MF3d

MF3d

I-Mab (NASDAQ:IMAB) Biopharma is a clinical-stage biotech company with a focus on immunotherapies and oncology. The company recently announced that it has signed agreement to divest its assets and business operations in China (the Hangzhou Company) to become a U.S-based biotech company. After the divesting, I-Mab will have a healthy balance sheet with more than $400 million in cash, a pipeline consists of three potential best-in-class clinical stage oncology assets, the potential to receive up to $80 million of cash consideration from its divested China operation, and the right of first negotiations outside of China for the three drugs developed by the China operation. Trading at about 1/3 of net cash value, I-Mab is significantly undervalued with a few call options in the next 2-3 years.

At the peak in 2021, I-Mab’s market cap was $7 billion. Since then, it has lost a whopping 98% of its market value. Obviously something went horrible wrong for the company. It’s important to understand the sequence of events that led to I-Mab’s rise and fall in order to assess the current situation.

I-Mab was once a darling of all Chinese biotech companies because of its differentiated business model and management team. Its founder Dr Zang was a renowned scientist responsible for GSK’s China R&D Center prior to founding I-Mab. Therefore, under Dr Zang’s guidance, while almost all Chinese biotech companies raised capital to develop me-too drugs, I-Mab has been an exception as it focuses on either FIC or BIC biologics that target the global immuno-oncology market. Back in 2020, one of the hottest target in immune-oncology was CD47 and I-Mab had one of the most promising CD47 assets globally. Gilead (GILD) spent $4.9 billion to acquire Forty Seven, whose main asset is magrolimab—the anti-CD47 antibody. I-Mab got a huge boost in September 2020, when I-Mab announced that it has licensed out the non-China commercial rights of its CD47 drug lemzopalimab to AbbVie (ABBV) in a $2 billion deal, which included a $180 million up-front payment.

Right after the AbbVie deal, I-Mab raised $418 million with a consortium of institutional investors

“led by Hillhouse with significant participation by GIC, and also includes certain other leading Asian and U.S. biotech investment funds, such as Avidity Partners, OrbiMed, Octagon Capital Advisors, Invus, Lake Bleu Capital.”

Unfortunately, In January of 2022, Gilead announced that “the U.S. Food and Drug Administration (FDA) has placed a partial clinical hold on studies evaluating the combination of magrolimab plus azacitidine due to an apparent imbalance in investigator-reported suspected unexpected serious adverse reactions (SUSARs) between study arms.” This announcement marked the beginning of demise of the global CD47 asset class. Since then, the global CD47 race has turned into a disaster as bad news emerged one after another.

In August of 2022, AbbVie ended its collaboration with I-Mab on lemzopalimab. Because I-Mab’s most important asset was lemzopalimab, investors dumped I-Mab’s shares. At the same time, I-Mab went through a management shake-up and a delisting threat. Its market cap evaporated by 98% from $7 billion to $180 million.

The bears have completely written off I-Mab. However, recent events suggest that I-Mab may be at a turning point, which I’ll explain in details below.

On Feb. 7, 2024, I-Mab announced the divesting of its China assets. According to the press release,

"This agreement to divest our operations in China marks an important milestone for I-Mab in bringing a greater focus on the U.S. and ex-China markets," said Raj Kannan, Director and Chief Executive Officer of I-Mab. "Importantly, we believe that this transaction allows us to reduce significant operational costs and enables us to reallocate our capital on current key priorities and new potential opportunities in further strengthening our portfolio while maintaining a strong balance sheet."

Importantly, the divesting will also help the company to extinguish an existing repurchase obligations owned by its wholly owned subsidiary to certain participating shareholders in the amount of approximately $183 million by transferring I-Mab’s equity interests in the divested China operation. After the divesting, I-Mab’s repurchase obligation to non-participating shareholders is expected to range from $30 million to $35 million.

The divesting will also provide I-Mab with up to $80 million of cash consideration,

“contingent upon the Hangzhou Company group's achievement of certain future regulatory and sales-based milestone events. I-Mab will also retain the right of first negotiation outside of Greater China related to three future investigational new drug candidates.”

Among the assets owned by the China operation (the Hangzhou Company group), the most promising is Eftansomatropin Alfa, a differentiated long-acting human growth hormone on track to a planned BLA filing in China in 2024.

China’s human growth hormone market is currently dominated by GeneScience Pharmaceutical (GenSci) which is the subsidiary of the publicly-listed company Changchun High-Tech Industries. According to BaiPharm, “Gene Science’s market share in China reached 76.13% in 2020, followed by Anhui Anke Biotechnology (12.48%) and Shanghai United Cell Biotechnology (8.81%). Other Chinese companies (e.g., Zhongshan Sinobioway Hygene Biomedicine) and two international companies (Novo Nordisk and LG Chem) altogether accounted for about 3% market share.”

GenSci’s revenue from human growth hormone in 2022 was RMB 10.2 billion, or roughly $1.4 billion. Once Eftansomatropin Alfa is approved in China, the Hangzhou Company group will partner with Hubei Jumpcan Pharmaceutical to sell it across China. Hubei Jumpcan Pharmaceutical is a leading pediatrics service provider in China with a great track record and a very wide network. By partnering with Hubei Jumpcan Pharmaceutical, the Hangzhou Company group can leverage Jumpcan’s network of pediatrics centers to sell Eftansomatropin Alfa. I-Mab will also benefit through the contingent payment with the Hangzhou Company group if Eftansomatropin Alfa turns out to be successful.

To sum up, the China divesting will greatly improve I-Mab’s balance sheet while gives I-Mab the upside call option if the divested China operation becomes hugely successful in the future.

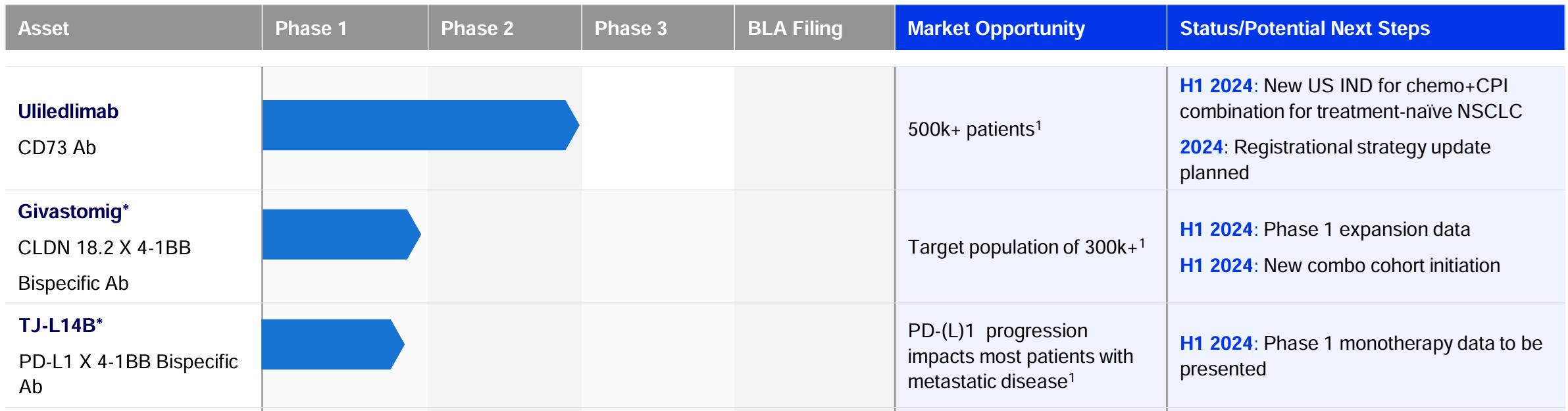

After the China divesting, I-Mab’s core assets will consist of three global Immuno-Oncology programs.

I-Mab investor presentation

Of the three Immuno-Oncology assets, Givastomig and TJ-L14B are both still in Phase 1, therefore, too early to evaluate.

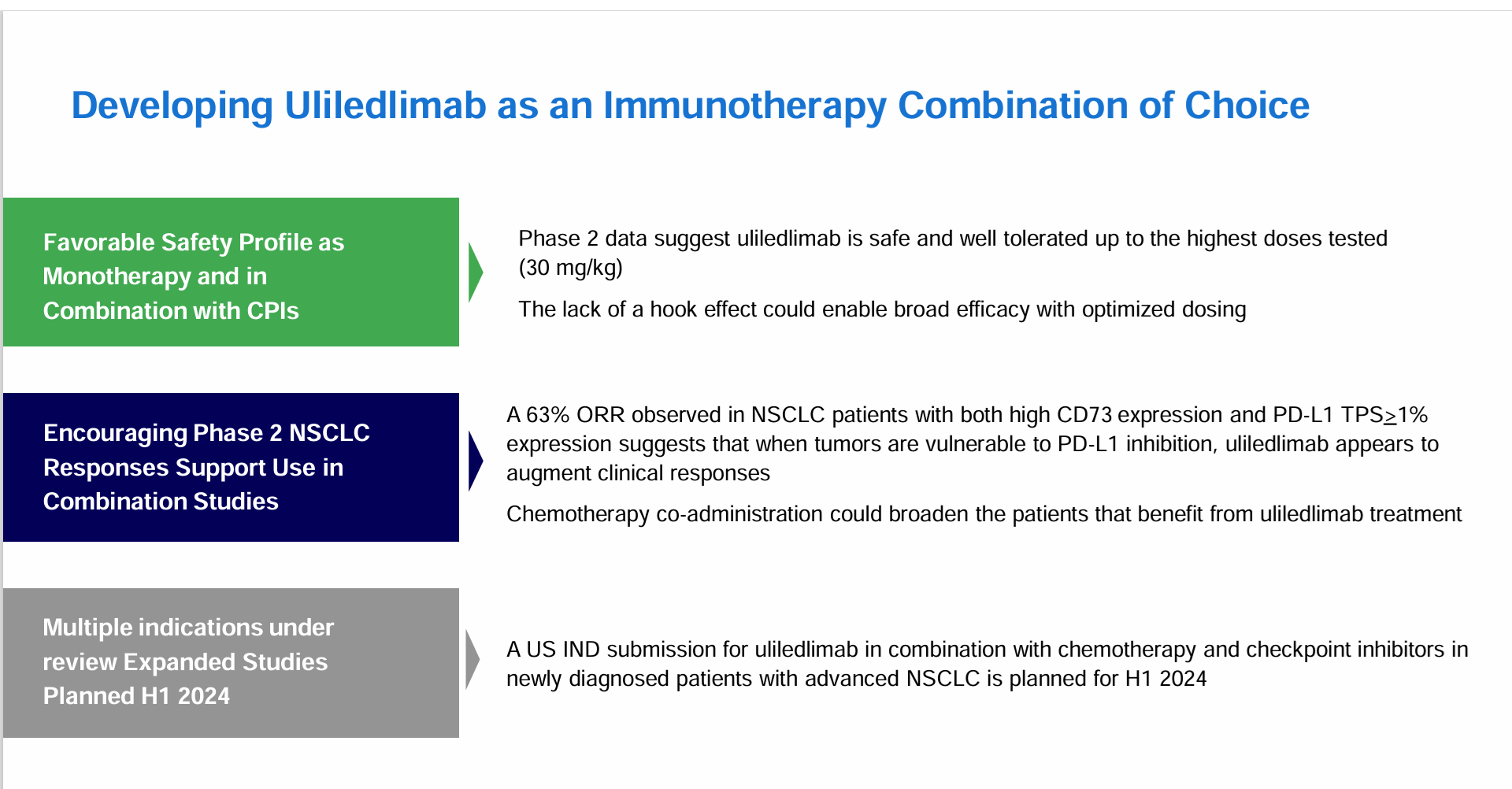

Uliledlimab is a phase 2 CD73Ab, a rate-limiting enzyme in the adenosine immunosuppression pathway. During the Q2 2023 earnings call, management explained uliledlimab and provided an update on the progress of uliledlimab clinical trials.

Speaking of uliledlimab’s differentiation, I-Mab’s CMO John Hayslip explained that

“uliledlimab is differentiated by design to avoid hook effect biology, which is a potential liability of other competitor drugs in development. Simply put, the hook effect may prevent other drugs from achieving complete inhibition of enzyme function. The uliledlimab is designed to allow up to 100% inhibition due to its unique functionality.”

I-Mab investor presentation

Additionally, uliledlimab has showed encouraging Phase 2 NSCLC clinical trial data with “a 63% ORR observed in NSCLC patients with both high CD73 expression and PD-L1 TPS> 1% expression suggests that when tumors are vulnerable to PD-L1 inhibition, uliledlimab appears to augment clinical responses”. Furthermore, “chemotherapy co-administration could broaden the patients that benefit from uliledlimab treatment”. I-Mab plans to submit an IND for uliledlimab in combination with chemotherapy and checkpoint inhibitor (toripalimab) in newly diagnosed patients with advanced NSCLC in H1 2024.

Besides NSCLC, I-Mab will also continue to “enroll patients with previously treated ovarian cancer to the combination regimen of uliledlimab and toripalimab and expect to report preliminary results in 2024 for this Phase 2 cohort of patients”. I-Mab’s management hopes that the combination of CD73 and chemotherapy can benefit a broader group of patients, regardless of pretreatment CD73 expression.

As of the latest report period, which is June 30,2023, I-Mab has cash and cash equivalent of $406 million, short-term borrowing of $4.1 million. The company’s net cash position is almost $400 million. This is down from $734 million at the peak in 2020 due to I-Mab’s heavy spending on the pipeline assets.

Management estimated the cash burn rate during the H1 2022 earnings call:

“The actual cash burn in the first half was around $85 million, and we expect to reduce the cash burn in the second half, which is the implementation of our cost and expenses initiatives just discussed. The annual cash burn rate, we expect to range that – in the range of $150 million to $160 million for 2022.

For next year 2023, we will continue to execute on our prioritization strategy and the expense initiatives including facility consolidation and projects prioritization, and the headcount – we need to further reduce the operating cash burn to around $100 million going forward.”

However, with the divesting of China operation, it is almost guaranteed that the cash burn rate will come down in the future. Although management has not provided guidance in terms of the cash burn rate after the divesting. As I-Mab's assets were essentially half China and half U.S before the divesting and most of I-Mab's operational stuffs were based in China, I expect the cash burn rate to decrease from the current $160 million run-rate to $50-80 million going forward.

The biggest risk related to I-Mab’s business is the failure of its remaining US pipeline assets, especially uliledlimab. As a clinical-stage biotech company, I-Mab has not gained any FDA approval so far. Although uliledlimab has showed encouraging Phase 2 data, plenty of questions remain in future trials.

Another risk related to I-Mab’s operation is the frequent of change of management team. During the two years, I-Mab has changed both its CEO and CFO multiple times. Obviously an unstable management team is not something investors want to see.

Lastly, there’s still uncertainty with I-Mab’s divesting of its China business. Non-participating investors may sue I-Mab for the equity interest transfer from I-Mab to I-Mab’s Hong Kong subsidiary. Although I-Mab has taken the lawsuit into consideration when signing the agreement, the actual claims in legal proceedings may exceed the company’s expectations.

After divesting its China operation, I-Mab has transformed from a China-based biotech company to a U.S-based biotech company. I-Mab is trading at 1/3 of its approximate $400 million net cash on the balance sheet currently. At the current valuation, I-Mab is a rare net-net play with multiple upside options. Therefore, I give I-Mab a “buy” rating.