Monty Rakusen

Monty Rakusen

When COVID-19 pulled down the airline industry, Howmet Aerospace Inc. (NYSE:HWM) fell with it. But the company has now rebounded and is expected to grow its earnings per share by about 20% per year this year and next year. Because the share price follows earnings quite well, I expect the share price to grow significantly this year and next year.

The company specializes in what it calls "advanced engineered solutions for the aerospace and transportation industries."

Its products include "jet engine components, aerospace fastening systems, and airframe structural components necessary for mission-critical performance and efficiency in aerospace and defense applications, as well as forged aluminum wheels for commercial transportation."

It operates through four segments, according to its fourth-quarter and full-year 2023 earnings report:

Howmet reported that its "differentiated technologies" provide aircraft and commercial trucks with lower carbon footprints and other benefits.

At the close of trading on February 20, 2024, its share price was $63.11 and it had a market cap of $25.78 billion.

In its 10-K for 2023, Howmet advised that each of its segments faces "substantial and intense competition" in the markets they serve. Named competitors include Precision Castparts Corporation, a subsidiary of Berkshire Hathaway Inc. (BRK.A)(BRK.B), High-Performance Materials & Components, a subsidiary of ATI Inc. (ATI), and Accuride Corporation (ACW).

Despite the competition, the company has argued it is a market leader in most of its main markets. It cites factors such as its technological expertise, capacity, quality, and more.

Behind its technological expertise are some 1,150 granted and pending patents and, of course, its brand.

Good competitive advantages usually go hand-in-hand with some degree of pricing power, as evidenced by strong margins.

That is the case for Howmet, with a gross margin [TTM] of 27.94%, an EBITDA [TTM] margin of 21.94%, and a net margin [TTM] of 11.52%. The latter is nearly double the Industrials sector median.

Management reported in the 10-K that it aims to improve its operational performance through profitable revenue, efficient operations and margin enhancement. In the Engine Products segment, for example, the company reported improvements in its segment-adjusted, EBTIDA margin, from 24.7% in 2021, to 27.0% in 2022, and 27.2% in2023.

Unfortunately, it has lost ground in the other three segments, the most glaring example of which is Forged Wheels, which has seen its segment-adjusted EBITDA margin fall from 31.9% in 2021 to 26.9% in 2023. Lower margins are due to issues such as a supply-chain disruption, unfavorable foreign exchange rates, and heat/fire problems at its forged wheels plant, according to the 10-K.

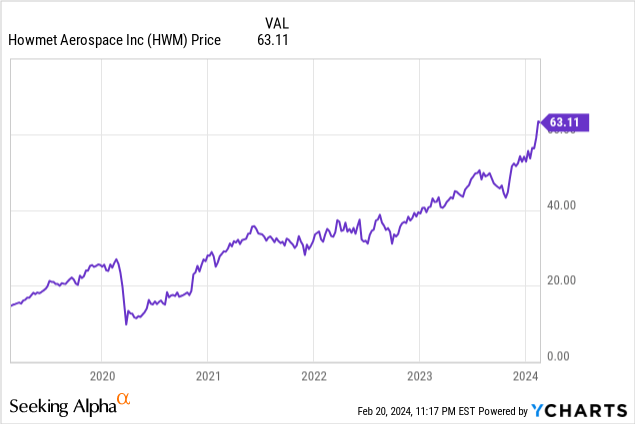

Further, Howmet depends heavily on the aerospace and commercial transport industries, which were hit hard by COVID-19. However, it is recovering from those blows, as this five-year chart shows:

HWM Revenue-EBITDA-EPS chart (Seeking Alpha)

Note how EBITDA and EPS have risen significantly since coming out the pandemic, while revenue has remained relatively flat. That suggests the company has done an excellent job of managing its costs.

Expect more of the same in the next two to three years. The 17 analysts covering Howmet expect year-over-year revenue growth to be 7.39% for 2024 and 8.66% for 2025. At the same time, they expect earnings per share to grow 19.59% this year and 21.11% in 2025. That's healthy growth.

The company offered its guidance with the full-year results. It expects baseline revenue for the four quarters of 2024 to increase to $7.1 billion, which would be an annual increase of 7.6%. Adjusted EBITDA is expected to grow by 22.9% to 23.2%. Again, there is a significant-and positive-gap between revenue and adjusted earnings.

For the fourth quarter and full-year 2023, Howmet reported 10 consecutive quarters of revenue, Adjusted EBITDA, and Adjusted EPS growth. Revenue increased mainly because of growth in commercial aerospace.

Free cash flow is one of the beneficiaries of this growth. The company expects it will increase about 8.0% in 2024, to about $735 million, with a free cash flow conversion rate of about 85.0%.

In 2023, it used its free cash flow of $682 million plus cash to pay down and refinance debt ($875 million), buy back common stock ($100 million), and increase the dividend (by 25.0% to $0.20 annually).

Howmet expects capital expenditures of $275 million to $305 million in 2024, a major increase from the $219 million in 2023 and $193 million in 2022.

Heavier capital spending usually means higher revenues and, of course, higher EBITDA and EPS. Both of those should push up the share price as well.

Chair of the Board and CEO, John Plant has held the former position since 2021 and the latter since 2019. He is a Fellow of the Institute of Chartered Accountants and has held senior leadership positions for more than 30 years. Before joining Howmet, he was the President and CEO of TRW Automotive Holdings between 2003 and 2015.

Ken Giacobbe, Executive Vice President and Chief Financial Officer, has held these roles since 2016. He previously held senior financial positions at Alcoa Corporation (AA), Avaya Holdings Corp. (OTC:AVYAQ), and Lucent Technologies, Inc. (now a subsidiary of Nokia Oyj (NOK)).

Both executives are seasoned leaders and navigated the company through the COVID-19 crisis that saw one of its major markets, aerospace, take a deep dive. They also led as the company rebounded from that economic slowdown.

The company offers no articulated business strategy, but several conclusions can be drawn from its reporting. First, its 1,150 patents tell us that the company emphasizes innovation and technological development.

Second, it is committed to its two major markets, aviation and commercial transportation, and the two markets are linked by engineered solutions. Both its aerospace products and its forged wheels help its clients be more fuel efficient.

Another part of Howmet's strategy is to reward its shareholders, through share repurchases and a dividend. While the dividend yields only 0.32%, it does remind shareholders of its commitment to them.

Fourth, we see its increasing capital spending and know that this is a growth firm, and not a mature company.

In summary, given its ability to generate free cash flow and keep its costs under control, the firm is well placed to maintain this strategy in the future.

There is nothing in the valuation ratios that suggests Howmet is a bargain. The PEG GAAP [TTM] ratio is 0.53, which indicates undervaluation, but the PEG Non-GAAP [FWD] is 1.61, which is in the upper half of the fair value range (1.00 - 2.00).

Similarly, EV/EBITDA is a hefty 19.94, well above the benchmark of 10, while the Price/Sales [FWD] is 3.61 and Price/Book [FWD] is 5.82. All of these ratios are higher than the Industrials sector median.

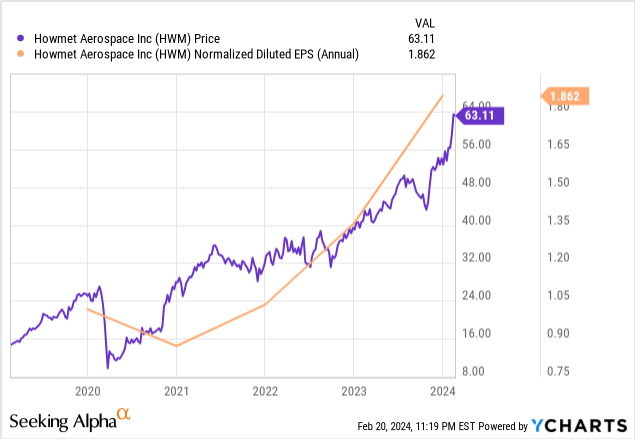

All of this suggests that Howmet is overvalued, likely because investors like the way their capital has grown, and especially since mid-2020:

But having to pay a premium doesn't always mean you're paying too much. After all, the current price is relative if you see even higher prices in the future. The analysts who follow Howmet see double-digit earnings increases in the next five years, and the share price has tracked earnings quite well in the past:

What are the analysts predicting about earnings increases?

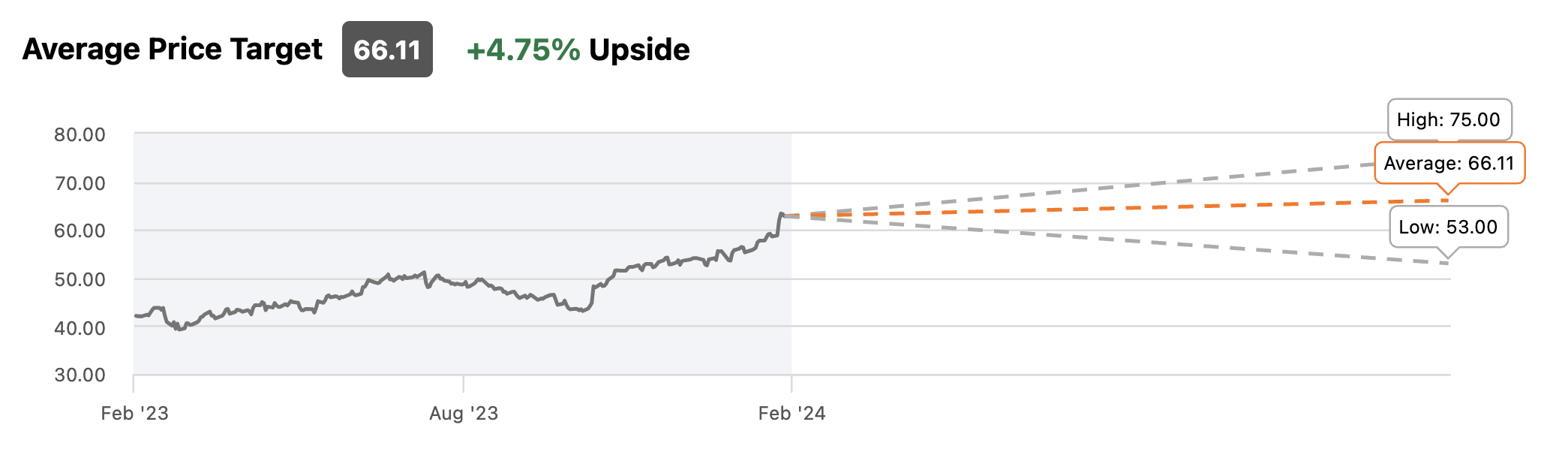

A 20% increase on the 2023 closing price of $54.12 would amount to $64.94 at the end of 2024. But the share price had already reached $63.11 by the close on February 20.

Twenty percent added to the February 20 closing price would be $75.23. That's quite close to the analysts' high target price:

HWM analysts' target price (Seeking Alpha)

It's true, Howmet is currently overvalued by the ratios, but given the potential for higher earnings in 2024 and a potential share price around $75.00, then we should consider it undervalued.

Based on that and my faith in the company's ability to keep delivering profitable growth, I am giving it a Strong Buy rating. Seeking Alpha's Quant rating is Hold; the one Seeking Alpha analyst who rated Howmet in the past 90 days gives it a Buy. Wall Street analysts give the firm 14 Strong Buys, four Buys, and three Holds.

Howmet's main market is commercial aircraft, and in the Q4/full-year 2023 earnings report, the company said its guidance is based on The Boeing Company building an average of 34 737-MAX aircraft per month and an average of 56 Airbus A320 units per month. But, as we learned in the news recently, a door on a Boeing 7373-MAX 9 blew out, prompting a grounding of those planes (since lifted). This event could have an effect on Howmet's first-quarter 2024 results.

The company also may be buffeted by economic conditions; a slowdown in the broader economy could slow demand for aircraft parts and truck wheels, thus having an adverse effect on Howmet. The firm acknowledges in its 10-K that its markets are cyclical.

As an engineered solutions company, one with more than a thousand patents, Howmet requires highly trained professionals and technicians. It must compete with other companies and organizations for a limited number of qualified people.

As it is a global player, the firm has exposure to geopolitical risks and unfavorable currency exchange rates. To make matters more complicated, there are also numerous export regulations at home and in other countries.

The company reports that "a significant portion" of its employees are represented by unions, both domestically and internationally. A work stoppage in one area could do substantial harm to its supply chains and operations.

Howmet Aerospace has made a strong recovery from the economic chaos caused by the COVID-19 pandemic. Its earnings surge is expected to continue as the aerospace industry continues to pick up speed and the company maintains its financial discipline.

Earnings are expected to grow vigorously over the next three years. And because the share price follows earnings quite well, I expect the price to rise a further 20% per year this year and perhaps the same in 2025. I thus consider Howmet a Strong Buy.