Khanchit Khirisutchalual

Khanchit Khirisutchalual

I award a Hold rating to iClick Interactive Asia Group Limited's (NASDAQ:ICLK) stock.

An offer made to acquire iClick's shares that is currently being considered by the company's board, and ICLK's current share repurchase program in effect until the end of the year, suggests to me that the company's stock price has limited downside. But the upside potential for iClick is capped by the fact that the company's Q4 2022 financial performance is likely to have been poor. This is why I have chosen to assign a Hold investment rating to ICLK.

In its 20-F filing, iClick describes itself as a Chinese "enterprise and marketing cloud platform" that provides services such as "traffic acquisition, customer relations management and business decisions optimization."

ICLK generated 61% and 39% of the company's Q3 2022 top line from marketing solutions and enterprise solutions, respectively as revealed in its most recent quarterly earnings presentation. According to its 20-F filing, iClick's core marketing solutions business was first started in 2009, and it only ventured into enterprise solutions a couple of years ago in mid-2018.

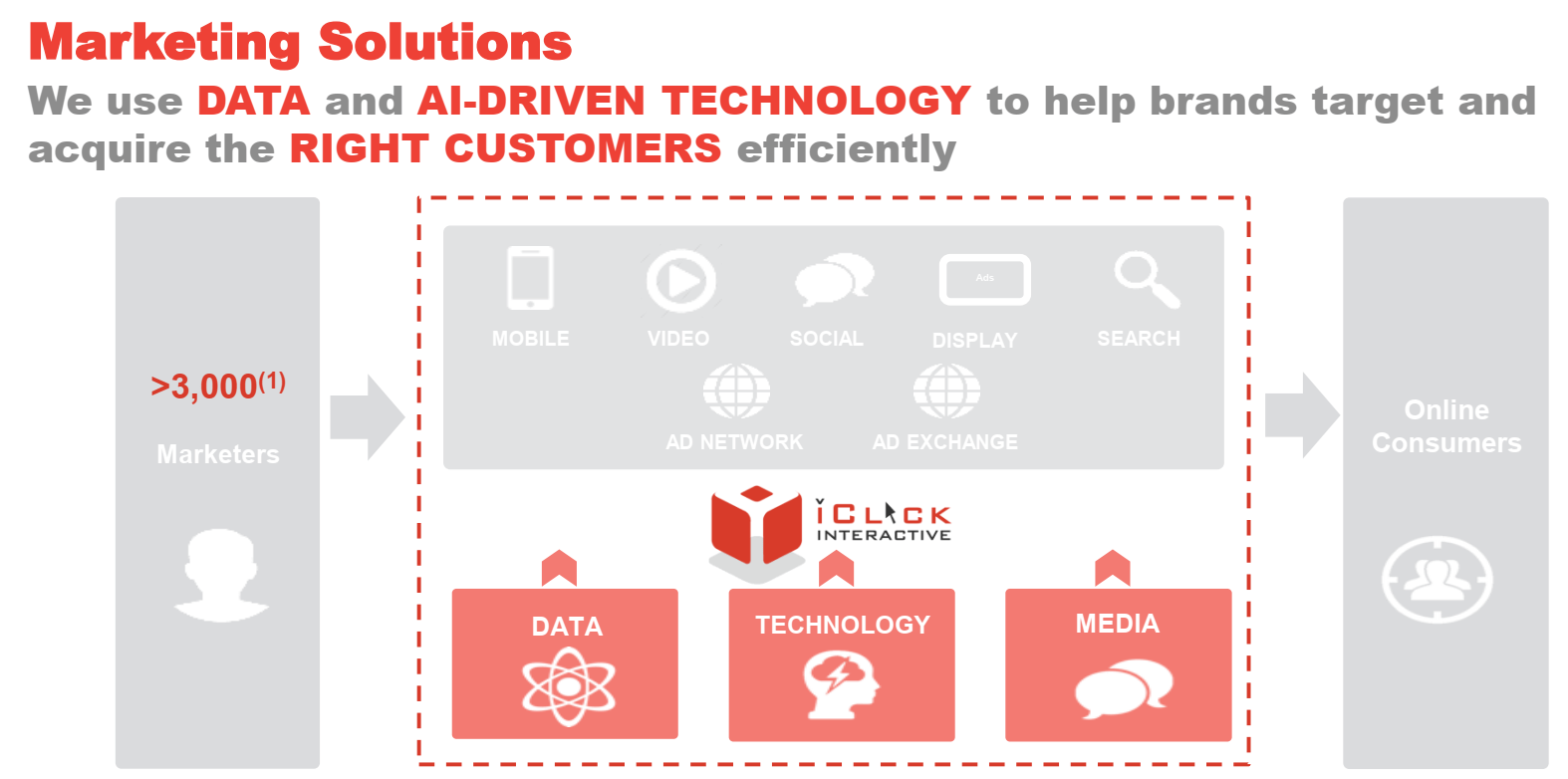

An Overview Of iClick's Core Marketing Solutions Business

ICLK's Q3 2022 Results Presentation

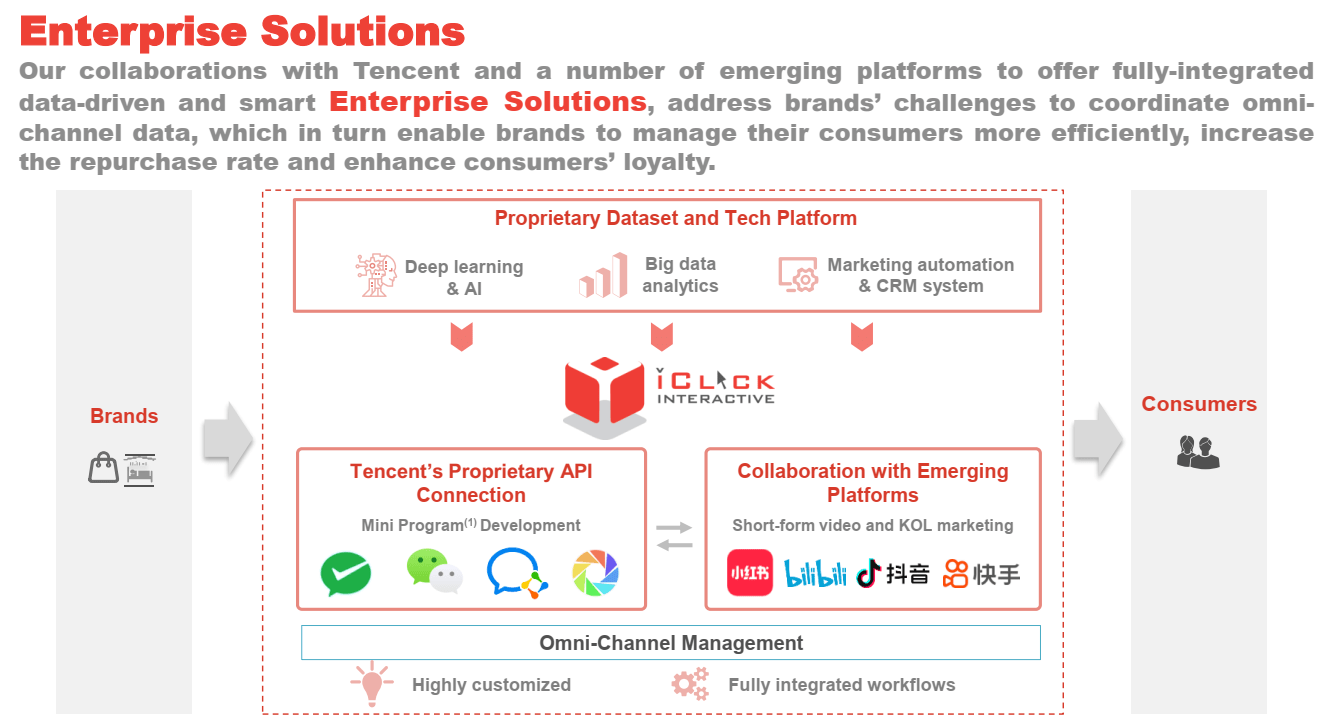

A Brief Description Of ICLK's Enterprise Solutions Business

ICLK's Q3 2022 Results Presentation

iClick is expected to reveal the company's financial performance for the last quarter of the prior year later this month on March 23, 2023, after trading hours. Q4 2022 should have been a very difficult quarter for ICLK.

As per the sell-side analysts' consensus financial forecasts taken from S&P Capital IQ, the market sees ICLK reporting a big drop in revenue and staying loss-making in the most recent quarter. Specifically, the analysts forecast that iClick's top line will drop significantly by -46.0% YoY from $76.3 million for the fourth quarter of 2021 to $41.2 million in Q4 2022. This is equivalent to a marginal +0.4% revenue growth in QoQ terms. The sell-side also estimate the iClick's non-GAAP adjusted net loss per share will widen substantially from -$0.30 in Q4 2021 to -$0.95 in the recent quarter.

China's prior COVID-zero policy and strict pandemic control measures should have had an adverse impact on iClick's top line performance in the fourth quarter of last year. Apart from that, ICLK's internal business restructuring might also have hurt the company's revenue growth in Q4 2022. iClick disclosed at the company's earlier Q3 2022 results briefing on November 30 last year that it had made the decision to exit the "the higher risk businesses within our Marketing Solutions segment."

In relation to the profitability outlook, ICLK has taken actions to make sure its key clients stay with the company in this tough operating environment, and this will inevitably be a drag on its profit margins. At its third quarter earnings call in end-November 2022, iClick acknowledged that it has provided "discounts" and "more Enterprise Solutions services to existing customers" as part of its new client retention approach. As an indication of how these changes have already affected its profitability, ICLK's gross profit margin had already contracted from 25.0% in Q3 2021 and 24.3% in Q2 2022 to 22.4% for Q3 2022.

In a nutshell, I think that the probability of iClick reporting better than expected Q4 2022 financial performance in late March is pretty low. At best, ICLK will announce in-line results on March 23. In other words, I don't expect any positive surprises associated with iClick's fourth quarter earnings announcement.

Recent corporate actions should provide some form of support for iClick's share price in the very near term, even though ICLK's Q4 2022 financial results are expected to be poor as detailed in the previous section.

In late-January this year, ICLK issued a press release disclosing that the company had appointed a "financial advisor and a legal counsel" to assess a "takeover bid" by a group of shareholders (including ICLK's CEO) for iClick's shares at $4.0672 apiece.

The good news is that iClick's shares are currently trading below the takeover offer price, which implies there is potential upside for ICLK stock at current price levels.

The bad news is that the takeover bid price represents an unattractive 11% premium over ICLK's last traded stock price of $3.67 as of March 2, 2023, and there is no certainty that this takeover bid will be successful. As an example, another US-listed Chinese company So-Young International (SY) saw an privatization offer for SY being rescinded in late 2022. As the delisting risk for Chinese ADRs is mitigated as a result of recent developments on audit checks, and China gradually reopens its economy, there is a reasonably high likelihood that the current takeover bid for US-listed Chinese company ICLK will be reconsidered.

Assuming that the takeover bid doesn't proceed, ICLK's $5 million share repurchase program in effect for calendar year 2023 could still help to keep the company's shares afloat. The $5 million buyback is pretty significant, as it is equivalent to roughly 14% of iClick's current market capitalization. In addition, ICLK's current valuations are not particularly demanding with its shares valued by the market at a mere 0.23 times consensus forward next twelve months' price-to-sales.

A Hold rating for iClick is justified. I have considered the positives associated with recent corporate actions and the negatives linked to the company's upcoming results in determining my Neutral rating for ICLK's shares.

Editor's Note: This article covers one or more microcap stocks. Please be aware of the risks associated with these stocks.