Edwin Tan

Edwin Tan

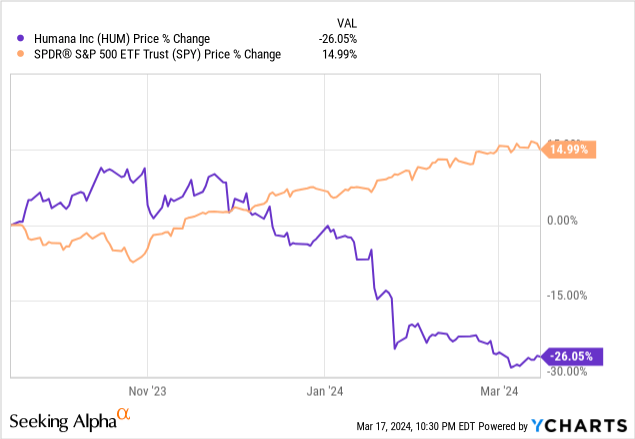

Humana (NYSE:HUM) is one of those rare stocks that received quite a beating from investors this year as most stocks seem to be having a party and making new highs every week. When the company announced its earnings in January, investors didn't like its newly updated guidance for 2024 as the company said it would earn only $16 per share this year whereas analysts were looking for $28 per share in net income. For the year 2025, it said that it estimates to post a net income gain of $6-10 over 2024 which indicates a guidance of $22-26 which is nowhere close to expectations of $37.

This was mostly driven by the company's troubles in its Medicare Advantage business segment which proved to be more challenging in terms of generating profits. As one of the biggest providers of government-sponsored insurance for senior citizens and those with disabilities, the company saw budget pressures as the relevant Federal agency dealing with this type of insurance CMS (Centers for Medicare & Medicaid Services) is aiming to cut payments to insurance providers in coming years. Adding to the pressures was the introduction of lower premium models by competitors such as UnitedHealth (UNH) and CVS Health (CVS) which may steal market share from Humana.

There are several trends in America that are putting pressure on healthcare companies. The population is getting older as a whole, healthcare services are getting more expensive and people start getting sick at an earlier age require more years of active care. Not long ago, people didn't get chronic diseases like diabetes (the type 2 kind), hypertension or heart disease until they were well into their 60s but now we are seeing people getting diagnosed with these diseases as early as in 20s which will require multi-decades of care for these people. This trend also puts pressure on the government to cut spending on its Medicare type of programs in order to keep them from collapsing. This means that insurance companies will have to do more with less and offer the same level of coverage for smaller premiums. In return, they might have to negotiate better deals with healthcare providers such as hospitals.

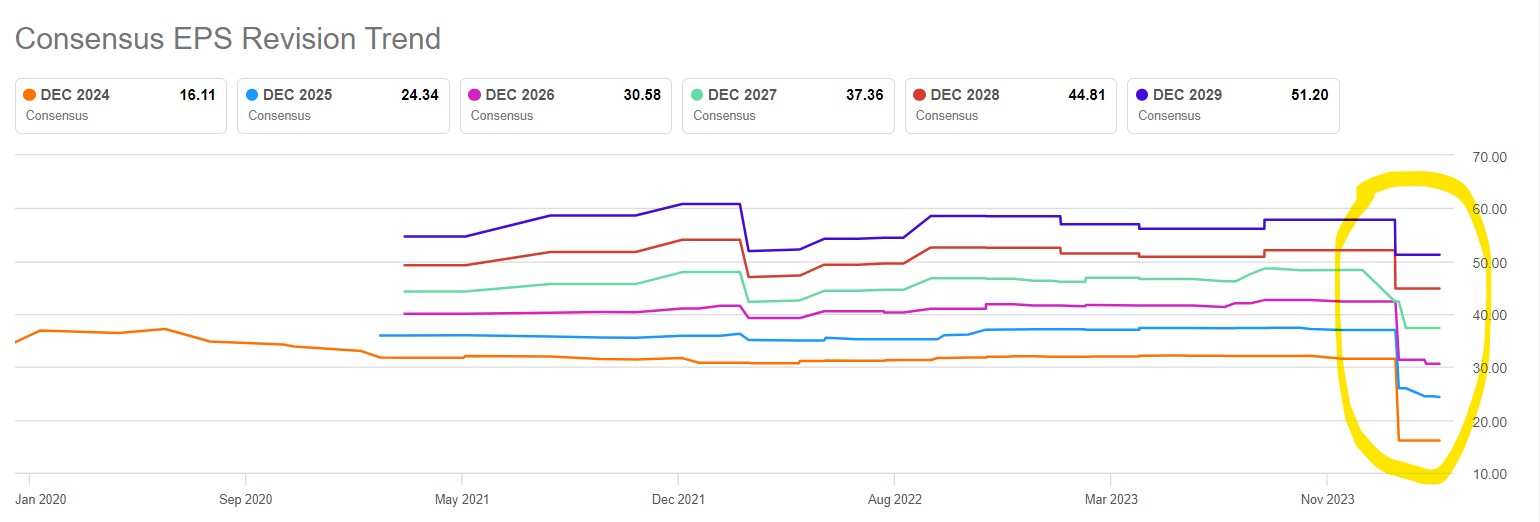

In recent months, we've seen analyst cut their estimates drastically for Humana's income projections as a result of these challenges. In the last 3 months, the average estimate for 2024 dropped by 48%, the average estimate for 2025 dropped by 34% and the average estimate for 2026 dropped by 27%. Estimates dropped anywhere from 15% to 25% for the years beyond 2027 which means that analysts expect this company's struggles to last for quite some time.

Analyst Estimate Revisions (Seeking Alpha)

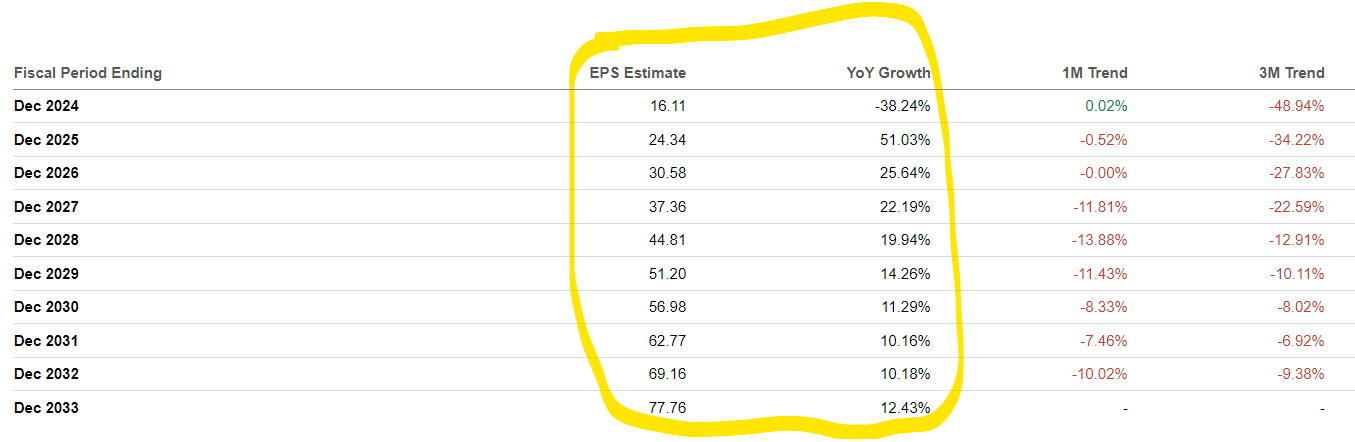

The encouraging news is that even with these large cuts, analysts still expect the company to be able to grow its earnings at a steady rate in the long run. Analysts now expect the company to generate $16 per share for this year and $24 for the next year both of which are in line with the company's own guidance I mentioned above. Beyond that, analysts expect the company to continue growing its net income at a steady rate, reaching $30 in 2026, $37 in 2027, $45 in 2028, $51 in 2029 and so on. Of course, it is always possible for the company to give another shocker and cut its guidance further in future years but it may also surprise to the upside if it can fix its cost structure.

Analyst Long Term Estimates (Seeking Alpha)

In the last year or so the company's profitability metrics took a hit as compared to its 5-year average but they still appear a bit better than its peers. For example, the company's EBIT margin of 4.30% is below its own 5-year average of 5.37% but significantly above the industry median of 0.75%. This was certainly not an easy year for the healthcare sector and just being able to post a profit at all would put this company in one of the top spots within its sector. The company seems to be pretty good at "Return On" metrics whether it's return on common equity, return on total capital, or return on total assets. These metrics tell us how good a company is at converting its business assets into profits. Humana has a return on equity of 16% which is worse than its longer-term average of 21% but significantly above the sector median. Similarly, the company's return on assets of 5.29% may be below its 5-year average of 7.39% but still significantly above the sector median which is actually in negative territory.

Humana Profitability (Seeking Alpha)

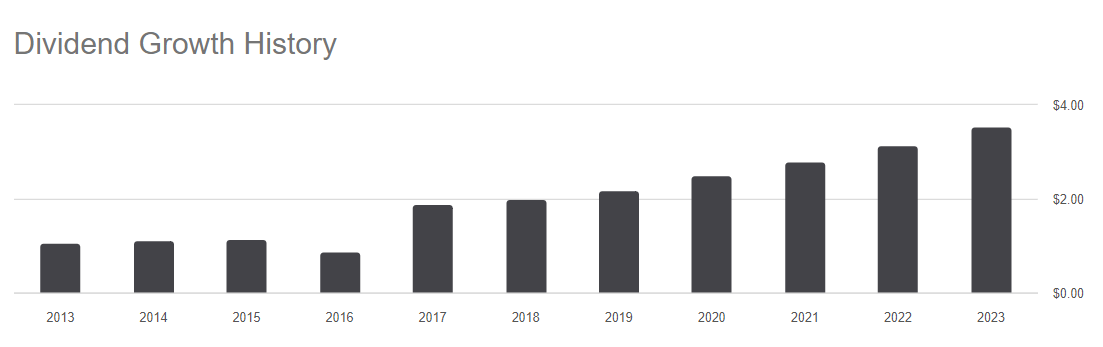

Humana has a low dividend yield of 1% but it has an impressive dividend growth history. In the last 10 years, the company raised its annual dividend from $1.07 per share to $3.54 per share, effectively more than tripling it. The current dividend of $3.54 seems to be well supported by the company's net income of $27 per share from last year of $16 per share from this upcoming year which gives it a payout ratio ranging from 13% to 20% for these two years indicating that it can easily afford the current dividend and even raise it more if it chose to do so. I still wouldn't treat this mainly as a dividend stock though because its yield is so low and it will take many years of dividend growth to give it a decent yield.

Humana Dividend History (Seeking Alpha)

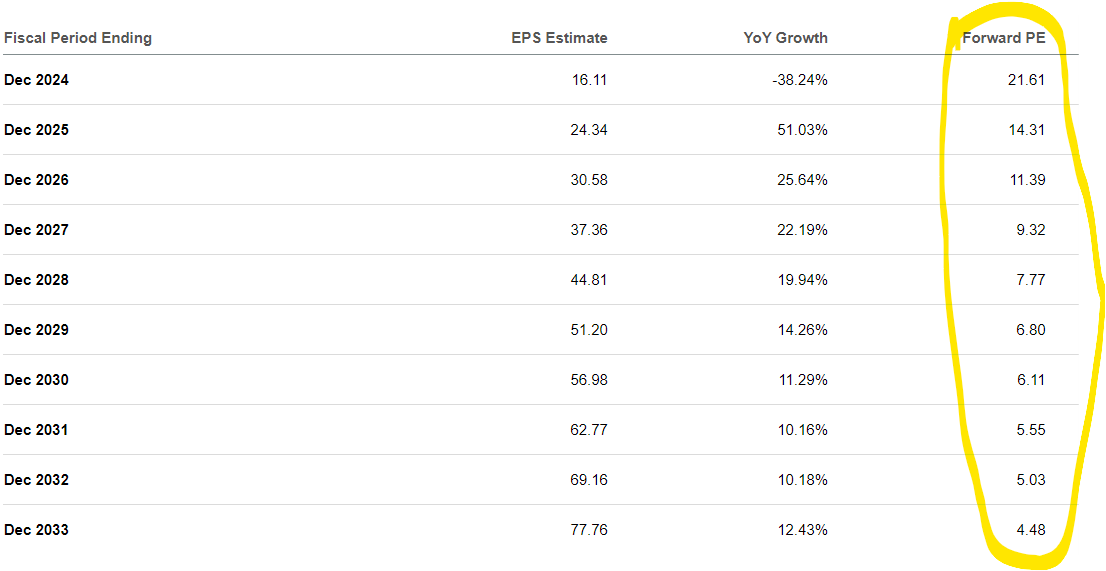

Assuming the company can meet or beat reduced estimates by analysts, its forward valuation looks cheaper and cheaper as you look further and further into the future. Based on this year's income estimates, Humana has a forward P/E of 22 but this quickly drops to 14 for 2025, 11 for 2026, and 9 for 2027 and stays in single digits for the foreseeable future after that. Again keep in mind that this is a big if and assumes that the company will meet or beat these estimates. The average P/E for a healthcare company is about 16 so assuming that the company meets its 2026 estimates, it might have a 40% upside between now and 2026 as its forward P/E will be 11 which indicates a deep discount.

Humana Forward P/E (Seeking Alpha)

To be clear, CMS will likely keep putting more pressure on insurance companies and competition will continue to attack from both sides to steal market share so these issues that caused the company's stock to decline in the first place will not be going away anytime soon. The company will most likely struggle with these two forces for quite some time and it will have to find a way of cutting its costs perhaps by renegotiating its contracts with healthcare providers.

There are still reasons to be hopeful though. The government is cutting its payout to insurance companies but not by that much. Last year it only cut its payouts by 1.5% in total and this is still manageable. Second, even with per-contract payments dropping, the volume of contracts is rising because more and more people are qualifying for Medicare benefits as the population gets older. Third, the company is not completely dependent on government payments either since it has a large and growing private business that's focused on non-Medicare Advantage contracts. This part of the business is likely to continue growing for the foreseeable future and help the company meet or beat analyst estimates in the long run.

This year's sharp drop in Humana's stock price might have provided a buying opportunity for long-term focused investors who have faith in the company's long-term prospects. As long as you are realistic about the challenges faced by the company and keep your expectations in check, this may not be such a bad stock to own in small quantity, especially after its correction earlier this year.