mmeee

mmeee

In 1999, Bill Clinton was president, Britney Spears topped the charts, and the Nasdaq skyrocketed 101% in a single year. Fear about a Y2K doomsday caused corporations and governments around the world to quickly spend an estimated $300-$500 billion on new technology. Twenty-five years later, we've come full circle. Today we have Joe Biden instead of Bill Clinton, Taylor Swift instead of Britney, AI hype/fear rather than Y2K hype/fear, and Nvidia (NVDA) instead of Cisco (CSCO). History is cyclical!

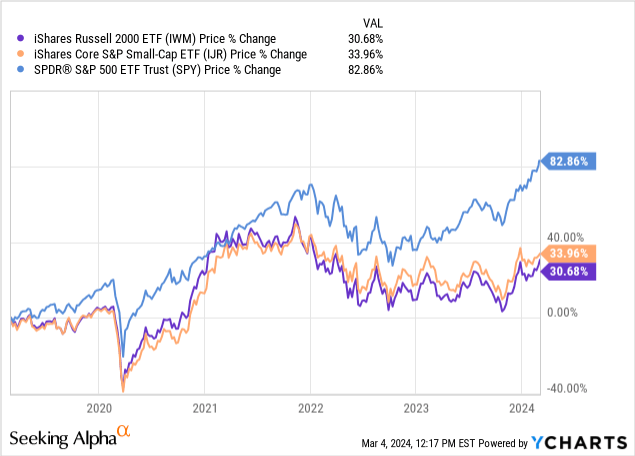

In hindsight, the best thing you could have done during the dot-com bubble was to wait for things to get crazy, then crazier, and then so crazy you couldn't believe it, and then cash a lot of money out. The second-best thing you could have done is less obvious, but it would have been to rotate into small caps. Due to their lower starting valuations, small caps (NYSEARCA:IWM) beat the S&P 500 (SPY) for five consecutive years starting in 2000. Research shows that focusing on small-cap stocks of companies that turn a profit is even better, with the S&P 600 (IJR) index crushing the broader small-cap index of IWM, which in turn beat the S&P 500. The data I have shows that an investment in small-cap IJR grew from $10,000 to $18,300 from June 2000 to December 2005, while the "can't lose" S&P 500 shrunk to $9,500. An investment in the Nasdaq during the same time would have been worth $4,900–an over 50% loss five years later.

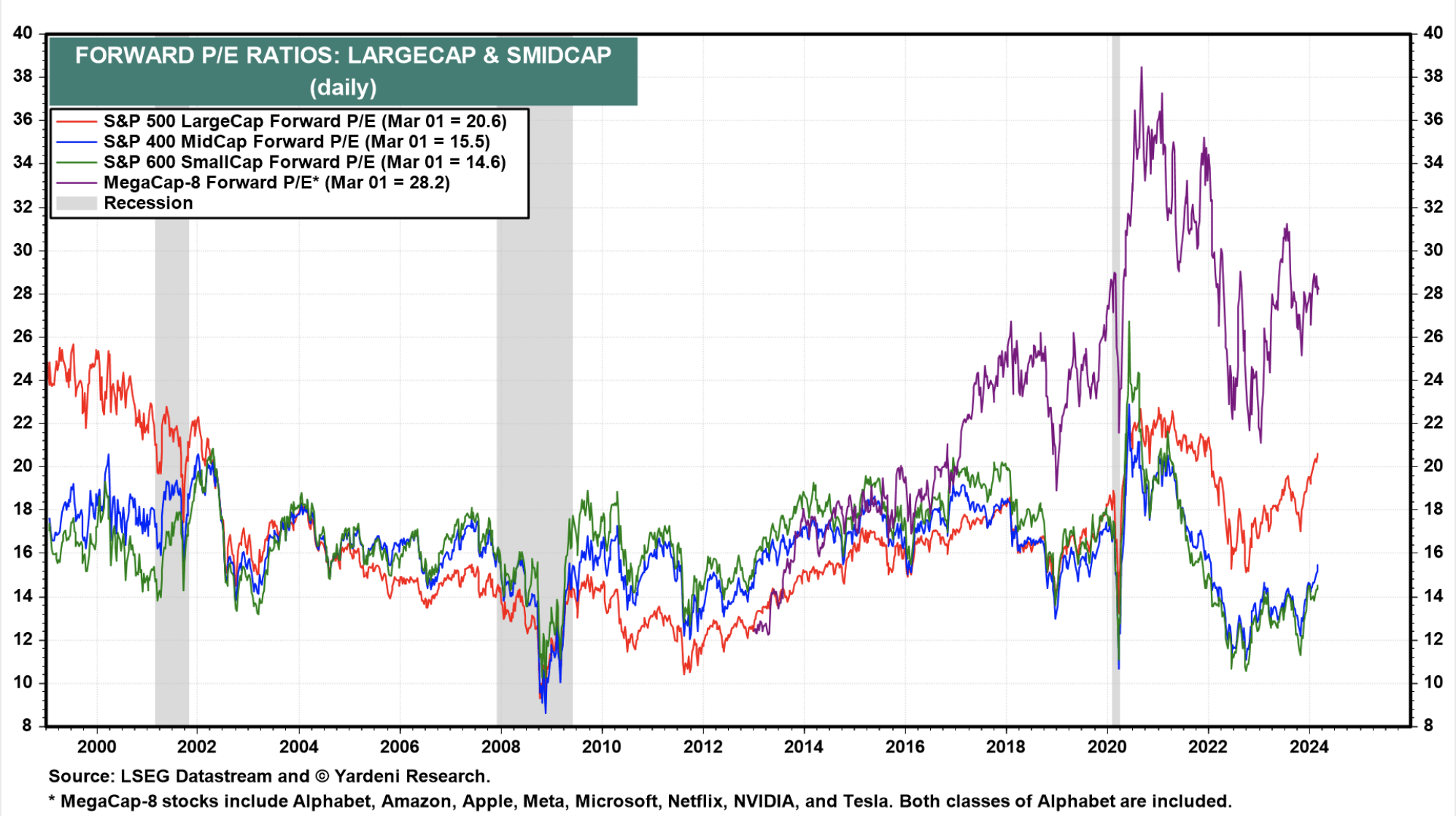

Look at the valuation disparity between large and small caps in 2000, and again at the valuation disparity now (megacap data since ~2013).

Forward P/E ratios by Company Size (Yardeni Research)

Small-cap stocks and mid-cap stocks are trading right in their historical norms, while large-cap valuations have ballooned, despite earnings being roughly flat year-over-year. The valuation gap is getting wider and wider between small and large caps, and this has accelerated early this year.

If we go up another 20% on the S&P 500 with current earnings, we would match the peak dot-com bubble valuation. Buying those stocks then would have put you underwater for about 15 years, so that's quite a feat. Tech bulls are likely to point at single stock valuations being crazier in 1999, but the overvaluation in the large-cap space is far more pervasive than people realize. Stocks like Costco (COST) are trading for close to 50x earnings, with 5% year-over-year revenue growth. With one of the biggest market caps in the world, Apple (AAPL) is close to 30x earnings with 1% revenue growth. Pretty much any company claiming to have a weight loss drug is now trading at 50-100x earnings, even though they're all in competition with each other for the same market share. Sun Microsystems co-founder Scott McNealy famously drew the line at 10x price-to-sales almost always being too high after the dot-com bust in 2002, but there are dozens of companies trading for over that now, including some you wouldn't expect. When you add up analyst market share projections for each individual company, and they add up to 150% or more of the market, you know someone won't have a chair when they try to sit down.

Small caps intrigue me. There's almost negative hype around them. No one seems to care to invest in companies anymore if they aren't burning money trying to mine rocks on the moon or promising a magic diet drug for the overweight masses.

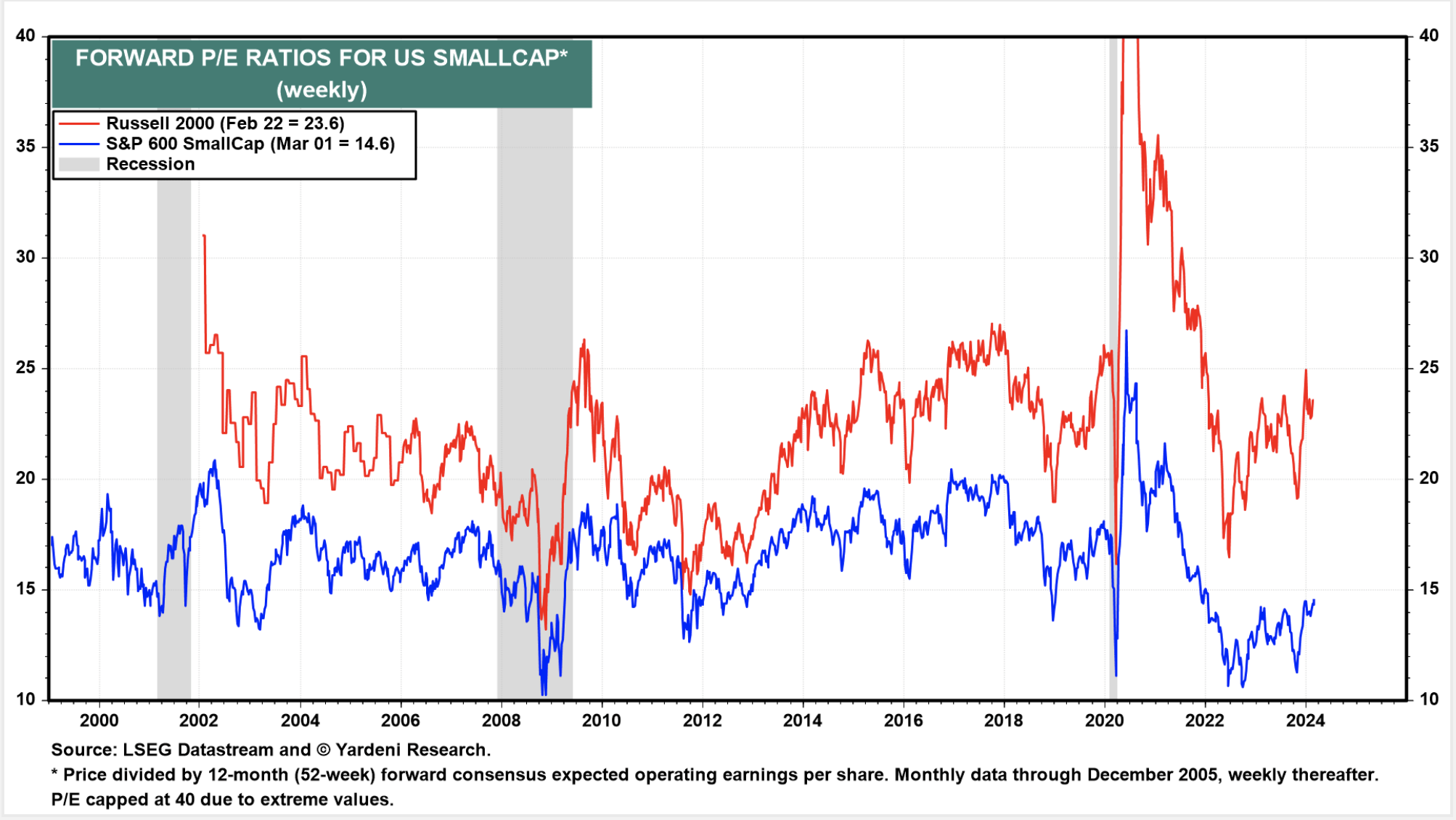

Russell 2000 vs. S&P 600 P/E Ratios (Yardeni Research)

We see this with the disparity between profitable small-cap companies in the S&P 600 and the broader Russell 2000 index. When you add a bunch of money-losing companies to the index, it makes sense that the P/E ratio is higher because your earnings are less. It's also rather intuitive that investing your capital in money-losing companies hurts your returns – my data shows the S&P 600 outperforms the Russell 2000 by about 1.75% annually on average.

1. No hype. Valuations for small-cap stocks are trading at or below their historical averages. If productivity and the economy are expected to do well, small caps should do well. I believe that things went off the handle some time in 2019 and markets stopped rationally pricing things. The valuation spread between small caps and large caps is a gift for patient investors. History shows that there generally is an extra premium for investing in small-cap stocks – they tend to outperform their larger peers over time.

2. Interest rates. Interest rate hikes affect large-cap stocks and small-cap stocks differently. Mega cap stocks with large offshore cash hoards saw their interest income increase when the Fed hiked rates because their cash saw higher rates while their debt was locked in long term. Now, if you think the Fed is going to cut (to be fair, maybe they won't), then this should decrease earnings for mega caps and help small caps. The market seems to be pricing that the Fed hiking and cutting is both good for mega caps, but I don't necessarily think this is true. If the Fed is going to cut, it should help small caps relative to large caps. Even if they don't, large caps are slowly going to have to refinance all their corporate debt to higher rates, creating a drag on their earnings relative to small caps which have refinanced much more debt since the Fed started hiking.

3. Small caps are traditionally thought of as more risky than large caps due to being more sensitive to the economy. However, with the current valuation spread, small caps may be less risky because they have more reasonable expectations for growth. A similar dynamic played out in the early 2000s, the economy briefly entered recession, but unemployment didn't skyrocket. Meanwhile, large-cap stocks fell 50%, erasing trillions in paper wealth. Risk is relative.

A large valuation gap has opened up between large caps and small caps since the pandemic. The last time this happened was during the dot-com bubble, and the result was that small caps demolished large caps over the coming years. I'd argue that this is likely to happen again. Is this time different? Why or why not? Share your thoughts below in the comments!