anouchka

anouchka

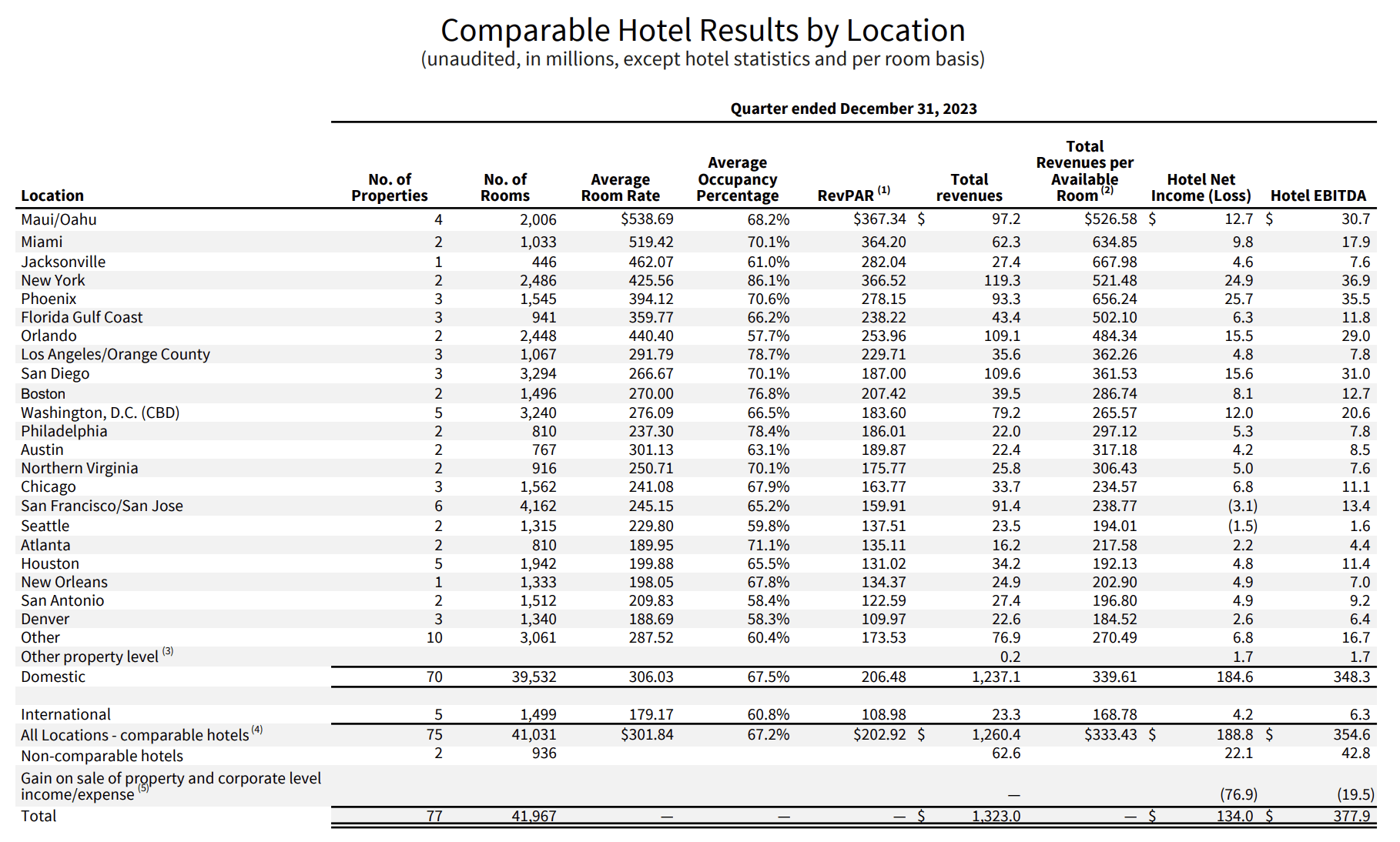

The short interest in its common shares of Host Hotels & Resorts (NASDAQ:HST) grew to roughly 5.35% in February even as the largest hotel REIT reported a beat on revenue for its fiscal 2023 fourth quarter. Revenue of $1.32 billion grew by 4.8% over the year-ago comp and outperformed consensus by $30 million. The REIT also last declared a quarterly cash dividend of $0.20 per share, kept unchanged from its prior distribution and $0.80 per share annualized for a 3.8% dividend yield. HST owned 77 luxury and upper-upscale hotels spread across 41,967 rooms at the end of its fourth quarter with comparable hotels notching a RevPAR of $202.92 and a 67.2% average occupancy percentage. These are great metrics with HST's $15 billion market cap being driven by just 77 hotel properties.

Host Hotels & Resorts Fiscal 2023 Fourth Quarter Supplemental

HST is up 8% since the start of 2024, sitting within a small basket of equity REITs with positive year-to-date returns. What's the play here? The bears think the commons are overvalued. HST is trading hands for 10.6x the midpoint of its fiscal 2024 FFO guidance range of $1.92 to $2.04 per share. For some context, peer lodging REIT Sunstone Hotel Investors (SHO) is trading for 13.5x times the midpoint of its 2024 FFO range of $0.78 to $0.90 per share. Park Hotels & Resorts is trading for 8.17x its 2024 guidance midpoint of $2.02 to $2.22 with DiamondRock Hospitality (DRH) swapping hands for 10x the midpoint of its range of $0.88 to $1.02 per share for 2024.

HST's fourth-quarter revenue growth came on the back of comparable hotel RevPAR growth of 8.3% for the full fiscal year 2023 versus 2022. This growth came despite the August Maui wildfires which impacted occupancy at three Maui hotel properties that formed HST's highest average room rates. HST placed the impact of the wildfires on fourth-quarter comparable hotel RevPAR at 130 basis points with a $9 million hit to comparable hotel EBITDA. Hence, a normalization should form a tailwind for 2024 with the high end of HST's FFO guidance range assuming faster recovery at the Maui resorts.

Fitch Ratings

The internally managed REIT recently saw its investment grade credit rating upgraded one notch to "BBB" by Fitch in December. This meant a return to HST's pre-pandemic rating level with the credit rating agency highlighting the REIT's low leverage, best-in-class asset quality, and prudent balance sheet management as reasons for the upgrade. HST has a 99% unencumbered property portfolio which means a potent source of liquidity and balance sheet flexibility.

Host Hotels & Resorts Fiscal 2023 Form 10-K

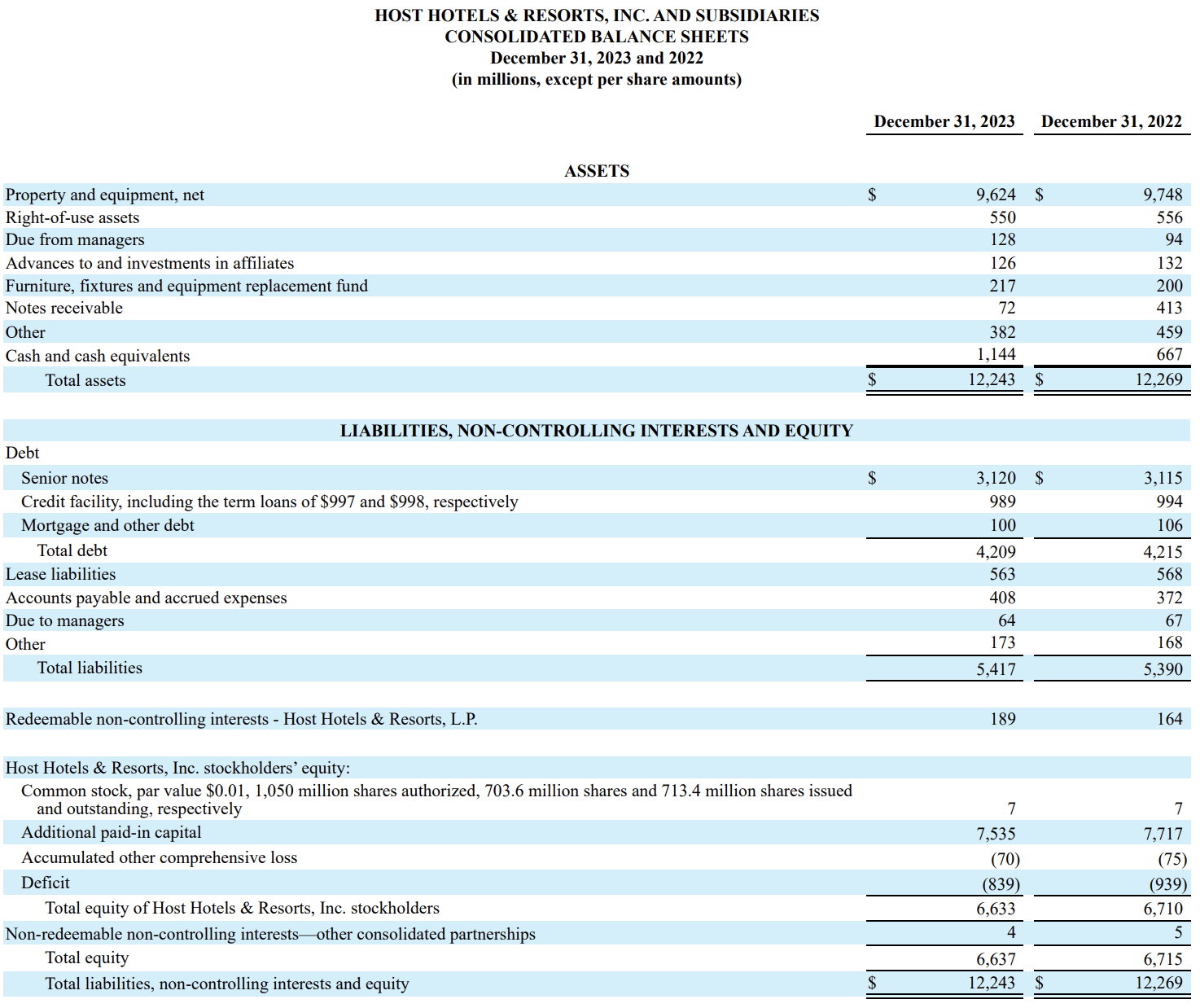

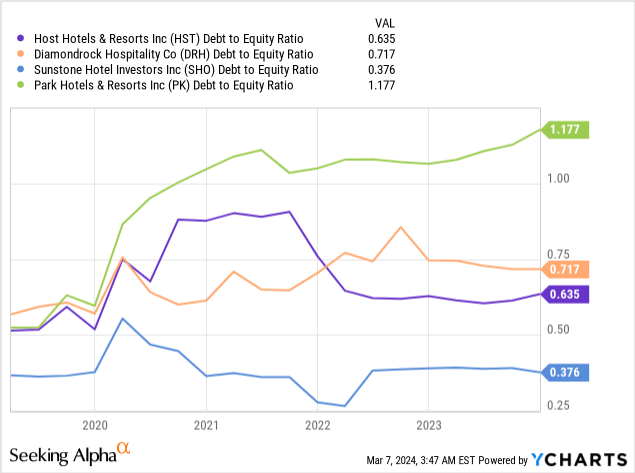

The REIT held total cash and cash equivalents of $1.14 billion at the end of its fourth quarter, up from $667 million in its year-ago comp. Total equity at $6.64 billion dipped by $77 million over its year-ago comp with HST's debt-to-equity ratio at the end of the fourth quarter at 0.64x. HST has operated around this level since mid-2022 which is a lower level of gearing than comparable hotel REITs DiamondRock and Park Hotels.

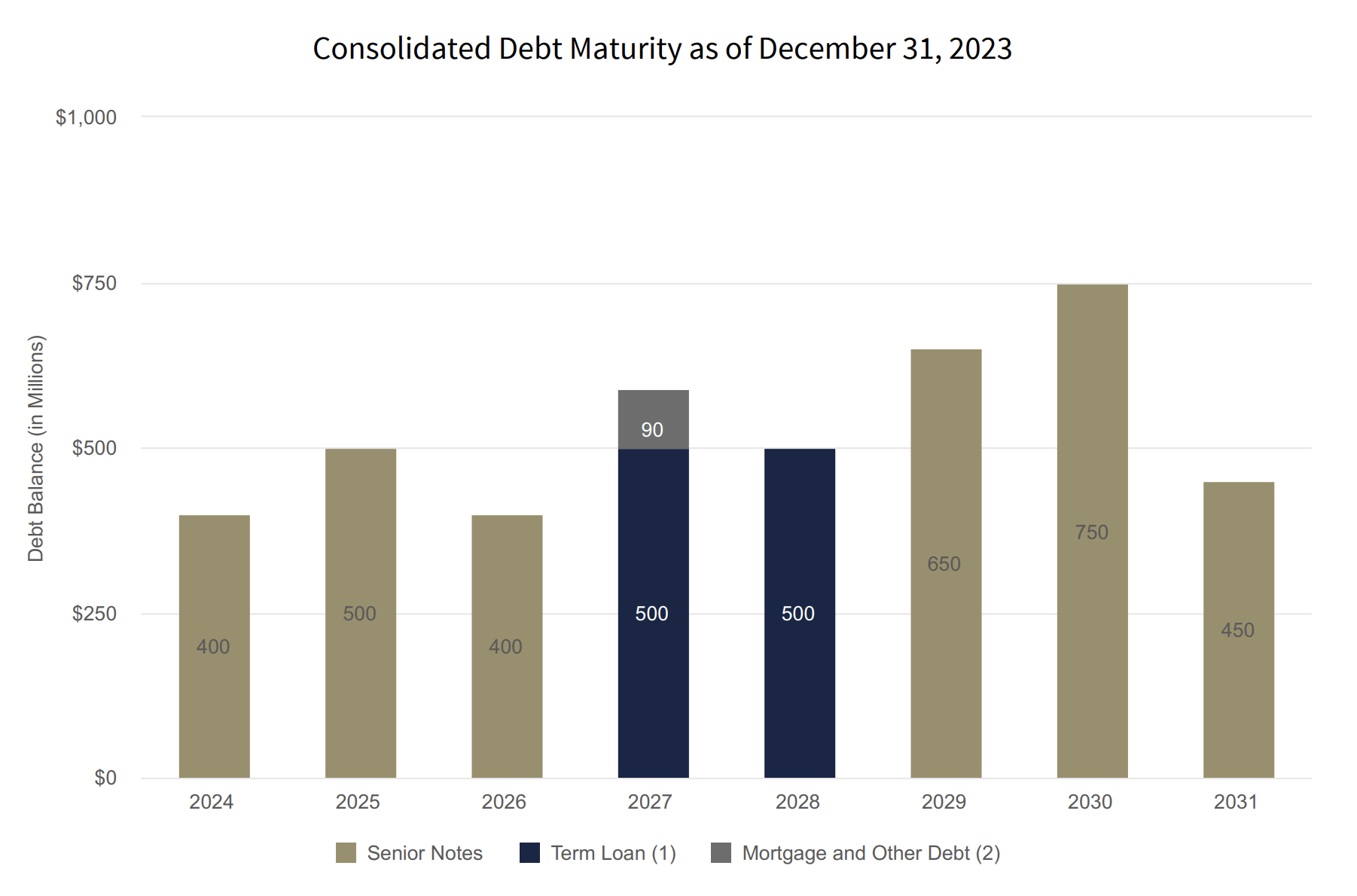

HST faces a modest wall of maturities with a weighted average maturity of 4.2 years at a 4.5% weighted average interest rate at the end of its fourth quarter. The REIT has $400 million coming due next month, this is set against $2.9 billion in total available liquidity including $217 million of FF&E reserves and a $1.5 billion credit facility. Overall, HST's flattish debt maturity schedule means less risk of FFO headwinds, with its weighted average interest currently below the Fed's funds rate of 5.25% to 5.50%.

Host Hotels & Resorts Fiscal 2023 Fourth Quarter Supplemental

The US skirting a soft landing continues to form a heightened risk as its leisure offerings for upper-tier centric customers would take a hit in a recession. This comes as HST's urban exposure continues to see tepid recovery on a slower return of business transient. Fourth quarter room nights at its downtown hotels were still down 15% versus 2019 even as 2023 business transient demand grew by 12% over 2022. The REIT expects this to pick up further in 2024 but is not anticipating a 2024 recovery to the 2019 level. HST paid out a special dividend of $0.25 per share for a total dividend of $0.90 per share in 2023, a 4.3% yield on the common shares. The REIT's fourth-quarter FFO at $0.44 per share means it's currently covering the base dividend by 220%, opening the scope of further special dividend payments through 2024 especially with FFO being guided to grow by 6 cents year-over-year at the midpoint of 2024 FFO guidance. HST also has an ongoing share repurchase program with a remaining capacity of $792 million after the repurchase of 1.9 million shares during the fourth quarter. This is fundamentally a high-quality REIT operating great hotel properties and forms a hold at its current level.