filo/iStock via Getty Images

filo/iStock via Getty Images

Since my last look in August, ImmunityBio (NASDAQ:IBRX) has continued to be a volatile stock. Its stock is up 100% since my "Sell" recommendation, and we've had some developments. So, it's time to reassess.

The company inches closer to Anktiva's PDUFA data (April 23rd) for the treatment of nonmuscle invasive bladder cancer. Recall that the original CRL was due to manufacturing issues (which are, typically, easier to fix compared to data issues). Anktiva figures to enter a competitive market, with Merck's (MRK) Keytruda being a leader. However, Anktiva's robust activity in combination with BCG likely will make it a key player in the treatment of high-risk non-muscle-invasive bladder cancer (NMIBC) patients, specifically, after failure with BCG monotherapy. This may be a blockbuster opportunity for Anktiva (>$1 billion in revenue per year), which is a biologic and, therefore, afforded 12 years of market exclusivity.

A major issue for ImmunityBio has been its financial situation, which has improved since August but with notable caveats. For one, the stock has seen more dilution. In January, ImmunityBio announced a Revenue Interest Purchase Agreement (RIPA) with Infinity. The deal gives ImmunityBio $200 million in upfront capital and an additional $100 million upon the FDA approval of Anktiva. However, the company will forfeit a tiered percentage of sales for up to 12 years, until Infinity sees a 195% return on investment. If Anktiva royalties do not satisfy this requirement, according to my understanding of the agreement, ImmunityBio will have to make up for it one way or another.

If the Purchasers have not received Total Revenue Interest Payments equal to 195% of the then Cumulative Purchaser Payments on or before the twelfth anniversary of the RIPA, then the Company shall be obligated to pay to the Purchasers an amount equal to 195% of the then Cumulative Purchaser Payments less the Total Revenue Interest Payments made as of such date.

ImmunityBio may opt to increase royalty percentages at any time to meet the obligation, or could simply pay in cash. Moreover, they could terminate the RIPA and buy the royalty rights back. The deal also places restrictions on ImmunityBio's ability to incur additional debt and asset sales (page 3). Although I have done my best to highlight the main issues, the agreement is significantly more intricate than what I have described and is fairly complicated overall.

In connection with the RIPA, a $10 million stock purchase and option agreement and possibly another $10 million are included.

Overall, I think ImmunityBio is taking a risk with this transaction. While it gives ImmunityBio's short-term liquidity a much-needed boost, it complicates the company's already convoluted finances and may eventually reduce its strategic options.

According to ImmunityBio's balance sheet as of September 30, the combined liquid assets total approximately $190.6 million, including $177.96 million in cash and cash equivalents and $11.83 million in marketable securities. When juxtaposed against its debts-such as $19.82 million in accounts payable, $64.87 million in accrued expenses, and significant long-term liabilities including $480.02 million in related-party promissory notes and $165.29 million in related-party convertible notes-its financial health demands scrutiny.

The current ratio, calculated by dividing total current assets by total current liabilities, stands at approximately 2.38, indicating a relatively comfortable liquidity position in the short term. This was further strengthened following the RIPA.

Over the last nine months, ImmunityBio reported a net cash used in operating activities of $251.49 million, translating to a monthly cash burn rate of approximately $27.94 million. Given the liquid assets, before considering the January update, the cash runway extends roughly 6.8 months. Keep in mind that this is an estimate based on historical data, and the $300 million infusion from the RIPA significantly extends this runway.

Based on the cash burn and the recent capital raise, the immediate need for additional financing appears mitigated, lowering the odds of requiring further funds within the next twelve months to medium.

According to Seeking Alpha data, with a market capitalization of $2.35 billion and revenue projections showing an increase from $508k in 2023 to $134.3 million by 2025, the growth prospects appear significant. The stock's momentum has been mixed compared to SPY, showcasing a -16.47% performance over the last 3 months but a notable +27.74% over the last year, indicating volatility and potential resilience.

Per Fintel, the short interest is substantial at 43,933,702 shares, representing 31.55% of the float, which indicates skepticism from some market participants or potential for a short squeeze. Institutional ownership is modest at 8.63%, with notable movements including 28 new positions and 15 sold-out positions, highlighting a dynamic institutional interest. Noteworthy institutions like State Street and Geode Capital Management have increased their holdings significantly, suggesting growing institutional confidence. Insider trades reveal compelling net activity with a massive increase in holdings over the past twelve months, indicating strong insider belief in the company's future.

Given the conflicting information above, the market sentiment around the company can be classified as "mixed."

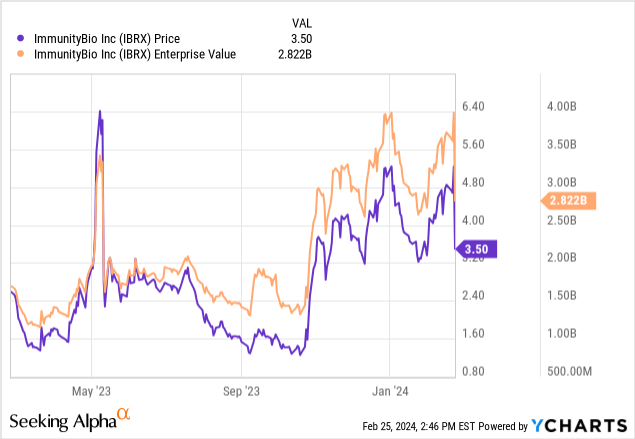

In conclusion, while the recent events have mitigated immediate liquidity concerns, they also add to the complexity of the financial situation for ImmunityBio. Moreover, dilution remains very relevant. After all, it is atypical for a $3.50/share stock to be valued over $2 billion. This usually indicates massive past dilution. So, while Anktiva is a promising asset with an extended life cycle, in my view, the ongoing financial concerns and regulatory/market risks lean considerably in the negative. Importantly, ImmunityBio's valuation isn't, by any means, "cheap." Its enterprise value of nearly $3 billion suggests the market is already pricing in great odds for regulatory and market success.

Given these concerns, my advice remains to sell ImmunityBio. The company's financial health remains unstable, despite short-term (<12 months) improvements. Uncertainties surrounding Anktiva's approval process add to the risk.

However, there are risks to my sell recommendation. Should Anktiva receive FDA approval without hitches, and if ImmunityBio manages to navigate its financial obligations efficiently, the stock could see significant upside. Additionally, the current high short interest indicates the potential for a short squeeze, which could temporarily inflate stock prices. Finally, unforeseen strategic partnerships or licensing deals could provide an additional capital influx or reduce financial burdens, improving ImmunityBio's outlook.