da-kuk

da-kuk

December, last year I wrote an article on Horizon Technology Finance (NASDAQ:HRZN) laying out an argumentation of why, in my opinion, HRZN was not the right business development company, or BDC, pick.

The key arguments were the following:

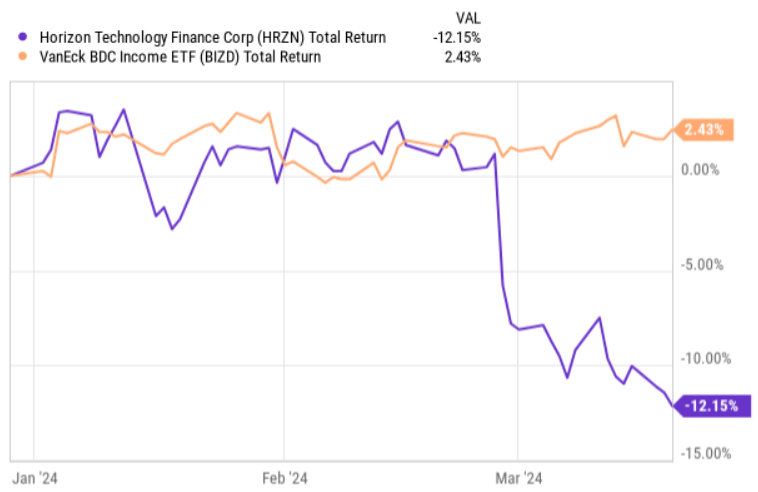

Since then, HRZN has clearly underperformed the BDC index and lost a meaningful share of its market cap.

Ycharts

As indicated in the chart above, until the earnings date HRZN managed to perform somewhat in line with the overall BDC market, but it was really the unpleasant earnings profile that sent the Stock price deep in the negative total return territory. Adjusted for the dividends, the Stock has decreased by ~15% (on a YTD basis).

I will go through some of the most important metrics in the Q4 2023 earnings deck and comment on how I view HRZN as an investment now once the Share price is materially lower from the date when I issued my bearish thesis.

In a nutshell, the fact that the market punished HRZN right after the earnings publication is fully justified and reflective of the underlying fundamentals.

Looking at one of the most important metrics for BDCs - net investment income - we can see that HRZN has clearly struggled during Q4 2023 to preserve its NII generation relative to the previous quarter.

Namely, the net investment income for the fourth quarter landed at $0.45 per share compared to $0.53 per share in the third quarter of 2023. This is a significant drop.

The reason behind this decline was driven by negative dynamics at both revenue and cost end. On the revenue or income side, the decline was quite material due to lower yield generation from the recent investments that have been signed at smaller margins than the previous investments. The cost side, however, was inflated by several factors such as increased cash interest expense, higher professional fees and administrative expense.

On top of this, we have to factor in HRZN's equity dilution that took place in Q4 2023 as the Management decided to de-risk the balance sheet and prepare for the potential distress going forward.

Moreover, if we assess the details further that are not directly related to cash generation, but more reflective of the underlying value, the picture is not that rosy, either.

For example, the most recent quarterly figures revealed a continued trend in the net asset decline due to rather tangible net realized loss items. This goes hand in hand with the overall market dynamics in the VC space, where company valuations are increasingly marked down as the financing has become excessively expensive and hard to access.

Summing all of this together, HRZN was forced to record a $0.70 per share reduction in its NAV figure compared to the level of the previous quarter.

As a result of this, the leverage level still remained at an aggressive territory of around 1.4x in terms of debt to equity metric, implying a massive deviation to the upside from the BDC sector average of 1.17x.

Besides this, there are two additional elements I would like to underscore.

First, the portfolio yield prospects are set to deteriorate as the incremental investments are clearly converging back to a more normalized levels.

Dan Trolio - CFO, in the most recent earnings call gave a nice flavor of the yields that are associated with new investments:

For the fourth quarter of '23, we achieved onboarding yields of 13.8% compared to 13.9% achieved in the third quarter. Our loan portfolio yield was 16.8% for the fourth quarter compared to 14.5% for last year's fourth quarter.

Again, this is not the first quarter when we can observe negative spreads between the new investments and the previous ones that have been assumed, when the overall VC investment environment was more favorable. In fact, we can already now notice some pressure on the net investment income, where the interest income component is gradually declining due to smaller spreads between HRZN's cost of capital and portfolio yield.

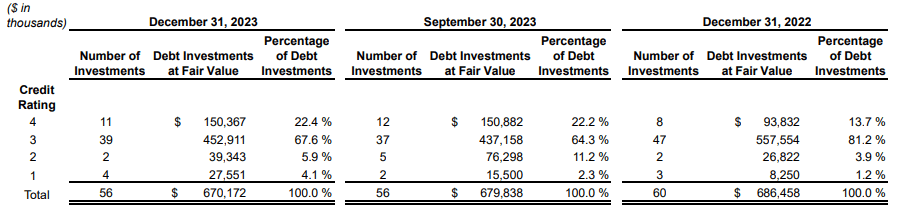

Second, the overall portfolio health of HRZN still remains challenging and prone to new non-accruals.

HRZN, Q4, 2023 earnings

In the table above, we can see that the "credit rating 1" category has experienced a meaningful uptick from the Q3 2023 level. This category implies that investments are effectively close to being fully written down.

Putting all of the aforementioned dynamics together, Horizon Technology Finance seems to be in a rather unpleasant position. The portfolio yield is set to go down, which will per definition impose a downward pressure to grow or even sustain the current NII generation. The portfolio quality also remains weak and, as predicted in my previous article, we can already now observe the consequences of carrying a pure-play exposure to an inherently volatile VC segment. On top of that, Horizon Technology Finance's leverage is still excessively high and above BDC average, which magnifies the potential negative effects from new non-accruals.

What is surprising for me is that despite all of this, Horizon Technology Finance trades at a premium to NAV (ca. 19%). Plus, if we adjust for the special dividends that are likely to decrease due to the weakening of the underlying fundamentals, the core forward dividend yield lands at ~ 11.7%, which is not that attractive compared to the BDC average.

All in all, it is a hold for me; and the reasons why I am not recommending to short the Stock is because Horizon Technology Finance (and VC sector in general) is heavily exposed to interest rate dynamics, where if the SOFR starts to go down, it is very likely that HRZN will experience a meaningful rebound.