HeliRy

HeliRy

Imperial Petroleum (NASDAQ:IMPP) is a spin-off of StealthGas (GASS). Its fleet initially had four tankers. The current IMPP fleet includes five product tankers, two crude oil tankers, and two dry bulk carriers. Fleet's average age is 14.6 years. IMPP has zero outstanding debt. Like GASS, Harry Vafias is the company’s CEO and the major shareholder with a 64.2% stake in the company.

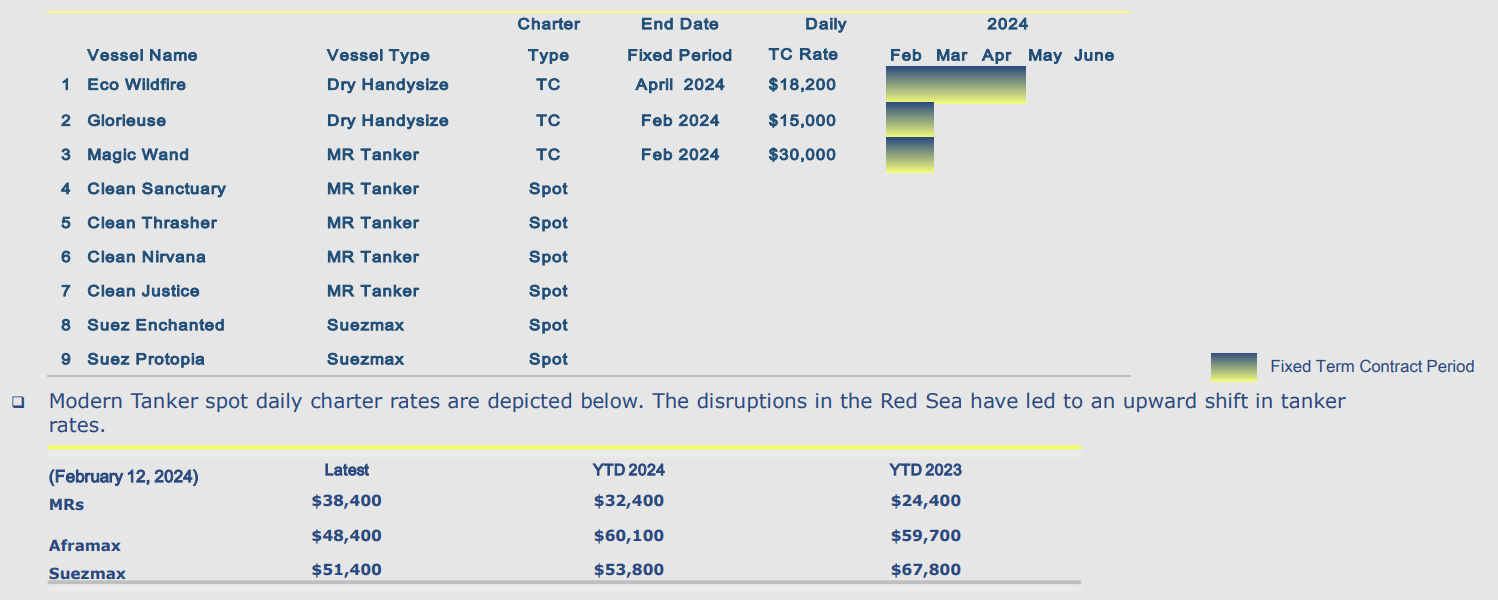

Last Friday again delivered exciting news for tanker stocks. Another set of sanctions on Russian entities was announced after the market closure. In the list is included Sovcomflot, the largest Russian tanker company. After the Red Sea crisis and the Panama Canal drought, this is the third event that may boost tanker day rates.

IMPP trades at 23% P/NAV and below its cash net of total liabilities. Compared to similar-sized shipping companies, Top Ships (TOPS) and Pyxis Tankers (PXS), IMPP is also cheap. The company offers preferred shares with an attractive dividend yield, at 10.0% at the current stock price.

IMPP has five MR product tankers, two Suezmax crude oil tankers, and 2 Handysize dry bulk carriers. The company’s average fleet age is 14.6 years. The table below shows the fleet employment status.

IMPP 4Q23 presentation

Dry bulk carriers and one of the MRs, Magic Wand, are employed under time charters. The charters end in April 2024 and February 2024, respectively. The remaining vessels are employed under spot contracts.

In December 2023, the company announced its plans to acquire two tankers, a 2009-built Aframax Stealth Haralambos and a 2008-built product tanker Aquadisiac. The total purchase price is $71 million. The delivery is expected at the end of January 2024. The tankers will come with a charter free.

On February 13, IMPP reported its 4Q23 report.

IMPP 4Q23 presentation

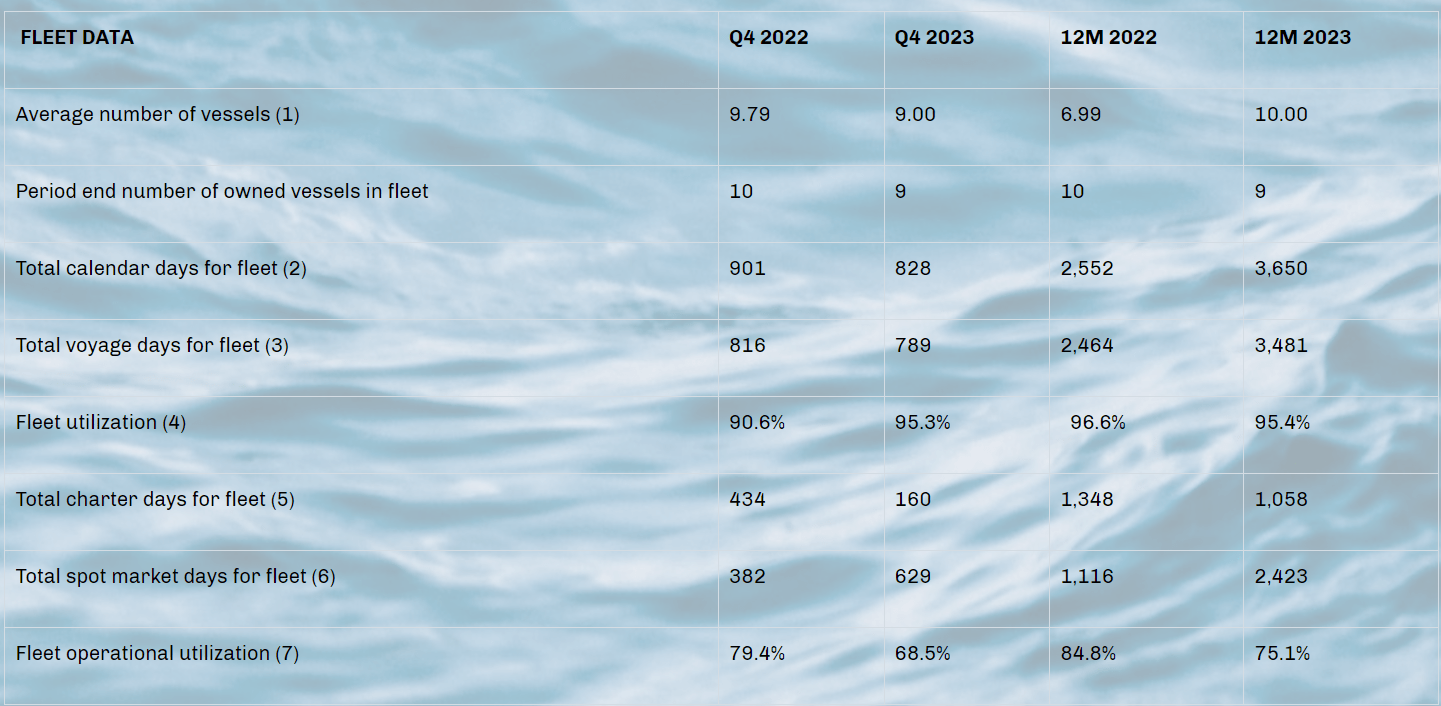

76% of the fleet calendar days, 629 days, were contacted under spot agreements. In 4Q22, the company’s fleet operational utilization rate was 79.4%. IMPP owned ten vessels in 4Q222, compared to nine in 4Q23. The company sold the 2010-built Aframax tanker Stealth Berana in 2Q23 for $43 million. FY2023 fleet operational utilization rate is 75.1%, compared to 84.8% FY2022.

The table below shows the IMPP income statement for 4Q23 and FY2023.

IMPP 4Q23 presentation

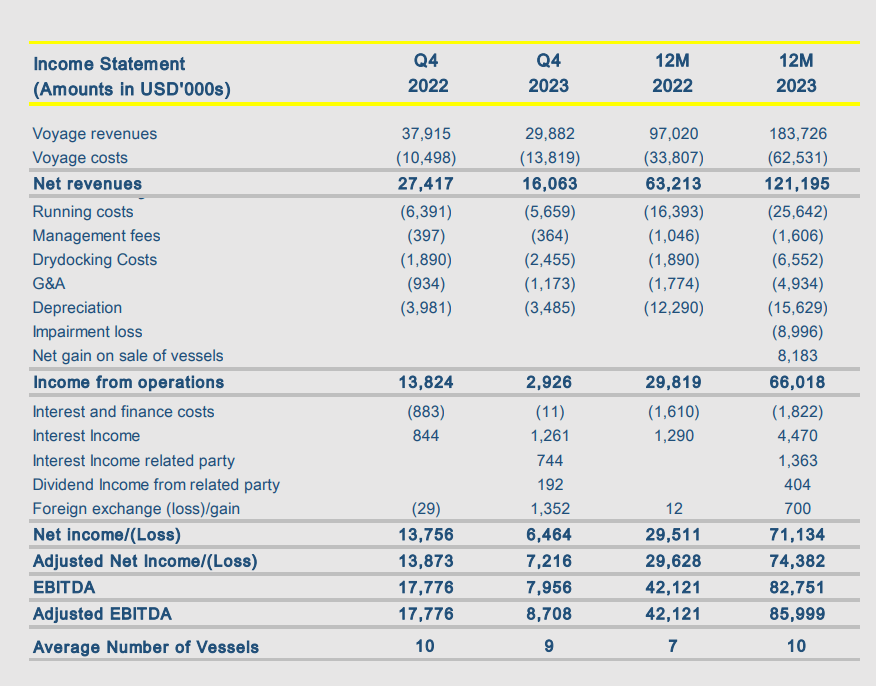

In 4Q23, the company generated $29.8 million in revenue, $8.1 million lower than in 4Q22. Voyage costs increased by $3.3 million to $13.8 million over the same period. The major drivers were higher bunker costs and port tariffs. The reason is that more company ships are employed under spot charters. Drydocking costs increased YoY by $0.56 million, reaching $2.45 million in 4Q23. Two company vessels underwent drydocking for the period, one of the handysize bulkers and Suezmax crude oil tankers.

4Q23 IMPP delivered $2.9 million operating income, $10.9 million lower than in 4Q22. Over the same period, the company reduced its interest and financing costs to almost zero. In 4Q23, IMPP had no outstanding debt. YoY IMPP’s interest income grew to $1.2 million due to a higher amount of funds being deposited and rising interest rates. IMPP delivered $6.5 million net income in 4Q23, $7.3 million lower than 4Q22.

FY23 IMPP realized $183 million in voyage revenue, an 88% increase compared to FY22 due to increased fleet size by three vessels and more robust market conditions. Voyage costs have doubled from $33 million in 2022 to $62.5 million in 2023 due to a higher percentage of the fleet employed under spot contracts. Operating expenses increased from $16.4 million in 2022 to $25.6 million in 2023. The main reason is the higher average number of vessels. In FY23, three of the company’s product tankers, one Suezmax, and two dry bulk carriers underwent drydock, resulting in higher YoY drydock costs of $6.55 million for 2023. FY23 IMPP delivered a $66 million operating profit, $36.2 million higher than FY22.

Interest income grew by 248% due to $1.4 million accrued income related to the Berana sale and higher interest rates. In 2Q23, the company repaid all its outstanding debt, resulting in higher interest expenses compared to 2022. IMPP realized $71.2 net income and $74.3 million adjusted net income in 2023, resulting in $3.39 EPS, compared to $2.89 EPS FY22.

IMPP paid its debts in 2023, so the company has zero outstanding debt.

Koyfin

The company delivers robust liquidity, $79.5 million LTM operating cash flow, and $66.8 million operating income. Besides that, IMPP generates positive net interest expenses at $4.9 million due to zero outstanding debt and increased deposited funds.

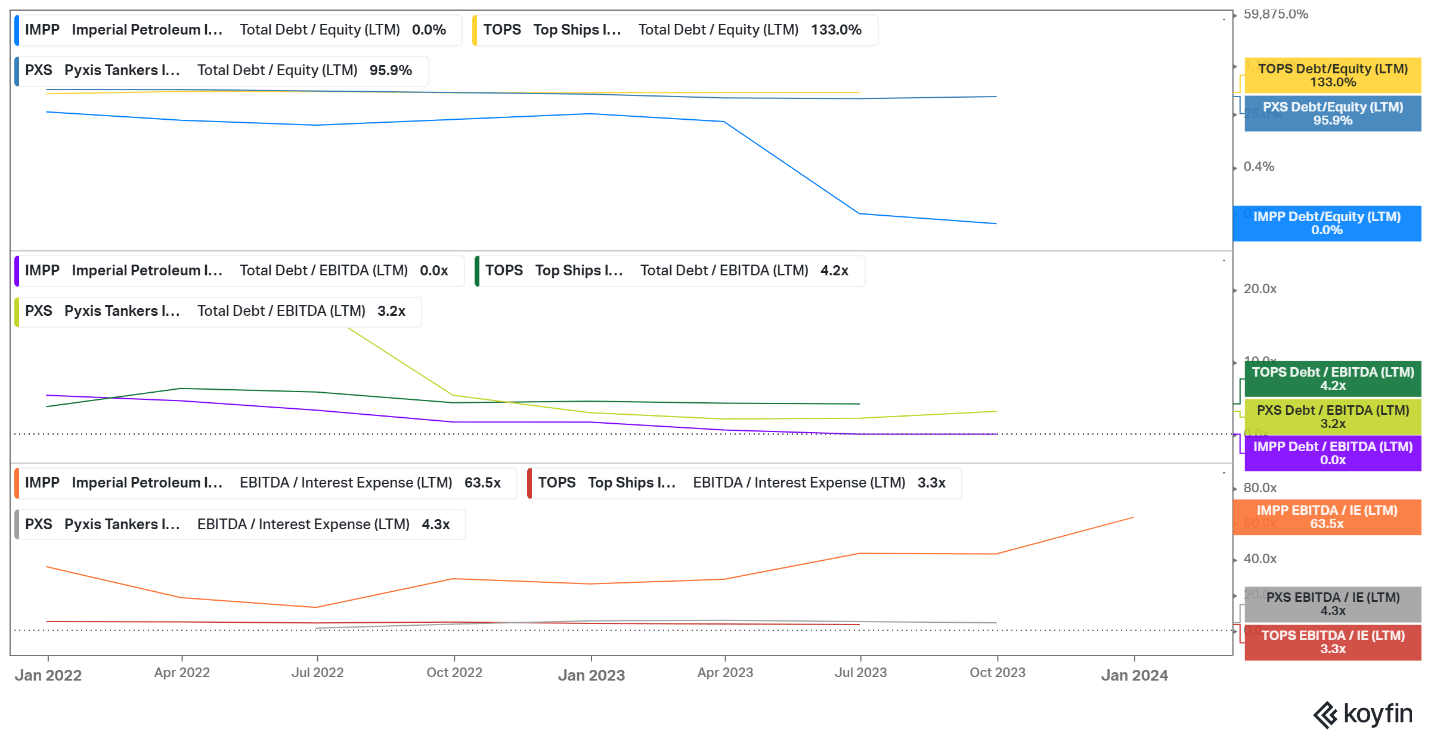

The graph below compares IMPP, Top Ships, and Pyxis Tankers solvency and liquidity metrics. All figures are LTM.

Koyfin

IMPP is the undisputable leader with zero outstanding debt. TOPS is the most leveraged with 133% Total Debt/Equity, 4.2 Total Debt/EBITDA, and 3.3 EBITDA/Interest expenses. However, we must consider TOPS fleet quality, ten tankers (3xMRs, 5xSuezmaxes,2xVLCCs) with an average age of 3.5 years, all built by Hyundai Heavy Industries. PXS fleet is 9.6 years old and consists of three product tankers, MR2, and two bulk carriers, one Kamsarmax and one Ultramax. Despite having higher leverage, TOPS scores 32% LTV, lower than PXS 50% LTV. IMPP has zero LTV, since the company repaid its debts in 2023.

The following chart compares IMPP, TOPS, and PXS margins and returns. All figures are LTM.

Koyfin

TOPS new fleet pays off, delivering superior margins compared to IMPP and PXS. Conversely, the old fleet of IMPP scores the lowest figures in the group. An aging fleet implies higher operational costs due to more frequent maintenance and unexpected breakdowns, resulting in extended downtime. The result is lower margins.

IMPP has 795,878 Series A preferred shares (IMPPP) outstanding as of December 14, 2023, with an 8.75% dividend yield. At the current share price, IMPP preferred units deliver a 10.0% TTM yield. On December 14, 2023, the company announced $0.546/share dividends on its series A preferred shares. For comparison, Pyxis Tankers preferred units (PXSAP) come with an 8.0% TTM yield.

In December 2023, the company announced that the holder, Flawless Management, had converted 13,875 Series C convertible shares of 795,878 into 6.9 million common stocks. In December 2023, IMPP announced the $10 million repurchase program of its common stocks.

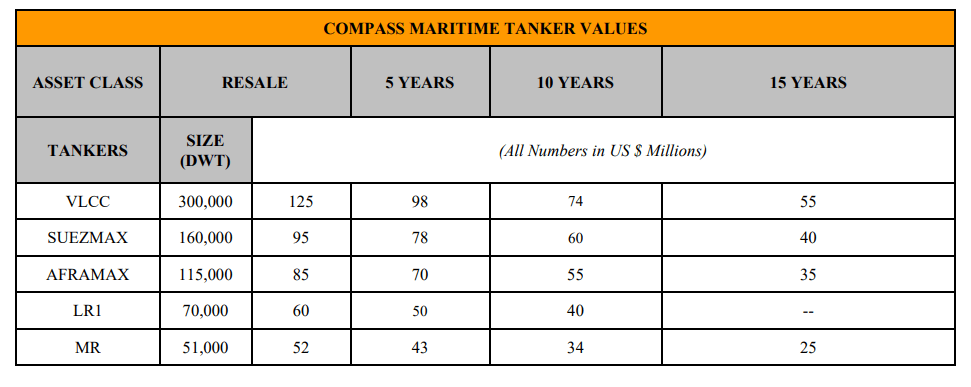

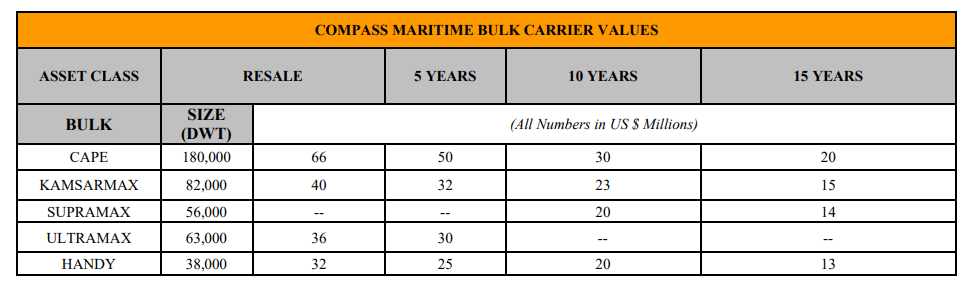

To value the IMPP, I use data from the last Compass Maritime report.

Compass Maritime Compass Maritime

The company owns five MRs at an average age of 16.0 years. Using a 5% annual discount, the value of a 16-year-old MR tanker is $23.8 million. So, the IMPP MR fleet replacement cost is $119 million. IMPP owns two Suezmax tankers at an average age of 16.5 years. Using a 5% annual discount, I obtained $37.1 million for a 16.5-year-old Suezmax. Hence, IMPP Suezmax replacement costs are $74.2 million. The company owns two Handysize bulk carriers at an average age of 11.5 years. Discounting the price of ten years of the vessel by a 5% depreciation rate, I obtain an $18.6 million cost per ship. IMPP bulk carries replacement cost is $37.2 million.

Inputs for the IMPP equation are:

IMPP's Net Asset value is $399 million based on the above inputs.

IMPP's market capitalization is $91.9 million, while its net asset value is $399 million. Hence, IMPP trades at 23% P/NAV. For reference, PXS trades at 44.6% P/NAV and TOPS at 12% P/NAV. It is worth mentioning that IMPP trades below its cash ($124 million) net of total liabilities ($14.5 million).

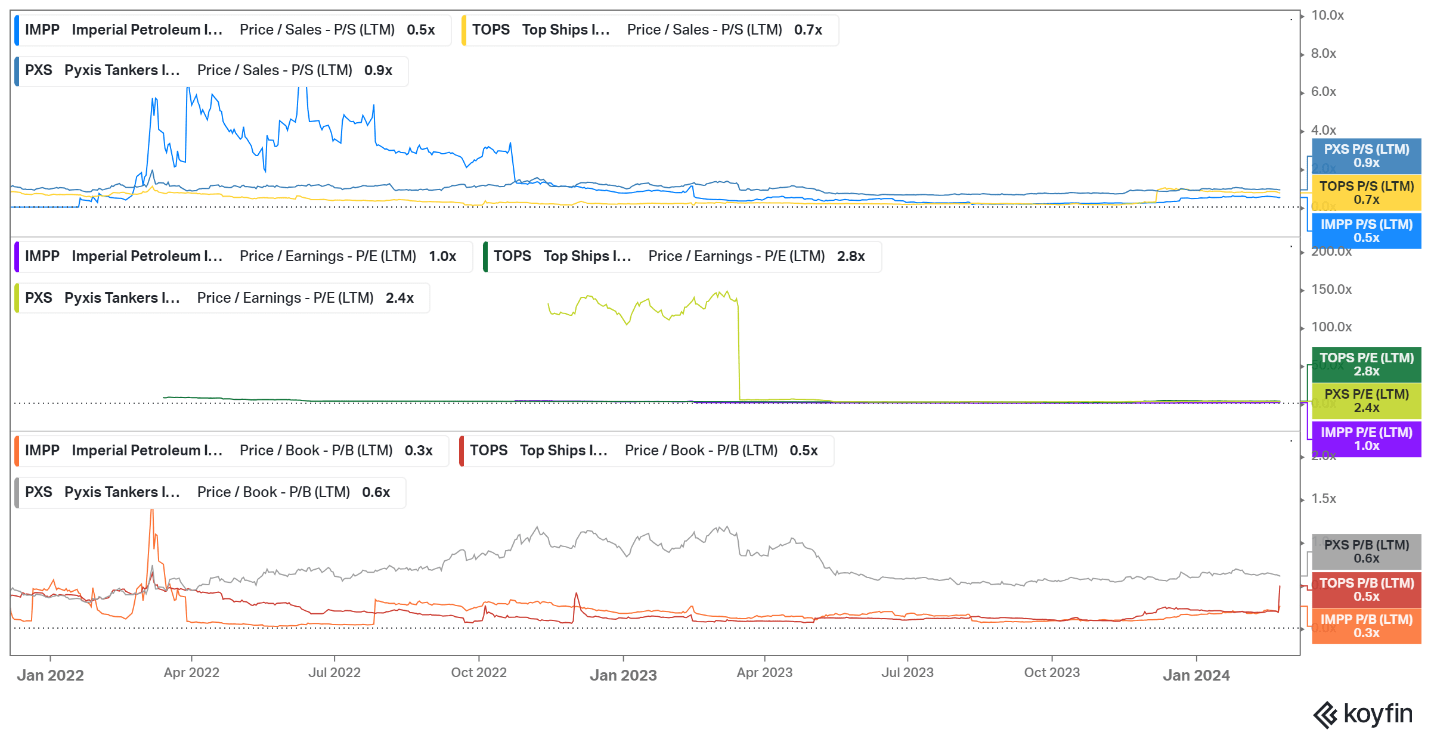

I picked Price-based ratios because IMPP has zero debt, and its cash exceeds its market cap. Hence, its EV is negative. All figures are LTM.

Koyfin

IMPP trades ate the lowest multiples in the group, 0.5 Price/Sales, 1.0 Price/Earnings, and 0.3 Price/Book. I believe the market heavily discounts the aging fleet of IMPP. The older ships have a lot of disadvantages; however, at the present stage of the cycle, I believe IMPP fleet will show its strengths.

IMPP is another shipping stock with preferred units offering an attractive dividend yield. However, the idea comes with a few risks. The first one is the aging fleet. As I pointed out earlier, the older the ships, the higher the operating expenses and the longer the downtime for maintenance and repairs.

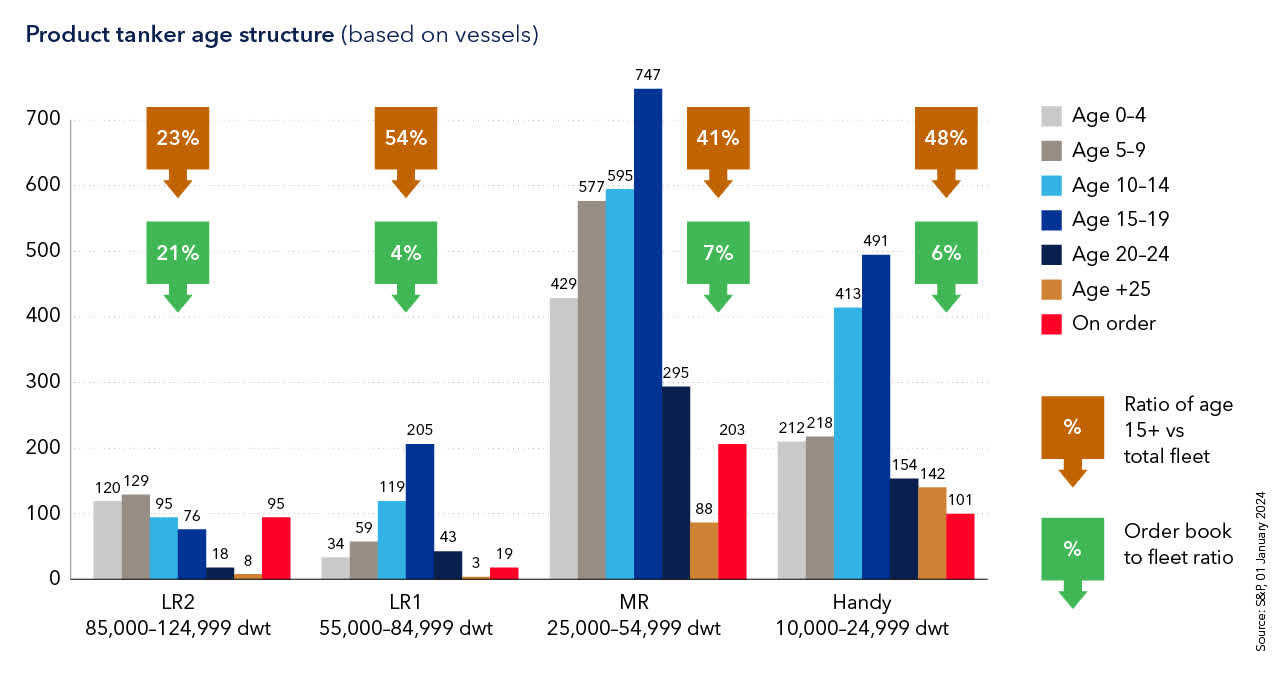

The second risk is the demand for tankers. IMPP MR vessels have an average age of 16 years. The global MR fleet is 15+ years old, representing 41% of all MRs, while MRs' order book is 7%. So, IMPP can still benefit from the expansion part of the tanker cycle.

DNV

Suezmax vessels older than 15 years make up 32% of the total Suezmax fleet. However, the Suezmax order book is 10%. Due to an aging fleet and low order books, I believe the tanker demand will exceed the supply in the coming 12-18 months.

Geopolitics has significantly influenced TCE rates over the last few years. Last Friday, OFAC announced another set of sanctions on Russian legal entities. Among them is Sovcomflot. Sovcom owns 147 vessels, 120 tankers, 12 LPG carriers, two bulk carriers, and 12 specialized vessels. Besides that, the company owns an interest in 14 other ships.

At first glance, the sanction seems the same: Russian tankers must export oil below the price cap of $60/barrel. However, the sanctions stipulate a 45-day grace period to operate for those 14 vessels. Then, they are not allowed to operate.

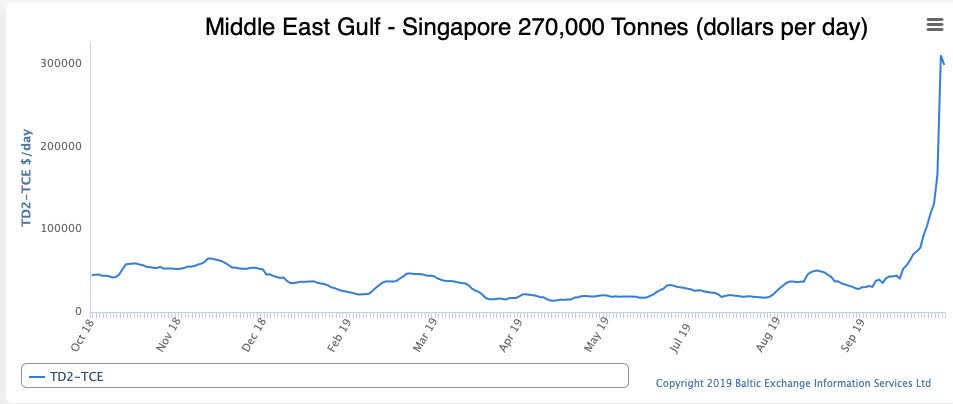

This is not the first time the US has sanctioned foreign shipping companies. In 2019, OFAC sanctioned COSCO. Within a few months, VLCC day rates exploded from $30,000/day to $300,000/day. In the long term, sanctioning those 14 ships might be the first sign for more drastic punitive actions on Sovcom.

Baltic Exchange/Twitter

IMPP does not own VLCCs. However, the Sovcom sanction adds one more constraint on the tanker supply, which may result in rising day rates.

Financially, IMPP is in excellent health with zero outstanding debt. The company has $124 million cash to employ in expanding its fleet. In 2024, IMPP expects the delivery of two vessels, one 2009-built crude oil tanker and one 2008-built product tanker. Buying older ships may play out well at the current stage of the tanker cycle. The reason is if the company orders a new vessel, its delivery will take at least 18-24 months. At that time, the cycle might have already changed direction. Buying old vessels in an inflationary environment has another advantage, too. They benefit from constant revaluation; hence, the company’s NAV keeps rising. The best thing is that IMPP has cash at hand, so there is no need to worry about financing terms.

In conclusion, I like IMPP's clean balance sheet and its focused approach. Preferred units deliver an attractive yield at 10.0% at the current stock price. My verdict is a buy rating.

Editor's Note: This article covers one or more microcap stocks. Please be aware of the risks associated with these stocks.