Just_Super

Just_Super

Last week, Innoviz Technologies (NASDAQ:INVZ) confirmed the company is moving full speed ahead with Lidar sensors entering production deals for the automotive market. The market just ignored the stellar growth and clear signs the company has exited the pre-revenue phase. My investment thesis remains ultra-Bullish on the Lidar stock, which is still trading near the all-time lows.

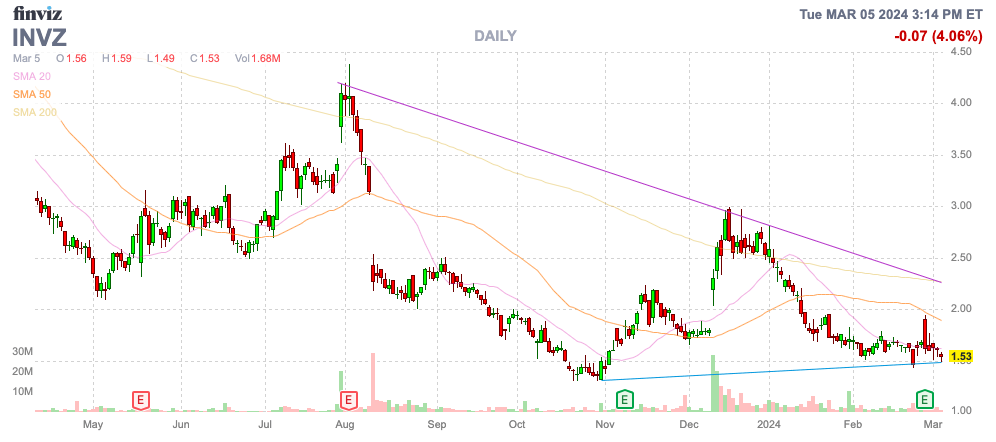

Source: Finviz

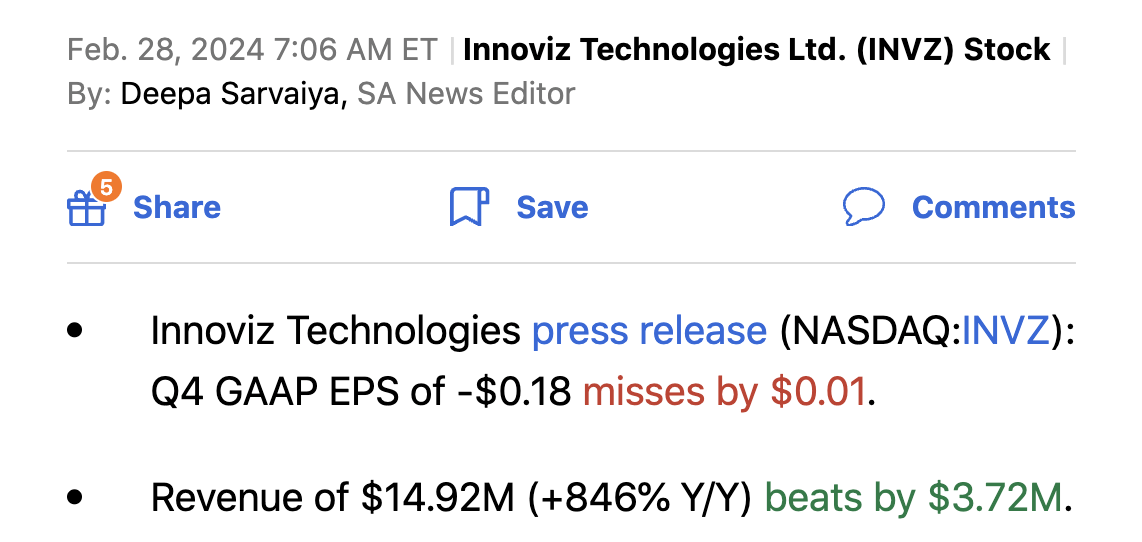

Innoviz reported a massive quarter to end 2023 with revenues surging 846% as follows:

Source: Seeking Alpha

Revenue surged due to sales of production Lidar sensors, NREs and sample sensors. Innoviz didn't provide any details on the specific quarterly numbers, suggesting the year-end boost wasn't due to production units.

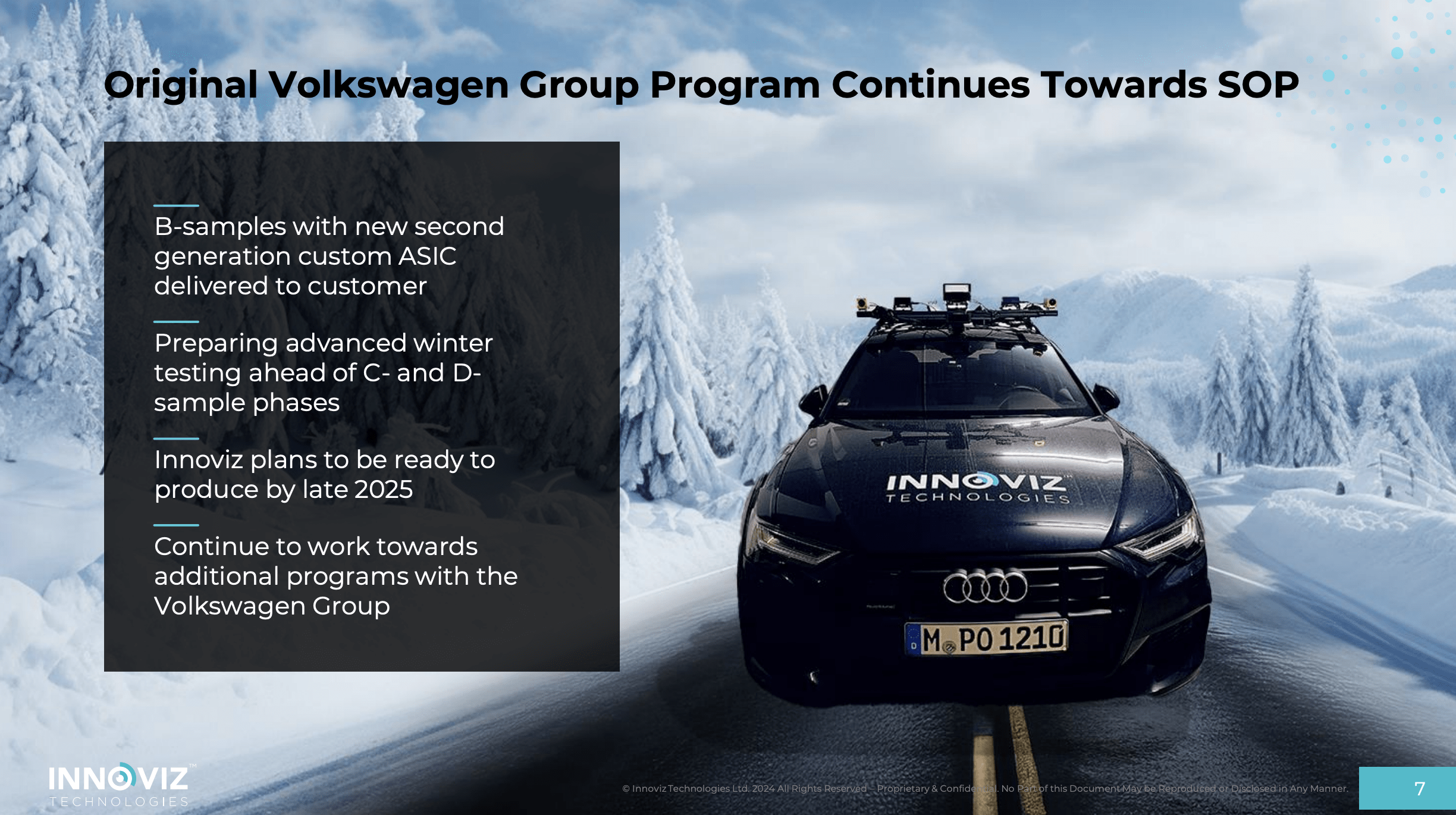

Innoviz did announce huge progress towards new and existing programs with key customers of BMW (OTCPK:BMWYY) Volkswagen AG (OTCPK:VWAGY) and in the last quarter as follows:

The original VW deal leading to the big proclamation of a $6+ billion forward order book is still in the works. Innoviz even suggested the order book was larger due to the second VW program for the light commercial vehicle, though the company didn't provide the updated order number in order to not inadvertently reveal order details about this program.

Source: Innoviz Tech, Q4'23 presentation

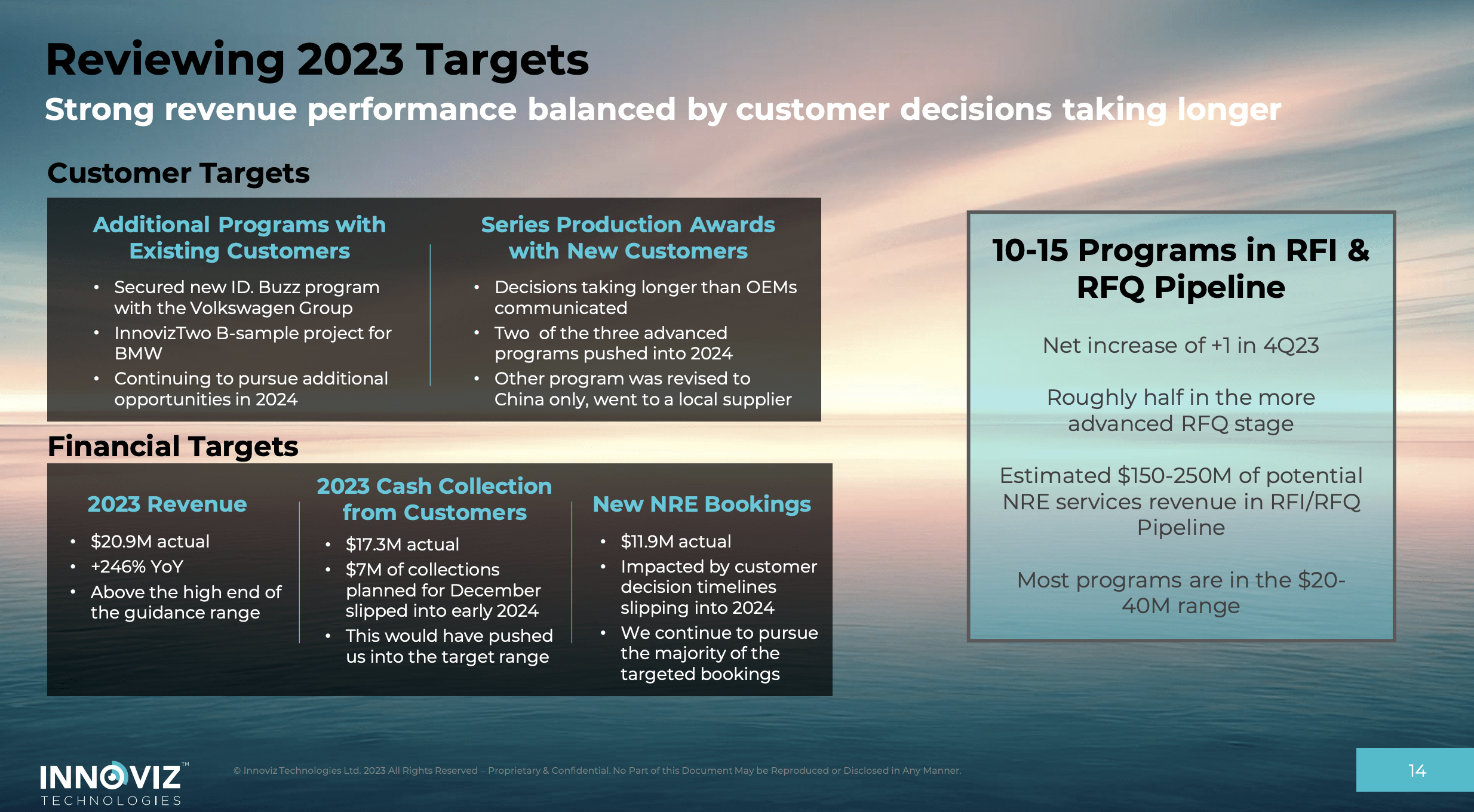

The stock has a market cap of just $250 million despite the large Q4 revenue posted, the massive order book and another 10 to 15 programs in the RFI and RFQ pipeline. Innoviz has multiple catalysts for the stock and the order book here.

Source: Innoviz Tech. Q4'23 presentation

The market wasn't happy with the guidance for Q1'24 revenues of only $5 to $6 million, though the guidance is for massive sales growth. Innoviz is set to report revenues growing 400% YoY for the March quarter, yet the market is worried about the sequential decline in revenues normal in this sector until production deals normalize the quarterly unit volumes.

A big key to the investment story here is the sales launch of the BMW i7 series in Germany. Along with the Volvo EX90 using Luminar Technologies (LAZR) Lidar, several major vehicles with production launches utilizing Lidar sensors will provide more confidence with sector stocks.

Once these production vehicles start, other vehicle lines will feel the pressure to match the technology of the BMW and Volvo vehicles, and the revenue streams will start flowing. Right now, a lot of the revenues reported by these companies are tied to NREs and sample units with unpredictable sales patterns.

Innoviz ended 2023 with a cash balance of only $150 million, so the successful launch of production vehicles is a game changer for the financial picture. Suddenly, the company can model the path to turning cash flow positive.

For Q4'23, the Lidar company only reported the quarterly cash burn at $14.5 million. Naturally, the cash burn won't improve much with revenues dipping in Q1'24, though the negative gross margins in the December quarter likely don't alter the cash flow picture for now.

Innoviz announced a 13% headcount reduction back in January. The company forecast a $22 to $24 million improvement in annual cash outlays going forward. With the Q4'23 operating expense base at $24 million, Innoviz just cut the quarterly cash expense rate below $20 million.

The Lidar company would appear poised to make that leap towards cash flow breakeven as production deals start. Higher production volumes should tip gross margins toward positive numbers finally allowing gross profits to offset operating expenses and further cut cash burn rates.

Innoviz is already poised to report substantial revenue growth in 2024, yet the lack of guidance for the full year weighed on confidence. The company has a vehicle actually in production with deliveries starting in Germany providing a game changer for the business.

The biggest negative is the minimal market cap could lead to massive dilution, if Innoviz is again forced to raise more capital. The limited valuation could provide substantial upside, if the Lidar company can report meaningful growth wiping out cash burn rates and limit any further dilutive capital raises.

The key investor takeaway is that Innoviz Technologies took massive steps, with Q4 revenues soaring to $15 million. The market has completely ignored the positives steps with key global customers and the stock is poised for a major rally with production deals ramping and the company likely to announce more Lidar deals in the automotive space.

Investors should use the ongoing weakness to load up on Innoviz.