Kemal Yildirim

Inmode products (Google Image)

Editor's note: Seeking Alpha is proud to welcome Guilherme Nunes as a new contributor. It's easy to become a Seeking Alpha contributor and earn money for your best investment ideas. Active contributors also get free access to SA Premium. Click here to find out more »

Kemal Yildirim Inmode products (Google Image)

After years of accelerated revenue growth, the year 2023 and the outlook for 2024 show a company that seems to have reached the exhaustion of its business model, especially in the short term, tending to exhibit slow growth going forward. This factor, combined with the management's reluctance to efficiently allocate the cash surplus ($700+ million), has led me to recommend "HOLD" for InMode's shares.

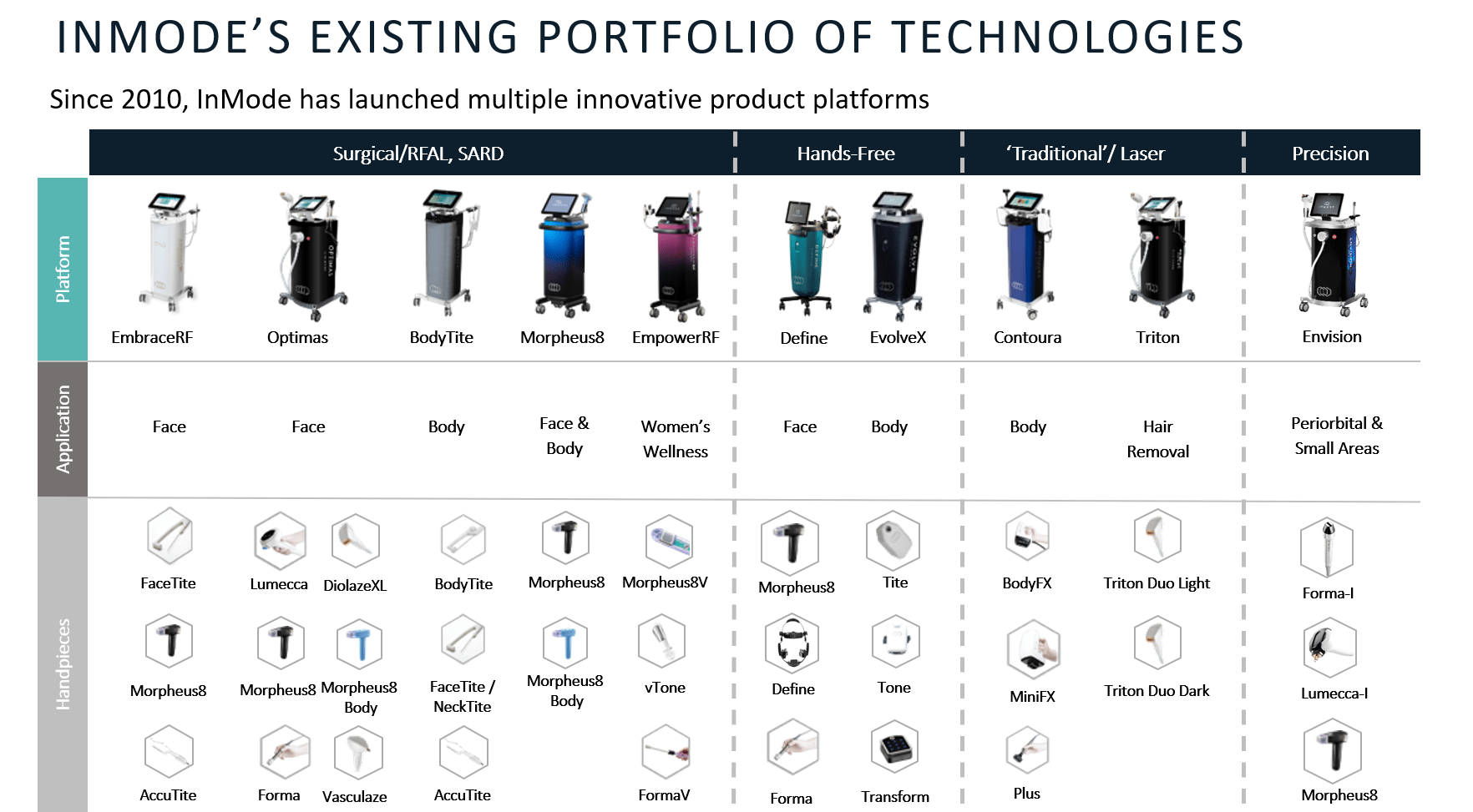

For those not yet familiar with InMode (NASDAQ:INMD), it is a leading global provider of innovative medical technologies. Inmode develops, manufactures, and markets devices utilizing novel radio-frequency (RF) technology aimed at enabling new and improving existing surgical procedures. With its medically accepted, minimally invasive RF technologies, Inmode offers a comprehensive range of products for plastic surgery, gynecology, dermatology, otolaryngology, and ophthalmology across various categories.

Its primary market is in the United States.

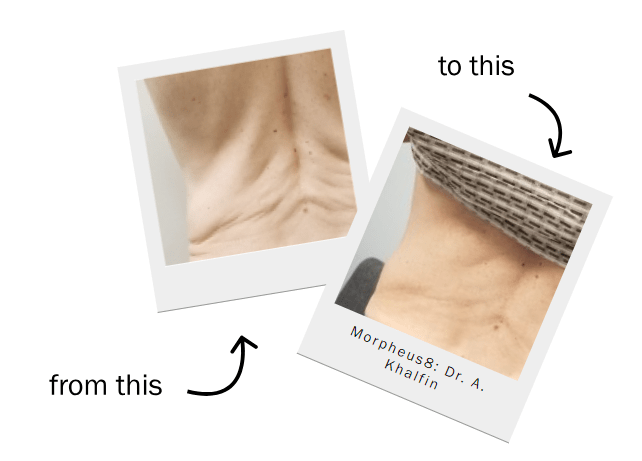

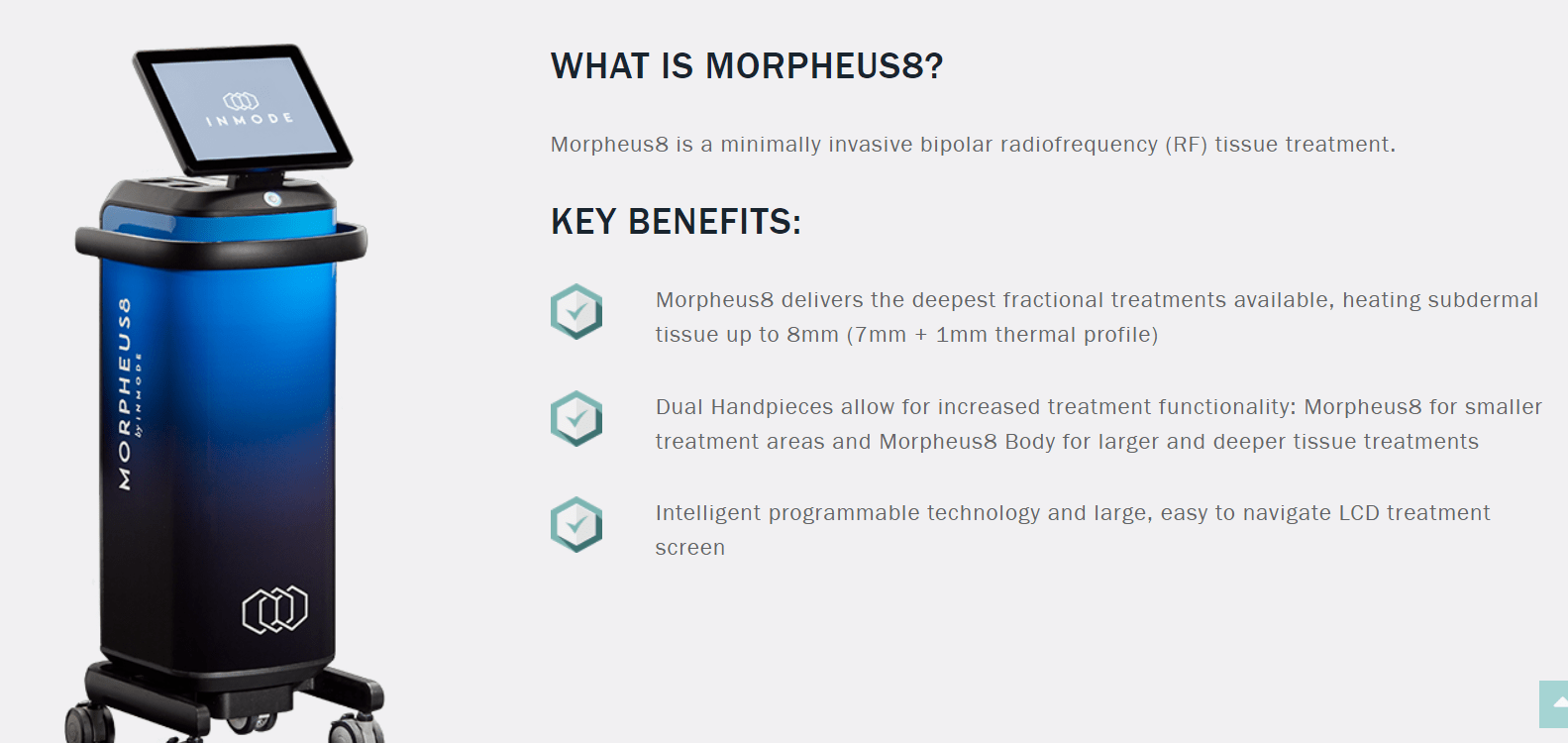

Some examples of improvements that INMD equipment and technology can deliver to its clients:

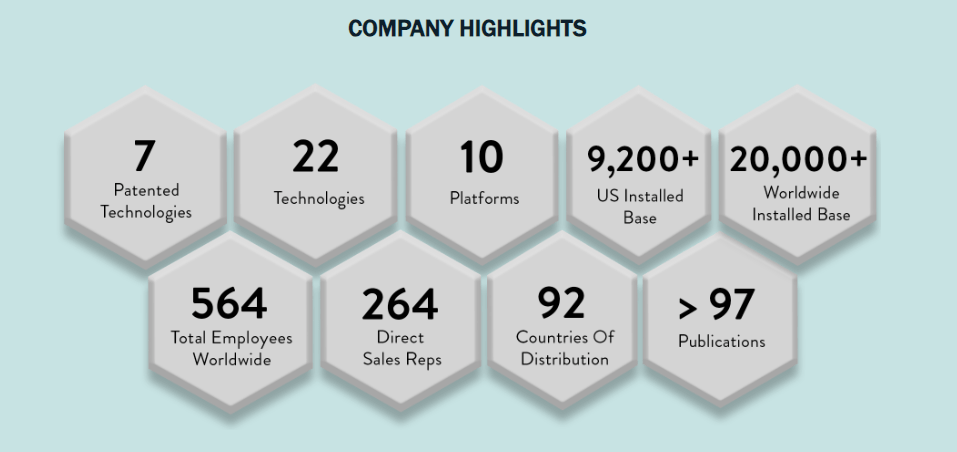

Company Website Company Website Inmode Overview (Inmode IR Website)

Being an Israeli company, its main office is located in the city of Yokneam - Israel, where the company focuses its investments in research and development, engineering center and production. The company also has 12 other offices spread around the world.

The aesthetic market is enormous, with more than 40 million procedures annually, according to data from the company itself. However, not all potential clients are willing to undergo the process, increasing the demand for minimally invasive procedures - this is where InMode comes in. In other words, the company is not only stealing market share from traditional method players but is also creating a new market, as people find the new solutions cause fewer negative effects and, consequently, are accepted by large number of preople.

Since ints foundation, INMD's equipment has performed more than 200,000 aesthetic procedures worldwide.

InMode Website

This high number of procedures is explained by InMode's close relationship with physicians and its increasingly frequent presence on influencers' pages (marketing strategy). This notoriety has brought the company various awards in the industry over the years.

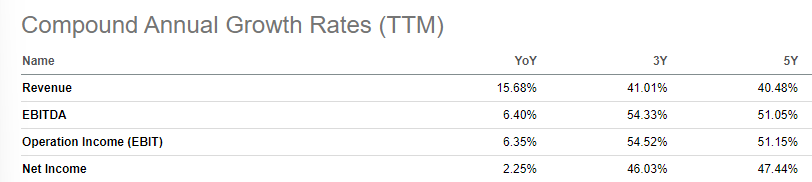

In previous years, the company reported explosive revenue growth, rising from $23 million in 2016 to nearly $500 million in 2023 (a 55% annual growth rate). Despite this significant growth, the company's products are niche and cater to the aesthetic market. In an era of low inflation and high income, as experienced in the last decade in the American market, people are more inclined to spend on non-essential procedures, such as aesthetic treatments.

InMode Website

Consequently, the company positioned itself as a high-growth, technology-driven entity expected to continue its growth trajectory for many years. However, with rising inflation and decreased demand for procedures, the company is seeing its results stagnate with no short-term improvement in sight.

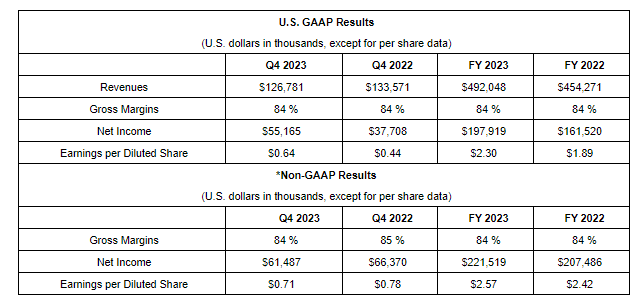

Results 2023 (Inmode IR Website)

On the last day of the 13th, the company announced its year-end numbers, achieving a revenue of $492 million, an 8% growth, which is well below the historical CAGR.

CAGR (SeekingAlpha)

Supporting the idea of stagnation, for 2024, the company expects revenue between $495 million and $505 million, with a gross margin between 83% and 85%. Notably, the guidance for non-GAAP earnings is set to be between $2.53 and $2.57, approximately a -1% change versus 2023 earnings.

Additionally, InMode plans to launch two new products in 2024, which should help maintain market share without much excitement for investors.

In my opinion, despite the conservative guidance, I would not find it strange if the company revises it down further in the future, just as it did throughout 2023.

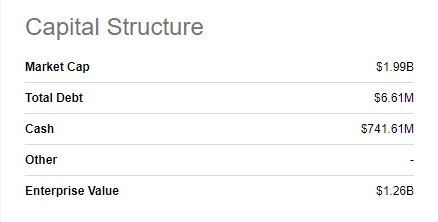

Capital Structure (Seeking Alpha)

Currently, Inmode's business model is asset-light, allowing the company to continue growing without needing significant capital investments in assets, such as factories, with most of the investment going into working capital. However, with a flat market, this need should not increase and likely will decrease over time.

In research and development, the company also invests minimally ($13 million in 2023 or 2.6% of revenue). These factors have historically enabled the company to generate substantial Free Cash Flow.

FCF (seeking alpha)

However, management has been reluctant to create shareholder value through buybacks, instead insisting on acquisitions that are unlikely to occur. If they do happen, they will be for minimal values relative to the company's size.

In a quick exercise, the company currently has over $700 million in cash with no significant liabilities. The company's EBITDA is approximately $200 million, providing ample room for investment, say, $500 to $600 million in buybacks. In the event of an acquisition, the company could take on debts up to $600 million. In this scenario, the company would have up to $800 million available for acquisitions ($200 million in cash + $600 million in debt), which would not significantly impact its financial stability, with leverage around 2x debt/EBITDA. There are no excuses for the company.

In the absence of M&As, the remaining $200 million is more than sufficient to meet the company's research and development investment needs.

Why do i believe the acquisitions will be small relative to the size of the company? Because of the management's fear of making mistakes. In my view, the only plausible explanation for a company holding more than $700million in cash without necessity is fear of the future. As we observed in the 3Q earnings conference, the board appears afraid of conducting buybacks and the stock failling, which reinforces my thesis that if something happens, it will be something that, if it yields negative results, will have a minimal impact.

Moshe Mizrahy

Well, we thought about buyback. We thought about buyback for a long time. But I have to say two things. One, our previous experience with buyback, actually we did buyback for $100 million, did not help, did not help at all. And the stock did not react to that. It was not now, but it did. Second, I'm sure you know that one of our competitors, a company called HydraFacial, which market the product to the same market that we do, mainly to spa and less to doctors, but they sell also to doctors. They have announced six weeks ago that they are doing buyback of $100 million, official buyback, $100 million. We all expected their stock to go up. The stock price when they announced it was $6.3. The stock price today is $4. So they lost 35% of their value in the last six weeks right after they announced the buyback. So it's made us to think twice if this is the best way to support the stock, to do a buyback.

Usually we believe that buyback is something that will help few days and the market will forget that.

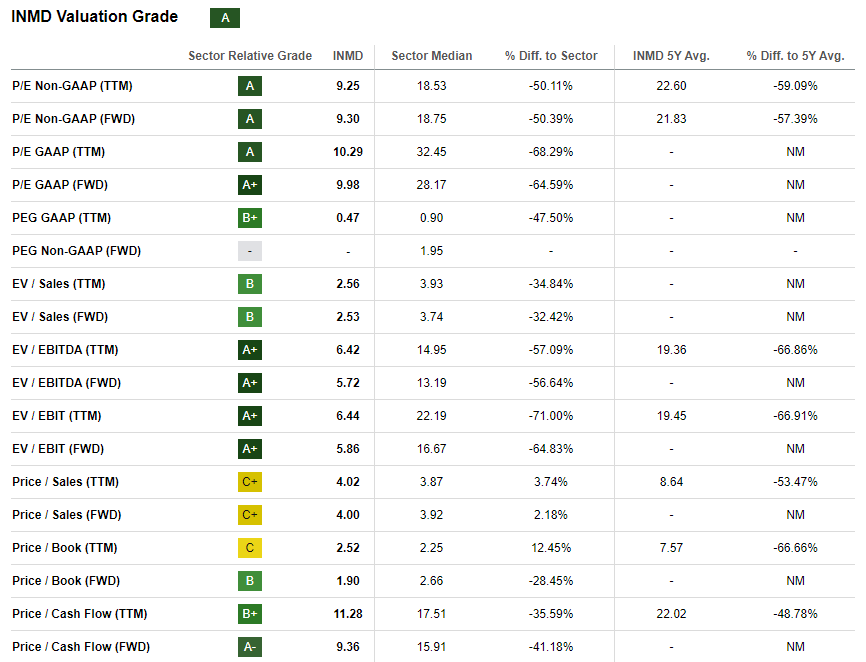

Valuation (Seeking alpha)

InMode is extremely undervalued when considering multiples, especially after adjusting for excess cash. However, acquiring a company solely because it is cheap does not seem sensible. With the market stabilizing and the cash pile growing, the inefficiency of management becomes clearer as they prefer retaining cash rather than creating shareholder value.

For these reasons, we reiterate the recommendation to HOLD.

Like any other investment thesis, the InMode thesis presents significant risks that could lead the company to retreat in the stock market. In my view, the market is tired of the delay in announcing acquisitions or a share repurchase announcement. If this persists for much longer, the company is likely to report negative results.

On the other hand, as previously mentioned, the company has a significant amount of cash available on its balance sheet. If this cash is used to repurchase shares, we're talking about the company potentially buying around 30 million shares (~35% of the total). This would bring an approximate increase of 54% in EPS.

Undoubtedly, InMode's past was magnificent, with significant growth, brand recognition, and market gain, but this does not mean that the medium term will continue similarly. As addressed, the uncertainties ahead are clear, with guidance for the year indicating little growth and a decline in EPS, which justifies the company's recent correction. This, combined with the refusal to usa cash to effectively generate value for investors, has been putting pressure on the stock.

As we say in Brazil, "the directors have both the knife and the cheese in hand" to increase shareholder returns throught aggressive buybacks. After all, doesn't the management believe the shares are cheap? Why aren't they buying?

Therefore, I reiterate my position to HOLD InMode shares.

A revision to BUY or STRONG BUY may occur if management demonstrates the ability to use this cash for purposes beyond paying salaries.