Spencer Platt

Spencer Platt

I can still remember when investors had to make a phone call to place a trade with a broker, who would charge a commission of as much as $100 for the purchase of 100 shares of a $50 stock. That was the going rate when I was a Financial Consultant at Merrill Lynch in 1993, which is unimaginable today. We have come a long way over the past thirty-plus years in terms of financial innovation for the retail investor.

The rise of computers during the 1990s, which helped bring the internet to the masses, led to the emergence of discount brokers like E-Trade and Scottrade. These online brokerages offered much cheaper commissions and eliminated the need for humans to serve as intermediaries in financial transactions. As a result, the number of households owning stocks soared by the turn of the century.

During the 2010s, our phones became mobile computers, otherwise known as smartphones, allowing investors to execute trades on the move. Robo advisors emerged with even lower fees and intelligent automation. Both full-service and discount brokers gradually lowered commission rates in a race to zero, but it was Robinhood Markets, Inc. (NASDAQ:HOOD) that spearheaded the effort to “provide everyone with access to financial markets, not just the wealthy,” according to company founder Vladimir Tenev.

Robinhood officially launched its phone app in March 2015 with zero commission rates and no account balance minimums in its attempt to unlock the micro-investor market. As a result, its customer base early on was predominantly Millennials with an average age of 26 who had little experience and just a few thousand dollars to invest. The clientele is not that much different today, except that Gen Z is becoming a meaningful percentage of the investor base. The average account balance is still approximately $4,000.

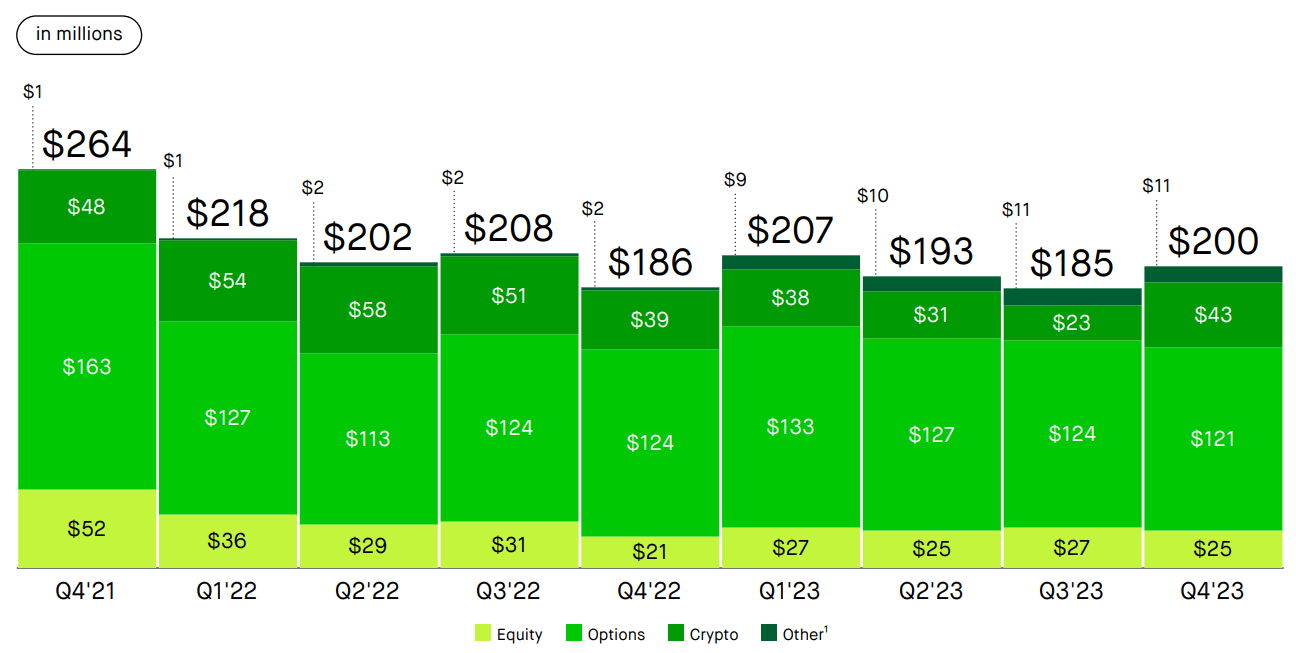

Given the account size, most of Robinhood’s active customers are trading, if not speculating, on a regular basis, and options are responsible for the bulk of trading activity with crypto a distant second.

Robinhood.com

I don’t believe this to be the foundation for a predictable and consistently growing business model. To the contrary, it is likely as irregular and unpredictable as the portfolio returns of its investors, which is why its customer base was cut in half during the last bear market in 2022.

Businessofapps.com

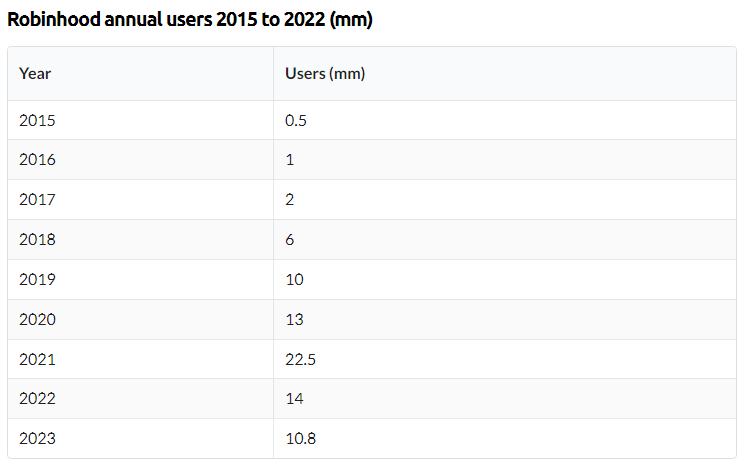

Robinhood’s peak in customers and market capitalization came in 2021 during the pandemic, which was also the year it went public. The company had multiple tailwinds at that time that are not likely to repeat. Millions were stuck at home on their computers with limited choices for entertainment. Three rounds of stimulus checks had been issued to every American household over the 12-month period from March 2020 to March 2021, whether they needed the money or not. This was a windfall for many newbie investors who had lots of time on their hands. No wonder Robinhood more than doubled annual users to a peak of 22.5 million by the end of 2021. It also didn’t hurt that Robinhood gamified investing with silly on-screen rewards designed to stimulate more investment activity. That clearly attracted new customers and increased the number of trades, which is the life’s blood for a company that makes its money from selling its order flow to market makers.

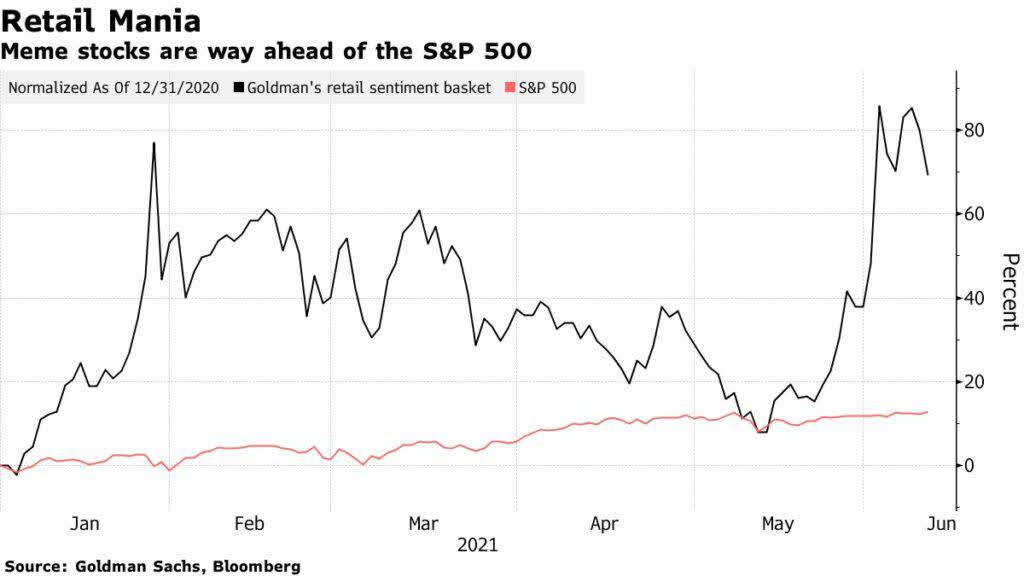

Completing the perfect storm for an investment boom on the Robinhood platform was the soaring popularity of WallStreetBets (WSB), which is an online community (subreddit) on the Reddit website that focuses on high-risk trading ideas with what are predominately option contracts. Traders crowdsourced their ideas on WSB, and then used their Robinhood brokerage accounts to pile into the same names in cult like fashion, giving birth to the meme stock craze of 2021. The most famous “meme” stock of them all was GameStop, which saw its stock price skyrocket from $1 to $86 in a complete dislocation from reality, but fundamentals don’t matter when enough traders who align in one direction become the entire market for a stock.

Bloomberg

The emergence of WSB and the meme stock craze was about more than just speculation. It was the most recent chapter of the rebellion against Wall Street, which dates to the Occupy Wall Street movement that started after the Great Financial Crisis in 2011, fueled by the public’s increasing mistrust of big financial companies and disgust of corporate greed. Those retail investors banned together to drive up the prices of stocks that Wall Street professionals were betting against, with the sole purpose of destroying them. It is no coincidence that the first commission-free brokerage firm catering to the underserved is called Robinhood, as in steal from the rich and give to the poor, or better yet, ignore the rich and focus on the poorer. My question is whether that is still the company’s focus.

Subscribers to Wall Street Bets were big fans of Robinhood’s commission-free option trading, and after the broker’s official debut in early 2015 the subs on WSB grew from less than 10,000 to 100,000 in the year that followed. The count was up to nearly 450,000 by the end of 2018 and nearly 800,000 by the end of 2019. Then came the pandemic and WSB subscribers grew to 10 million. You can see it in the annualized Robinhood user numbers at that time, which have now returned to 2019 levels. What happened?

Robinhood couldn’t protect newbie investors from their biggest enemy—themselves. The company executed trades and got paid for selling order flow, but they did not provide much beyond that. This means that when a $4,000 account is holding significant losses, as typically occurs in a bear market, it goes dormant. There was nothing beyond the basic service of executing orders to keep these investors engaged or assist them in improving their investment skills.

I think that if Robinhood wants to grow on a sustainable basis, especially during the next bear market, it will need to refocus on this younger demographic with something more than speculative trading tools. Trading is not easy for professionals, much less an inexperienced investor, and most will eventually get wiped out by a bear market or their own devices. The company’s focus should be on helping traders become astute investors, which I think would be a more successful long-term business plan.

They are broadening their scope by offering additional products and services, which include crypto-trading, debit cards, and retirement accounts. The most promising product has been their subscription membership program called Gold, which costs $5 per month. Gold members earn 5% on cash balances, pay a reduced margin rate of 8%, and have access to Morningstar research. Members also earn a 1% bonus on retirement account transfers, which goes up to 3% for annual contributions. That sounds great until you learn that it takes five years to vest in the bonus. Still, these are not services that a newbie investor with $4,000 to invest can capitalize on. Instead, Robinhood is targeting larger and more sophisticated investors at Fidelity, Schwab, and Interactive Brokers, but I don’t think the product and services menu is strong enough to compete. Meanwhile, I suspect millions of their small accounts lie dormant and ignored, which seems to be turning their back on the very investors who helped build the company — the underserved and relatively inexperienced micro investor. Robinhood himself wouldn’t be pleased. This is where the competition is nipping at its heels, which could be problematic if its efforts to win larger accounts fail.

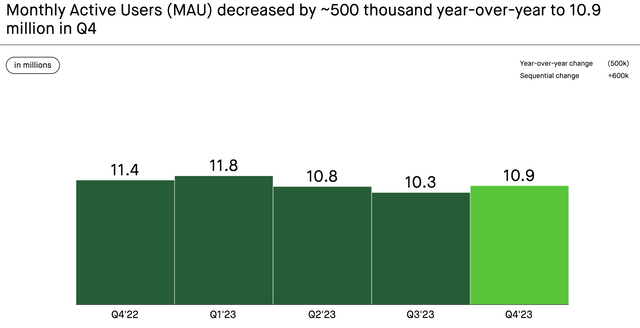

There are new Robinhoods emerging in hopes of capturing the millions of young investors who still don’t trust Wall Street and have a general disdain for traditional money management products and services. As we learned from WSB, members of this cohort find each other to be their most valuable and trusted resource when it comes to investment decisions. I suspect they are targeting Robinhood accounts that no longer remain active, which is a number difficult to determine, but the monthly active user count has been waning over the past year in what was a bull market. What will happen during the next bear?

Robinhood.com

Acorns is an emerging fintech that is targeting the micro investor with a similar line-up of products and services as Robinhood, but its focus is on saving and investing rather than speculating. For those committed to a mobile app, the firm offers a series of ETF portfolios that it recommends to users based on their investment profile. They then have the freedom to move between those portfolios at no cost if they choose to be more aggressive or conservative. More recently, Acorns introduced the ability to add individual stocks and ETFs to the firm’s diversified ETF portfolios, which allows for more customization, but it is a far cry from the freedom and excitement offered by Robinhood. Acorns has more than six million users and approximately $7 billion in assets, with an average account size of around $1,000.

Webull is a commission-free competitor of Robinhood’s launched in 2017 that offers a user-friendly mobile app with advanced trading tools. That has made it popular with both newbie investors as well as the more experienced. It has had major success as a competitor, as estimates are that the company has more than 13 million users, but it is difficult to know how many of those users are active. Based on public comments from the CEO, the average account size approximates $4,000, which is what we see at Robinhood.

The third competitor is called dub, which is the most interesting for three reasons. The first is that one of its seed investors is Nathan Rodland, who is co-founder of Robinhood. The second is that this is the only company trying to leverage the social media phenomenon focused on investing that emerged through WallStreetBets and made Robinhood a household name during the pandemic. Lastly, its founder and CEO at 23 years of age is a member of the newest generation of investors (Gen Z), which most of the emerging fintech companies want to target. Who better than Steven Wang knows what they want in a mobile financial services app.

Dub is the first and only broker to promote a copy-trading platform approved by FINRA and registered with the SEC. It allows retail investors to open a brokerage account on its mobile app and automatically copy a portfolio and the subsequent trades in that portfolio on an ongoing basis with nothing more than a tap of the screen. Some of these portfolios are created by seasoned investors with professional backgrounds who are implementing sophisticated hedge fund strategies, while others are popular financial influencers on social media who have created and actively manage portfolios of their own. Any of these can be copied by a retail investor who wants to have their money actively managed alongside that of the portfolio creator they choose. There is also full transparency, as they can see the historical performance of the portfolio and the real-time trading activity that occurs automatically in their account. It brings back some of the excitement from the meme-stock craze without the outsized levels of risk. It turns speculators into investors.

This is revolutionary for a very important reason. Whereas WSB on Reddit emerged as a site where investors could crowdsource information about investing in stocks, dub is an app where investors can now crowdsource information about investing in people. Furthermore, dub intends to serve as an incubator for undiscovered investment talent, as retail investors can create their own portfolios, build a track record, and amass a following of their own. Dub’s only source of revenue today is payment for order flow, which is how Robinhood started. I was impressed with the recent interview of CEO Steven Wang on CNBC last week, who discusses this next chapter in the evolution of retail investing.

CNBC.com

This new fintech is likely the greatest threat to the low hanging fruit among Robinhood's inactive user base.

Robinhood is looking higher up the investor food chain at larger accounts held by the likes of Schwab and Fidelity with new products and services that cater to wealthier investors. The jury is out whether that will be successful or not. Meanwhile, the likes of Acorn, Webull, and dub are nipping at Robinhood’s heels from down below where I suspect millions of accounts holders with balances well below the $4,000 average lie dormant. This is where a company like dub has the most potential in offering alternatives to those who want to revitalize their accounts with a new approach to investing that brings back the kind of excitement they likely once felt when the activity levels in their accounts were much higher. Robinhood should be refocusing on the needs of these investors before the competition takes over.