fizkes

fizkes

The objective of this article is to analyze the transaction announced on February the 29th between EVERI Holdings Inc. (NYSE:EVRI) and IGT's Global Gaming and Play Digital businesses focusing on the valuations used for both operations and trying to contrast those estimates with all the available information for each of the businesses that take part in this deal.

I was (but no longer am) a holder of a small position of EVRI stock at the day of the announcement of said transaction, so the article is written from that point of view, but if you are an International Game Technology (IGT) stockholder the opposite implications should apply to you.

I understand that the Hold rating might be confusing given that I sold my shares, but it's simply there in the spirit of consistency with the valuation exercise that I will show later in the article. And should be a secondary consideration to the main purpose of the article which is answering the following question: Is this deal in the best interest of shareholders or not?

THE AVAILABLE INFORMATION

We of course have full financial reports for EVRI as the whole operation is taking part in this combination, but that is not the case for IGT’s part of the deal. And because of that, before starting with the exercise, I will try to be as transparent as possible by providing the detailed figures that I am relying on for EVRI and especially when it comes to IGT Global Gaming and Play Digital operations as only two of the three segments of IGT are taking part in this combination.

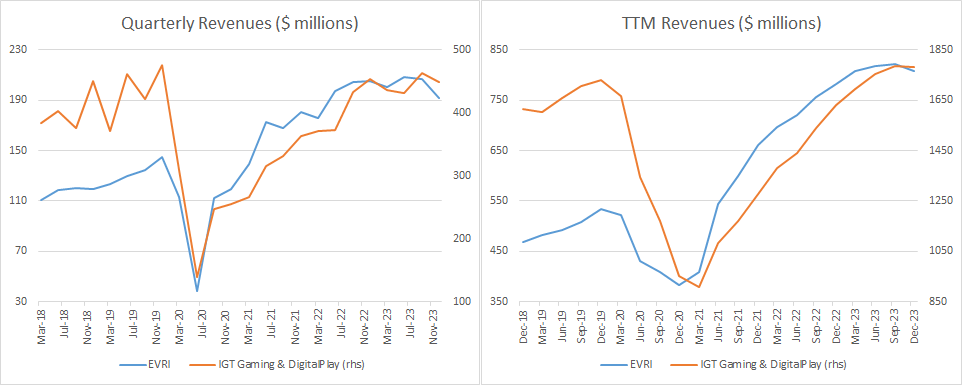

Let’s start by looking at the revenue evolution for EVRI and both of IGTs segments taking part in this combination.

IGT and EVRI Earning Releases

From those two charts we can see that today EVRI’s revenue is more than 50% higher than pre pandemic peak and IGT Gaming & DP businesses are only 3% above those levels.

But to be fair we need to recognize that both companies have allocated roughly the same capital towards acquisitions since 1Q2018 (approx. $175 millions), and that amount is more material for EVRI as a smaller business. So, let's correct today’s revenue assuming that those acquisitions were done at a 1-time price-to-sales multiple. With that, on an organic basis, today’s revenues stand 34% above 4Q18 TTM figures for EVRI, while IGT Gaming & DP businesses are basically at the exact same level.

So, we can conclude that (1) EVRI has shown a more solid organic growth track record than IGT Gaming and DP Businesses and (2) EVRI was able to recover much faster from the impact of the pandemic than IGT Gaming and DP Businesses.

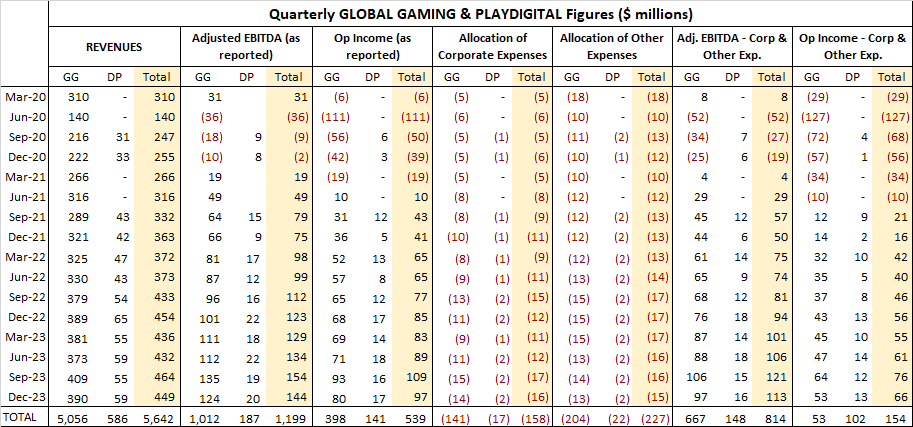

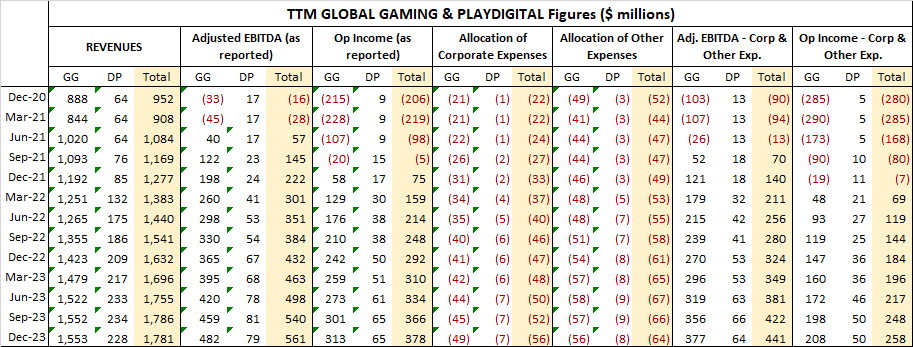

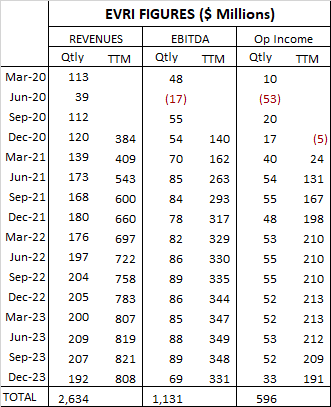

The two additional main variables that I will be using are Ebitda and Operating Income as both have been reported by IGT separately on their quarterly reports since the 1st quarter of 2020. And to make these figures consistent with EVRIs I have adjusted them by allocating Corporate and Other expenses to each of IGT 3 segments (Lottery, Global Gaming and Digital Play) as proportion of total revenue. The Only further adjustments that I made to the reported data is to correct for impairments made by both companies in the window that goes from 1Q2020 to 4Q2023 those are: (1) a $296 million goodwill impairment in the 1st quarter of 2020 in the case of IGT and (2) a $11.7 million intangibles impairment in the 4th quarter of 2023 for EVRI.

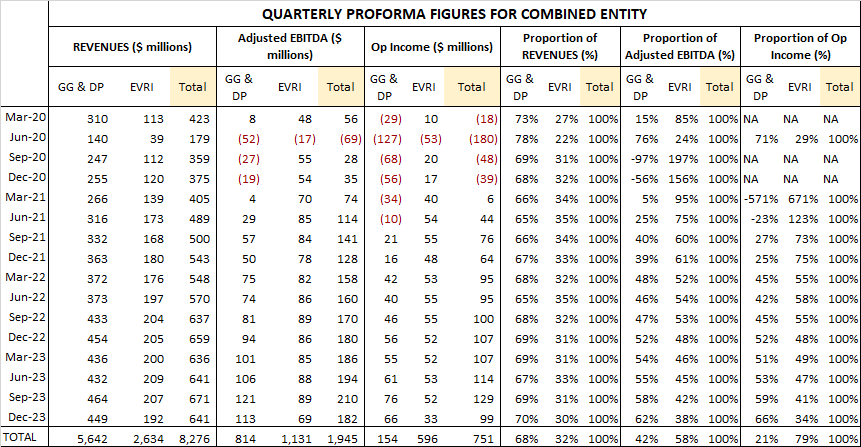

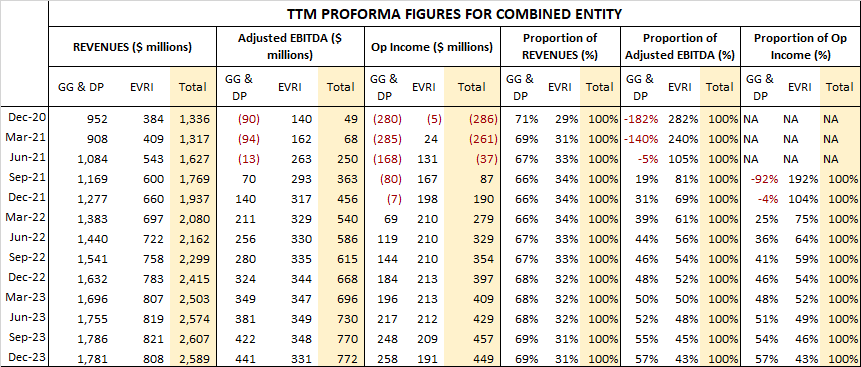

With that, the available figures for both EVRI and IGT Gaming & Digital Play businesses on a quarterly and TTM basis are as follows:

IGT Earning Releases and author calculations

IGT Earning Releases and author calculations

EVRI Earning Releases

And now let’s see the how the combined entity would have looked on a Quarterly and TTM basis for the same time period.

IGT and EVRI Earning Releases and author calculations

IGT and EVRI Earning Releases and author calculations

From that combined data we can observe that during this period (1) IGT Gaming & Digital Play businesses shows a more consistent growth rate than EVRI and (2) EVRI generated a 58% and 79% of the combined Ebitda and Operating Income respectively. But as we saw when we looked at revenue trends (where we have a longer dataset) both observations are deeply affected by the fact that IGT Gaming & Digital Play Businesses were more heavily affected by the pandemic and just recently have recovered their pre pandemic financial results.

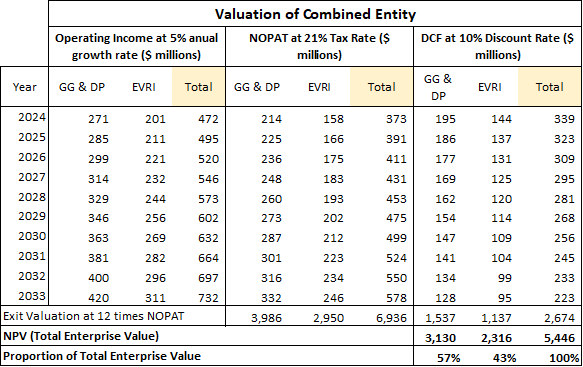

So having looked at those historical figures in detail let's try to value each of the operations using the following set of assumptions.

Growth rate: In the combination presentation (page 11) both managements (I assume) pointed towards a Mid-single digit revenue CAGR through 2026 and a High-single digit Adjusted EBITDA CAGR through 2026. Even though they only gave their expectations up to 2026 and this type of combination usually does not go as smoothly as expected, let's be relatively optimistic and assume a 5% growth rate for both sides of the combination for the next ten years (I personally think that 5% is too high to provide sufficient margin of safety, but that is what I will use in this exercise). Here, it's important to remember that as we saw when we looked at revenue trends, EVRI’s track record is much better than that of IGT Gaming & DP businesses, so this assumption is much more charitable towards the later.

Starting Point: We will apply that 5% revenue growth starting with the last TTM operating income for each side of the deal, by far the best picture of the window that we had available for IGT Gaming & DP businesses versus EVRI as a proportion of the proforma total combined entity. By starting with Operating Income, I am assuming that depreciation and amortization will be equal to Capex going forward, a reasonable assumption given the financial history of EVRI.

Tax Rate assumptions: I will assume a 21% tax rate for each business even though IGT as a consolidated entity has been paying a higher rate and EVRI a lower one.

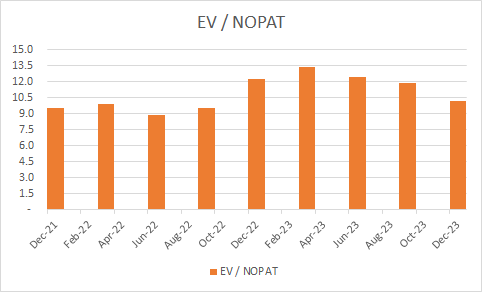

Other assumptions: I will assume a 10% discount rate and an exit multiple after 10 years of 12 times EV/NOPAT (a little above where EVRI has traded the last two years)

EVRI Earning Releases and Author Calculations

The next table shows the figures under those assumptions:

Author Calculations

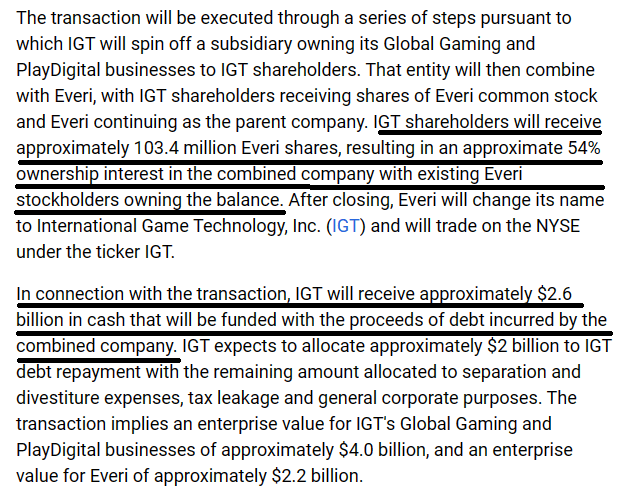

Now let look at the terms of the agreed deal:

Combination Announcement

As there is the mention of debt coming from the side of IGT Gaming & DP businesses, it’s important to point out that EVRI has at their latest earning release a total net debt of $730.7 million. You can check that for yourselves in this SA link (forth row from the bottom).

If the reader agrees that the assumptions used are reasonable (I personally would have preferred to be a little more conservative) we can make the following observations: (1) EVRI was undervalued by 5% (2) IGT Gaming and DP businesses were overvalued by 28% (3) The combined entity was overvalued by 14% (4) the deal allocates 64.5% of the combined entity to IGT Gaming and DP businesses and a 35.5% to EVRI, a 7% unwarranted overallocation towards IGT c and a 17% unwarranted under allocation towards EVRI (5) IGT gaming and DP businesses carry total net debt of 83% of its total estimated enterprise value, EVRI carry total net debt of 32% of its total estimated enterprise value and the combined entity carry total net debt of 61% of its total estimated enterprise value (6) Total Net debt for the combined entity will stand at $3,330.7 million leaving a net present value of $2,115 million, valuing EVRI’s market cap at $972 million (46% of the combined entity) and (7) If the combination would have been done at the valuations that I showed and under the same indebtedness for each side of the deal, the total value of the combined entity would have been exactly the same but EVRI would have received a 75% allocation of the merged entity and consequently its market cap would have been valued at $1.585 million, $612 million more than under the agreed terms.

And one final point that makes this deal even harder to understand, is that the 54%/46% final distribution of the combined entity between EVRI and IGT shareholders should be the result of the agreed valuations minus the net debt coming from each side, and even that does not add up.

Even if we accept (and I clearly do not) that EVRI and IGT Gaming & Digital Play businesses should be valued at $2.2 billion and $4 billion respectively, and we recognize that the former has net debt of $730.7 million and the later $2.6 billion, the distribution of the combined entity should be as follows:

For EVRI: ($2,200 - $730,7) / ($2,200 + $4,000 - $2,600 - $730.7) = 51.2%

For IGT: ($4,000 - $2,600) / ($2,200 + $4,000 - $2,600 - $730.7) = 48.8%

And this fact alone implies an under allocation towards EVRI of 5.2% of the combined.

I purposely tried to make this article very clinical in my language and a little dry by showing a lot of detailed figures and assumptions to be as transparent as possible, letting you the reader, be the judge.

Having displayed my analysis in detail I think I have shown that under the assumptions used (that I think are somewhat favourable to IGT Gaming and Digital Play Businesses) the terms of the announced combination are not in the best interest of the EVRI shareholder, and even under the agreed terms, the final distribution of the combined entity does not make sense.

And the market reaction to this announcement, leads me to think that I am not alone in that perspective.

I accept that is possible that there is some extra or more detailed information that would make the agreed terms more understandable, but management explicitly decided to not face their shareholders and defend the agreed terms of the deal when they decided to cancel their quarterly earning call.

EVRI 4Q2023 earning release (page 8)

And that, makes me even more confident in my perspective.

Thanks for reading and better luck with your investments!