dutchphotography/iStock Unreleased via Getty Images

dutchphotography/iStock Unreleased via Getty Images

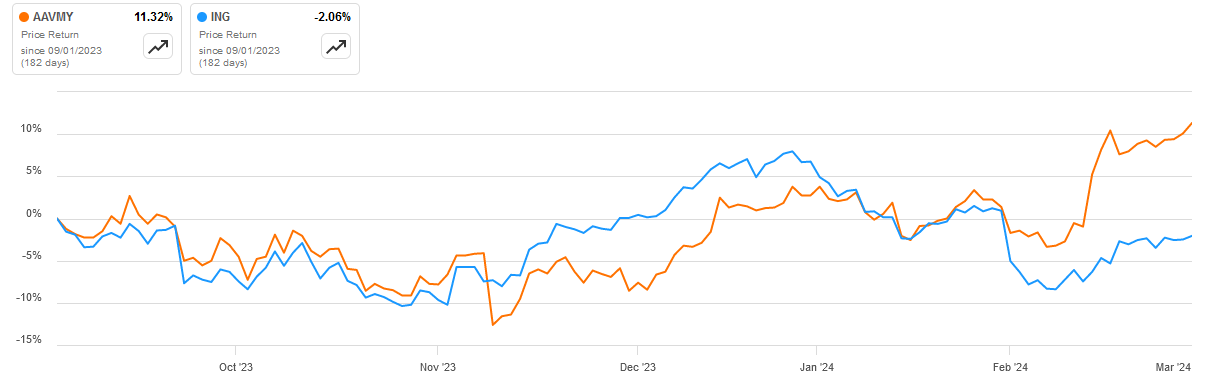

I previously covered ABN AMRO Bank N.V. (OTCPK:AAVMY, ABMRF) back in February 2023, when I argued improving profitability and share buybacks could bridge the valuation gap with its largest peer ING Groep (ING). Over the past year, ABN AMRO actually marginally lagged ING's performance (-6.27% to be precise), although momentum has shifted in the smaller Dutch lender's favor over the past 6 months:

ABN AMRO vs ING, past 6 months (Seeking Alpha)

In brief, I expect this recent outperformance to continue considering the attractive valuation of ABN AMRO, improving underlying economic fundamentals, and scope for further share buybacks.

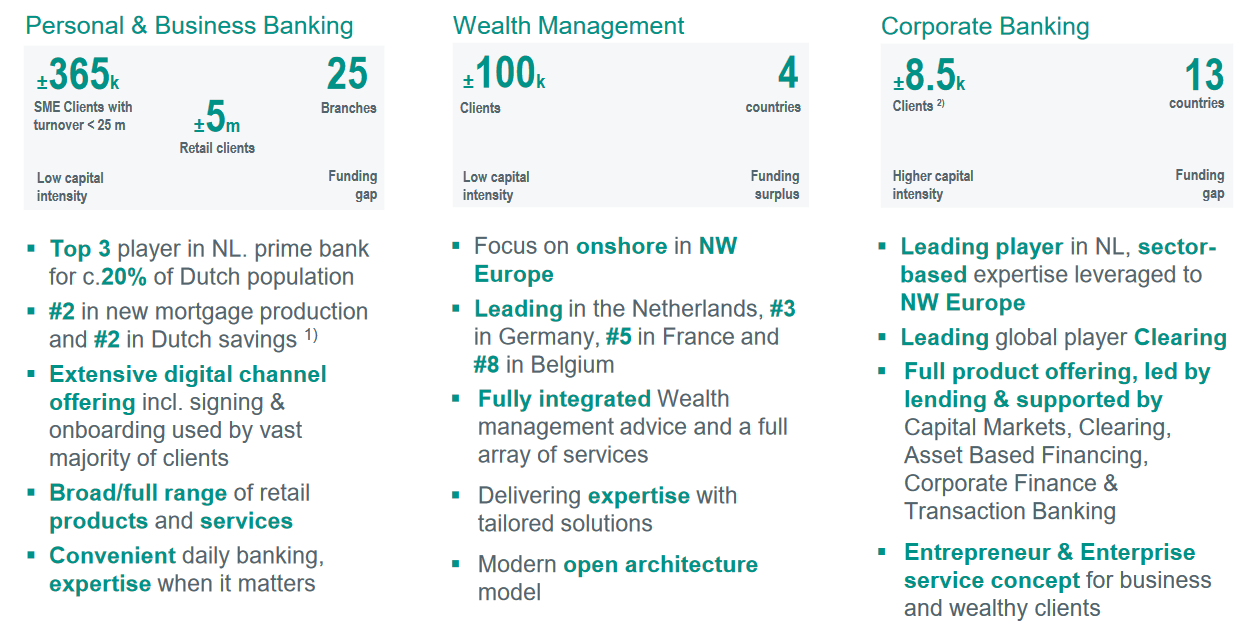

You can access ABN AMRO's financial results here. The bank reports results in three main segments, namely Personal & Business Banking at 45.9% of 2023 operating income (OI), Wealth Management at 18.6%, and Corporate Banking at 39.1% of 2023 OI (totals do not round to 100% due to negative 3.6% OI contribution of Group Functions).

Segment Overview (ABN_AMRO_Q4_2023_Roadshow_booklet)

Personal & Business Banking delivered 6% Y/Y OI growth in Q4 (2023:+19%). The slowdown in the final quarter of the year was due to both 5% Q/Q lower net interest income (NII) and net commission income (NCI). Nevertheless, 2023 was characterized by provision releases, with the cost of risk at -9 basis points ((bps)) in Q4 (2023: -5 bps). This resulted in a 28% Y/Y growth in segment profit for Q4 (2023:+150%).

Wealth Management saw 2% Y/Y OI growth in Q4 (2023:+8%). The slowdown relative to the prior quarter was due to lower NII. Cost of risk was 10 bps in Q4 (2023: -4 bps), which together with higher incidental expenses resulted in a 67% Y/Y drop in segment profit in Q4 (2023: +8%).

Corporate Banking grew its OI 5% Y/Y in Q4 (2023: +4%). This was the only segment to deliver Q/Q OI improvement, driven by NII gains. Cost of risk was negative 27 bps in Q4 (2023:-5 bps), which helped boost segment profit by 78% Y/Y in Q4 (2023:+21%).

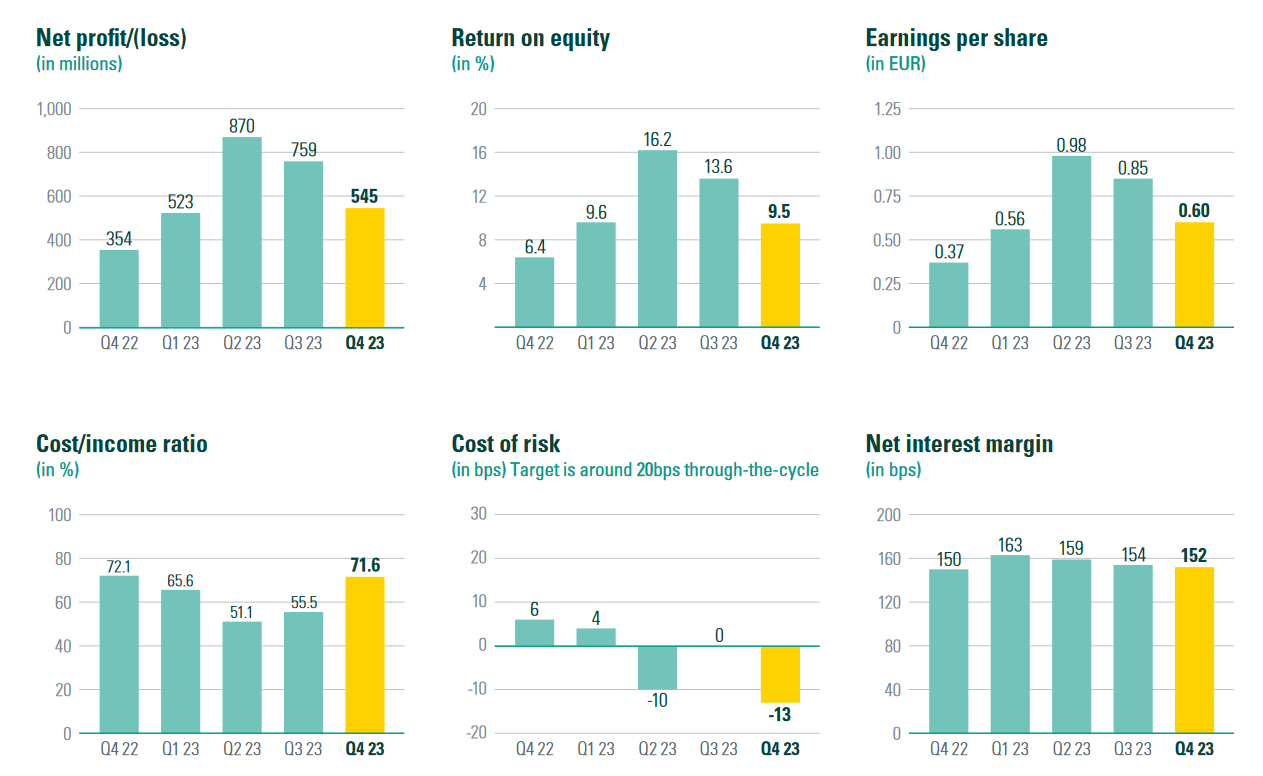

On a consolidated level, operating income increased 10% Y/Y in Q4, in line with the full-year 2023 result. The cost/income ratio was 71.6% in Q4 (2023:60.7%). EPS grew 62% Y/Y to € 0.60/share (2023: €2.99/share, +53%). Cost of risk was -13 bps in Q4 (2023: -5 bps). Return on equity was 9.5% in Q4 (2023: 12.2%). Tangible book value per share was €25.48/share at year-end, +2.6% Q/Q.

Financial result highlights (ABN AMRO Q4 2023 Report)

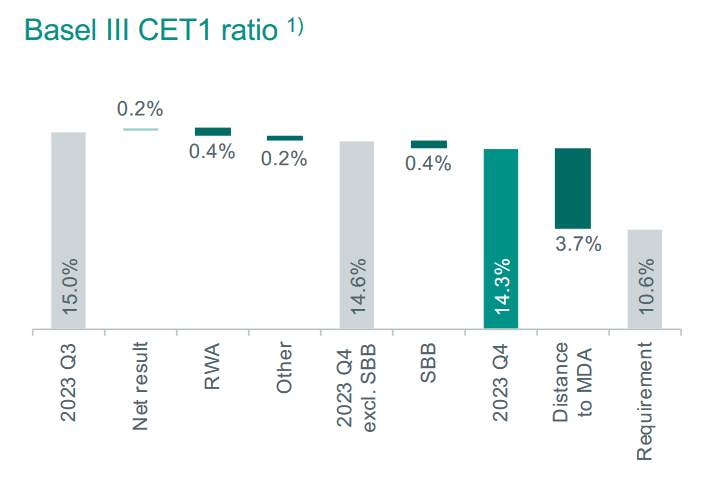

ABN AMRO finished 2023 with a CET1 ratio of 14.3%, down 0.7% Q/Q. With the current regulatory requirement set at 10.6%, ABN AMRO has a 3.7% CET1 capital surplus. What's more, the CET1 ratio already includes a deduction for the €500 million buyback already underway. At current prices, the buyback will be able to retire about 33 million shares, or about 3.8% of total shares outstanding.

Quarterly capital evolution (ABN AMRO Q4 2023 Analyst Presentation)

ABN AMRO expects to benefit from the implementation of Basel IV in January 2025, with the Basel IV CET1 ratio currently calculated at about 15%.

Together with its Q4 results, ABN AMRO also unveiled its 2026 strategic aspirations. My key takeaways are:

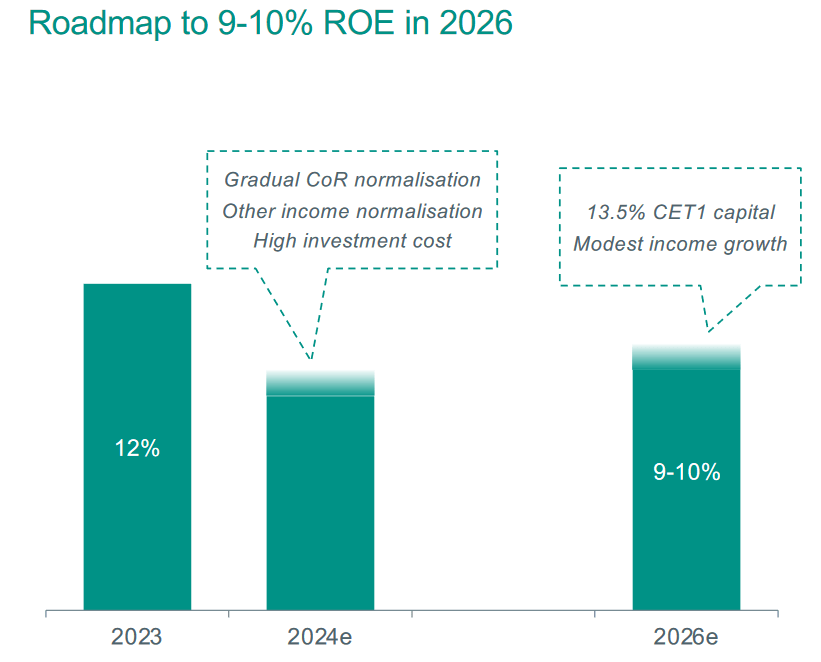

Return on equity is targeted at about 9-10% in 2026. Considering that ABN AMRO has negligible intangible assets, I reckon the 9-10% target applies to tangible equity as well.

Costs are expected to increase by 3.9% in 2024 to about €5.3 billion, and remain broadly flat in 2025 and 2026, with cost-saving initiatives offsetting inflation.

Cost of risk is expected to be 15-20 basis points throughout the cycle.

CET1 target of 13.5% on a fully loaded Basel IV basis. The target includes a management buffer of 225bps. Share buybacks will be considered annually and announced at Q4 results. Dividend policy 50% pay-out of reported net profit, with an interim dividend of 40% of H1 reported net profit.

Return on equity outlook (ABN AMRO Q4 2023 Analyst Presentation)

Given the outlined capital and payout policy, I expect further buybacks to be announced together with the 2024 and 2025 annual results.

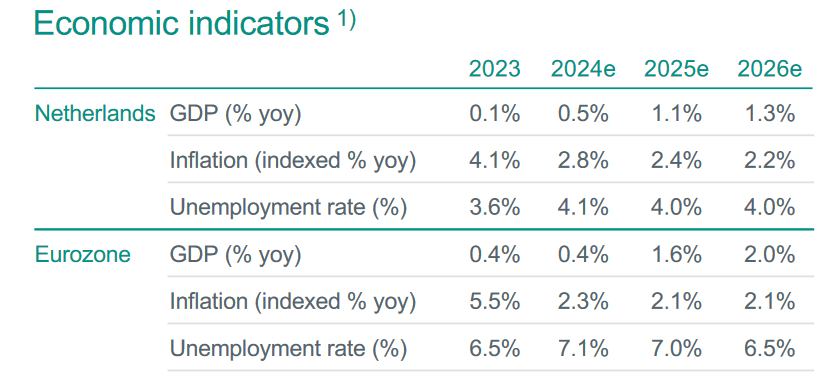

The European economy has been flirting with recessionary readings in recent quarters. ABN AMRO expects the Dutch and Eurozone economies to accelerate in the 2024-2026 period, boosted by easing financial conditions by the ECB:

Macro forecast (ABN AMRO Q4 2023 Analyst Presentation)

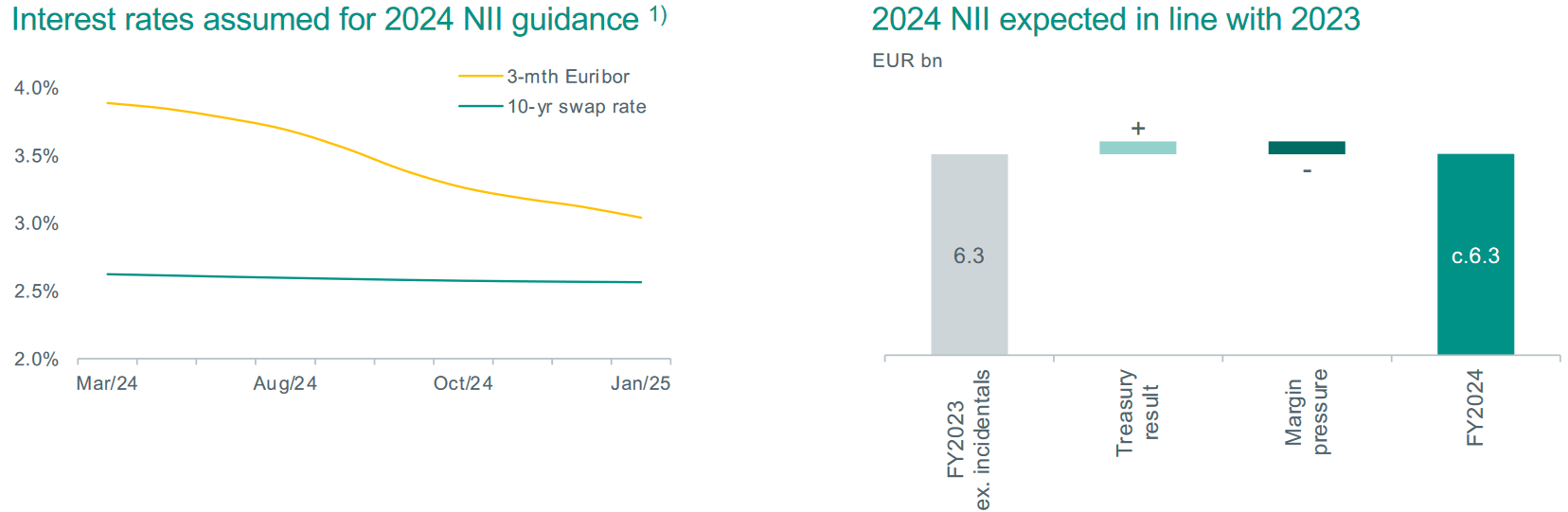

ABN AMRO expects the rate on the ECB deposit facility to be 2.75% in December 2024, with the result on the bank's replicating portfolio offsetting margin pressures, helping keep net interest income stable in 2024:

2024 Interest rate and NII outlook (ABN AMRO Q4 2023 Analyst Presentation)

ABN AMRO Bank N.V. delivered 12.2% ROE in 2023 thanks to strong NII and provision releases, which speak of the quality of its lending book given the sluggish performance of the Dutch and Eurozone economies. While normalization in credit costs is expected over the 2024-2026 period, I think the cost of risk will remain subdued and below the 15-20 bps average through-the-cycle range given accelerating economic growth.

ABN AMRO currently trades at just 0.59 times its tangible book compared to 0.85 at its largest peer ING. While the new 9-10% ROE target of ABN AMRO Bank N.V. appears underwhelming, I reckon the smaller Dutch lender will deliver superior investor returns due to more accretive share buybacks and a lower P/E ratio. I estimate ABN AMRO shares are worth around €17.15/share, implying some 14% upside from the current €15 share price. Hence I rank the shares a buy.

Thank you for reading.

Editor's Note: This article discusses one or more securities that do not trade on a major U.S. exchange. Please be aware of the risks associated with these stocks.