AntonioSolano/iStock via Getty Images

AntonioSolano/iStock via Getty Images

REITs are often perceived to be boring income investments that are only suitable for retirees.

But the reality is very different

The REIT (VNQ) market is vast and versatile with about 1,000 companies worldwide and there is truly something for everyone.

There are REITs that are great for conservative income-oriented investors. A good example would be Realty Income (O).

Then there are REITs that are better suited for growth investors. They have consistently outperformed the broader market (SPY) and a good example here would be Prologis (PLD).

Finally, there are some REITs that are best suited for aggressive investors who are looking for deep value situations with significant upside potential.

The focus of today's article will be on such REITs.

Now, let me make it clear here that these REITs are extremely risky and some of them may even go bankrupt. There are typically some good reasons why they are so heavily discounted and offer such huge upside potential.

But in select cases, the potential reward outweighs the risks, and the risk-to-reward may be compelling for more aggressive investors.

In what follows, I will highlight two speculative REITs that are so cheap that they could triple in value in a short amount of time if they manage to survive. On the flip side, both of these could also be a 0 if more risk factors play out.

Branicks (BRNK) is a German real estate investment firm that owns mostly industrial properties, and it also operates an asset management business that earns fees.

Their latest net asset value is estimated to be €21.19 per share and yet, their share price is just €1.2, representing a ~95% discount. Such a valuation only makes sense if there is a high risk of bankruptcy, but if you can remove or significantly reduce that risk, then the share price should recover very significantly already in the near term.

So what are the odds?

Before we answer this question, let’s first take a step back and review how Branicks got into this situation.

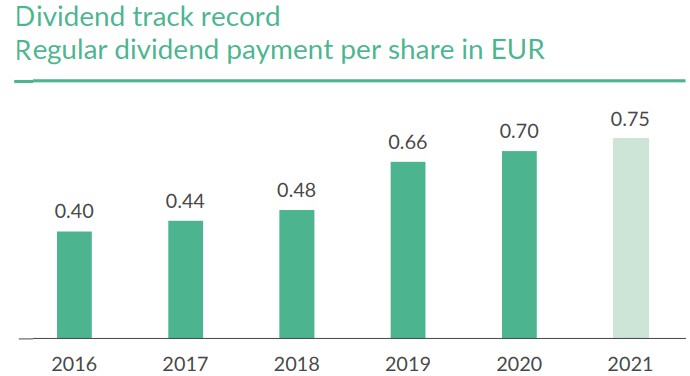

Up until the pandemic, Branicks was doing very well. The company had managed to grow its cash flow and dividend by ~15% annually and its share price had surged to new highs:

Branicks Google

But then came the first black swan.

The pandemic hurt Branicks because it was heavily invested in office buildings back then. It stopped all transaction activity, which greatly reduced its current cash flow and also its growth rate. Remember that Branicks is not just a landlord, but also an asset manager that earns fees for managing capital for others. If there are no transactions, it won’t earn transaction fees and it also won’t be able to grow its assets under management.

This prompted Branicks to make a bold move into the industrial property sector. No one wanted to invest in offices in the post-pandemic world so Branicks needed to rapidly reinvest itself to return to growth.

It did so by acquiring a major industrial landlord/asset manager called VIB.

This acquisition was risky because it significantly increased its leverage in the near, but it could turn out to be very lucrative over the long run because it rapidly transformed Branicks from a fairly small office landlord/asset manager into a much bigger and better-diversified landlord/asset manager with primarily industrial properties.

The plan was to then sell some of the industrial properties to reduce the debt and return to growth from there.

But then came another black swan.

Inflation took off and this forced central banks to significantly increase interest rates. This came right after Branicks had taken a lot of short-term debt to close its acquisition.

Making matters even worse… a third black swan hit Branicks.

Russia invaded Ukraine, starting the biggest war on the European continent since the Second World War. This only increased inflation even further and forced central banks to keep hiking interest rates. It again stopped all transaction activity in Germany, derailing the company’s plans to sell assets to reduce debt.

Since then, Branicks has made some progress in selling assets, but not enough to address all of its near-term maturities, and this brings us to today.

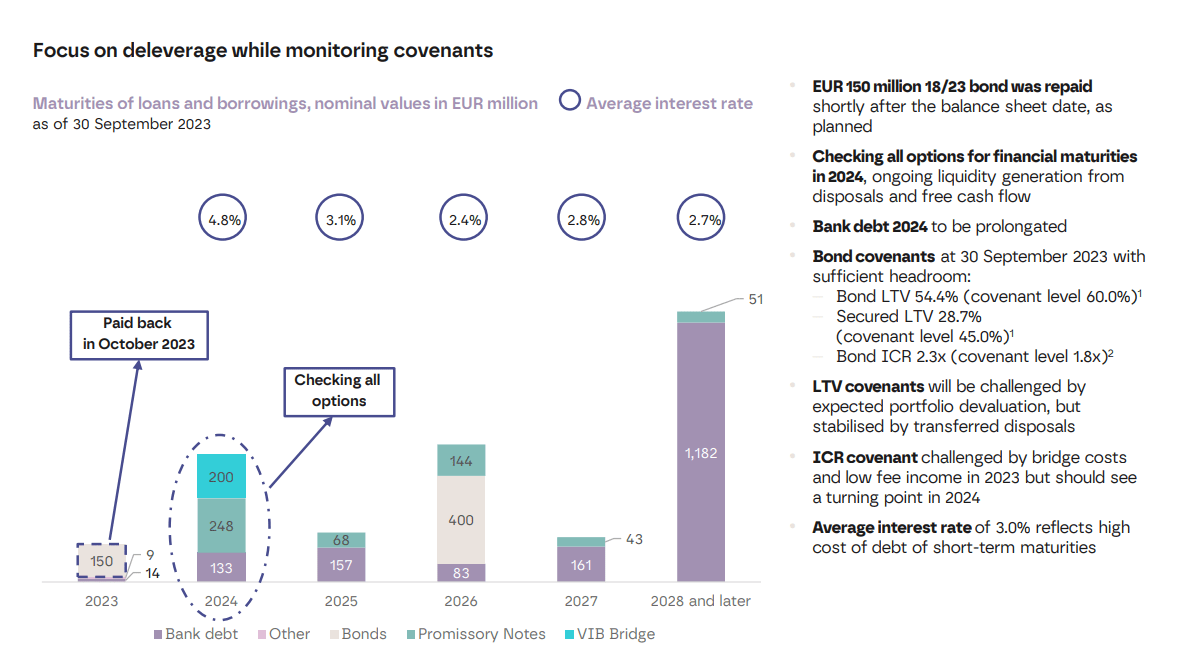

Branicks has its €200 million bridge loan maturing on the 31st of July 2024 as well as its promissory notes of €225 million. There's also another €133 million of bank debt maturing this year, bringing the total to €558 million:

Branicks

That's significant and they don't have nearly enough cash to pay this off as of today. As noted earlier, the plan was to sell assets to pay off some of this near-term debt, but the war in Ukraine, the high inflation, and the surge in interest rates stopped nearly all transaction activity. Moreover, the company is also very close to breaching debt covenants, which increases the risk of bankruptcy even further. Therefore, the risk of bankruptcy has become significant and the market is right to be nervous.

Even then, I continue to think that Branicks has potentially a way out of this mess.

Just recently, they announced that they had entered into negotiations with the lenders of the bridge loan and the promissory notes to extend the maturities and to temporarily suspend some of the lending conditions.

If the lenders refuse and Branicks doesn't manage to sell enough assets or find an alternative solution, this would push the company into default later this year.

But if they accept to extend the debt, Branicks could gain the time that it needs to sell enough assets and pay off this debt.

So what's the most likely? Will they refuse or accept to extend?

While it is far from being certain, I remain optimistic that they will come to a deal because of the following 8 reasons:

Reason #1: This is mainly a temporary liquidity issue, not a solvency issue

Overall, Branicks owns great assets that are generating steadily rising cash flow and its asset management business also has more assets under management than ever before. It is not getting any transaction fees or incentives fees right now because there is no transaction activity in the German property market, but despite that, it was still able to earn $50 million of FFO in what was a very challenging year. Its rents also rose by 7% on average in the last quarter, which is very encouraging.

So in a typical year, Branicks should be able to meet all their obligations including interest payments, salaries, etc. They are earning significant positive cash flow and it is not as if Branicks was begging for more cash from its lenders. It is just that they have significant debt maturities coming their way and they don't have the cash right now due to their inability to sell enough assets in this frozen market.

Under such circumstances, the lenders should be more willing to work with the borrower because extending the loan by another 6-12 months would not materially increase the risks. Branicks is generating significant cash flow from its business and retaining all of it for deleveraging.

Therefore, it is not as if its assets were about to disappear due to large losses.

Branicks simply needs some more time to monetize assets and the lenders would get to earn additional profits if they agreed to extend the debt.

Reason #2: Branicks has made progress selling assets even despite the challenging market conditions

In their most recent announcement, they noted that they had recently sold another €60 million worth of assets, bringing the total to €285 million for 2023. This is not enough, but it still indicates to the lenders that Branicks has valuable assets, is making progress in monetizing them, and may be able to pay off its debt if given enough time.

If they managed to sell €285 million worth of assets in one of the toughest years, it probably means that they will have more success when interest rates head lower and the transaction markets recover. They sold $60 million worth of assets in December alone and there are clear signs that the market is starting to stabilize in Germany.

Reason #3: They finally suspended the dividend to retain significant cash flow for deleveraging

We have long called for a full suspension of the dividend and we blame the management and the board for taking so long to make this decision.

I understand that they were hoping to close a major asset disposition to repay the debt maturities and continue their dividend track record, but this increased risks as they were paying out significant cash flow that could have been used to partially repay the debt.

Well, hopefully, it is not too late. They finally took that difficult step and while the market hates it, it is the right move. Lenders should feel reassured to know that the company is now 100% committed to deleveraging and not paying out dividends until its maturities have been handled. It decreases risks for lenders.

Reason #4: Branicks has already paid off a large portion of its bridge loan as well as other debt, indicating to lenders that they are serious about deleveraging

Branicks has already made some progress in reducing their debt. They paid off €200 million off their bridge loan already in July last year, and they also fully repaid a €150 million bond last October.

These debt repayments show lenders that they are not just talking and making empty promises. They are making real progress in paying back their debt.

Reason #5: Lenders may be reluctant to force a default when it seems that a simple extension could potentially solve the issue

Legendary real estate investor, Barry Sternlicht, recently made an interesting remark about lenders and how they are dealing with the distress in real estate today.

He is the CEO of the private equity giant Starwood so he is constantly dealing with lenders. Here is what he said:

"We were going to give back an office building... and the bank said "well not so fast, if you want, we are going to restructure the loan... we will cut the loan in half... and you will put the money in here and we will take this as a junior note because the banks don't want the assets back. They are not set up to carry these assets. They then have to go hire someone. Do the leasing themselves. It is not their business. They would have rather have a GP hold on the assets and try to work it out.

Right now, we have an unusual situation in the real estate market because everyone is sort of looking at the yield curve and it says that rates will be lower later. Everyone says survive till 2025. Hold on to your assets and sell later." Barry Sternlicht

This seems very relevant to Branicks' situation.

Forcing a bankruptcy could mean shooting themselves in the foot since this could then lead to lengthy and expensive legal battles in court with all the other lenders and stakeholders to decide who gets what. It will then also likely lead to a liquidation of the assets, which would be very challenging in today's market. Even an expert asset manager with the right relationships and incentives is struggling so you can just imagine how complicated it would be for a lender that lacks the operational capabilities.

It could get very messy and most lenders would rather avoid such situations when possible. An easier solution would seem to be to extend the debt by another 6-12 months and demand higher interest rates and/or penalties in exchange to compensate for the additional risk. It could be a win-win for both parties.

Reason #6: Interest rates are expected to head lower later this year and this should lead to a recovery in transaction activity

Barry Sternlicht noted that: "Everyone says survive till 2025. Hold on to your assets and sell later."

That's because interest rates are expected to head lower in the near term and this should lead to a recovery in transaction activity and higher property values.

This could be what ultimately saves Branicks from bankruptcy. If the outlook was for even more rate hikes, it would be an even more complicated story. But since rates are expected to go lower in the near term, it should get easier to monetize assets in 2024.

Reason #7: There was a recent insider purchase

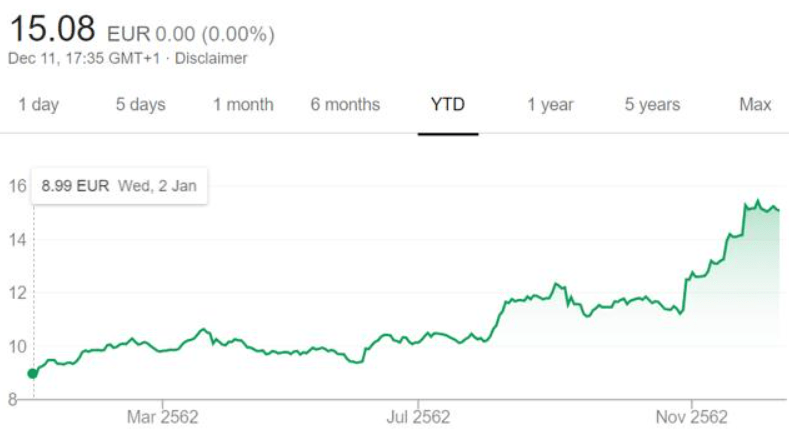

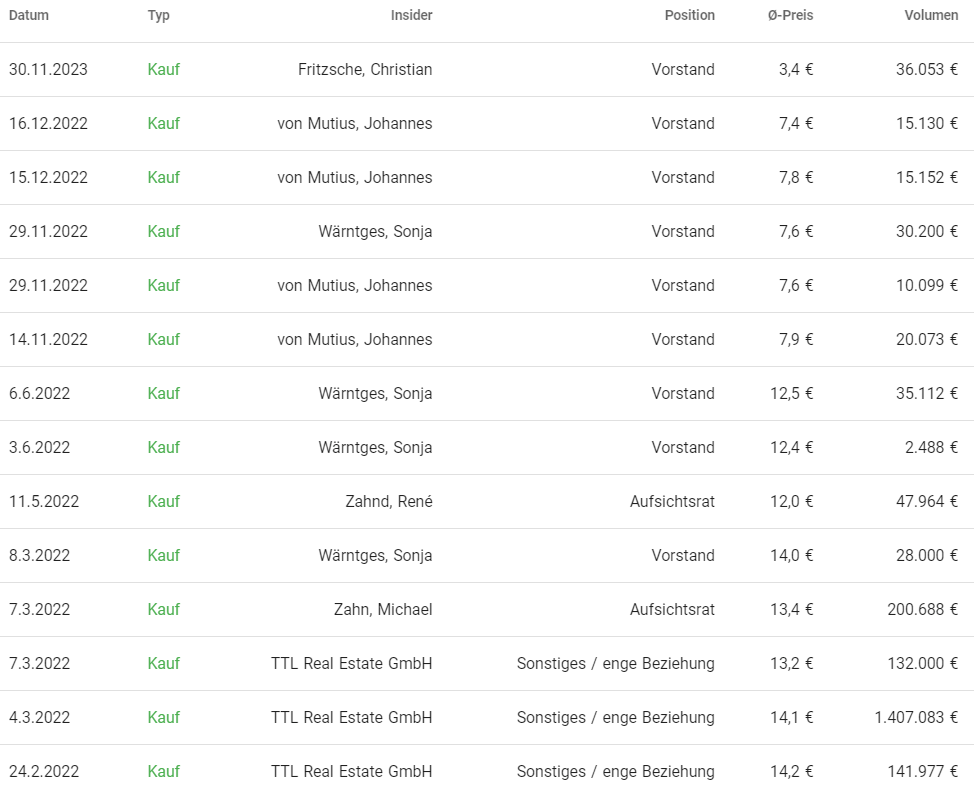

The Chief Operating Officer of the company bought ~$40,000 worth of stock in the open market last month when the shares traded at €3.43. Today, the share price is below €2 per share.

Moreover, throughout 2022, insiders including the CEO, the CIO, and the Vice Chairman of the supervisory board also bought more shares at materially higher levels:

Ariva

In hindsight, these purchases from management and the board look just as terrible as ours. But there is some comfort in knowing that they have been buying more stock as it shows that they haven't lost hope and also have some skin in the game.

Reason #8: The recent change in the company name and management commentary give hope

DIC Asset was rebranded as Branicks in mid-2023. It would seem like a very poor idea to rebrand yourself right before bankruptcy. You would much rather do that during or after the bankruptcy to dissociate from the troubled past and start a new chapter. The fact that they rebranded shortly before the recent troubles might indicate that they don't expect bankruptcy.

Moreover, their commentary on their November conference call was rather positive. Here is what they said about 2024 debt maturities:

"But also for most of the other maturities in 2024, we are in negotiations with banks and investors regarding a mixture of repayment and refinancing via new debt instruments. Overall, we target to reduce our leverage through disposals in the midterm."

Then later on the call, they added that they were already in deep discussions and were preparing different options just in case they didn't manage to sell enough assets on time:

"So at the end of the day, it's disposals because it's for the goal to reduce the leverage and to bring the liquidity in. But on the other hand, we are also working on plans to refinance and to bring liquidity in other ways, and all possible ways, we can imagine so that we are secured on the liquidity side, so to say. We are in deep discussions here. And we are working on all these streams. But at the moment, I cannot say what option we take at the end of the day. But it's all about to develop options and to be prepared that we can - yes, that we have secured an option that we can finalize them."

They also felt confident that they would manage to keep covenants under control. Again, this was in November:

"The covenants of our green bond maturing in 2026 have sufficient headroom. While we see some pressure on the increased interest costs and lower fee income on our bond ICR with coverage of 2.3x, we are still comfortably above the threshold of 1.8x. According to our business plan, we expect the stabilization and turning point for this metric in 2024.

The bond LTV will also benefit from the equity release of our disposal, thereby mitigating the expected negative effect from the portfolio devaluation."

The bottom line is that Branicks has become a very speculative investment.

It has been hit by a series of black swans and it is now at the mercy of its lenders.

It could be a 0 and that is why the market is pricing it today at a 95% discount to its net asset value. If it is ultimately going to zero, then no share price is low enough.

But there's still hope... and based on my analysis, there's more hope than what's implied by the current share price, but I have been dead wrong so far.

It would seem that it would be in the best interest of the lenders to work out a solution with Branicks to give it some more time to sell assets, and if they manage to secure an extension, and then succeed in selling assets, the upside could be immense.

If over the next few years, they manage to pay off all this short-term debt, deleverage the balance sheet, and return to growth, the share price could easily triple or much more in the best-case scenario.

ILPT is an industrial REIT that owns some amazing assets, especially in Hawaii, where the supply of land is strictly limited and existing properties enjoy high barriers to entry:

Industrial Logistics Properties Trust

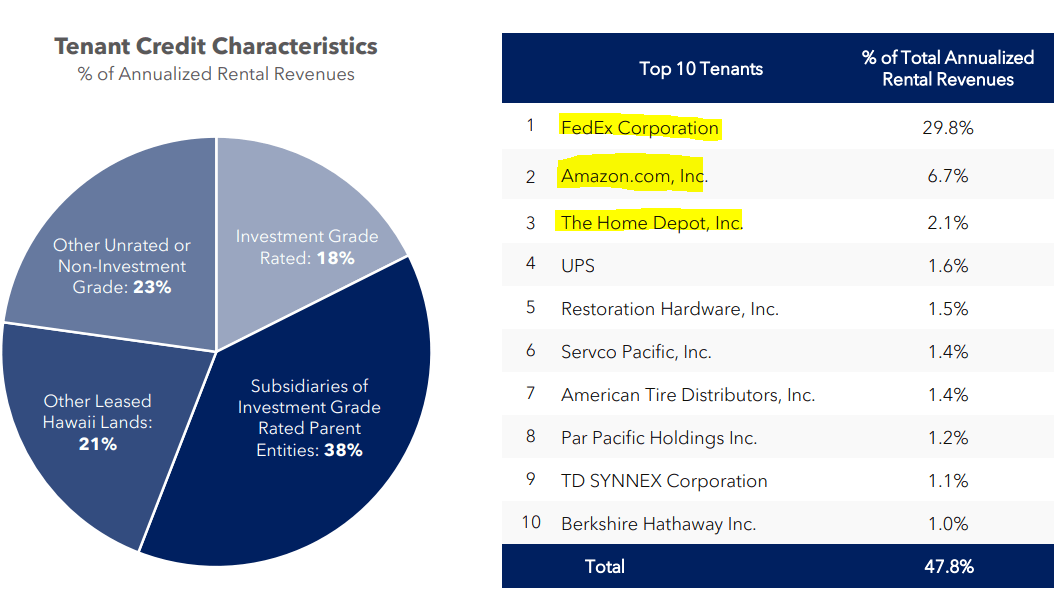

ILPT today generates 28% of its revenue from Hawaii, and the rest of the portfolio is mostly leased to investment-grade-rated tenants like FedEx (FDX), Amazon (AMZN), and Home Depot (HD):

Industrial Logistics Properties Trust

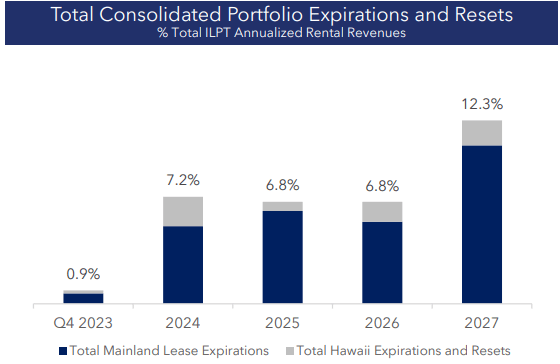

The average occupancy rate of the portfolio is ~99%, which is strong evidence of the high quality of the portfolio. Moreover, the rents of its properties are deeply below market, providing a path to 10-20% rent bumps as its leases gradually expire. In the last quarter, it again enjoyed 11.2% releasing spreads and over 30% of its leases are set to expire in the next 4 years:

Industrial Logistics Properties Trust

But unfortunately for ILPT, it made a similar mistake as Branicks and took on too much leverage.

Back in 2022, it made a huge investment by acquiring another REIT called MNR Real Estate (MNR) and it funded a big chunk of its purchase with some short-term debt.

The plan just like in the case of Branicks was to then sell some of the assets to pay the debt and only retain a portion of the assets.

But that plan was then derailed by the surge in interest rates.

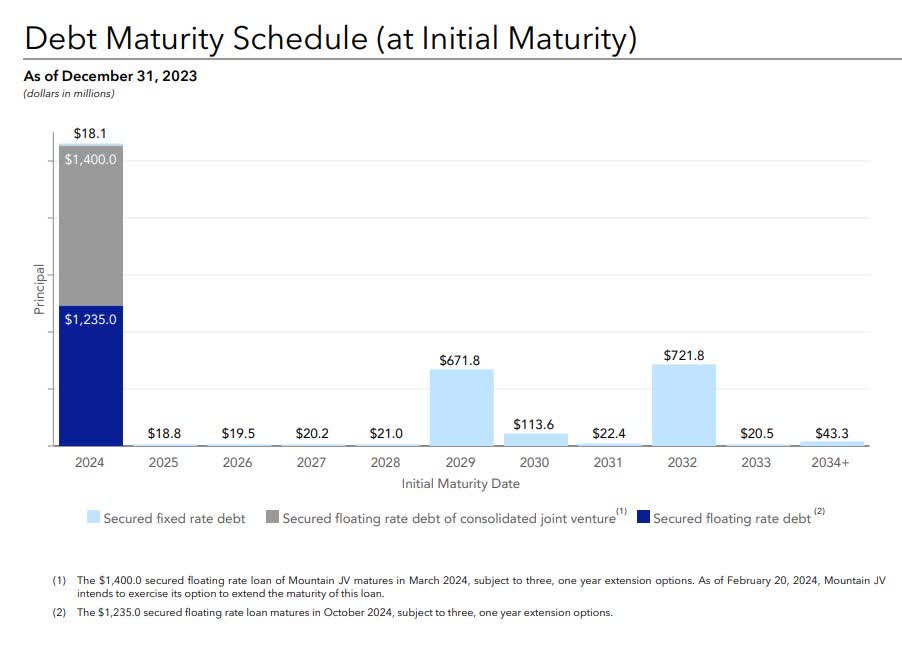

It failed to sell enough assets to deleverage and it is now at high risk of bankruptcy because it is facing a big maturity wall later this year:

Industrial Logistics Properties Trust

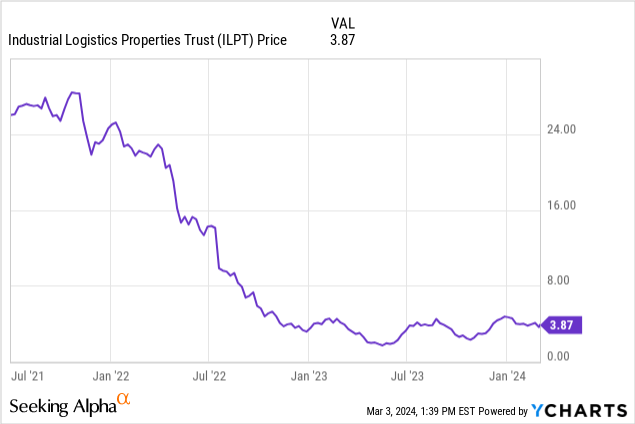

This has caused its share price to crash from nearly $30 per share to just $3.80 today. If the company is ultimately going to default, then no share price is low enough... But if it manages to survive, the upside could be huge in the recovery because its NAV per share is estimated to be about $20 per share.

So what's the most likely outcome here?

There is hope, but also significant uncertainty.

On one hand, things may not be as bad as they may first seem because most of those 2024 maturities include extension options. This is why the management said the following on their most recent conference call:

"Including extension options, ILPT has no debt maturities until 2027. In March, we intend to exercise our first extension option on the $1.4 billion floating rate loan held by our consolidated joint venture."

But extension options are typically subject to certain conditions and there is no guarantee here that the lenders will want to work with ILPT.

The management is confident that they will be able to extend this debt and talks on their conference call as if it was a done deal, but the manager of RMR (RMR) has a poor track record so you need to take it a grain of salt.

Moreover, extending the debt will come at a cost as it will result in higher interest rates and require them to purchase additional rate caps since most of their debt has a floating rate.

That's a big issue since ILPT is massively overleveraged with a ~70% and 12.3x Debt/EBITDA. Fortunately, the REIT is gradually bringing its leverage down by raising equity into JVs and retaining all of its cash flow for deleveraging instead of paying a dividend.

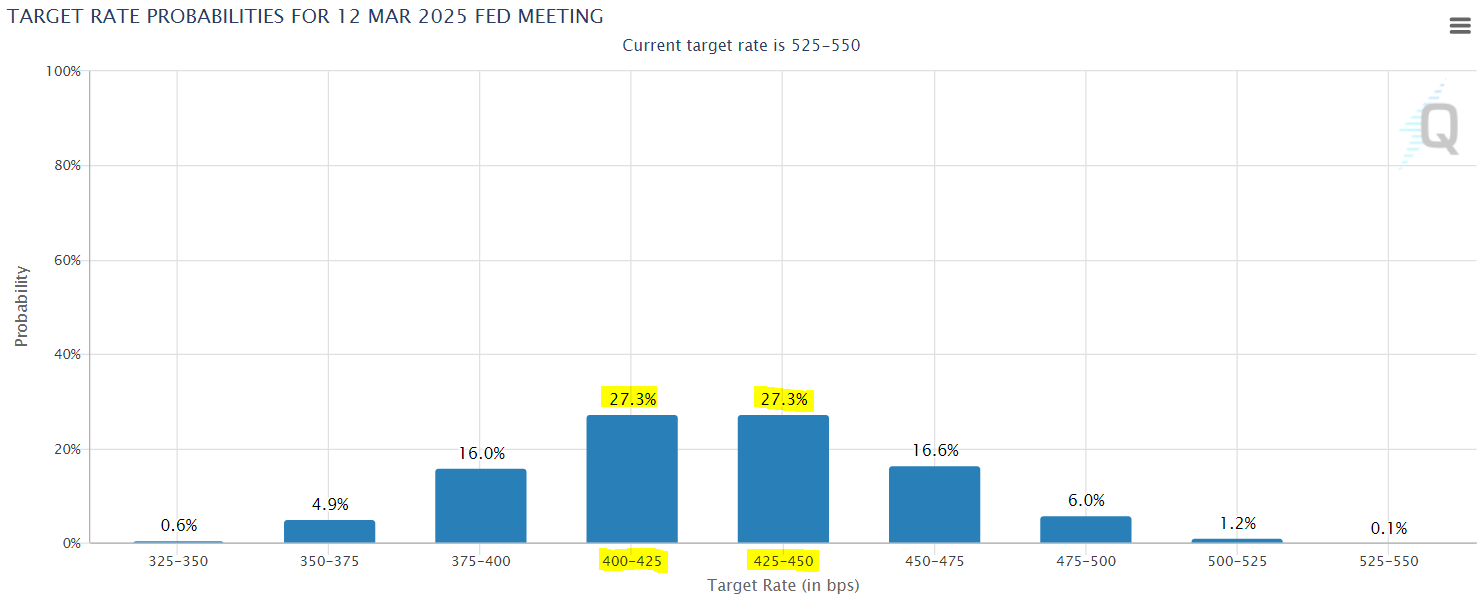

The anticipated cuts to interest rates should help them a lot as well. Within a year from now, interest rates are expected to be >100 basis points lower according to FedWatch, and that on its own should make a big difference.

FedWatch

Will they have made enough progress before the debt comes due?

There is a good chance that they will and in that scenario, the stock price could easily triple from here.

But such high returns come with high risk. Just like Branicks, the situation is very tough and while they may well survive, this has become a very speculative situation and this is why it is priced at such a huge discount to its net asset value.

I will keep monitoring it closely.

There are other examples of REITs that present such massive upside potential. Uniti (UNIT) comes to my mind.

But remember that high reward comes with high risk and if risk factors play out, any of these companies could be a 0. You need to be comfortable with that if you are going to speculate and make sure to diversify your risks.

Editor's Note: This article discusses one or more securities that do not trade on a major U.S. exchange. Please be aware of the risks associated with these stocks.