Just_Super

Just_Super

As with a lot of auto tech players, indie Semiconductor, Inc. (NASDAQ:INDI) has seen the growth opportunity disappear in the short term. The sector continues to face some inventory digestion issues along with the electric vehicle ("EV") pause, potentially slowing down some of the extra growth opportunities. My investment thesis remains ultra-Bullish on the stock not being priced for the massive opportunity ahead in the auto tech sector.

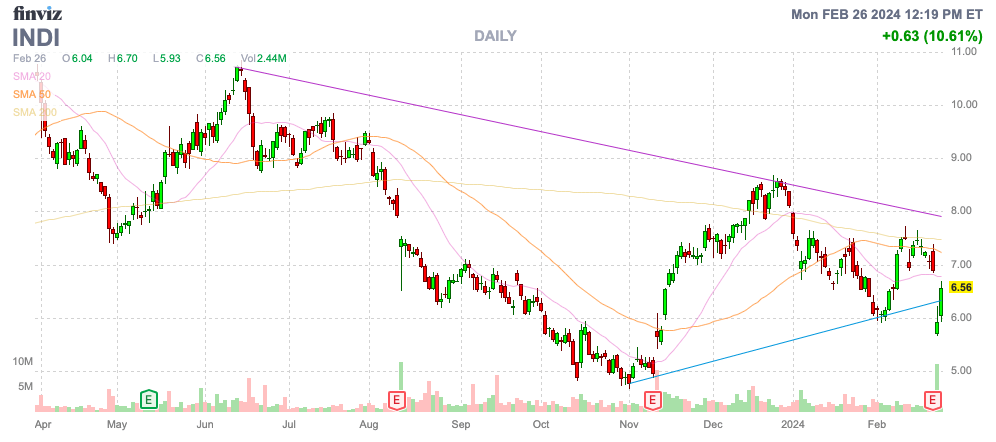

Source: Finviz

As with a lot of SPACs, results haven't seemed to really matter for indie Semiconductor, Inc. The auto tech company just reported a quarter with 112% growth to reach $70.1 million, yet the stock collapsed to near the yearly lows due to missing targets by $2.5 million.

Since going public, indie Semi. has reported soaring sales and massive growth in their strategic backlog. The stock hasn't responded despite regularly trading above $10 back in 2021, when quarterly sales were just topping $10 million and the company just topped $70 million, for 6 fold growth.

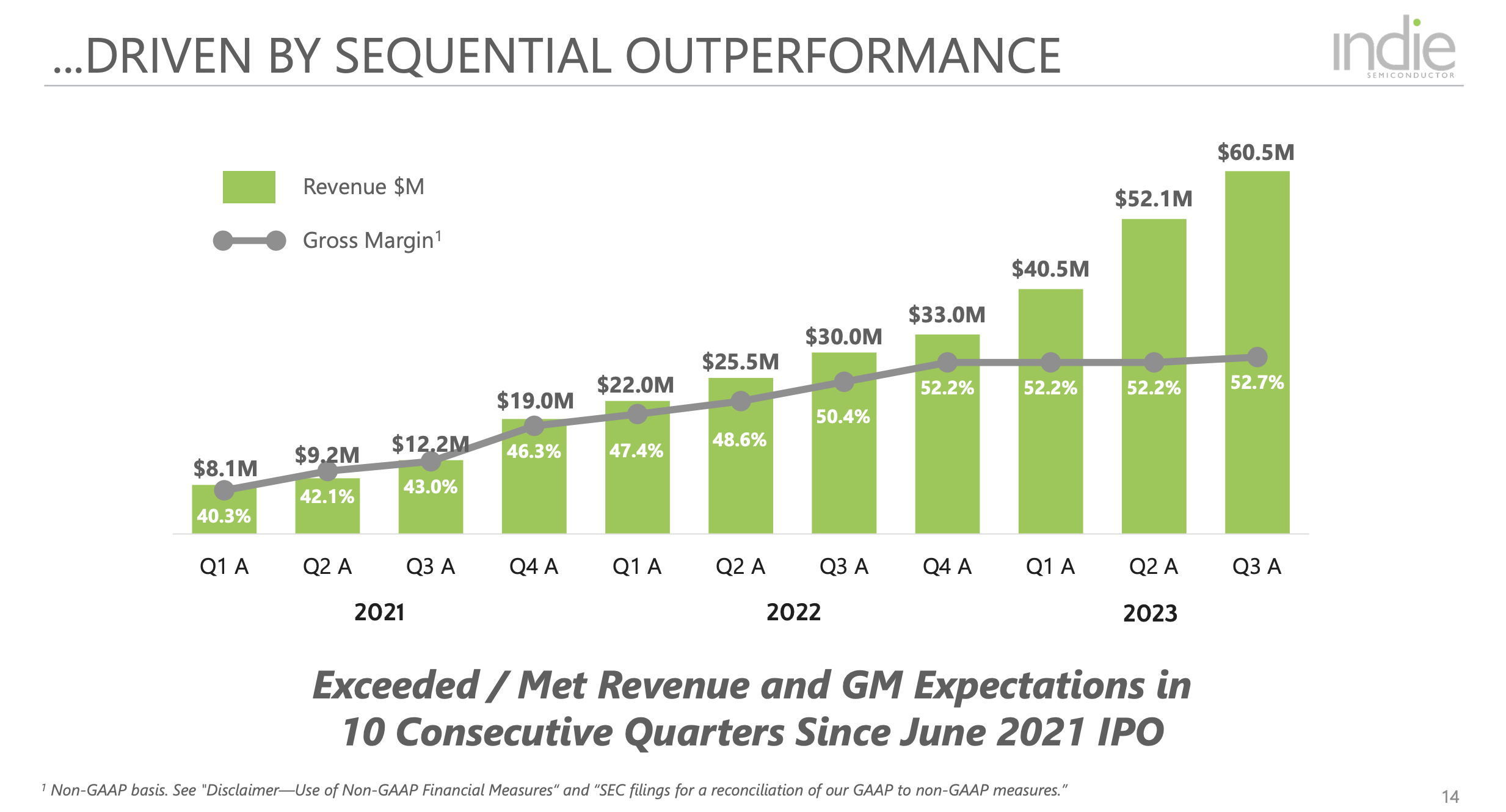

Source: indie Semi. Q4'23 presentation

The major problem with most SPACs is the lack of confidence in corporate guidance regarding long-term financial targets. indie Semi. guided to Q1 '24 revenues of only $56.1 million, but the company discussed a massive growth opportunity in the years ahead.

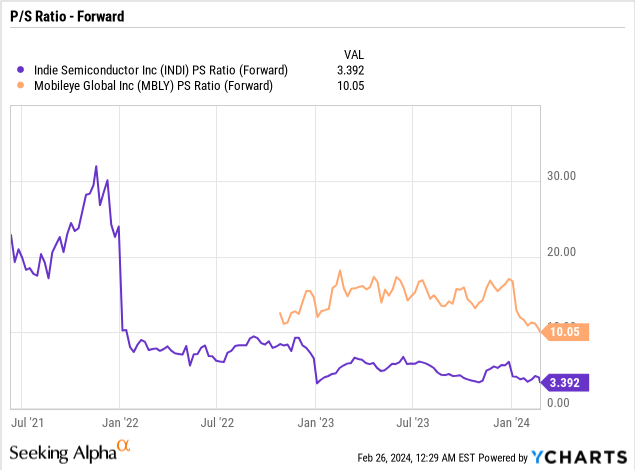

The auto tech company reported numerous quarters with over 100% growth rates, but with the momentum suddenly coming to a stop similar to the inventory digestion issues at Mobileye Global (MBLY). The only major difference is that MBLY stock trades at a major premium of 10x forward sales, while indie Semi. now only trades at 3x forward sales.

indie Semi. isn't profitable or cash flow positive yet, so maybe a discount is warranted. The company has a cash balance of $152 million, and the company only guided to a cash burn total of $30x million this year, leaving plenty of cushion if indie Semi. doesn't reach targets this year.

The company originally guided to being profitable in Q4, but some of the slowdown caused indie Semi. to end up reporting a small operating loss of $2.4 million. The market clearly didn't like the profitability guidance pushed out until the 2H'24 per this statement from the earnings release from CFO Thomas Schiller:

Looking forward, based on our new product pipeline, we anticipate Q1 to be a trough quarter with top line recovery in Q2 and a resumption of outsized sequential growth in Q3 and Q4, yielding a profitability baseline in the second half of this year, ahead of our significant Radar and Vision ramps in 2025.

The odd issue with where indie Semi. trades is the massive strategic backlog that continues to grow. One has to really wonder if the lack of analyst coverage is the prime reason the stock isn't rewarded with the massive backlog.

Everyone knows auto deals are typically for 5 to 7 years, but a lot of the SPAC auto tech companies aren't rewarded for large backlogs. In the case of indie Semi., the company only has a few analysts covering the stock, with just 5 participating on the Q4 '23 earnings call.

The company has reported the following massive increases in the strategic backlog:

The stock currently has a market cap of just above $1 billion despite the backlog topping $6 billion. Management discussed some developments on the earnings call highlighting how the opportunity in auto tech is only growing as follows:

While we navigate automotive industry weakness in the short-term, stemming from rising interest rates, slowing in-market car sales, decelerating consumer transition to semiconductor content-rich electric vehicles, and inventory rebalancing across the automotive industry, our design win momentum has continued unabated and reinforces our confidence in indie’s business model.

indie Semi. even discussed an OEM that canceled an ADAS program in the short term, but replaced it with higher revenue opportunities in the medium term. The long term financial picture doesn't appear altered one bit.

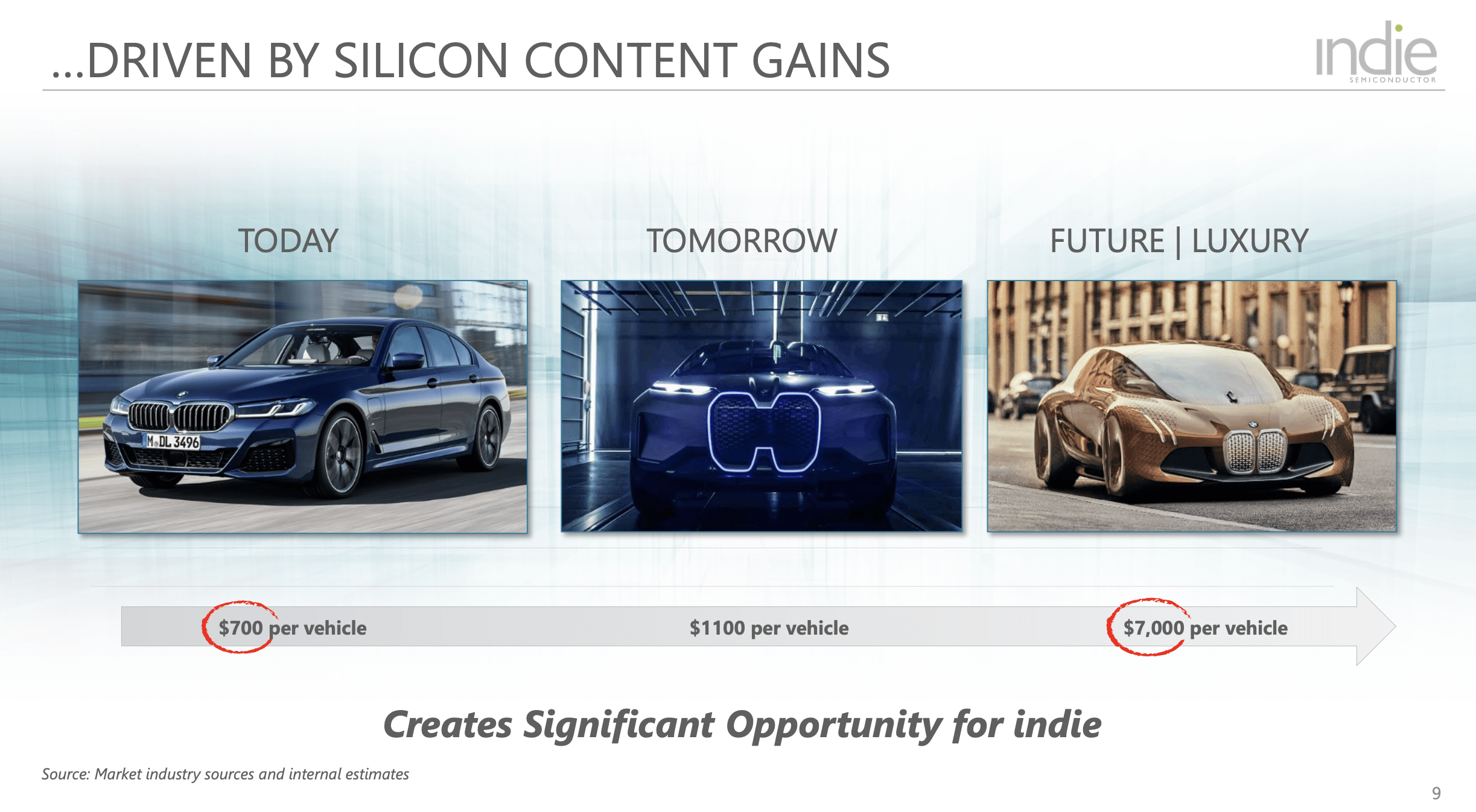

As is the case with auto tech, vehicles are only increasingly moving to more advanced ADAS and autonomous technologies via Lidar, Radar and Vision. The only major question is when indie Semi. sees the major backlog turn into actual production deals and revenues with silicon content per vehicle set to soar 10x by the time cars are fully electric with autonomous driving and advanced cabin features.

Source: indie Semi. Q4'23 presentation

As with most auto tech companies, the large revenue ramp is only around the corner. With indie Semi., the market already got to see years of 100% growth as a public company and investors still appear to illogically question the opportunity ahead.

The key investor takeaway is that Mobileye highlights the valuation an auto tech firm can obtain when the market has confidence even despite the recent major warning. indie Semiconductor, Inc. appears the far better play here due to valuation and years of execution prior to the current slowdown, which would normally provide investor confidence.