pidjoe

pidjoe

The BlackRock Utilities, Infrastructure & Power Opportunities Trust (NYSE:BUI) is a closed-end fund that aims to provide its investors with a high level of current income by investing in a portfolio of common equity securities issued by companies that traditionally have higher yields than most other things in the market. This is not an altogether bad strategy, as it allows for the generation of income while still retaining some exposure to the upside potential of common equities. In addition, many utilities tend to raise their dividend yields every year, so the fund's income should grow with the passage of time. This is, therefore, somewhat better in an inflationary environment than a fixed-income fund would possess. After all, most fixed-income securities do not change their coupon payments and they almost never raise them just because the issuing company's profits rise.

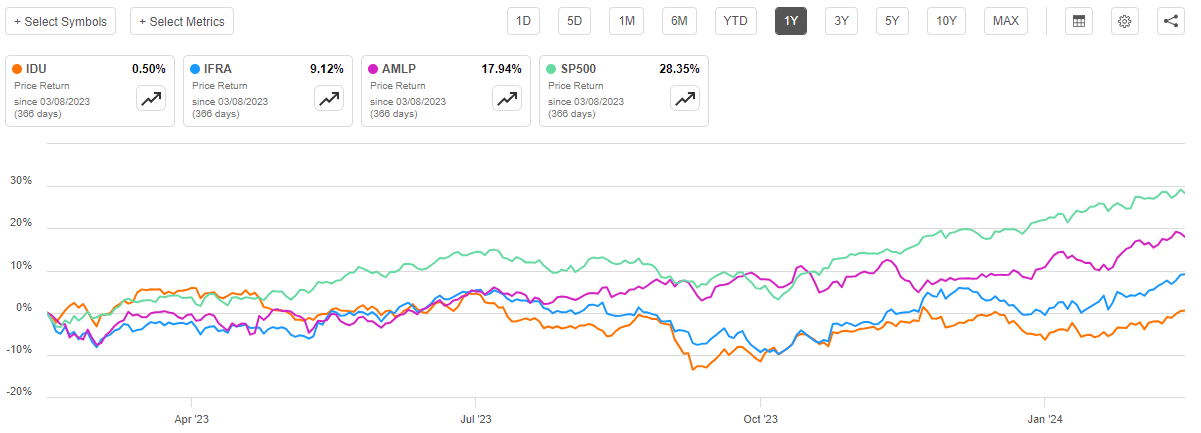

Unfortunately, the strategy has not been especially impressive recently as the utility sector in general was one of the worst-performing ones in the market over the past year. Infrastructure plays managed to do a bit better, though. Master limited partnerships also performed pretty well over the past year, but this fund does not invest too heavily in those. We can see this quite simply in this chart that compares the iShares U.S. Utilities ETF (IDU), the iShares U.S. Infrastructure ETF (IFRA), and the Alerian MLP ETF (AMLP) to the S&P 500 Index (SP500) over the past twelve months:

Seeking Alpha

As we can clearly see, all three of the various infrastructure index funds underperformed the market by a wide margin. The utilities sector barely managed to eke out a gain over the period. Unfortunately, this underperformance will do little to aid in our thesis of investing in infrastructure unless we are talking specifically about energy master limited partnerships, and as already mentioned this fund does not invest in those to any great degree. We will see that later in this article.

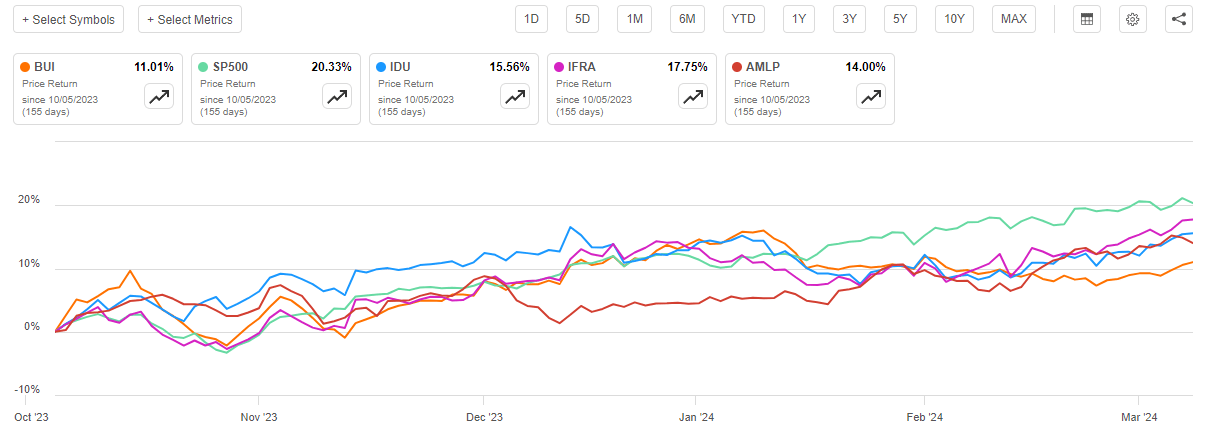

As regular readers may remember, we last discussed the BlackRock Utilities, Infrastructure & Power Opportunities Trust in early October 2023. As infrastructure has generally not been the best-performing sector over most of the past year, we might expect that the fund's own performance has been rather disappointing. However, it still managed to see its share price appreciate by 11.01% since the date that my previous article on this fund was published. That is not a bad performance over a six-month period, although it did underperform all of the index funds shown above:

Seeking Alpha

This is almost certainly going to disappoint many investors, including those who are willing to sacrifice a bit of capital appreciation in exchange for a high yield. After all, some of the index exchange-traded funds shown in the chart above have respectable yields:

Fund | TTM Distribution Yield |

iShares U.S. Utilities ETF | 2.72% |

iShares U.S. Infrastructure ETF | 1.90% |

Alerian MLP ETF | 7.58% |

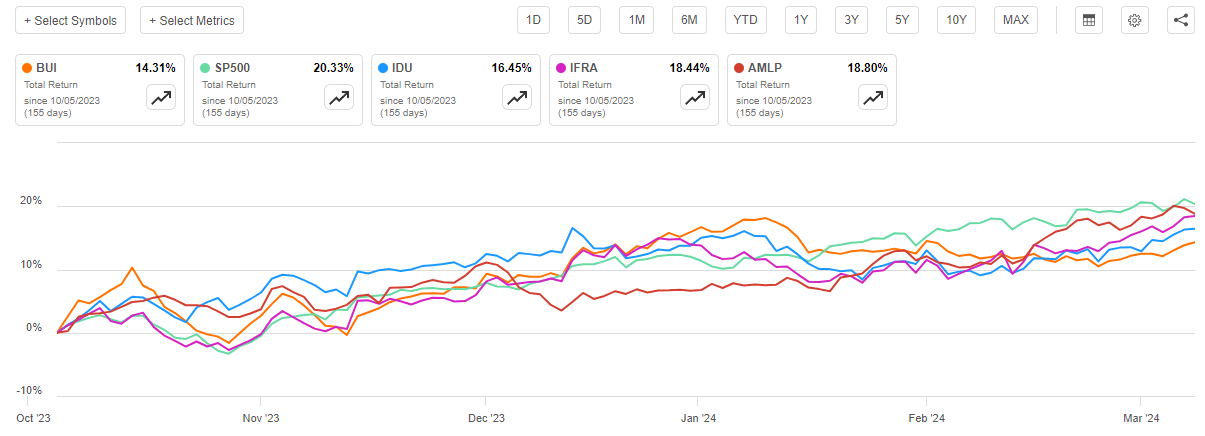

The BlackRock Utilities, Infrastructure & Power Opportunities Trust currently yields 6.82% so it does not manage to beat the Alerian MLP ETF. However, it does manage to outperform both the utilities and the broader infrastructure index funds in terms of yield. That is quite important because the yield of the fund represents a very real return to its investors. As a result of the regular payments that the fund makes to its shareholders, the actual performance realized by the fund's investors will generally be quite a bit better than the share price performance indicates.

When we take the fund's distributions into account, we get this performance chart:

Seeking Alpha

This is still, unfortunately, rather disappointing. The BlackRock Utilities, Infrastructure & Power Opportunities Trust clearly underperformed the comparable American indices even when we take the fund's much higher yield into account. That will undoubtedly reduce the fund's appeal in the minds of many investors, and it certainly does not reflect well on the fund overall. However, past performance is not necessarily an indicator of future results and this is only a relatively short snapshot of time so the fund might still be worth investigating further.

According to the fund's webpage, the BlackRock Utilities, Infrastructure & Power Opportunities Trust has the primary objective of providing its investors with a very high level of after-tax total return. As is usually the case with BlackRock funds, the website includes a very detailed description of how the fund intends to achieve this goal:

BlackRock Utilities, Infrastructure & Power Opportunities Trust's investment objective is to provide total return through a combination of current income, current gains and long-term capital appreciation. The Trust seeks to achieve its investment objective by investing primarily in equity securities issued by companies that are engaged in the Utilities, Infrastructure, and Power Opportunities business segments anywhere in the world and by utilizing an option writing (selling) strategy in an effort to enhance current gains. The Trust considers the 'Utilities' business segment to include products, technologies and services connected to the management, ownership, operation, construction, development or financing of facilities used to generate, transmit or distribute electricity, water, natural resources or telecommunications and the 'Infrastructure' business segment to include companies that own or operate infrastructure assets or that are involved in the development, construction, distribution or financing of infrastructure assets. The Trust considers the "Power Opportunities" business segment to include companies with a significant involvement in, supporting, or necessary to renewable energy technology and development, alternative fuels, energy efficiency, automotive and sustainable mobility and technologies that enable or support the growth and adoption of new power and energy sources. Such companies may include, among others, electrical equipment producers (such as wind turbine manufacturers), producers of industrial or specialty chemicals (such as building installation producers), and semiconductor and equipment companies (such as solar panel manufacturers). Under normal circumstances, the Trust invests a substantial amount of its total assets in foreign issuers, issuers that primarily trade in a market located outside the United States or issuers that do a substantial amount of business outside the United States. The Trust may invest directly in such securities or synthetically through the use of derivatives.

We can immediately see here a few things that could have had an adverse impact on the fund's recent performance relative to the index. For example, the strategy description specifically states that the BlackRock Utilities, Infrastructure & Power Opportunities Trust writes call options against a portion of its portfolio. A covered call strategy has an adverse impact on a fund's ability to benefit from stock price gains because it caps them. If the stock price goes above the strike price of the option before the option expires then the fund will have to either buy back the option or end up with the common stock getting called away when the option is exercised. In either case, a fund employing this strategy will have lower gains than a fund that is not running a covered call option strategy if the stocks in the portfolio appreciate sufficiently. Over most of the past six months, we have experienced a very strong bull market as investors are seemingly buying anything that they can get their hands on. The fund's covered call-writing strategy has reduced the fund's ability to fully capitalize on this market rally, and thus could be contributing to its recent underperformance. Fortunately, the fund is not overly dependent on its options strategy as a source of income, as it only has 32.89% of its portfolio overwritten as of the time of writing. That is lower than many funds that employ this particular strategy, but it does still cap the upside potential compared to a fund that is not using derivatives.

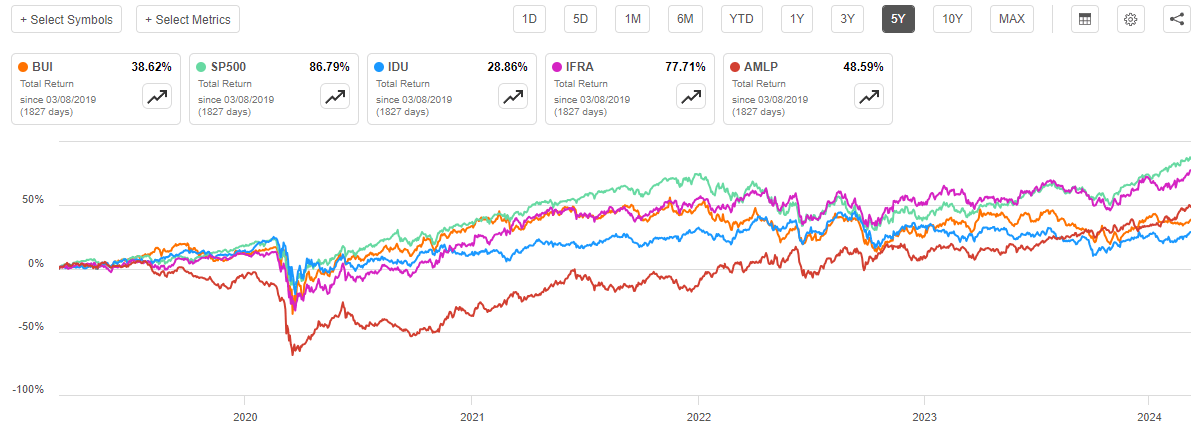

With that said, the fund's underperformance relative to the indices is not exactly a new phenomenon. As we can see here, the fund underperformed both the U.S. Infrastructure Index and the Alerian MLP Index over the past five years. It did manage to outperform American utilities, though:

Seeking Alpha

This is a period of time that included the COVID-19 lockdowns that crashed the price of midstream energy partnerships, such as the ones that are included in the Alerian MLP Index. The fact that the BlackRock Utilities, Infrastructure & Power Opportunities Fund still underperformed that index is thus something that certainly will reduce the fund's appeal in the eyes of any investor (especially since the Alerian MLP Index has a higher yield).

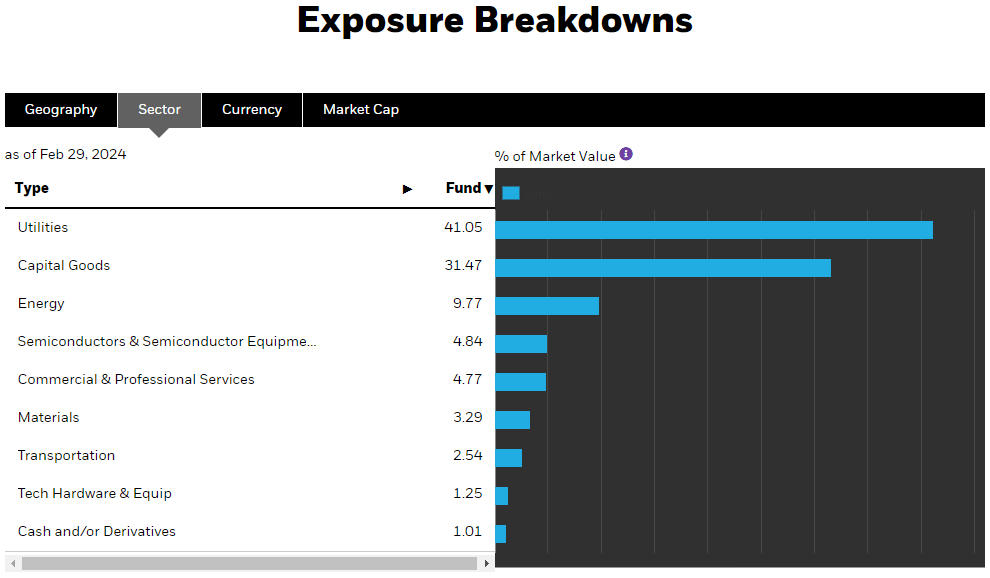

In our previous article on this fund, we saw that roughly half of the fund was invested in utilities. This is still the case, although the fund's allocation to these companies has been reduced a bit. Here is the sector allocation as of the time of writing:

BlackRock

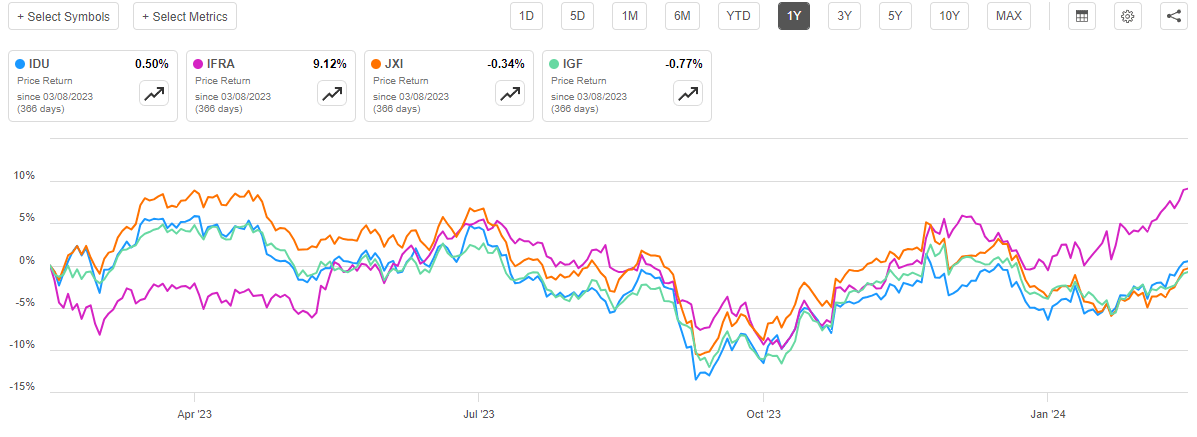

As we can clearly see, 41.05% of the fund's assets are invested in the utility sector. When we previously discussed it back in October, the fund's allocation to the utility sector was 49.45% of its total assets, so clearly its allocation to that sector has decreased significantly. This is somewhat understandable for two reasons. The first of these is that utilities in general have been underperforming the rest of the broader market for quite some time. This is clearly shown in this chart showing the iShares U.S. Utilities ETF against the iShares U.S. Infrastructure ETF over the past year:

Seeking Alpha

For good measure, I also included the iShares Global Utilities ETF (JXI) and the iShares Global Infrastructure ETF (IGF) on this chart because the BlackRock Utilities, Infrastructure & Power Opportunities Trust invests in both American and foreign companies. We can clearly see that both the American and global utilities indices underperformed American infrastructure. However, the worst performer here was the global infrastructure index. We also see that both global indices underperformed the American indices, which actually could account for another cause of the BlackRock Utilities, Infrastructure & Power Opportunities Trust's underperformance relative to other options that many American investors would consider as alternative potential investments.

When we consider this, it makes a great deal of sense for the fund to be reducing its exposure to utilities in favor of other infrastructure assets. However, it is not certain whether the management is making a conscious decision to reduce exposure to the underperforming utility sector or if this is simply a result of the other things held by the fund outperforming its utility sector holdings. The fund only had an annual turnover of 31.00% in the full-year 2023 period, so it does not seem to be engaging in a great deal of trading activity. There is still some room here to allow for some intentional efforts by the fund to reduce its exposure to underperforming stocks, but it seems most likely that the reduction to utilities that we see over the past six months was caused by a combination of performance differences and intentional trading activity.

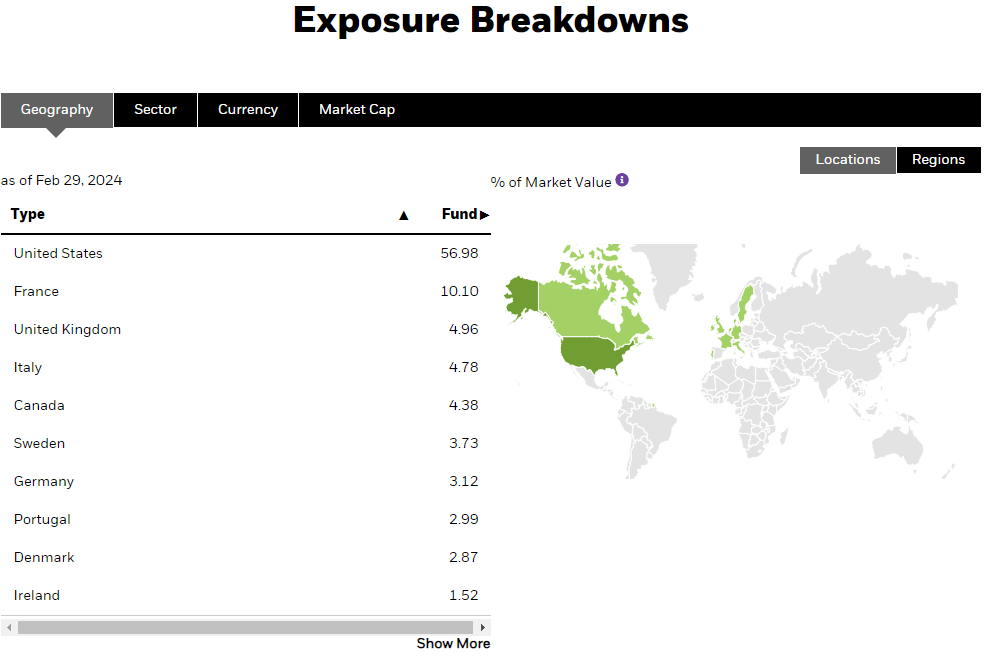

The description of the fund's strategy found on the webpage (quoted above) states that the BlackRock Utilities, Infrastructure & Power Opportunities Trust invests a significant percentage of its assets in non-American companies. However, as is frequently the case with closed-end funds that make this claim, the fund still has more than half of its assets invested in domestic companies:

BlackRock

This results in a 43.02% weighting to non-American companies. I would not call that a "significant percentage" as the fund claims. After all, the United States is responsible for a bit less than a quarter of the global domestic product, so the fund is still overweight to the country relative to its actual representation in the global economy. However, the iShares Global Utilities ETF, which tracks the S&P Global 1200 Utilities Capped Index, has a 63.29% weighting to the United States so the fund is underweight to America compared to that index. It is substantially overweight versus the iShares Global Infrastructure ETF, which tracks the S&P Global Infrastructure Index:

Index | United States % Weighting |

S&P Global 1200 Utilities Capped Index | 63.29% |

S&P Global Infrastructure Index | 38.16% |

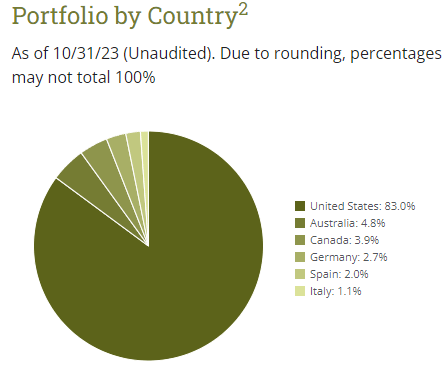

This is actually a bit disappointing because one of the biggest problems faced by American investors is that they tend to be very heavily exposed to their home country. This causes them to have some risks that could be easily avoided by achieving more international exposure. The BlackRock Utilities, Infrastructure & Power Opportunities Trust unfortunately does not completely solve this problem, as it still has more than half of its assets in the United States. However, it is still better than some similar funds that claim to be global funds. For example, the Duff & Phelps Utility and Infrastructure Fund (DPG) currently has 83.0% of its assets invested in the United States:

Duff & Phelps

Thus, the BlackRock Utilities, Infrastructure & Power Opportunities Trust could be an option for those investors who are looking to access opportunities and markets outside of the United States, but it is still not as good at this as it could be.

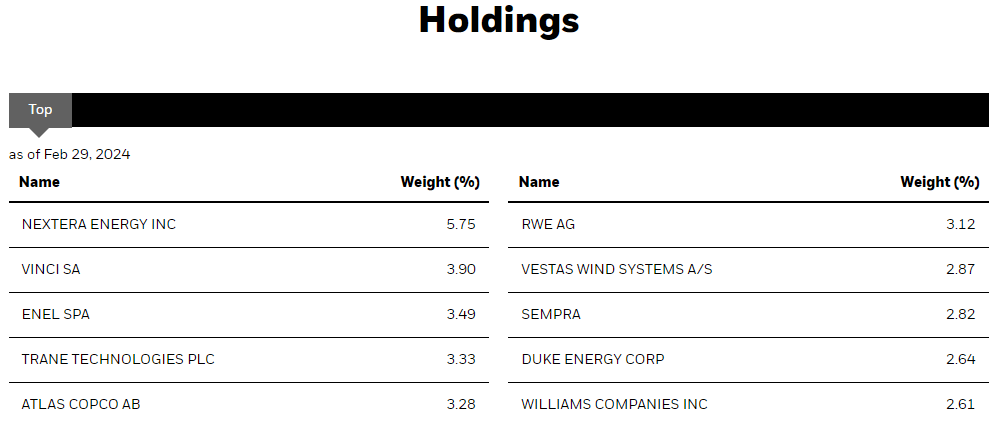

Let us have a look at the changes to the fund's largest holdings since the last time that we discussed the BlackRock Utilities, Infrastructure & Power Opportunities Trust. Here are the largest holdings in the fund's portfolio as of today:

BlackRock

There have been a surprising number of changes to the fund's largest positions over the past six months when we consider its low 31.00% annual turnover. In particular, we see the following removals and additions:

Removed Holding | Added Holding |

Waste Management (WM) | Trane Technologies (TT) |

Cheniere Energy (LNG) | Atlas Copco (OTCPK:ATLKY) |

American Electric Power (AEP) | Vestas Wind Systems (OTCPK:VWDRY) |

Exelon (EXC) | Duke Energy (DUK) |

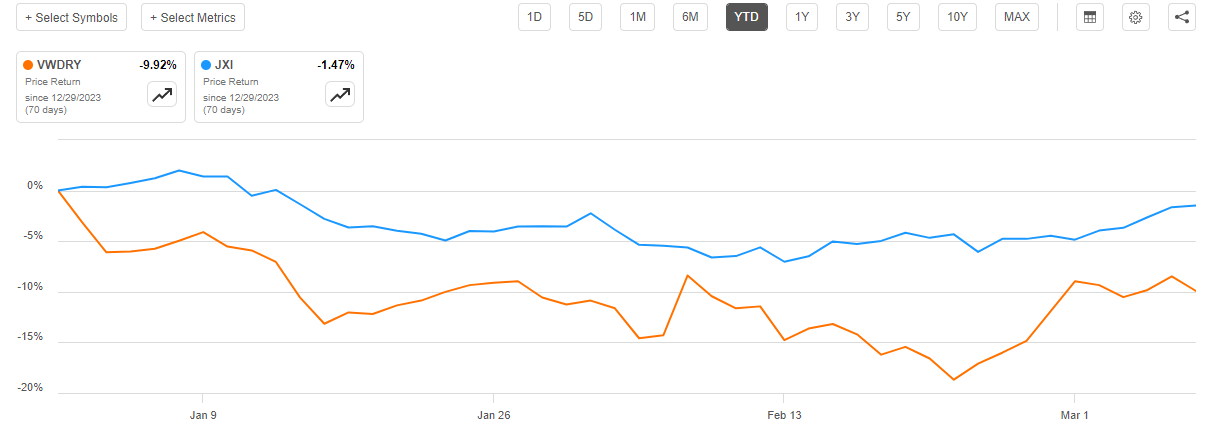

In addition to this, there have been a number of weighting changes over the trailing six-month period, but there are many things that could account for this, such as one stock outperforming another in the market. I will admit that I am not a fan of all of these changes. The one that most catches my eye here is the addition of Vestas Wind Systems. Wind power companies have been struggling severely in the high-interest rate environment as despite numerous government subsidies, they are still finding it quite difficult to actually earn a profit from wind power development. This has weighed on Vestas Wind Systems' stock price, as the company's shares are down 9.92% year-to-date:

Seeking Alpha

The company did recently announce an earnings beat and managed to swing to a profit in the fourth quarter so it is not all bad, but clearly, the stock could have proven to be a major drag on the fund's portfolio depending on when it acquired its position. I would rather it have kept that position in Cheniere Energy, as the fundamentals for liquefied natural gas are still very good despite the White House halting approvals for the construction of new export facilities. Indeed, that approval halt may actually benefit Cheniere Energy as it removes some of the new capacity that was expected to come online over the remainder of this decade.

One of the biggest attractions of utilities and infrastructure companies in general is that they tend to have fairly high yields compared to many other things in the market. This is largely due to the slow growth rate of many of these companies. It takes a lot of time and expense to construct utility or other infrastructure, so it is not often done unless the existing infrastructure cannot meet the current demand. The basic model followed by these companies is to pay the high upfront expense of construction and then receive a steady stream of cash from their infrastructure assets over the following years. As a result, these companies do not have very high-growth rates, and they generate far more cash than can be realistically redeployed into their businesses. As a result, they simply pay a sizable proportion of it out to their investors. The market does not tend to assign high multiples to most infrastructure companies due in part to their low growth rates, so the dividends tend to account for a high percentage of the stock price.

The BlackRock Utilities, Infrastructure & Power Opportunities Trust invests its assets in these companies and so is naturally the recipient of the dividends that they pay out. This serves as a source of income for the fund, but it does not stop here. It also writes call options against some of the stocks that it holds in its portfolio, with the basic intent being to receive a premium from the sale of the option. Those premiums serve as an additional source of income for the fund, although they could be wholly or partially erased if the fund has to buy back the option to avoid having it exercised. These premiums can serve as a very large synthetic dividend from a stock, though, as I pointed out in a recent article. The fund combines these standard and synthetic dividends with any capital gains that it manages to realize from the appreciation of the common stocks that it holds, which it pays out to the shareholders after deducting its own expenses. We might assume that this would give the fund's shares a very high yield.

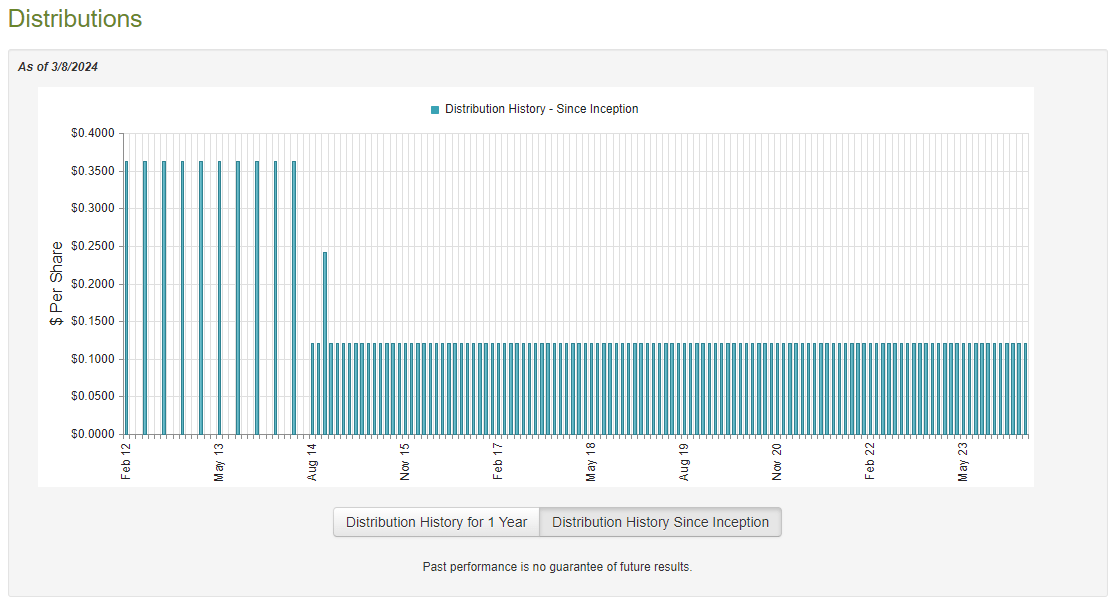

This is certainly the case as the BlackRock Utilities, Infrastructure & Power Opportunities Trust pays a monthly distribution of $0.1210 per share ($1.452 per share annually), which gives it a 6.82% yield at the current price. As mentioned in the introduction, this is considerably higher than most index funds that invest in utilities or infrastructure, although admittedly, it cannot compare to some energy infrastructure partnerships. One thing that might be very appealing though is that this fund has been remarkably consistent with respect to its distribution over the years:

CEF Connect

As we can clearly see here, the BlackRock Utilities, Infrastructure and Power Opportunities Trust has not had to cut its distribution since its inception. The apparent reduction that we see in the chart above was caused by the fund switching from a $0.3625 per share quarterly distribution to a $0.1210 per share monthly one. The actual amount paid out during a given three-month period actually increased by $0.0005 as a result. Therefore, there was no distribution cut. This will undoubtedly appeal to any investor who is seeking to receive a safe and stable income from the assets in their portfolios. However, in today's inflationary environment, a stable distribution is less attractive than a growing one because the purchasing power of a stable distribution is constantly decreasing due to inflation. This can easily be overcome by reinvesting some of the distributions, but that still reduces the money that is available to spend on bills or enjoyment. This is still a far better history than most closed-end funds that have had to cut their payouts over their lifetimes, however.

As is always the case, we should have a look at the fund's finances to ensure that it can actually afford the distribution. After all, we do not want the fund to be distributing more than it is able to earn from the assets in its portfolio because that will deplete the fund's net asset value. A fund cannot indefinitely sustain net asset value destruction, so we do not want to see that in any fund that we are hoping to use as a long-term income vehicle.

Fortunately, we have a fairly recent document that we can consult for the purpose of our analysis. As of the time of writing, the most recent financial report for the BlackRock Utilities, Infrastructure & Power Opportunities Trust corresponds to the full-year period that ended on December 31, 2023. This is a much newer report than the one that we had available to us the last time that we discussed this fund, which is quite nice to see. After all, the second half of 2023 was not exactly friendly to utilities, as rising yields over the summer punished most of the companies in the sector. This almost certainly imposed some realized or unrealized losses on this fund, and this report will give us a much better idea of how well the fund handled that environment than we had previously. In addition, it is always nice to have recent information when determining a fund's ability to sustain its distribution.

During the full-year period, the BlackRock Utilities, Infrastructure & Power Opportunities Trust received dividends totaling $13,872,731 and surprisingly nothing in interest. It did have some securities lending income, though, as well as some foreign withholding tax liability that we need to deduct from its investment income. Overall, the fund reported a total investment income of $13,219,835 for the full-year period. It paid its expenses out of this amount, which left it with $7,841,668 available for the shareholders. As might be expected, that was nowhere near enough to cover the fund's distributions as the fund distributed a total of $32,524,989 over the full-year period. At first glance, this may be concerning, as the fund clearly does not have sufficient net investment income to fully cover its shareholder distributions.

However, the fund does have other methods through which it can obtain the money that it needs to cover its distributions. For example, the fund might be able to realize some capital gains by selling appreciated stock in a friendly market. The fund also receives a certain amount of premium income from the sale of call options. Realized capital gains and options premiums are not considered to be investment income for tax or accounting purposes, but they obviously do cause money to come into the fund that can be paid out to the investors.

The fund did, fortunately, have a reasonable amount of success at earning money via these alternative sources. For the full-year 2023 period, the fund reported net realized gains of $19,192,335 and another $9,049,746 net unrealized gains. Overall, the fund's net assets increased by $8,068,964 after accounting for all inflows and outflows during the period. This net asset increase would have happened even if the fund had not conducted an offering of new shares during the period. Its net investment income, net realized gains, and net unrealized gains totaled $36,083,749 so it still managed to cover its distribution independently of the capital raise. However, it did have to partially depend on net unrealized gains to cover the payout, so we still want to keep an eye on it as there is no guarantee that unrealized gains will become permanent.

For now, the market overall seems strong, so we probably do not need to worry too much about a distribution cut.

As of March 7, 2024 (the most recent date for which data is currently available), the BlackRock Utilities, Infrastructure & Power Opportunities Trust has a net asset value of $22.13 per share but the shares trade at $21.28 each. This gives the fund's shares a 3.84% discount to net asset value at the current price. This is in line with the 3.42% discount that the shares have averaged over the past month, so the current price seems reasonable for anyone who wants to add this fund to their portfolios.

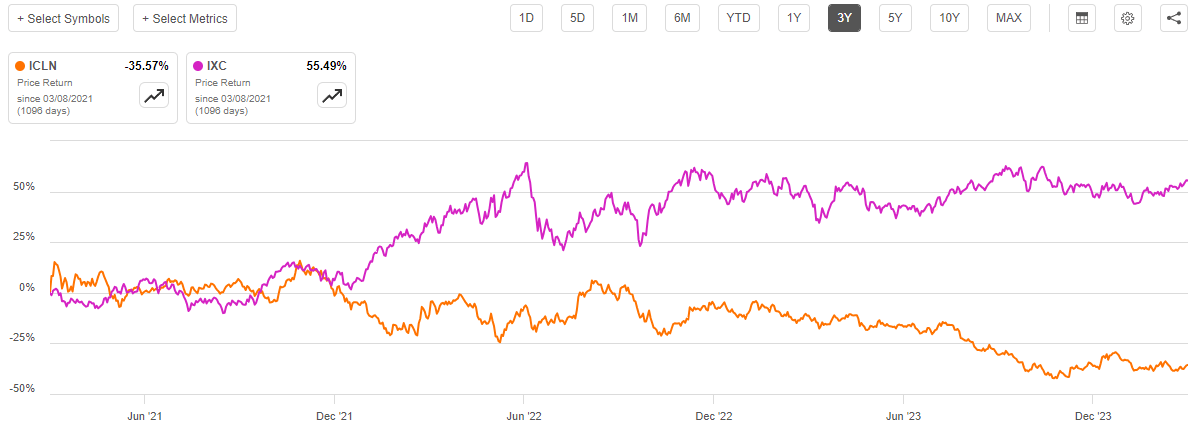

In conclusion, the BlackRock Utilities, Infrastructure & Power Opportunities Trust is one of the more reliable utility closed-end funds available on the market as it has not cut its distribution over the past several years nor does it appear that it needs to. The covered call-writing strategy may help with this, but unfortunately, it may also be one of the reasons why the fund is lagging behind some of the comparable indices. I will admit that I am not too sure about some of the recent portfolio changes, as this fund seems to be suffering from the same problems as other infrastructure funds in that it has marked favoritism for renewable energy despite that sector lagging behind traditional hydrocarbon energy since 2022. We can see this very clearly by comparing the iShares Global Clean Energy ETF (ICLN) against the iShares Global Energy ETF (IXC) over the past three years:

Seeking Alpha

It is fully covering its distribution though, which is nice, as is the fact that the fund is trading at a discount on its net asset value.

Overall, I do not see any compelling reason to rush out and buy this fund today, but I also cannot see a reason to dump it. As such, maintaining the hold rating seems to be the most appropriate today.