathy.

This year, Ionis hopes to file an New Drug Application ("NDA") for its proprietary drugs Olezarsen, in familial chylomicronemia syndrome ("FCS"), for donidalorsen, in hereditary angioedema ("hAE"), as well as potentially for Novartis partnered pelacarsen, Phase 3 data permitting.

At the end of September Ionis announced positive Phase 3 clinical study results for olezarsen in FCS - a rare, genetic disease that results in extremely elevated triglyceride levels, and can lead to acute panceratitis. The drug met its primary endpoint of achieving a statistically significant reduction in triglyceride levels versus placebo.

The underwhelming sales of Waylivra, also indicated for FCS, suggests that olezarsen will not be a major revenue driver in this small market, but an approval may help pave the way for a an approval in severe hypertriglyceridemia (SHTG) - in fact, the Phase 3 data readout in SHTG probably the more significant catalyst to keep an eye on.

The 2-part pivotal study in SHTG will enrol nearly 1,000 patients, and should that be successful, Ionis believes it will have another approvable drug with "blockbuster" (>$1bn revenues per annum) potential on its hands.

Ionis reported last month that donidalorsen, indicated for HAE - a rare disease characterized by instances of welling of the skin, gastrointestinal and respiratory systems, face and throat, which can be life-threatening - met its primary endpoint of statistically significant reduction in the rate of HAE attacks in patients, and also met all key secondary endpoints, with no serious adverse events reported.

As such, an approval looks highly likely - Ionis has already sold exclusive rights to market and sell its drug in Europe to Otsuka Pharma, in exchange for $65m cash upfront, and tiered royalties on sales ranging from 20-30%. Biocryst's (BCRX) Orladeyo, and Takeda's Takhzyro will represent donidalorsen's main competition within the HAE market. The two drugs earned respectively ~$150m, and $325m in 2023.

While noting Phase 3 readouts for Zilganersen and Ulefnersen in 2024, neither drug is likely to make too significant a contribution to Ionis' top line revenues, if approved, but pelacarsen, in cardiovascular disease ("CVD"), ought to have "blockbuster" potential. Novartis took up the option to co-develop the drug with Ionis in 2019, and has also paid Ionis a further $60m for rights to a next-generation version of the drug, with additional milestones and royalties on sales in play.

Considering the breadth of Ionis' pipeline and how many Big Pharma partners the company has managed to attract, I find it hard to blame management for running up a huge R&D bill - $900m in 2023, and $833m in 2022 - that is not nearly offset by revenues, royalties and milestones at the present time.

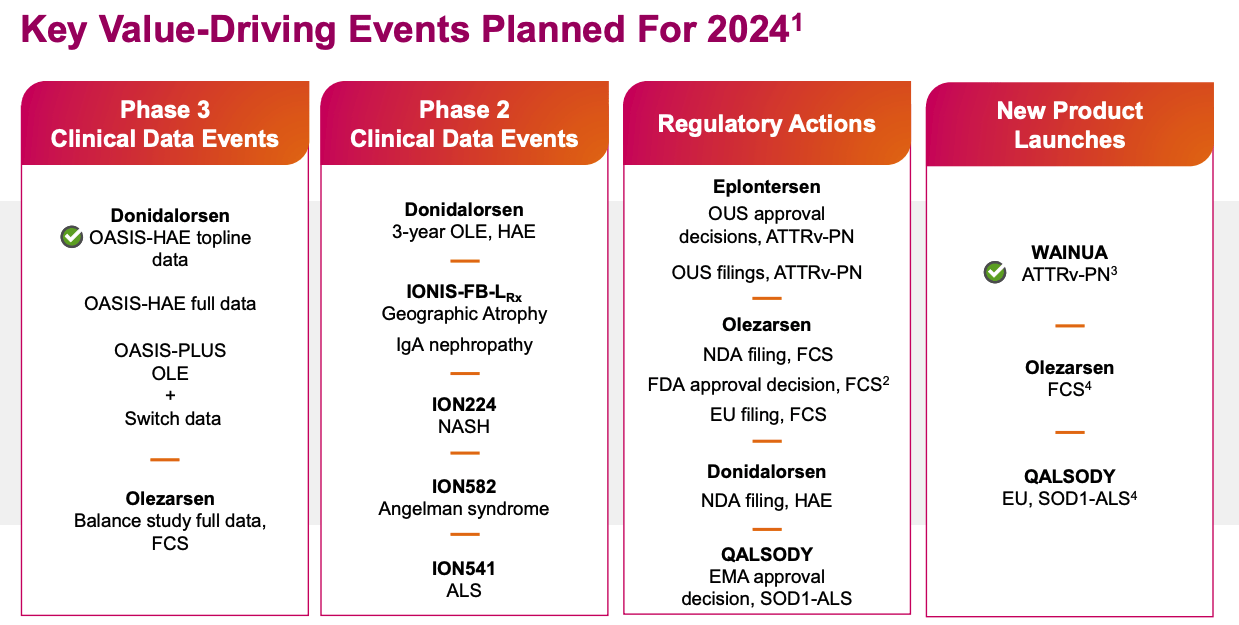

If we look ahead at 2024, this may not be the year that Ionis breaks its pattern of heavy spending and unpredictable revenue generation, with expectations managed downward by the forward guidance for >$575m of revenues and <$475m of operating losses, although management clearly believes revenues could outperform its guidance (as they did in 2023), and losses could be narrower than expected.

Ionis key catalysts in 2024 (ionis presentation)

As we can see above, there are plenty of non-revenue generating catalysts for share price upside in 2024 - I have not mentioned it yet in this post, but the Roche (OTCQX:OTCQX:RHHBY) partnered geographic atrophy (eye disease) and IgA nephropathy candidate data could be highly significant - with $810m of milestone payments in play, and tiered royalties on net sales which could rise to 20% (according to Ionis' 2022 10K). This could be the most likely source of additional revenues in 2024.

Looking beyond 2024, the olezarsen / SHTG opportunity, Wainua in ATTR-CM, pelacarsen, and bepiroversen (a GSK partnered project to develop a more effective hepatitis B therapy, with $260m of milestones payments in play, plus tiered royalties) opportunities come into play, and on revenues and royalties alone, I estimate Ionis could generate close to >$4bn of revenues - $1.5bn from Wainua, if approved in ATTR-CM, $1bn from olezarsen, $0.3 from donidalorsen, and $0.5 from pelacarsen, bepiroversen, and the ROCHE candidate, plus as much as $300m per annum in milestone payments.

To sum up Ionis 2023 earnings and 2024 guidance by critiquing the company for being loss-making, and for failing to generate much in the away of revenues from its commercial drug portfolio, would be wrong in my opinion.

The likes of Tegsedi, Waylivra, and even Spinraza can be characterized as a "first wave" of antisense drug products that establish proof-of-concept, validate Ionis technology and approach to drug development, and have helped attract some of the biggest names within the pharmaceutical industry, prepared to invest money upfront, and pledge generous milestone payments and royalties on future sales.

The "second wave" of Ionis drugs - olezarsen, pelacarsen, Wainua, and others - appear to have genuine "blockbuster" potential, and even though Ionis is sometime compared favorably with other drug developers operating in a similar space - Arrowhead Pharmaceuticals (ARWR), for example, often cited as having the best-in-class technology platform, or Alnylam (ALNY), further along commercially, the reality is that Arrowhead remains a clinical stage company, and Alnylam's market cap valuation makes investing in the company almost prohibitively expensive.

Ionis ticks many of the crucial boxes when it comes to assessing the investment appeal of a drug development company - primed for revenue growth, narrowing losses, ability to attract Big Pharma, billions of milestone payments in play, lucrative royalty streams, with many more set to initiate in the coming years, healthy cash position, and very low forward price to sales ratio of <1.5x, based on my ballpark revenue forecasts at least. In short, I believe Ionis warrants a >$10bn market cap valuation today, based on its stand-out potential.

I continue to make Ionis Pharmaceuticals, Inc. stock a Strong Buy opportunity. Even if 2024 is not going to be the company's breakout year, much of the groundwork for a surge in valuation will be laid in 2024, I believe. My suspicion is that investors paying $45 per share for Ionis stock today will be handsomely rewarded in the years to come.

Editor's Note: This article discusses one or more securities that do not trade on a major U.S. exchange. Please be aware of the risks associated with these stocks.