AndreyPopov/iStock via Getty Images

AndreyPopov/iStock via Getty Images

HealthEquity, Inc. (NASDAQ:HQY) is a managed healthcare provider that plays in the Health Savings Account market. On March 19th, the company announced a beat on both revenues and EPS which has made me revisit a stock I always thought was expensive. As the share price has been largely unchanged in the last five years and sales and revenue have grown at rapid rates, I think it's time to take another look at the company. In this article, I'll delve deeper into the latest results, assess the company's strategy, and provide my thoughts on why I believe the valuation is attractive today.

HealthEquity is a managed healthcare provider that provides flexible spending accounts (FSAs), health reimbursement arrangements (HRAs), but most principally, health savings accounts (HSAs). Through HealthEquity, individuals can make better decisions related to their health spending needs and better manage their healthcare needs. Through their products, they also allow individuals to save for future medical expenses. Often times, HealthEquity partners with employers who offer HealthEquity services to the employees of these companies as part of their benefits packages and perks.

Health Savings Accounts came about in the early 2000s when the U.S. Congress decided to change up government intervention in the medical profession. As they became law in 2004, they replaced the previous system which was called Medical Savings Accounts (MSAs).

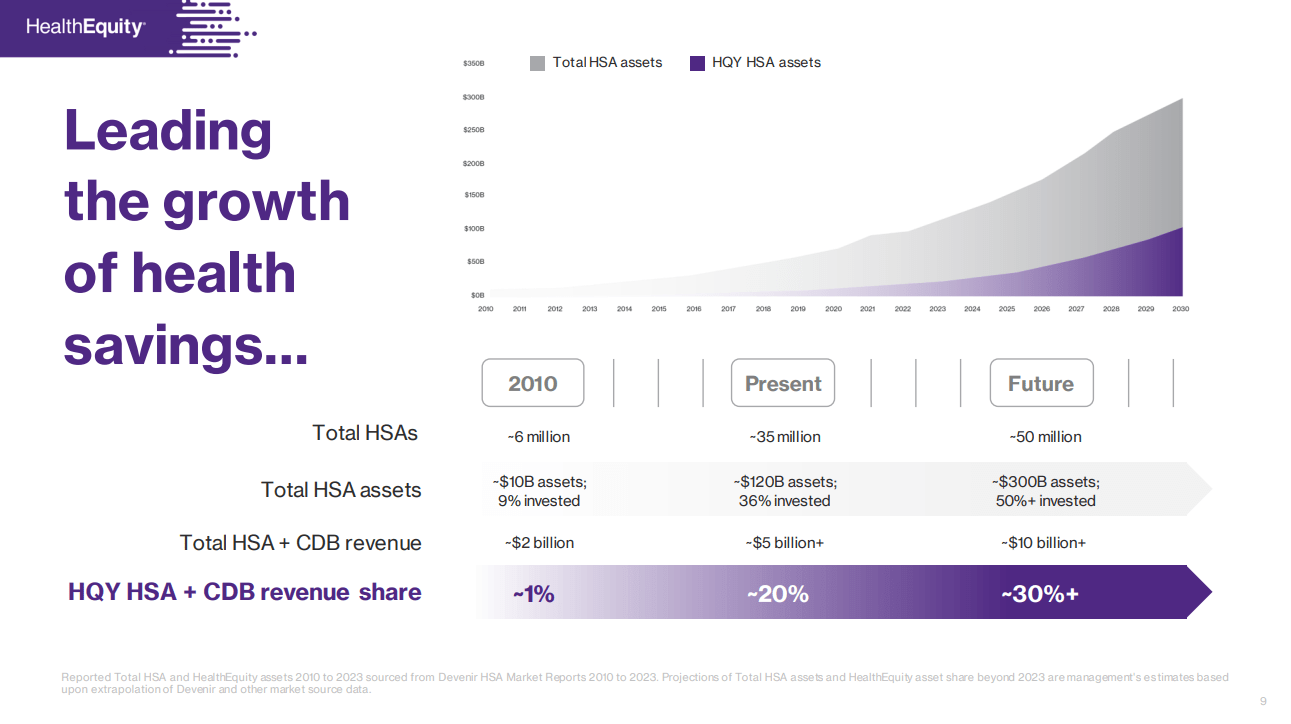

While there are some differences between the two, the real advantage of a Health Savings Account is that contributions are not taxable to the employee and both the employer and employee are able to make contributions. Since you can take your HSA from one employer to another, remaining cash balances in the account are carried over year by year and interest earned in the account is tax-free. As such, this can be a great method for individuals to save up for qualified medical costs for things like doctors' visits, hospital expenses, lab, x-ray, and diagnostic services, prescription drugs, dental care, vision care, and much more. Due to their flexibility and versatility, the total number of HSAs (at least at HealthEquity) has increased 6-fold since 2010. In the HSA and consumer-directed benefits (CDB) space, the company has a 20%+ market share.

Investor Presentation

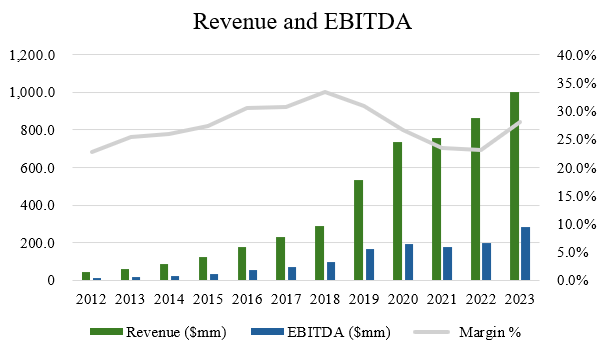

When looking at the historical financial performance of HealthEquity, the company has been growing at eye-watering rates of return, particularly as a result of the growth in HSAs. Over the last 10 years, the company has compounded revenues at a 32.0% CAGR and EBITDA at a 33.4% CAGR. In the last 5 years, the company's growth rates are still impressive with revenue and EBITDA growing at CAGRs of 28.3% and 24.0% (source: S&P Capital IQ).

Author, based on data from S&P Capital IQ

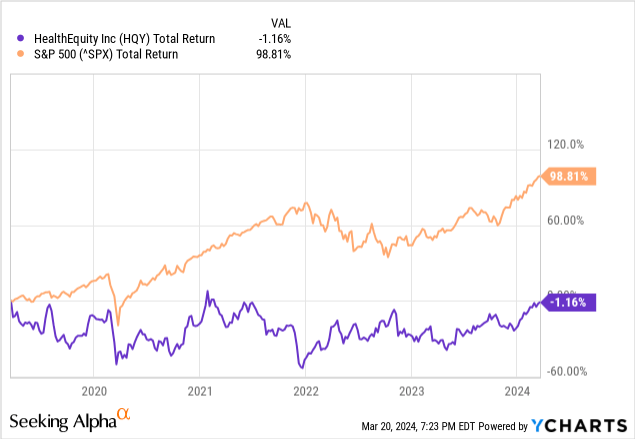

Despite the company's impressive financial performance with growth in both the top and bottom line, the company's share price performance has been a laggard. For example, over the last five years, the company's shares are nearly unchanged down just 1.1% while the S&P500 has almost doubled when factoring in both price appreciation and dividends.

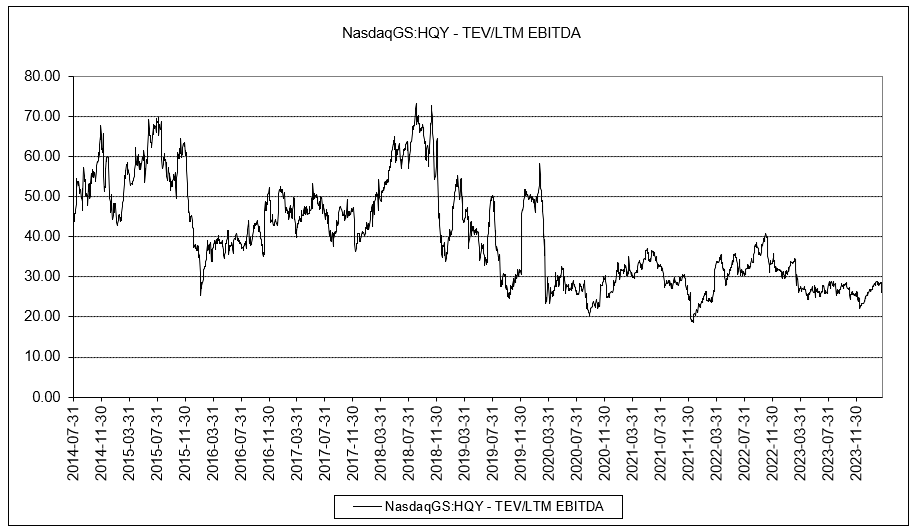

Why has HealthEquity been underperforming in spite of its high growth rates? Well, when looking at the historical EV/EBITDA multiple, we can see that shares of HealthEquity had traditionally been quite expensive as investors paid up for the company's growth. Today, with shares trading at 26.8x EV/EBITDA, I think the stock is worth a revisit to see if shares are a buy today.

Historical EV/EBITDA Multiple (Author, based on data from S&P Capital IQ)

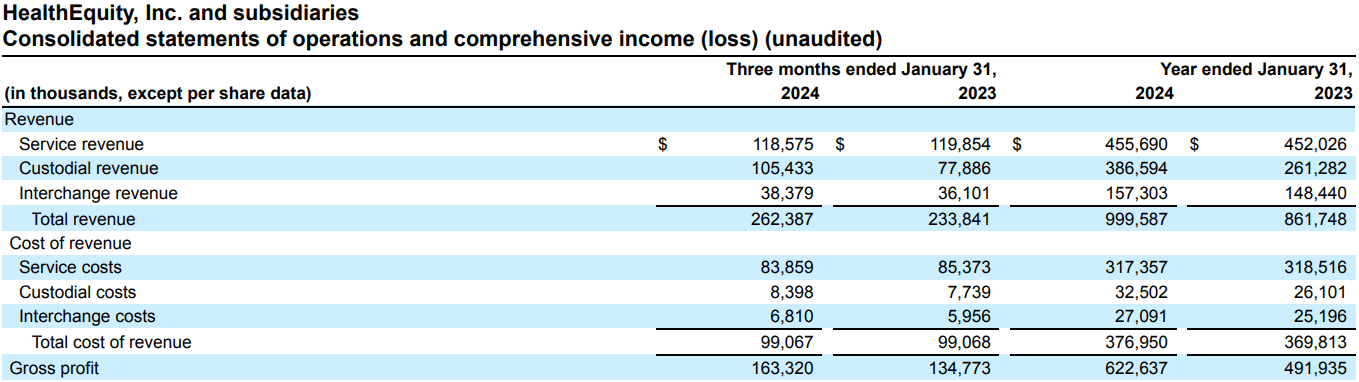

When looking at the recent Q4 and full year 2024 results for HealthEquity, the company reported a beat on both sales and EPS. For the quarter, revenue clocked in at $262.4 million, which was up 12.2% on a year over year basis, but missed estimates by 3.4 million. For the full year, revenue came in just shy of a billion at $999.6 million which was 16.0% higher than the year prior.

As mentioned previously, much of this growth has been driven by more customers opening HSAs with HealthEquity. For F2024, the company had total members under the program grow 9% with total assets increasing 14%. With an additional 949,000 new HSAs during the year, this brought the total number of HSA members under HealthEquity's umbrella to 8.7 million members with 15.7 million total accounts.

Breaking the revenue down by segment, service revenue continued to be the largest contributor to revenue at 45% of total sales but was down slightly (-1.1%) on a year over year basis. Service revenue generally comes from fees which are paid by network partners, clients, and members for the administration services the company does in conjunction with its service offerings via HSAs and other CDBs. Service revenue growth has been a bit muted this year given the impact from National Emergency. With the impact from calendar 2023 behind the company now, I would foresee service revenue to pick up again in the high single digits for F2025.

Company Filings

The biggest standout in terms of growth, however, was the company's custodial revenue which was up 35% during the quarter and 48% for the full year. Custodial revenues, which are generated from clients assets as the custodian of their accounts, has been a growing part of HealthEquity's business. With improving custodial yields at around T+75 bps for the enhance yield business with a 4.5 year repricing cycle compared to T+10 bps for the basic yield side, HealthEquity has been a benefitting from rising spreads as well as more and more customers moving to enhanced rates.

At quarter end, more than 30% of HSA cash was in enhanced rates and I would expect that to hit 50%+ over the next two to three years. Why? Management has already stated moving a significant portion of the business to enhanced rates will be a major factor in doubling the company's EPS over the next three years. In my view, the spreads also seem to be manageable from here on out due to the fact that management doesn't view spreads narrowing as a result of mostly locking this in with partners.

Finally, with respect to the company's interchange revenues, this segment's revenues were up 6% on a year over year basis for the quarter. Interchange revenues can be a bit hard to forecast and predict, as they are generated from fees paid by merchants on payments that HealthEquity members make using the company's physical payment cards and on the company's virtual payment system and management doesn't provide guidance by segment. It seems to be that interchange revenues are likely to grow at the same pace as service revenues as more member accounts are opened so I foresee high-single digit growth for this segment going forward.

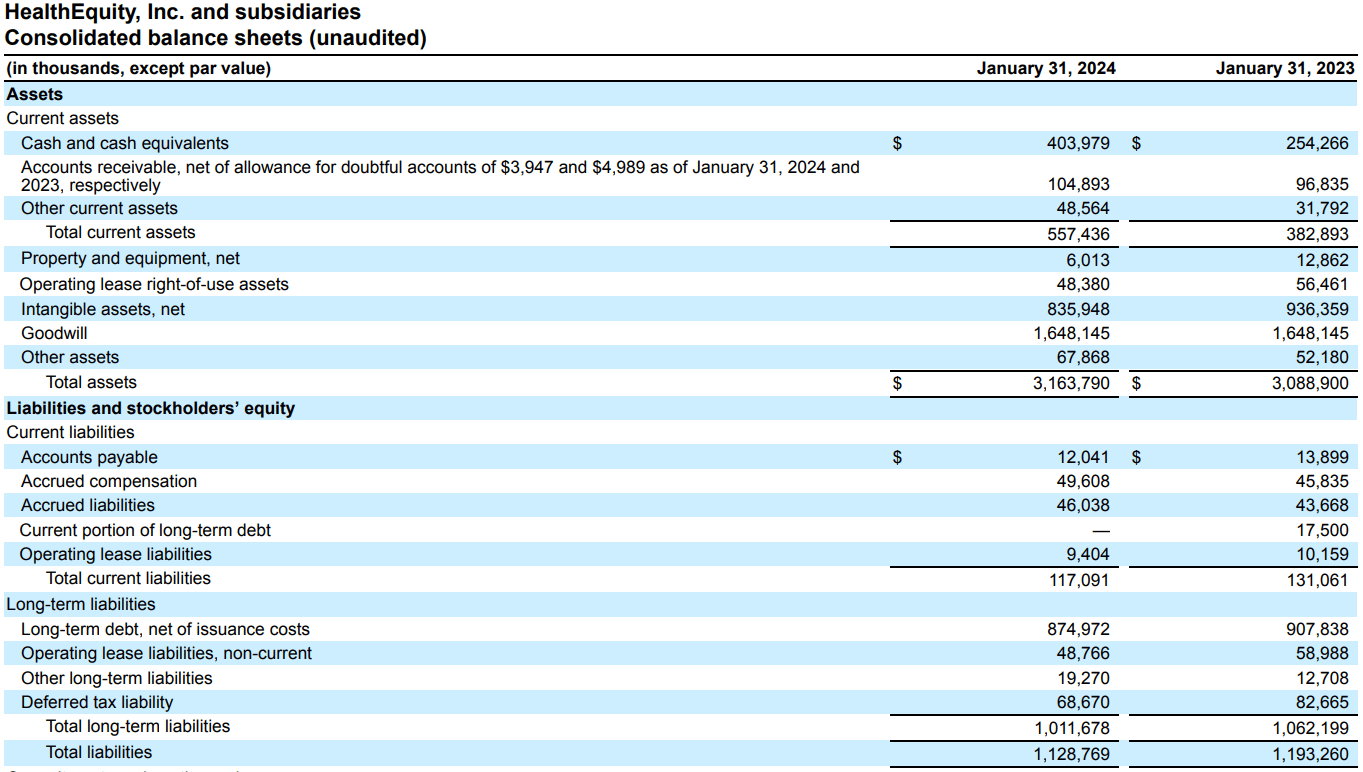

As for the company's balance sheet, at quarter end, HealthEquity had $404.0 million of cash on its books against $875.0 million of long-term debt. With $369.2 million in EBITDA for the F2024 year, the company has a Net Debt to EBITDA ratio of 1.3x so the leverage profile is very reasonable. With the announcement of the BenefitWallet acquisition, this should increase slightly but it seems like there's more room to add leverage should the company want to take on more debt. Overall, I'm pretty optimistic on the BenefitWallet transaction as this should increase the total assets under management by about 10%, adding $2.7 billion of client assets. As these HSAs get transitioned into the HealthEquity platform, HealthEquity has just removed a competitor from the market so the deal seems strategically sound, leveraging synergies and expanding its current customer base.

Company Filings

Based on the 7 analysts who cover HealthEquity's stock, all 7 have buy ratings with an average price target of $99.00, with a high estimate of $110.00 and a low estimate of $92.00 (source: TD Securities). From the current share price to the average price target one year out, this implies potential upside of about 21.7%.

Based on the historical EV/EBITDA chart I presented earlier, the company is trading for about 26.8x EV/EBITDA, which is close to the cheapest multiple it's ever traded at. It's difficult to find adequate comparables to HealthEquity, but keep in mind that this is a very capital light business with capex that averages less than $10 million per year. So in my view, I don't believe this multiple to be unreasonable.

With the announcement of the Benefit Wallet and given the guidance for FY2025, management is now guiding for $438 to $458 million of EBITDA. At the mid-point of this guidance range at $448 million, assuming the company takes on new debt to fund the full purchase price of the $425 million acquisition, this would put the forward EV/EBITDA multiple closer to 22.5x EV/EBITDA which is a below market multiple for a business that can likely grow in the mid-teens long-term through a combination of asset growth (i.e. more custodian revenues), new HSA account openings, and a small bit of M&A.

In terms of the risks to my investment thesis, the biggest one would be changes in legislation to the Health Savings Account. As of my knowledge, there haven't been any changes from Congress on this front, but monitoring the legal developments and legislation around HSAs and CDBs will be important to watch. Secondly, despite being a healthcare services company, HealthEquity is similar to a financial services company in that it is exposed to similar risks via interest rates. While some of this is protected as spreads don't fluctuate too much, adverse and sudden changes in interest rates could be a negative headwind that impacts the earnings and profitability of the company.

Overall, HealthEquity has been stealing market share in the Health Savings Account space and has been a strong performer, despite its share price saying otherwise. With strong results this quarter and an acquisition and balance sheet that should propel future growth, the company is poised to benefit from industry tailwinds and the outlook looks very favorable. In my view, while the share price has essentially gone nowhere in the last 5 years, the valuation multiple has compressed to a much more reasonable 22.5x forward EV/EBITDA so I think the valuation is attractive. For a company that can grow in the mid-teens long-term, I think investors should expect double-digit annualized returns going forward for the company which is why I rate shares as a 'buy' today.