Kateryna Onyshchuk/iStock via Getty Images

Kateryna Onyshchuk/iStock via Getty Images

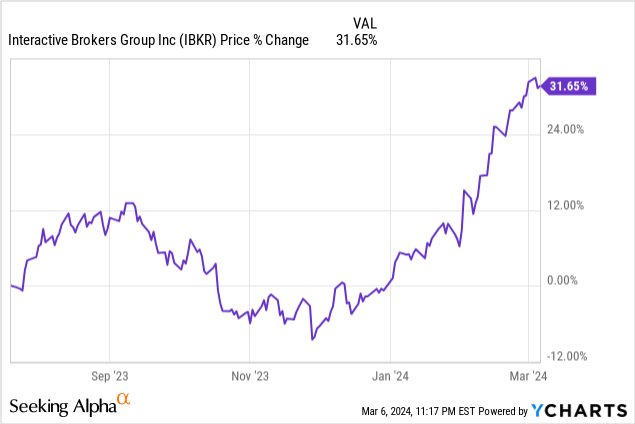

My first coverage of Interactive Brokers (NASDAQ:IBKR) was over half a year ago and I felt that it is prudent to review my investment thesis given the healthy rise in its stock price against a market where "Mag 7" dominates and popular narrative would have you believe that the returns in the market are very concentrated. It could be concentrated but I have no exposure to the Mag 7 (it could be Fab 4 now) and so far I have no complaints with my investments. From what I have seen, businesses that display quality are still being rewarded, and Interactive Brokers is one such name where I see them delivering. I have the confidence that they will continue to deliver barring a deep recession risk.

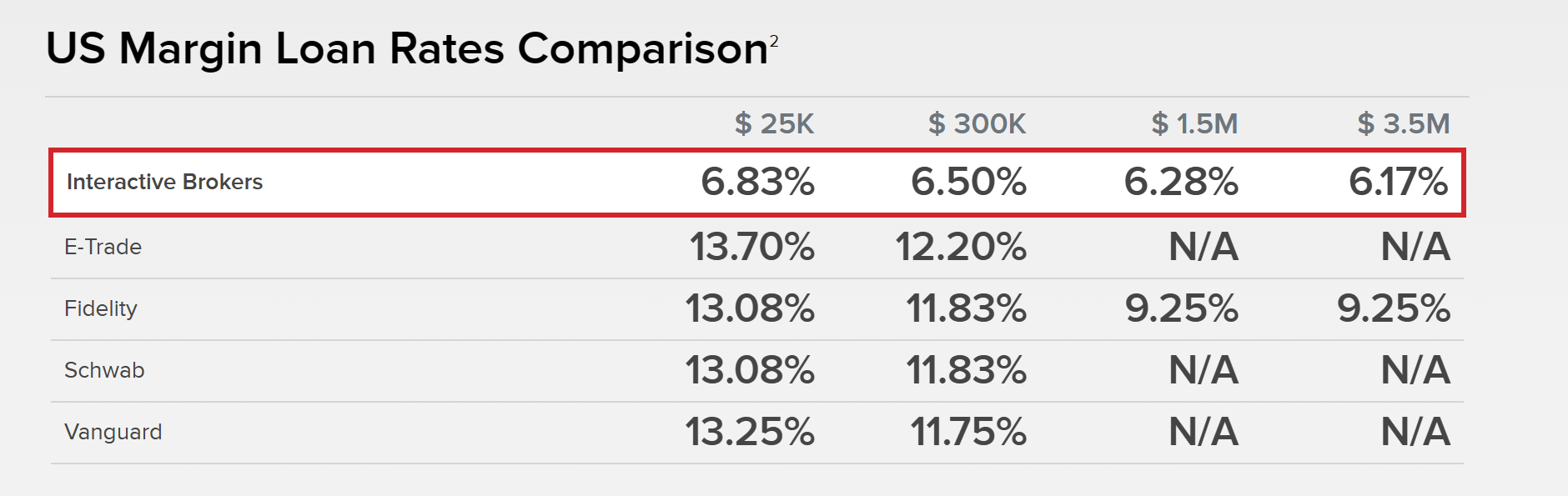

In my first coverage, I explained why I was attracted to this stock. I have been through plenty of brokerages and let's face it. The company's app is not exactly intuitive and the best to use. Other brokerages such as Robinhood (HOOD) are known for their User Interfaces. In my personal experience, it is hard to come across an interface that is so beautiful and easy to use. But Interactive Brokers know their strengths and target audience. Their users are more sophisticated and are looking for access to a wide variety of markets (broad investment selection universe) which other brokers are not so good at providing. Since their focus is also to cater to institutional clients their order execution is quite unparalleled and they are known in the industry to have a strong capital position with automated risk controls to protect their clients' capital. They also have extremely competitive rates on margin loans and unused cash balances (4.83%)

IBKR website

Their reliance on technology and automation made them the best-of-breed operators with the highest operating margins in the industry. But even with all these differentiators and a leading position in the industry they still seemed the cheapest among all their competitors. As a result, I entered into a small position in the company.

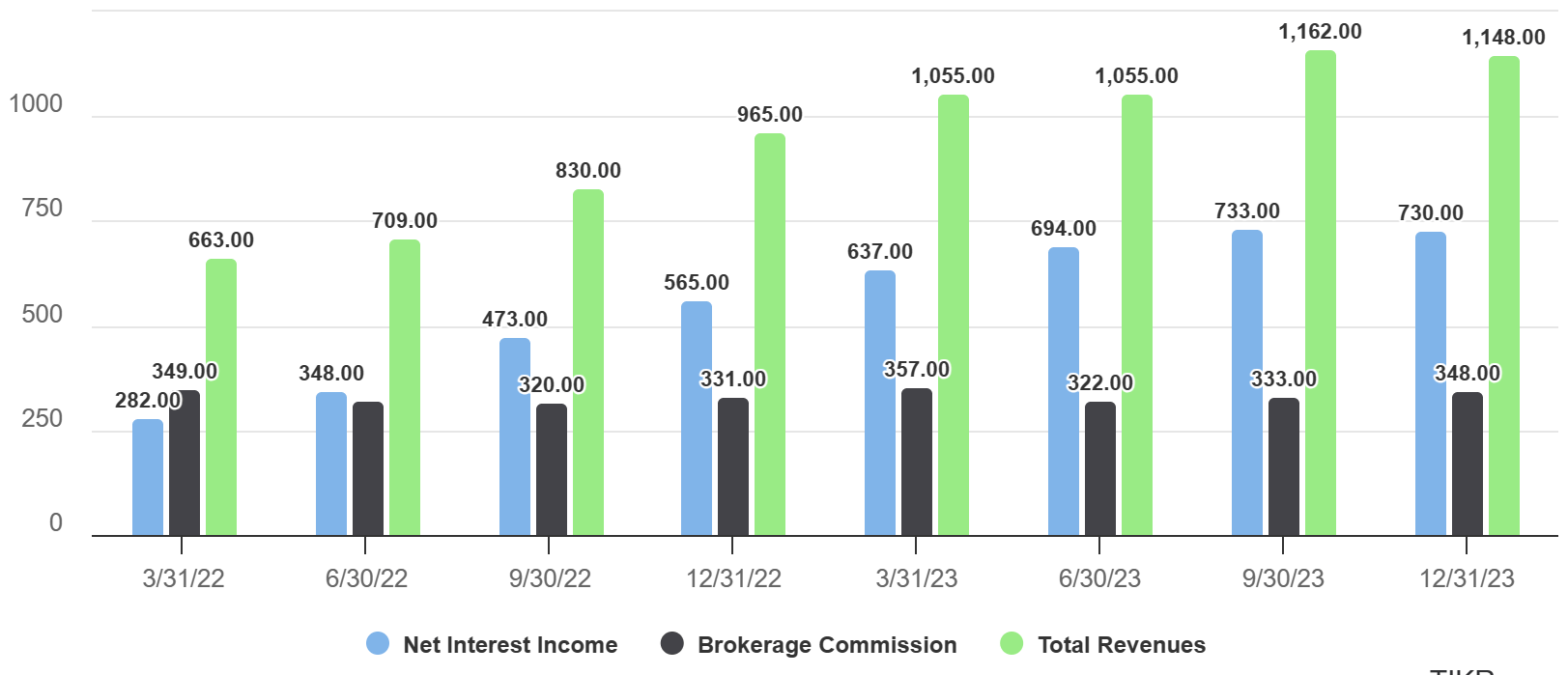

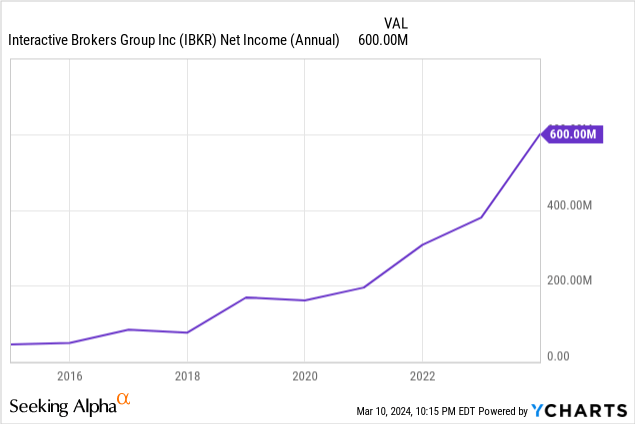

The company has been quite adept at making use of the high interest rates which by and large attract capital to be parked in customers' brokerage accounts. It's a win-win situation for both the customer and the company. The customer gets high interest on the capital and the company gets to pocket the differential (between what it makes on the capital and what it gives out to the customer). Trading commissions are another lucrative stream of revenues and the explosion of trading in the markets combined with the fact that Interactive Brokers is a trusted and widely used broker means that the company wins on this front as well. The aggregate effect of an increase in net interest income and brokerage commissions means consistent growth in the top line.

Revenue composition per quarter ($M) (Tikr)

Many of the metrics from the company's latest earnings report are truly impressive(compared to the same quarter in the previous year) which lends further credence to the fact that it has been great at exploiting the current environment -

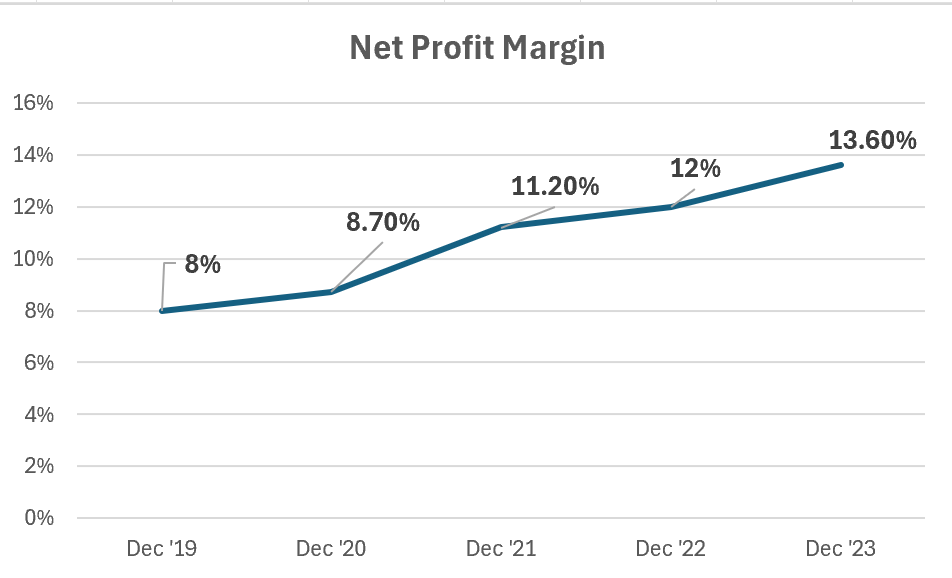

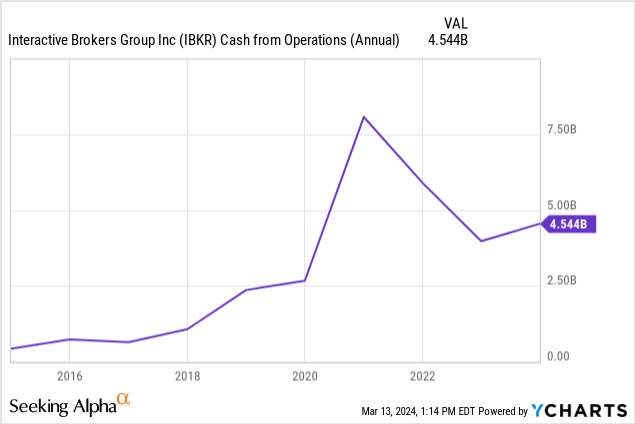

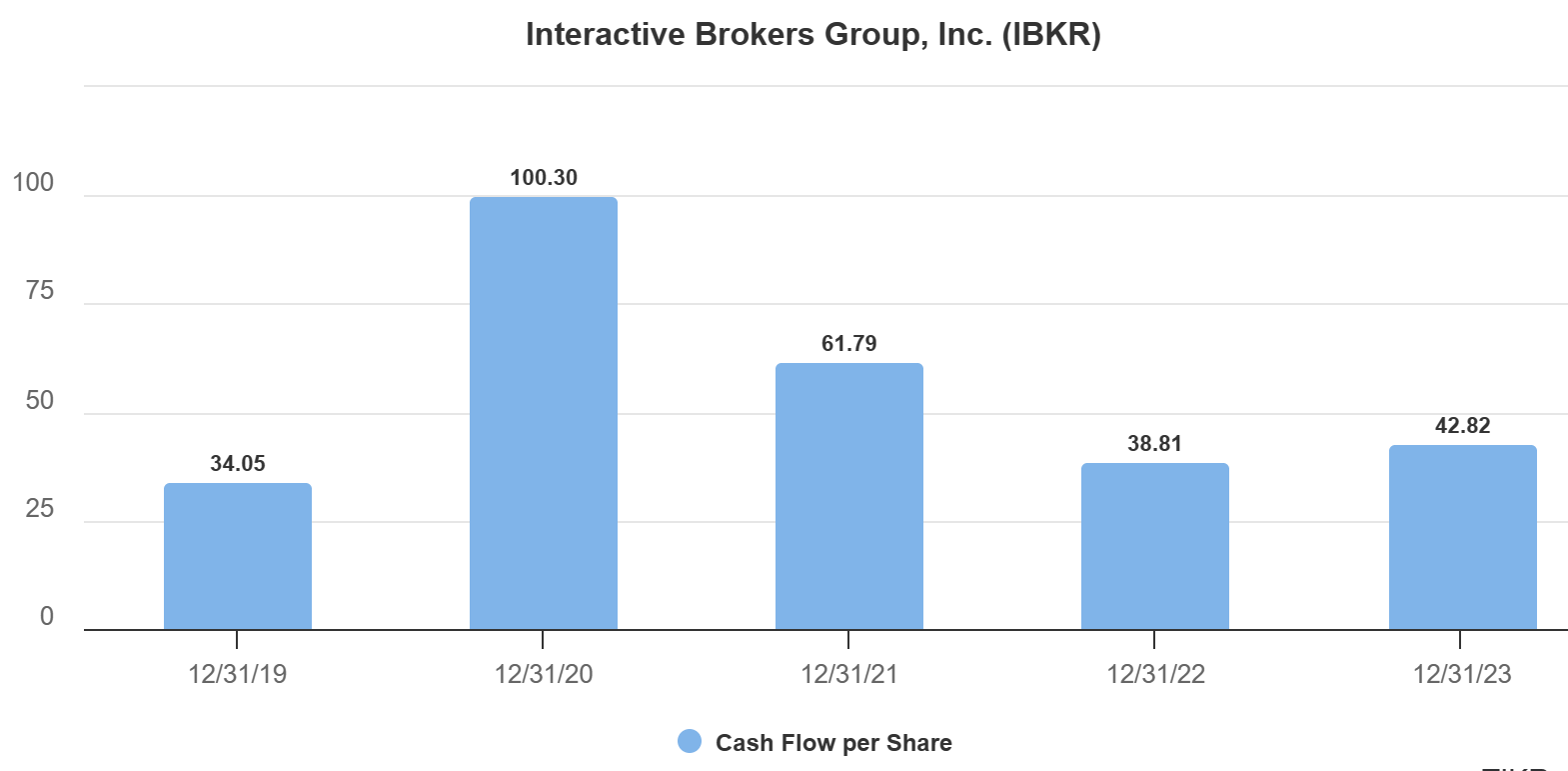

Looking at the company's bottom line and cash flows, we see they have a healthy financial position. Their net profit margin is 13.6% and this metric has been trending up for a while.

Company Financial data

Their continuous improvement in net profit margins indicates efficient management of costs and operations.

Their operating cash flow shows strong cash generation from their core business activities. Overall, it can be said that it's a well-managed business.

TIkr

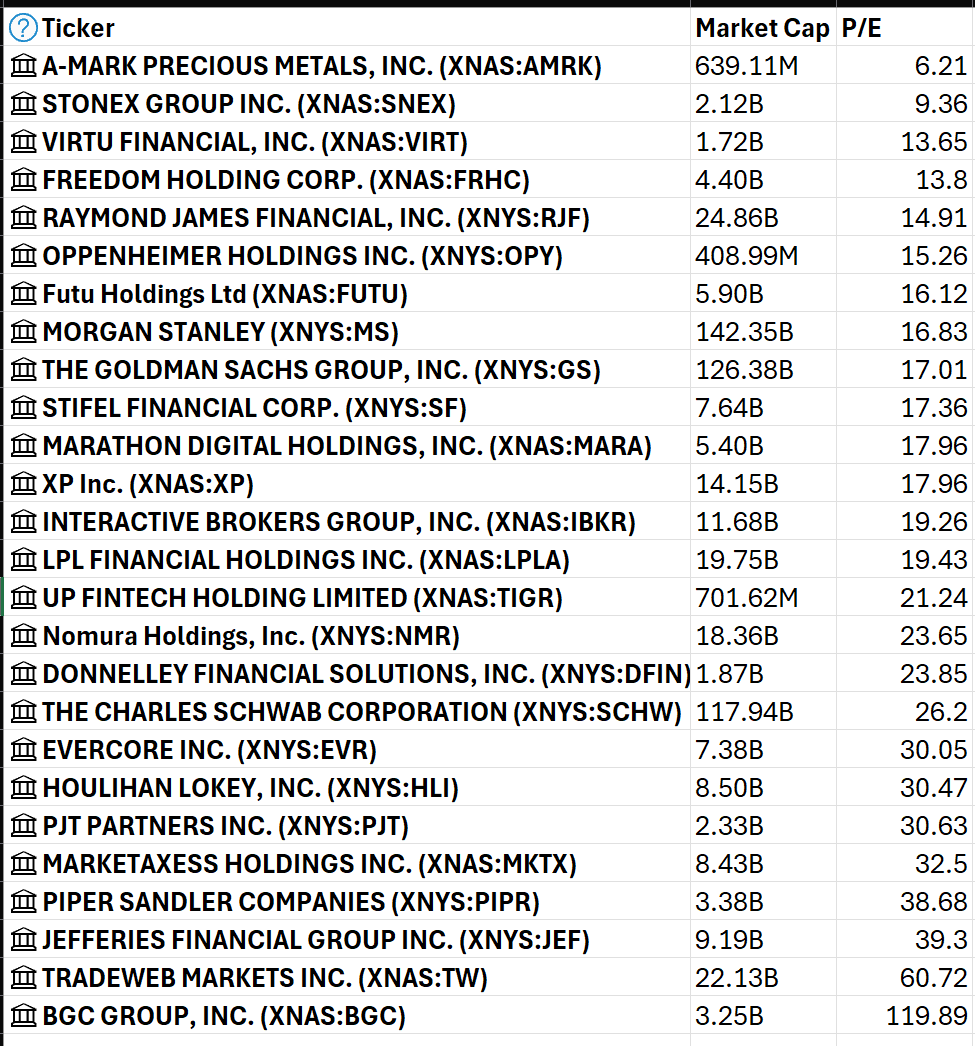

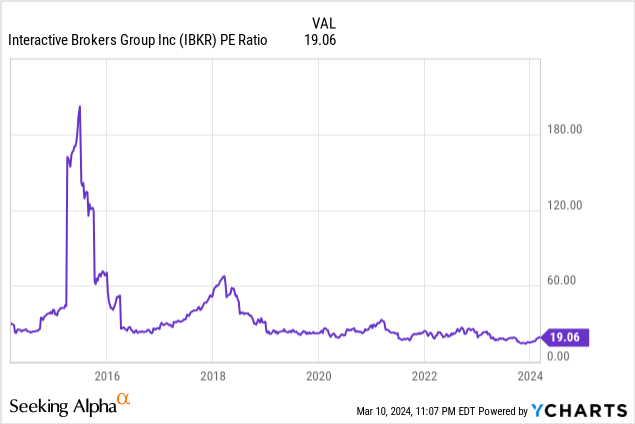

The company trades at a Price to Earnings multiple of 19x and has a forward multiple of 17x both are relatively low when compared to its historical valuation. When compared to the sector median (Financials - 10.5) it may seem high but two things to note here.

1. Interactive Brokers is a stock brokerage and pure brokerages are a very small and specialized subset within financials. The number of direct comparables is low so we can look at the industry average which offers more insight than the sector median.

Capital Markets Industry Comparables for valuation (Finviz)

The sector median comes out to be 19.3x which means our candidate is fairly valued.

2. Even with the recent rise in stock price, it has not kept up with its earnings growth which results in a very attractive PEG ratio of 0.37. Low PEG ratios are generally not sustainable and it would be hard to expect them to be maintained at this level. But going forward, I would expect the company to keep growing its earnings at least modestly in light of present conditions (Rate cut expectations have diminished and the economy shows no signs of exhaustion. This could mean that interest income and trading volumes continue to stay elevated)

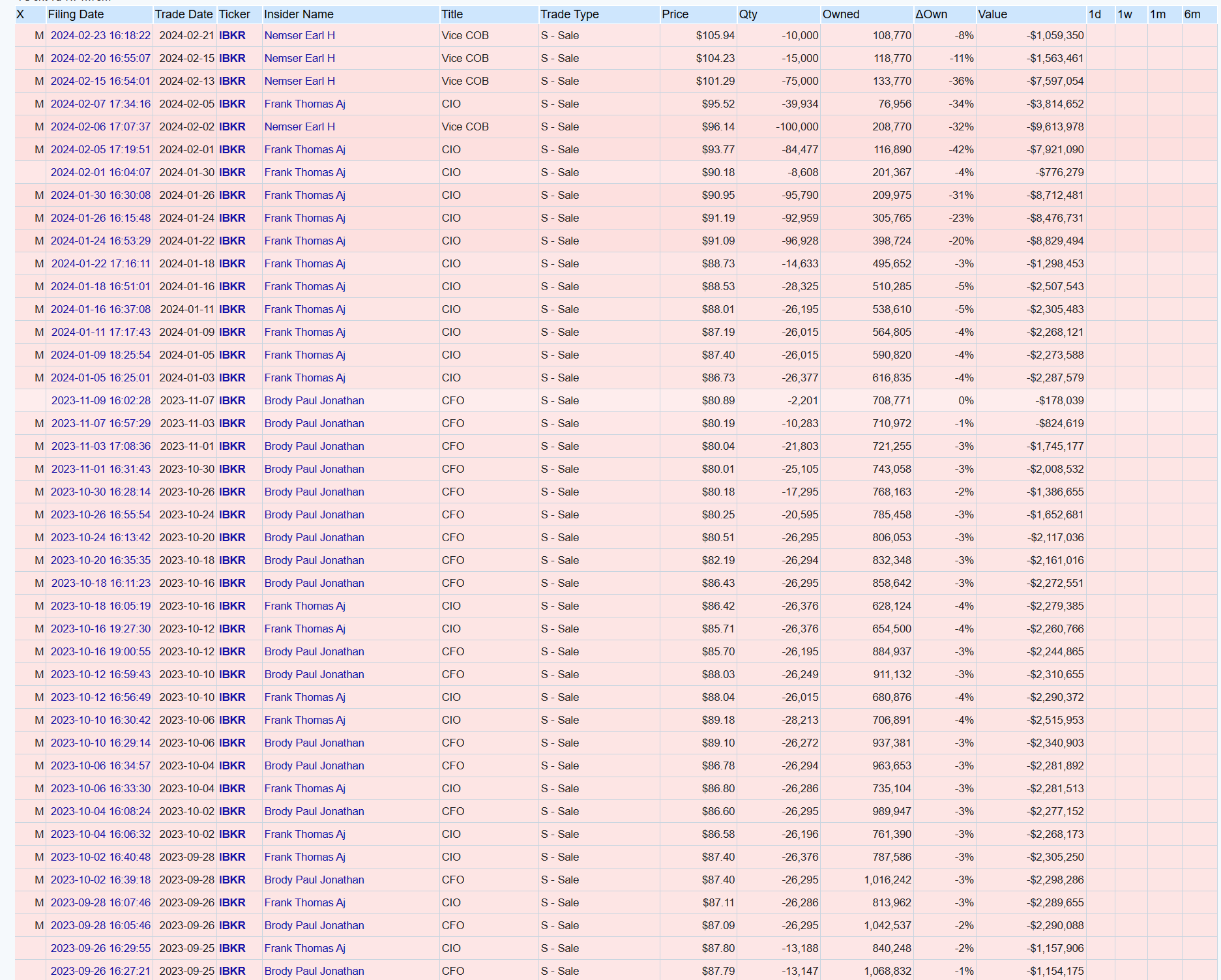

Personally, I like where the company is trading and would be a buyer at these levels. However, insider activity is not very encouraging. It could be that the company is trading around the highest level in its history and the upside from here could be interpreted to be limited. As it is well known, insider selling could mean any number of things but it is hard to dismiss the fact that so many insiders have been unloading sizeable positions in the company.

Insider Activity snapshot (Open Insider)

For the risks to this investment, my big argument would be it has to come from outside the company. The company has proved time and again that it can innovate, differentiate itself, and stay competitive in its offerings. So it is highly unlikely to lose its competitive advantage. So its fortunes are closely tied to the strength of the economy which in turn affects interest rates which in turn would bring down the interest income. But it is not just any rate cut that would affect the company. The rate cuts would have to be deep and be a direct result of the Fed acknowledging a big deterioration in the U.S. economy. This would also mean a double whammy in terms of trading volumes as well, which typically take a big hit during economic hangovers. Last year when I first covered the company, this seemed a big risk on the horizon. But increasingly, macro views point to a no-landing scenario, with the United States beginning to look like a rare example in the world being able to come out of this economic cycle unscathed.

But in the investment world, nothing is a given, and protecting my profits and capital would be my number one priority. For now, this risk combined with discouraging insider activity means I will be holding the stock with a watchful eye.