JasonDoiy

JasonDoiy

First wave artificial intelligence ("AI") stocks obviously include NVIDIA Corporation (NVDA) and Super Micro Computer, Inc. (SMCI), as these companies are already seeing a positive financial impact from orders. However, there is likely to be a second wave of AI-related stocks that have not yet seen a significant beneficial impact on profits, but potentially could in the near future. Nvidia CEO Jensen Huang recently said we are only at the beginning of an AI computing ramp that will last for years. This suggests there could be many more winners in this sector over the coming years.

Let's take a closer look at one company that is planning for a big future in AI.

Hewlett Packard Enterprise Company (NYSE:HPE) is offering consulting services to help companies implement AI in their business models. (Hereafter, I will refer to this company as HPE.) HPE Greenlake offers an AI cloud platform as well as data analytics and high-performance computers. This company also offers software and storage and secure data management solutions. HPE Servers and HPE Financial Services are other important divisions.

In 2019, Hewlett Packard Enterprise Company acquired Cray, Inc. for $1.3 billion. Cray supercomputers have made some of the world's most powerful computers. These computers are used for simulations, deep learning, AI, and more. Going forward, HPE is focused on AI infrastructure, supercomputing, and AI platform software.

As noted in the statement from HPE below, management expects the total addressable market, or "TAM," to expand significantly over the next few years. It states:

"HPE is successfully shifting its portfolio to higher-growth, higher-margin businesses, increasing its long-term profitability potential. When combined, HPE's largest growth businesses - Intelligent Edge, HPC & AI, and the company's future Hybrid Cloud segment - are expected to exceed 50% of the company's total segment revenue by fiscal year 2026. The company is continuing to invest in these areas to increase recurring revenue and further expand margins. HPE expects to increase its total addressable market by nearly $100 billion over a four-year period to more than $340 billion, led by a larger market in AI."

Antonio Neri is the CEO at HPE, and he recently announced the acquisition of Juniper Networks, Inc. (JNPR). This $14 billion deal is being made with the goal of shaking up the networking industry and integrating another key component, which could help make HPE a leader in AI.

What's notable is that the former CEO of Cisco Systems, Inc. (CSCO) spoke out about this HPE acquisition of Juniper Networks, and he gave quite a strong endorsement. These comments were detailed in an article which stated:

"Former Cisco CEO John Chambers is giving the thumbs up to Hewlett Packard Enterprise CEO Antonio Neri's bid to make HPE-Juniper Networks a force to be reckoned with in the AI era. "Antonio is a competitor, turned business partner, and a friend who I trust with my life," said Chambers in a LinkedIn post on Tuesday. "I believe HPE will become a top AI leader in the industry with Antonio at the helm."

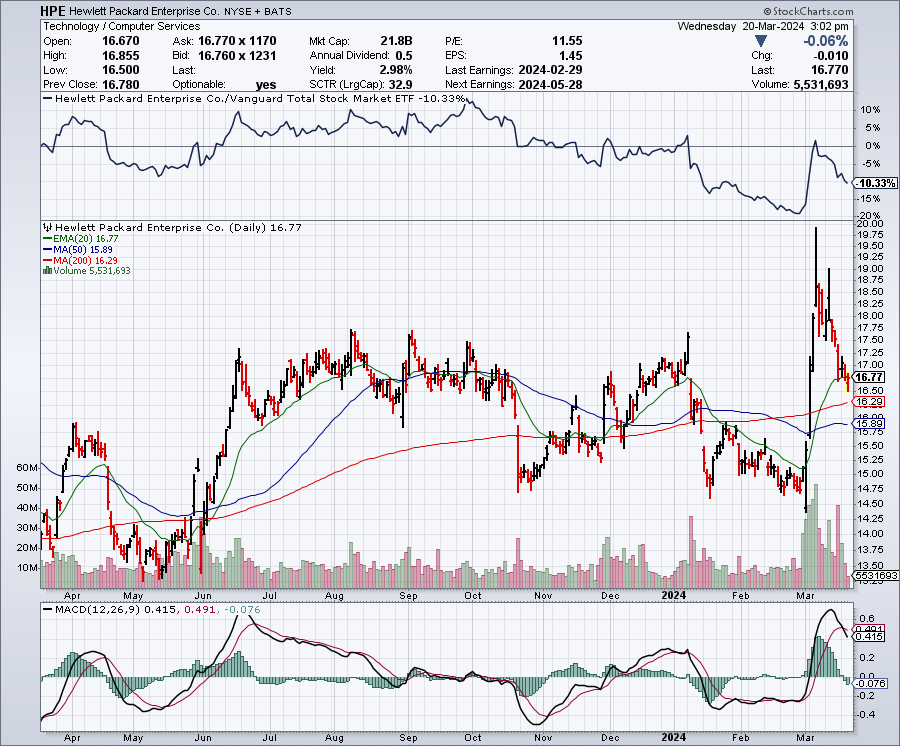

As the chart below shows, HPE shares recently surged from around $15 to nearly $20 per share. The stock has since given back some of those gains and it now trades in the $16 range. The 200-day moving average is $16.28 and the 50-day moving average is even lower at $15.90 per share. With the recent strength this stock is exhibiting, the 50-day moving average might soon move over the 200-day moving average, creating a very bullish "Golden Cross" formation. With the stock currently trading above the 50-day and 200-day moving average, I would look to buy more shares at $16 or below, which could happen if the market has a pullback.

StockCharts.com

HPE appears to be well-positioned to be a big beneficiary of AI and possibly even a leader in some aspects. After all, it is targeting the AI market and it is expanding into other important areas with the acquisition of Juniper Networks. HPE has even entered into a strategic collaboration with Nvidia. It announced a generative AI full-stack solution as well as AI-native software and hybrid cloud solutions. In December, HPE stated:

"This week in Barcelona, we extended our strategic collaboration with NVIDIA by announcing a new generative AI full-stack solution co-engineered and pre-configured specifically for enterprises to quickly fine tune foundation models using private data that can be deployed everywhere. We also announced new AI-native and hybrid cloud offerings that bring together HPE's leadership in hybrid cloud, supercomputing and AI/ML software to enable organizations to become AI-powered businesses."

I know some investors won't be able to consider a legacy tech company like HPE as having much potential in anything, especially in something that is as fast-growing as AI, but we have seen similar examples of this happening in the past.

For example, in 2017, Microsoft Corporation (MSFT) was trading in the $50 range and many investors thought of this company as a has-been. Microsoft had missed many important tech trends and did not capitalize on huge themes as other companies did in areas like search and mobile. But, fast forward a few years and now you can see investors paying a premium valuation for Microsoft and thinking of it as a leader in AI, with a commensurate share price of over $400. That is an eight-fold gain in the share price, in just 8 years.

This is why it makes sense to never underestimate legacy tech companies because they just might be positioned to catch a secular growth opportunity. It also certainly doesn't hurt that John Chambers believes HPE could be a leader in AI.

For 2024, HPE is expecting earnings of $1.83 to $2.02 and it recently stated it is targeting an 8% increase in its dividend in 2024. Analysts expect HPE to earn $2.05 per share in 2025, and $2.14 per share in 2026. These numbers don't suggest enough growth for most investors to get excited about, but it is possible these estimates are too low if HPE is truly able to capitalize on AI opportunities.

With the stock in the $16 range, HPE shares are trading for just about 8 times earnings, which is far below the market average multiple of around 20 times earnings. If HPE shows some better-than-expected growth in the coming years, the multiple has room to expand significantly.

As for the balance sheet, HPE has about $12.9 billion in debt and nearly $3 billion in cash. It's not the best balance sheet in the tech sector, and I would like to see this company pay down the debt, but it is not unreasonable for a company with nearly $30 billion in annual revenues.

HPE pays a quarterly dividend of 13 cents per share, which totals 52 cents per share on an annual basis. This provides a yield of over 3%. The dividend has been growing over the years and should continue to grow. For example, in 2015, the quarterly dividend was just 5 cents per share, so it has more than doubled in less than 10 years. The dividend appears very safe because the payout ratio is low, with the earnings estimates being around $2 per share.

The tech space is extremely competitive, and there are other companies with larger R&D budgets and stronger balance sheets that are going after some of the same markets as HPE. This stock has been cheap for a long time, and it might be a value trap. However, if it is a value trap, it might not have a significant downside, especially considering it pays a solid dividend. The stock is currently trading above key support levels such as the 50-day and 200-day moving average, so this stock could be more susceptible to a pullback in a market downdraft. This means there could be greater short-term risks at current levels.

I am somewhat skeptical as to whether Hewlett Packard Enterprise Company can become a real AI leader, but given the potential upside and the business strategy to pursue AI opportunities, I believe it deserves the benefit of the doubt. I am impressed that Cisco veteran John Chambers has so much confidence in HPE, in terms of AI potential.

I think it is important to consider that at around 8 times earnings and with a yield of over 3%, there is probably not a lot of downside if Hewlett Packard Enterprise Company does not end up capitalizing on AI, but if it does, the upside could be very significant. This suggests that HPE shares have a very ideal risk/reward ratio. I am not planning to buy a big position, but I think a buy and hold of this stock makes sense, especially on pullbacks.