su tim/E+ via Getty Images

su tim/E+ via Getty Images

Huntsman Corporation (NYSE:HUN) is a multinational chemical company that has three segments, Polyurethanes, Performance Products, and Advanced Materials.

In 2023, Huntsman's Polyurethanes business accounted for 63% of segment revenues, performance products accounted for 19%, and advanced materials accounted for 18%.

In terms of segment adjusted EBITDA for 2023, polyurethanes accounted for 39%, performance products accounted for 32%, and advanced materials accounted for 29%.

In recent years, Huntsman has faced headwinds given weaker end market conditions due to factors such as higher interest rates and also weaker Chinese economic conditions. Around 15% to 20% of the company's sales are into China and less than 10% are into property in China.

Another reason for the weakness in the past two years in demand is that many of Huntsman's customers built up unnecessarily large amounts of inventory a few years ago given there was concern there wasn't going to be enough production at the time and as markets turned, it took longer for those customers to de-inventory than expected.

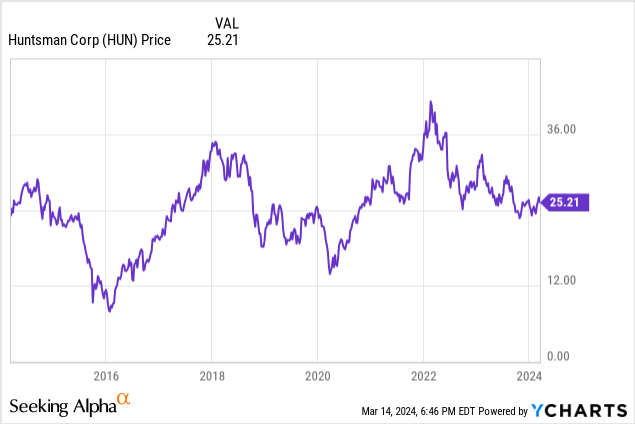

As a result of the soft end markets demand and macro headwinds in China, Huntsman's financial performance weakened in the past two years and the company's stock has not done well since the beginning of 2022.

On February 21, 2024, Huntsman reported fourth quarter 2023 results and full year results that showed continued weakness in demand that resulted in a softer financial performance.

Nevertheless, management is cautiously positive about the future, and analysts on average expect the beginning of a profitability rebound this year.

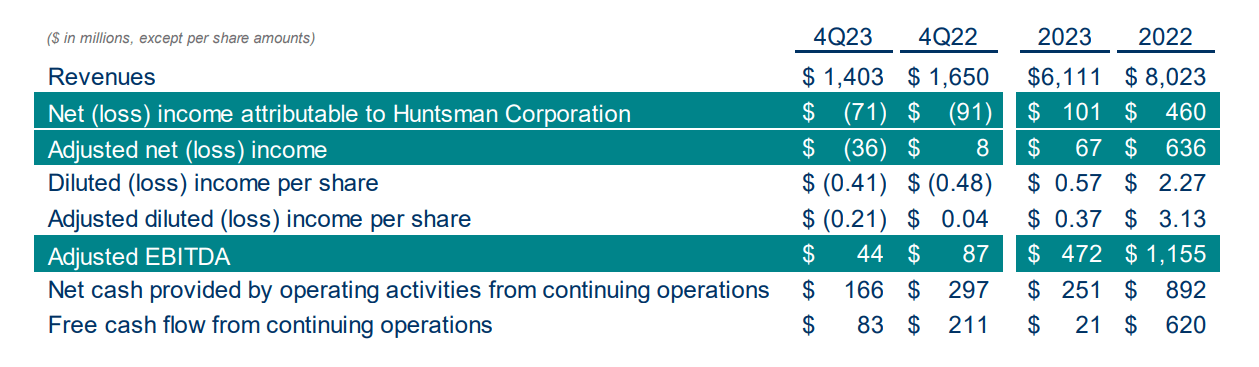

For the fourth quarter of 2023, Huntsman's revenues were $1.403 billion, down from $1.65 billion in the prior year period as the company faced a tough demand environment.

In terms of the demand environment, Huntsman said in the Q4 earnings release that it withstood "one of the toughest demand environments we have seen in well over a decade".

With the headwinds, adjusted EBITDA fell to $44 million from $87 million in the prior year period.

Furthermore, the company had adjusted net loss of $36 million for Q4 2023, versus adjusted net income of $8 million in Q4 2022.

Adjusted diluted loss per share was $0.21 in Q4 2023 versus adjusted diluted income per share of $0.04 in the prior year period.

Huntsman Investor Presentation

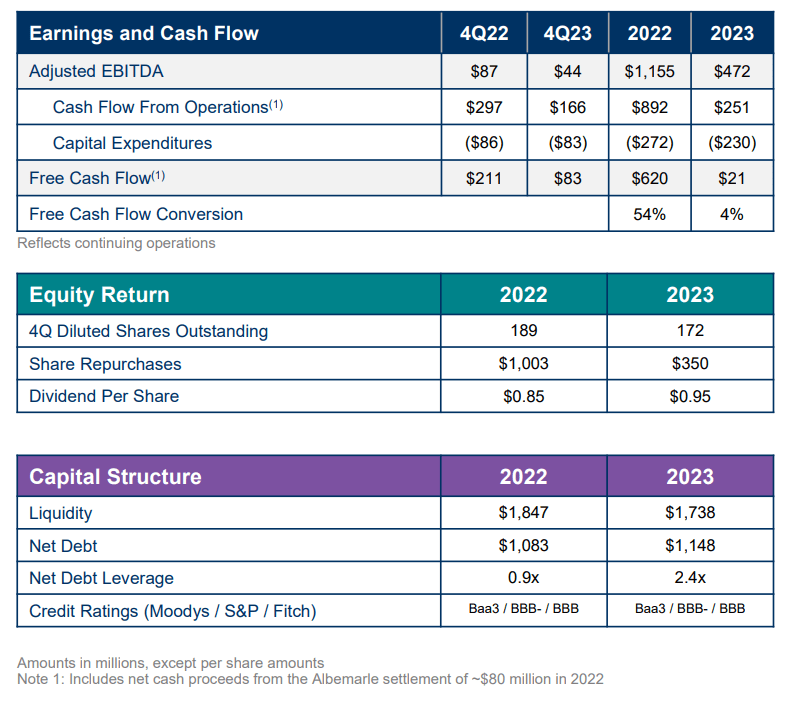

Despite the adjusted loss and the lower adjusted EBITDA, Huntsman repurchased 2.1 million shares for around $50 million, and the company's board of directors approved a 5% increase in the quarterly dividend.

My takeaway is that the company's financial results were weak in Q4 given the tough end markets demand conditions.

Nevertheless, I think it's interesting how Huntsman's board increased the quarterly dividend despite adjusted EBITDA declining year over year and the company also having an adjusted net loss. To me, this shows that management is positive about an eventual recovery in the future.

Like Q4 2023, Huntsman's full year 2023 financial results were generally weaker than 2022 given softer end markets.

For 2023, Huntsman's revenues fell 24% year over year in 2023 to $6.111 billion while adjusted EBITDA fell 59% year over year to $472 million.

Some of the revenue and adjusted EBITDA decline in 2023 was due to Huntsman selling its textile chemicals and dyes business (textile effects business) for a purchase price of $593 million in February 2023.

In terms of the last twelve months ending June 30, 2022, Huntsman's textile effects division reported sales of $772 million and adjusted EBITDA of $94 million.

The majority of the decline was due to softer demand, however.

In other metrics, free cash flow from continuing operations declined to $21 million from $620 million in 2022 and the company's adjusted diluted income per share fell to $0.37 in 2023 from $3.13 in 2022.

As of the end of 2023, Huntsman had net debt of $1.148 billion, with net debt leverage of 2.4x.

In 2023, the company bought $350 million worth of shares back.

Huntsman Investor Presentation

My takeaway is that Huntsman faced headwinds in 2023 that have resulted in lower profitability. Management nevertheless bought back stock in the year, which signals confidence in an eventual recovery.

While Huntsman is facing tough demand conditions, management nevertheless has seen moderate improvement in early 2024 from the lows experienced in the fourth quarter of 2023.

They said in the earnings call in February 2024,

As I said at the beginning, it is still too early in the quarter to make bold predictions. However, the order patterns that I'm seeing in most areas of the world tells me that in most of our divisions, we have seen the end of a very long period of inventory drawdowns and prices and volumes look to be gradually improving.

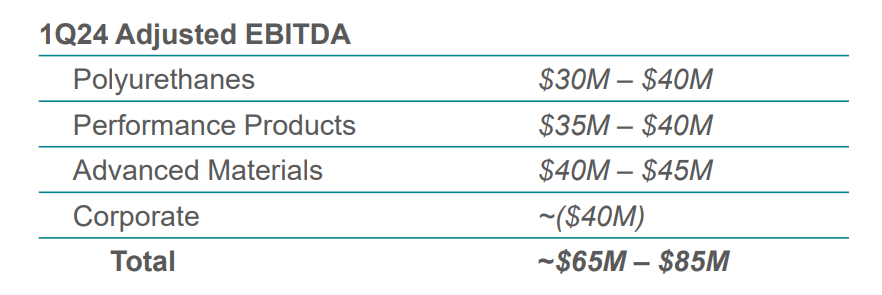

In terms of financial outlook for Q1 2024, management expects adjusted EBITDA of between $65 million to $85 million, which would be an improvement from Q4 2023's adjusted EBITDA of $44 million.

Huntsman Investor Presentation

Management added,

while we are yet to see a clear inflexion point in demand, we remain positive about the future. We are well positioned to benefit significantly from volume leverage once our end markets improve and as we continue to control our cost base. While the exact timing of a recovery remains uncertain, we are confident that construction spending and industrial activity in our core markets will return to past cycle averages and the world will continue to value energy efficiency and light weighting which impacts two-thirds of our total sales.

In terms of strategy, Huntsman is also still looking for M&A opportunities to expand its more differentiated downstream businesses.

I agree with management that demand will recover and that the exact timing of the recovery is uncertain.

A slowing Chinese economy could continue to be a headwind for demand for end markets.

Global economic weakness would be a headwind for demand for end markets.

Huntsman's expected rebound might take longer than expected.

Huntsman's EBITDA could decline if economic conditions decline and make servicing the company's net debt harder.

In terms of expectations, analysts on average expect Huntsman's profits will begin to rebound this year and for the profit rebound to be a multi-year process.

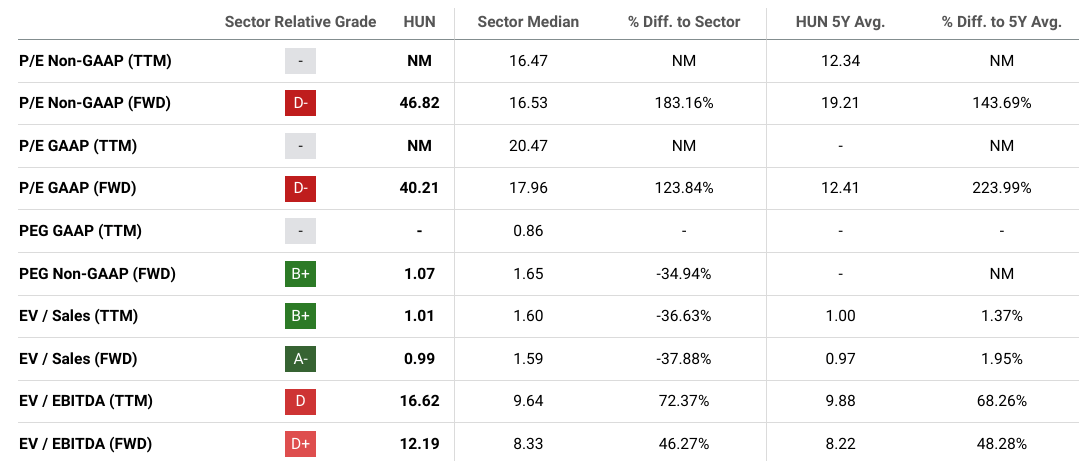

In terms of earnings expectations, analysts on average estimate Huntsman will earn $0.55 per share for 2024, $1.64 per share for 2025, and $2.01 per share for 2026. Adjusted diluted EPS for 2023 was $0.37 by comparison. That gives the company a forward PE ratio of 46.82 for 2024, 15.71 for 2025, and 12.86 for 2026 as of March 14.

In terms of EBITDA estimates, analysts also expect a multi-year rebound. Analysts at Wells Fargo, for instance, said in February 2024 they estimated Huntsman would increase EBITDA from $472 million in 2023 to $500 million in 2024 and over $700 million by 2025 as demand recovered into 2025.

While analysts are optimistic, Huntsman management has been cautious saying they remain positive about the future but acknowledges that the exact timing of a recovery remains uncertain. Furthermore, my takeaway from the Q4 earnings call is that they expect the recovery in demand to be gradual in many products.

As a result, I think there's a chance that Huntsman doesn't meet EPS estimates this year, but nevertheless, I think the company will outperform EPS estimates more in the long term given my view that I think infrastructure/construction demand will increase faster than expected in the future as technology advancement makes more infrastructure/construction possible.

In terms of valuation, Huntsman looks pretty expensive in terms of forward EV/EBITDA and forward P/E ratio because analysts don't see that much of an EBITDA and EPS recovery in 2024. According to Seeking Alpha as of March 14, Huntsman has a forward EV/EBITDA ratio of 12.19, versus the sector median of 8.33.

Seeking Alpha

Nevertheless, Huntsman would look more attractive in 2026 given the forward P/E ratio of 12.86 for 2026. I think the company will also make more than $800 million in adjusted EBITDA for 2026 (excluding M&A effects) as I expect the demand recovery to be more or less realized by then. If that happens, the company would have a forward EV/EBITDA valuation of under 8x for 2026 using March 14 prices, which is fair.

In terms of adjusted EBITDA in the past, Huntsman had adjusted EBITDA of $1.246 billion in 2021, $1.155 billion in 2022, and $472 million in 2023. (The company sold off its textile effects business that accounted for adjusted EBITDA of $94 million in terms of the last twelve months ending June 30, 2022)

In the longer term, I expect Huntsman's annual adjusted EBITDA to be considerably higher than $800 million (excluding M&A effects) as I think infrastructure/construction demand and industrial demand could be considerably stronger than current expectations as technology advancement makes more construction and industrial applications possible. This is the main reason why I'm bullish on the stock.

If Huntsman innovates and keeps on the cutting edge, I think the future for the company is bright as there are a lot of opportunities to meet new demand.

I rate Huntsman a 'Buy' and I would own Huntsman as 'Equal Weight' in a diversified portfolio with the Magnificent Seven. I would not own too much of Huntsman, however, as the recovery could be gradual and the exact timing of the recovery is uncertain.

Excluding any M&A in the future in my calculations, I think a fair price would be around 8.5x EV/estimated EBITDA for 2026, which is when I think earnings would potentially be more recovered and more normalized, and that gets me a target price of around $29.31 per share assuming EBITDA of around $800 million for 2026. If EBITDA is considerably better, the stock would have more upside. Huntsman also has a dividend yield of around 3.97% as of March 14.

For the long thesis, I would follow several things.

First, I'd follow Huntsman's earnings reports and EBITDA, and check to see that EBITDA is growing. Huntsman had a net debt leverage of 2.4x at the end of 2023 so it needs to ideally grow its adjusted EBITDA.

Second, I would follow interest rates. If interest rates begin to decline, I think many of Huntsman's end markets such as housing/construction would benefit and this could increase demand for the company. In my view, I think interest rates will begin to decline this year and normalize within a few years.

Third, I'd follow China, and U.S. and China relations as China accounts for 15% to 20% of Huntsman's revenues. If economic conditions in China rebound, particularly in the housing market, Huntsman's overall financials could benefit. If geopolitical relations between the U.S. and China weaken, I think this would be a headwind for the stock.

Since Huntsman has a history of M&A in the past, I'd also follow the company's future transactions to see management's plan for the future. Huntsman has transformed itself through a series of acquisitions and divestitures to become what it is now and it will likely continue to do M&A in the future in my view.