ArtistGNDphotography

ArtistGNDphotography

My recommendation for Installed Building Products (NYSE:IBP) stock is a buy rating. The outlook for IBP is very attractive in the near term, given the housing situation in the US. I expect housing starts to remain favorable to IBP as the US aims to close the undersupply gap. This should drive top-line growth for IBP. Coupled with a positive mix shift in products and lower cost inflation, the outlook for IBP’s margin is also attractive, and management has shown that they are capable of driving margin expansion. With this outlook, I believe the market will continue attaching multiple premiums to the stock.

IBP is a leading player in the US for the installation of insulation in the residential new construction market. This segment represents 60% of FY23 revenue. Aside from insulation, IBP also offers other complementary products like waterproofing, fireproofing, garage doors, shower doors, etc. IBP operates an end-to-end model where it manages all aspects of the installation process for customers. As of FY23, IBP had a total revenue of $2.78 billion and an operating income of $370 million. The business also has a manageable net debt position of ~%70 million, or just slightly above 1x EBITDA.

IBP reported a mixed bag of results in 4Q23, exceeding expectations on sales but falling short on operating margins. Reported and organic sales came in at 5% and -1% growth, respectively, surpassing consensus estimates of 1% and -3%. This positive performance was driven by a strong showing in the multi-family segment, with sales up 30% organically, partially offset by a decline in single-family new residential sales. Total commercial sales also saw healthy organic growth of 11%. While sales exceeded expectations, operating margins did not fare as well. While EBIT margin grew 80bps to 15.8%, this fell short of consensus expectations for 16.3%. At the bottom line, IBP reported operating EPS of $2.72, which surpassed the consensus estimate of $2.44.

In my opinion, growth is going full steam ahead based on the current performance momentum of IBP. In 2024, IBP should see the most revenue growth from new single-family construction. To give better context, the current housing undersupply situation in the US is by far the worst since the past 30 years (albeit a decent recovery recently). This, combined with the fact that the lower mortgage rates are unlikely to drive existing homeowners to sell (if not, they have to refinance at a higher rate), means that in order to close this gap, housing starts have to increase. During the call, management also noted that rate cuts will probably not cause a significant decrease in supply in the current market. Hence, my take is that the demand for housing is still going to be met by new housing, which is a tailwind to IBP.

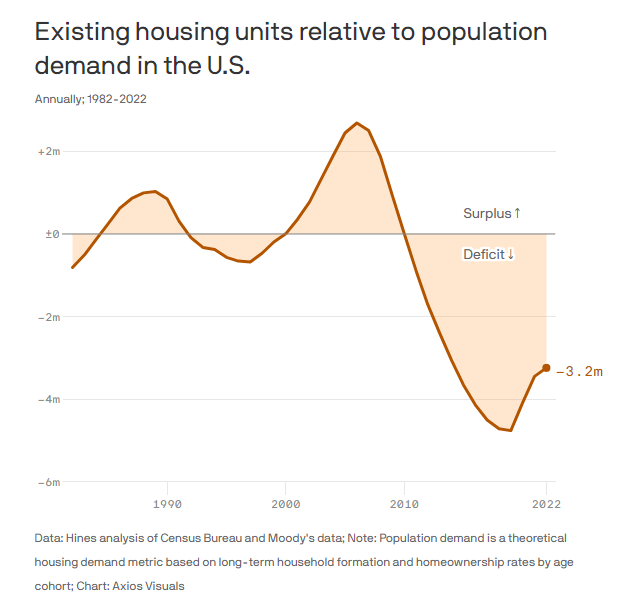

Axios Visuals

Regarding multi-family housing, I want to point out that the situation is significantly better than 2023, with rates coming down, even though management has acknowledged that starts are likely to be down in the low to mid-teens in 2024. Contrary to the bears that think growth will be weak, I anticipate that the multi-family business will outperform housing starts in 2024, thanks to IBP's backlogs that extend into 2025 and share gains. Aside from residential, the commercial side of things is also still going strong; the segment increased by a whopping 11.5% in 2023, and management is expecting even more growth in 2024.

But now, I want to back that up a little bit and just say our multifamily backlogs continue to be very strong, extremely strong. 4FQ23 earnings

One minor point to monitor regarding growth is that IBP pointed out that there might be a shortage of fiberglass insulation if single-family starts reach around 1 million. However, they also noted that manufacturers are unlikely to add additional capacity later this year, so a more severe shortage is unlikely. This, in my view, points to a possible trend of rising volume and price/mix that is closer to normalized rates over time. All in all, after years of supply chain interruptions, rising rates, and recession fears, management finally described the operating environment as "extremely healthy" on the call. As such, from a macro perspective, I am very confident in the growth outlook for IBP ahead, and this confidence is further enhanced by how management has executed so far. On the latter, management has shown that they are able to continuously capture the value provided to customers despite a weak macro backdrop (growth was up 4.1% for FY23 on the back of 36% growth in FY22).

I believe margin expansion is going to be a central focus for investors in the coming quarters, as the past three quarters of strong gross margin performance (outperforming management's guidance) convince the market that further expansion is possible. Although management guided for a change in the mix, with fewer smaller regional builders and more larger production builders, which seems margin dilutive, my view is that if inflation rates for insulation and other materials are normalized further, margins should be well supported. There are a number of additional qualitative factors that give me faith in the future possibilities for margin expansion. For example, the management's ongoing goal of raising the profitability of its heavy commercial segment has proven to be very effective thus far, as evidenced by the 2023 gross margin improvement. Along similar lines, they are working to bring the margin profile of ancillary products closer to insulation as market conditions improve; this should increase their margins. As such, all of these, combined with inherent operating leverage, make me believe that margins can expand.

Redfox Capital Ideas

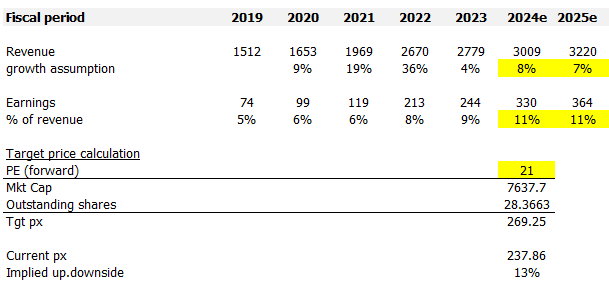

In my model, I used consensus estimates for my FY24/25 revenue and earnings assumptions. I believe consensus estimates are reliable because, historically, they have been accurate. In fact, IBP has, on average, beat consensus estimates most of the time. For revenue, reported results have beaten consensus estimates of 3% on average, and for earnings, 14% on average. As such, my estimates could be underestimating IBP growth and earnings potential. On an absolute basis, I believe the high single-digit revenue growth is achievable mainly because of the housing supply situation. If we look at the chart above, the current undersupply is around ~3 million, and assuming housing starts to accelerate in the near term to close this gap, y/y growth vs. 2023 should provide an easy comparison, easily driving low- to mid-single-digit growth from a volume perspective. This, along with IBP's ability to capture more value in the value chain, makes me believe the expected growth is doable. The margin should expand as well, as discussed above. Based on my outlook, I expect the market to continue attaching a premium multiple to IBP as it is in the “upswing mode." Hence, I model IBP to trade at 21x forward PE in the near term. This gives me a target share price of~ $270.

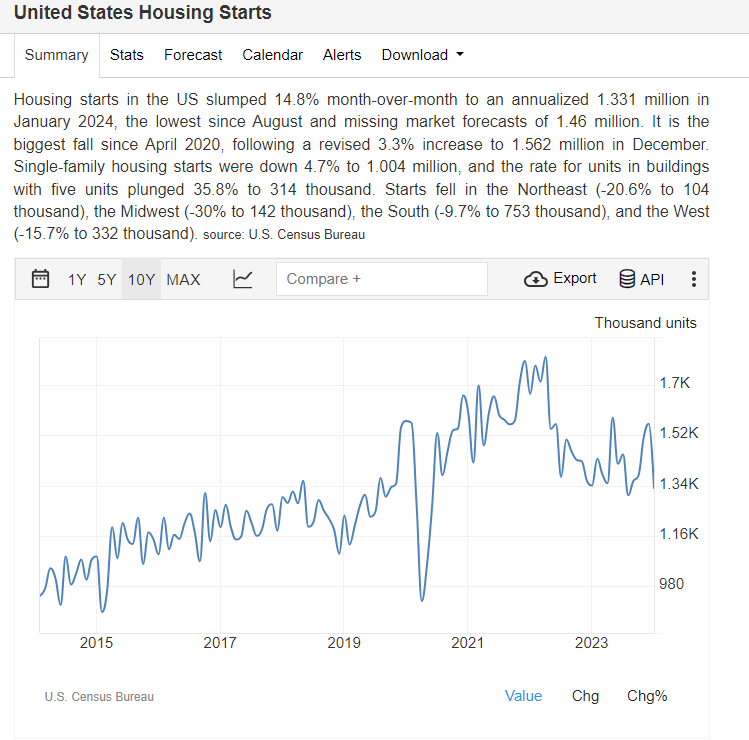

US census

Housing starts might not accelerate as I expect, as the US economy is not entirely out of the woods yet. If a major recession kicks in, it will put pressure on the underlying construction companies to build more houses. Note that the labor market is still hot in the US, and this puts additional pressure on wage expenses for the construction industry.

I recommend a buy rating for IBP due to its compelling near-term growth outlook. The severe housing undersupply in the US should lead to increased housing starts, directly benefiting IBP's core business. I expect growth in both single-family and multi-family housing, with robust backlogs in multi-family providing additional support. The commercial segment is also poised for continued expansion. Moreover, management's focus on cost control and operational efficiencies, combined with easing inflation, creates opportunities for margin expansion.