AAlves/iStock via Getty Images

AAlves/iStock via Getty Images

The main thesis of IDT Corporation (NYSE:IDT) revolves around the potential spin-offs of its three high-margin, rapidly growing businesses: NRS, BOSS Money, and Net2Phone (N2P).

However, the decision to postpone the spin-offs is rooted in a prudent assessment of market conditions and valuation dynamics. By awaiting a more favorable market environment, the management team aims to maximize shareholder value by ensuring that the spin-offs occur at an opportune moment, where they can fetch an optimal valuation.

Nonetheless, while awaiting the ideal time for a spin-off, management did splendidly well in running these businesses as shown in its strong organic growth and successful transition to profitability. More specifically, 2Q24 marks a significant milestone for the company as these businesses are self-sustainable and no longer require new cash investments to fund their growth. This allows the company to reallocate resources more efficiently, potentially accelerating growth in other areas or enhancing shareholder returns. Indeed, during the quarter, they announced the issuance of dividends as a way to return capital to shareholders.

And based on my sum-of-the-parts (SOTP) valuation, IDT Corporation remains attractively priced with a 17% upside from its current share price, leading me to assign it a "buy" rating. Additionally, if you have not, I recommend you to check out my previous article.

Finally, in this article, I will be diving deeper to evaluate the performance of each business.

IDT's Quarterly Results IDT's Quarterly Results

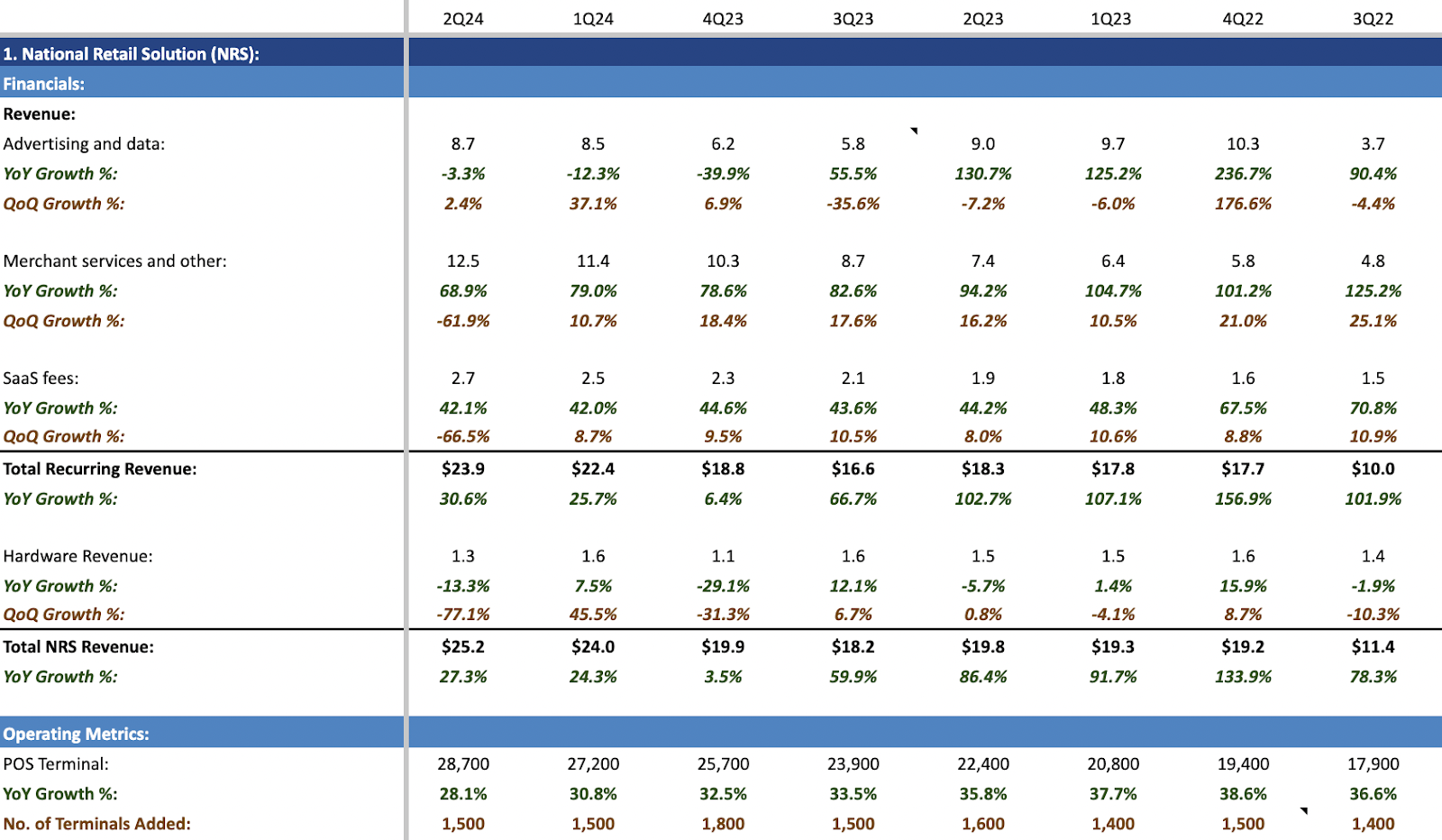

In 2Q24, NRS maintained its pace by adding 1,500 POS terminals, bringing its total number of POS to 28,700. This reflects the continued growth and expansion of NRS' market share, particularly in the small retail segment.

Unlike competitors such as PAR Technology (PAR), Lightspeed (LSPD), and Toast (TOST), which predominantly target mid-to-large restaurant operators, NRS has carved a niche by focusing on serving small independent retailers. These retailers, often overlooked by other providers, have faced challenges in digitizing their operations, making NRS's tailored solutions, particularly valuable to this underserved market segment. As NRS continues to expand their footprint, this creates a flywheel effect which helps NRS to land more merchants.

NRS high-margin advertising and data revenue, a major contributor to its NRS profitability, has marked its second consecutive quarter of revenue recovery, demonstrating a sequential growth of 2.4% from 1Q24. However, given the economic challenges we are in today, it is still important to monitor the stability of this revenue segment, and assume no margin expansion in our forecast in the near-term.

NRS's EBITDA margin remained the same as 1Q24 at 25.8%, an industry-leading margin when compared to competitors like Lightspeed and Toast who have yet to attain profitability.

IDT Quarterly Result

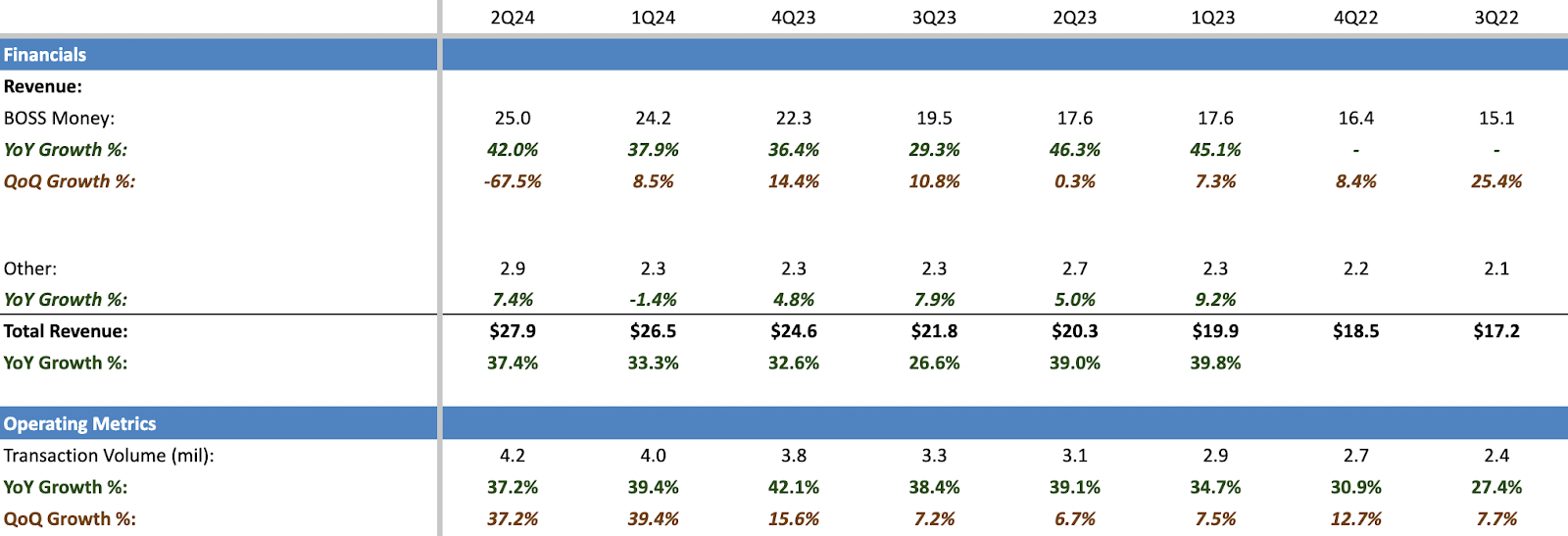

BOSS Money, IDT's money transfer business, is a standout during the quarter.

2Q24 transaction volume grew 37.2% YoY, resulting in an impressive 42% revenue growth. Firstly, the synergistic cross-marketing efforts between BOSS Money and BOSS Revolution, IDT's established mobile top-up service, played a pivotal role in driving transaction volumes. By leveraging the existing customer base and distribution channels of BOSS Revolution, BOSS Money was able to expand its reach and attract new users to its money transfer platform. Moreover, management's proactive approach to expanding the retail agency network also contributed significantly to the division's growth. By forging partnerships and increasing the number of retail locations where customers can access BOSS Money's services, the company enhanced its accessibility and convenience, thereby attracting more users and driving transaction volumes.

The robust growth exhibited by BOSS Money not only underscores its resilience but also highlights its potential as a key revenue driver for IDT. As the company continues to capitalize on synergies within its business ecosystem and expand its market presence, BOSS Money is poised to play an increasingly integral role in IDT's overall growth strategy.

FinTech's Profitability

More notably, this quarter was a milestone for BOSS Money as its strong operating leverage resulted in positive EBITDA for the first time, demonstrating that their decision to pursue growth at the expense of profitability has not been futile.

During the 2Q24 earnings call, when asked if its positive EBITDA could be sustained and its future potential EBITDA margin, here's what management has to say:

"...if we continue to grow the business at sort of like half the pace that we've been growing, we could see it getting to $14 to $15 million of profitability…over the next two to three years….Gibraltar, the Neo-Bank, they're kind of mostly pre-revenue at this stage…So we're kind of investing in those initiatives now with the cash flows from Money Transfer…scale matters hugely in terms of getting to higher profitability in that industry and growing organically have been good for us. We've been growing at around 35%, 40% clip, which is excellent, better than other in this industry."

Achieving profitability alongside a remarkable 42% growth rate is a testament to the company's exceptional performance. Once again, management has showcased its adeptness at fostering both organic growth and profitability, a feat previously demonstrated with NRS and Net2Phone. With BOSS Money now joining the ranks of profitable ventures, the company is strategically reinvesting cash into other initiatives such as its digital banking arm, or Neo-Bank, further fueling its expansion and innovation efforts.

IDT quarterly results

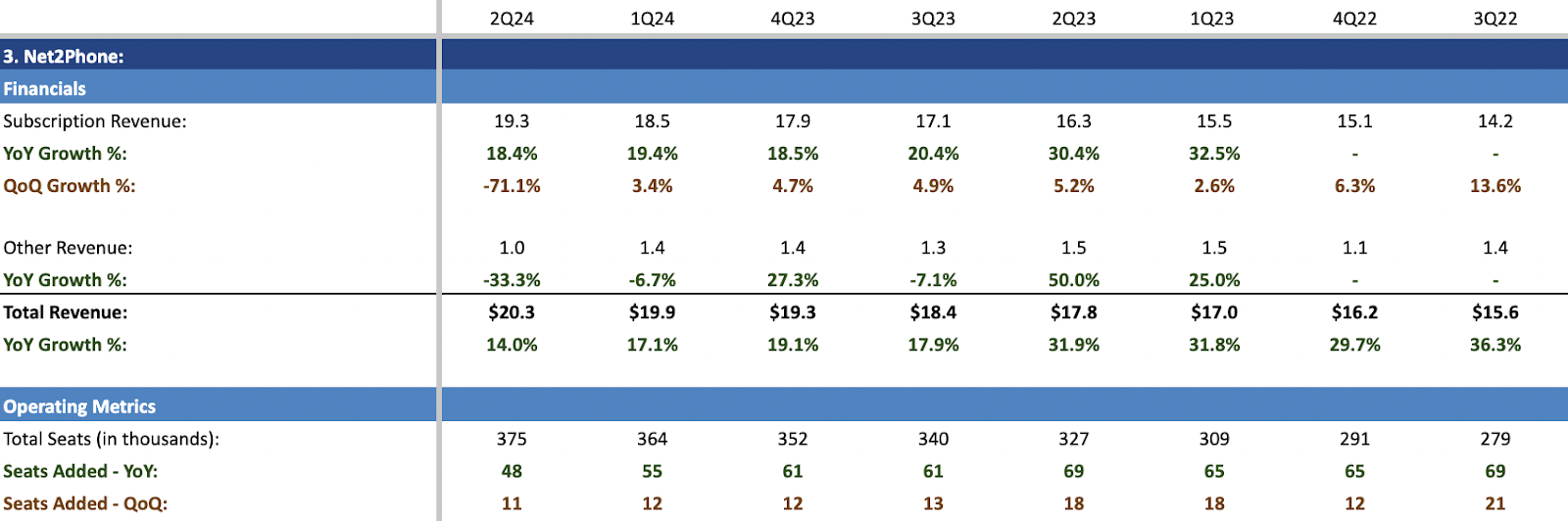

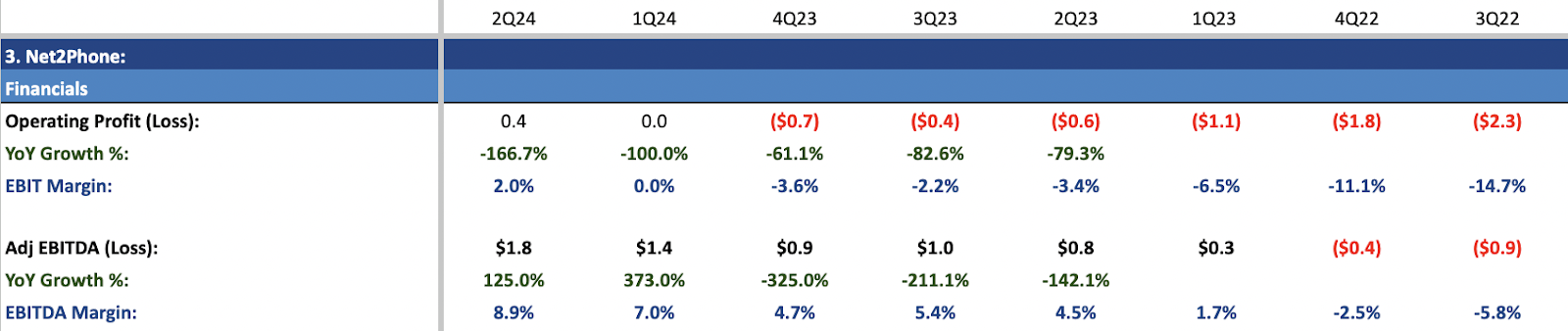

Net2Phone's subscription revenue reached $19.3 million, marking an impressive 18.4% growth from 1Q24, propelled by the addition of 11,000 seats during the quarter. This expansion in the customer base is notably observed in both the U.S. and LatAm markets. As a result, Net2Phone's total seats have now reached 375,000, underscoring its growing market presence and revenue streams.

IDT Quarterly Result

Net2Phone's EBITDA demonstrates remarkable growth, surging by an impressive 125% YoY, which has elevated the EBITDA margin to 8.9% from 7% in the previous quarter. Additionally, management has reported that Net2Phone has achieved positive cash flow, marking a significant milestone for the company. The sustained growth and enhanced profitability of Net2Phone in 2Q24 underscore its ability to expand organically while delivering robust financial performance.

IDT Quarterly Result

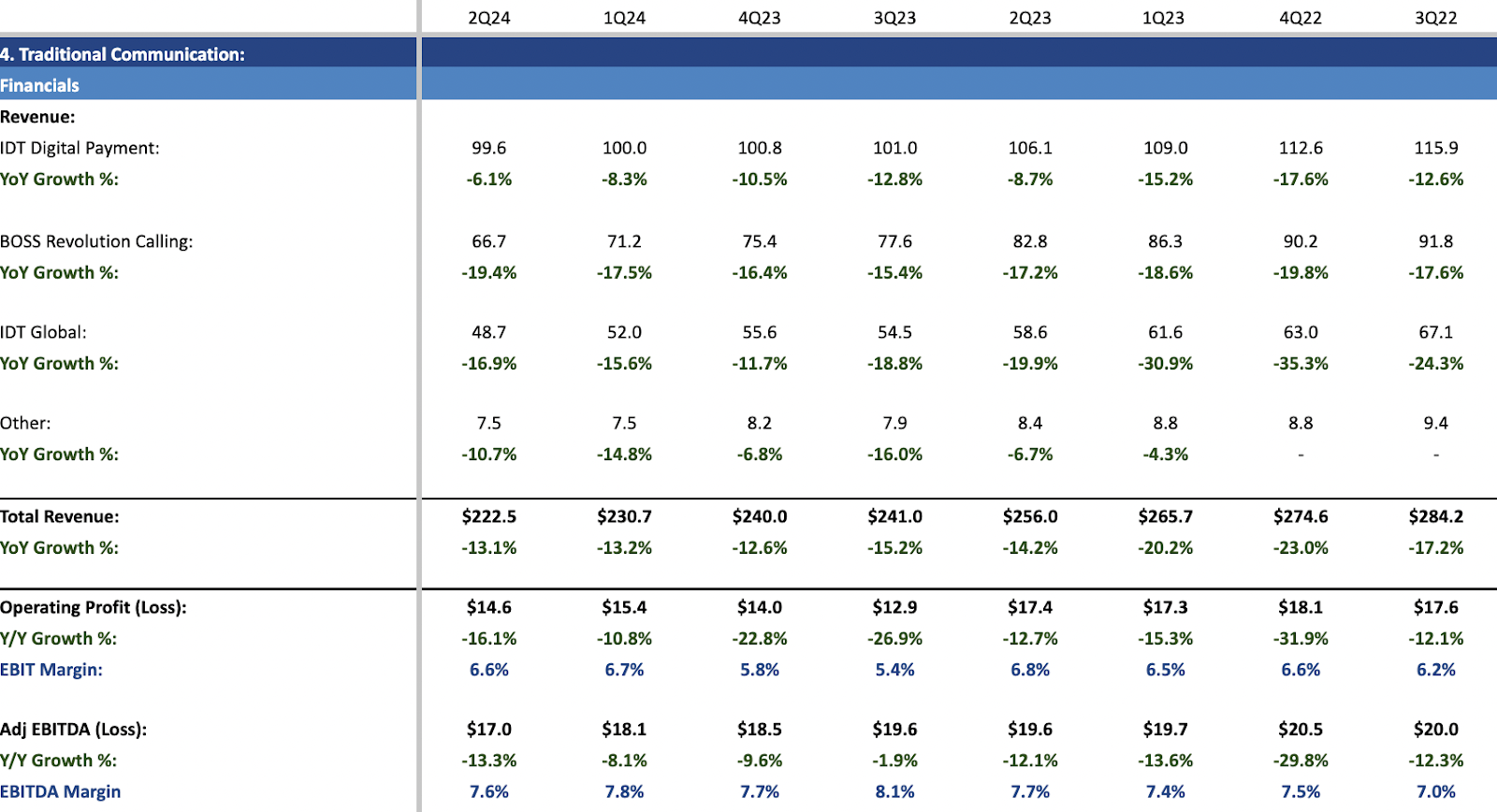

The traditional communication segment of the company witnessed a YoY revenue decline of 13.1%, totaling $222.5 million in 2Q24, while maintaining a stable adjusted EBITDA margin of 7.6%. With the three high-growth, high-margin businesses now operating as self-sustainable entities, the robust cash flow generated by this segment is poised to play a pivotal role in bolstering the company's balance sheet.

Despite the challenges faced by its legacy business segment, the stability in the adjusted EBITDA margin indicates a degree of resilience in the face of market dynamics. Moving forward, the reliable cash flow from this segment will provide a strong foundation for the company's financial health, allowing it to reinvest in growth initiatives, pursue strategic opportunities, and enhance shareholder value.

Moreover, during the 2Q24 earnings call, management addressed inquiries about IDT's substantial cash reserves of $234 million, representing 23% of its market capitalization. They indicated that these funds would be allocated towards either acquisitions or stock buybacks. Notably, the company initiated a $0.05 dividend payout during the quarter, underscoring their dedication to delivering value to shareholders.

It will be compelling to observe whether management opts for acquisitions to diversify into new ventures or fortify their existing high-growth businesses, with the latter appearing more probable. Ideally, shareholders would prefer to see management strategically reinvesting these funds into high return on capital (ROC) projects, maximizing value creation for stakeholders.

BOSS MONEY Valuation BOSS Money's Relative Valuation

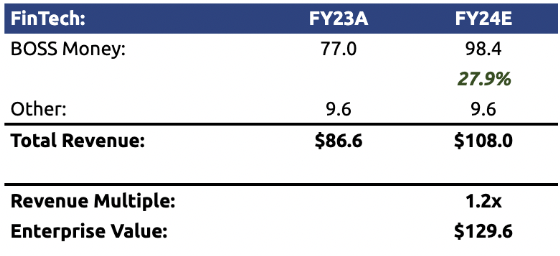

As of 1H24, BOSS money revenue totaled $49.2 million. By doing simple forecasting by annualizing 1H24 revenue, this generates an expected FY24 revenue of $98.4 million. Using an EV/Sales multiple of 1.2x, gives us an enterprise value of $129.6 million.

NRS Valuation

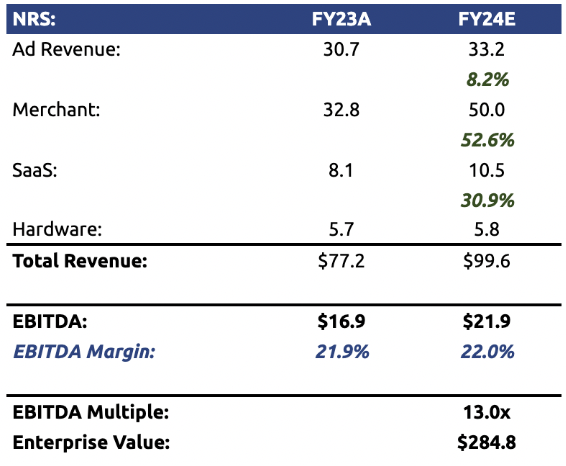

Using the same methodology that I did for the FinTech segment, I annualized 1H24 revenue for both advertising and merchant revenue while maintaining hardware revenue at a constant $5.8 million. Assuming that EBITDA margin remains the same at 22%, this generates EBITDA of $21.9 million in FY24E. With an EV/EBIT of 13x, which is reasonable for a company with an industry-leading margin, and growing revenue at 29% YoY, this multiple is deemed reasonable. Consequently, the enterprise value for this segment is estimated at $284.8 million.

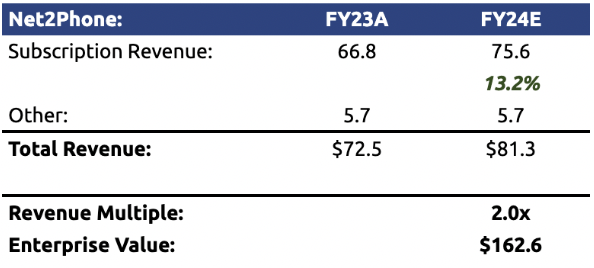

N2P Valuation (N2P Valuation) N2P Peers

Annualizing N2P 1H24 revenue would produce an expected revenue of $75.6 million in FY24. Using a relative valuation, and applying an EV/EBIT multiple of 2.0x, this yields an enterprise value of $162.6 million.

Unlike its competitors, N2P boasts a notably higher gross margin of 80% and has achieved profitability, a feat its competitors have yet to accomplish. Based on these strong fundamentals, I believe my valuation for N2P is conservative and justified.

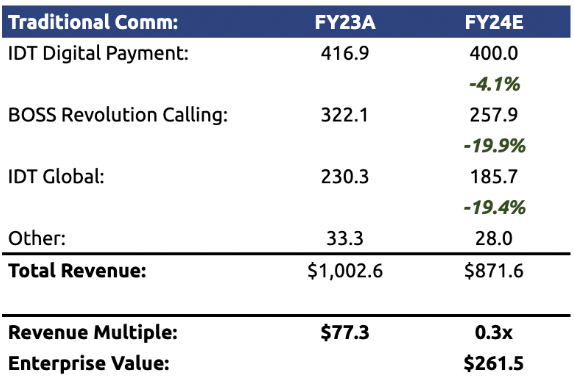

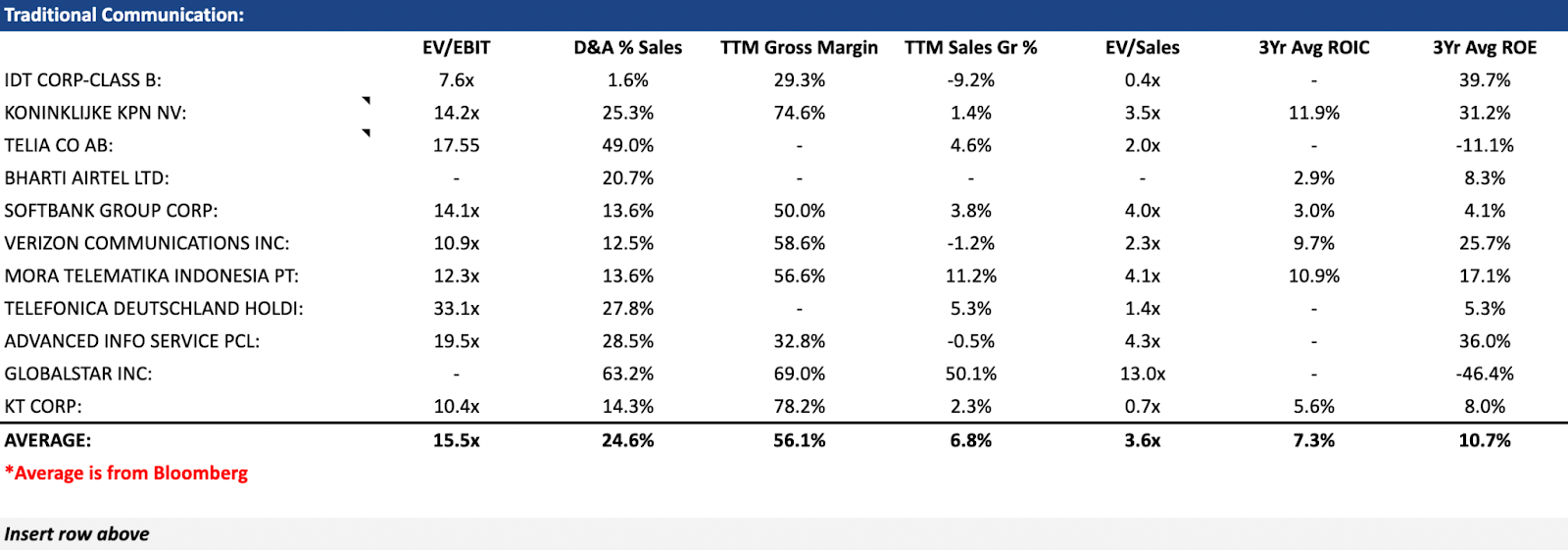

Traditional Communication Valuation Traditional Communication Peers

For the Traditional Communication segment, revenues are expected to continue to decline as a result of reduced calling minutes, especially for the BOSS Revolution Calling and IDT Global segments, with each segment revenue declining by 19.9%, and 19.4% YoY, respectively. IDT Digital Payments, on the other hand, are more resilient and I projected a modest decline of just 4.1% from FY23. This generates a total revenue of $871.6 million by FY24.

Considering the declining growth rates and lower margins associated with IDT's legacy business, I do believe using a revenue multiple of 0.3x, would be more conservative, which yields an enterprise value of $261.5 million.

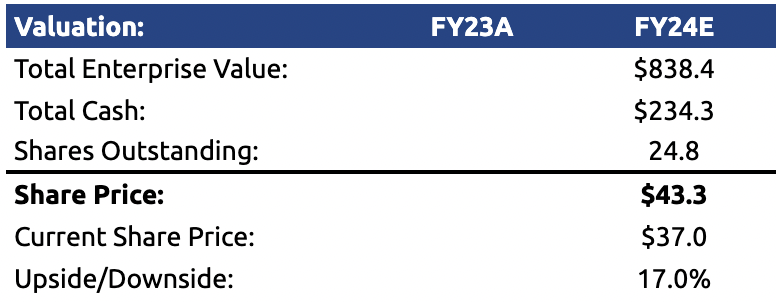

Valuation of IDT

Putting it all together, based on my SOTP valuation, my intrinsic valuation for IDT is $43, a 17% upside from the current share price of $37. With IDT's 3 high-margin, high-growth businesses demonstrating robust top-line growth and self-sustainability, I rate IDT as a buy.

There are a few risks to bear in mind:

NRS: Volatility of ad revenue causes uncertainty in NRS' profitability

BOSS Money: Poor execution risk may result in the inability to translate marketing spend to transaction volume growth, thus, impacting profitability

N2P: Competitors with more financial resources enter into N2P's market, particularly in the LatAm region, and impact its ability to gain market share. Difficulty in gaining market share and weaker execution can lead to slower growth in seat counts, translating into lower revenue, and thus, lower margins.

Traditional communication: Ability to maintain profitability since this represents an important cash cow for the firm.

In conclusion, IDT Corporation presents a compelling investment opportunity driven by the potential spin-offs of its three high-margin, rapidly growing businesses: NRS, BOSS Money, and Net2Phone (N2P). While the decision to postpone these spin-offs reflects management's prudent approach in awaiting favorable market conditions for optimal valuation, the company continues to excel in running these businesses efficiently.

Notably, in 2Q24, these businesses achieved self-sustainability, eliminating the need for new cash investments to fuel their growth. This milestone not only strengthens the company's balance sheet but also allows for more efficient resource allocation, potentially accelerating growth in other areas or enhancing shareholder returns. Furthermore, initiating dividends during the quarter underscores management's commitment to returning value to shareholders.

As each business segment continues to demonstrate robust performance and resilience, IDT's future prospects remain promising. With prudent cash management strategies and a commitment to shareholder value, the company can capitalize on growth opportunities and drive long-term value creation.

Moreover, my SOTP valuation suggests that IDT is attractively priced with a 17% upside potential. Therefore, I rate IDT as a "buy," believing that the company's strategic initiatives and solid fundamentals will continue to drive shareholder value in the foreseeable future.