Mario Tama

Mario Tama

Herbalife's (NYSE:HLF) low valuation (P/E 4.27, P/FCF 3.8) is undeniably attractive, especially considering its historical multiples. However, stagnant revenue, shrinking margins, and eroded consumer trust paint a worrying picture. While management's recent efforts offer a glimmer of hope, debt reduction prioritization over share buybacks raises concerns about short-term upside. Moreover, Herbalife presents an intriguing value play, but significant risks remain for long-term investors. Ultimately, I think for now, the company is a ‘Hold.’

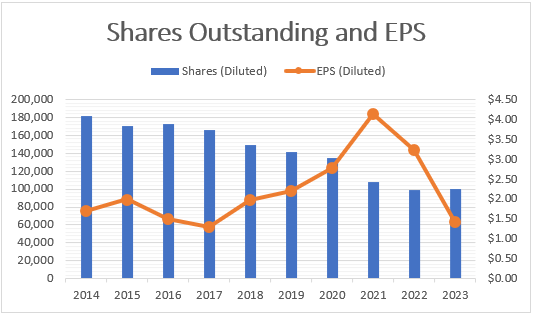

Herbalife trades at a FWD P/E of 4.27, a TTM P/E of 5.94, and a TTM P/FCF of 3.8. These multiples are considerably low compared to their historical. For instance, before 2022, the firm traded inside a range between a P/E of 8 and a P/E of 22 (excluding the high multiples experienced during 2018), according to data from MacroTrends. Most of the time, Herbalife traded at a P/E of around 13; this low P/E, alongside debt issues and strong FCF generation, allowed Herbalife to become a cannibal as its outstanding shares (diluted) decreased from 181,600 thousand in 2014 to 100,200 in 2023.

Author's Elaboration with data from QuickFS

Nonetheless, even if it has repurchased almost half of its outstanding shares, its EPS hasn’t increased significantly if the pandemic boom is excluded. The EPS reached a six-year low, while the stock price is at a multiple-year low (we must go to 2009 to see similar prices).

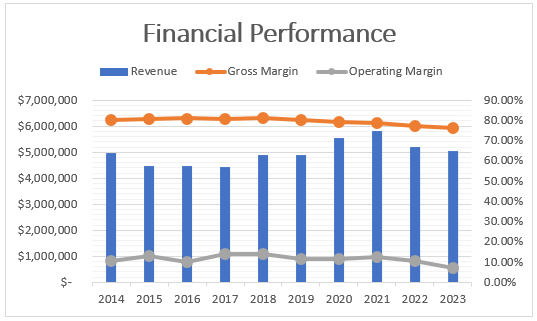

Falling revenues and margin contractions due to macroeconomic headwinds have caused recent stock performance problems. However, revenue problems are not new; Herbalife has experienced a decade of stagnation in revenue. Furthermore, margins have continued to shrink since 2018. Lately, the company has been experiencing margin reductions due to inflation and operating deleverage (as volume decreases and fixed costs are spread over fewer products), partly offset by price increases.

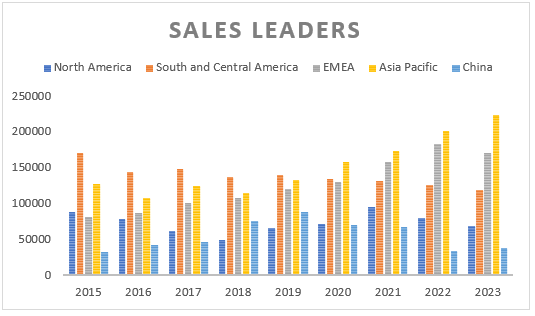

Author's Elaboration with data from QuickFS MarketScreener

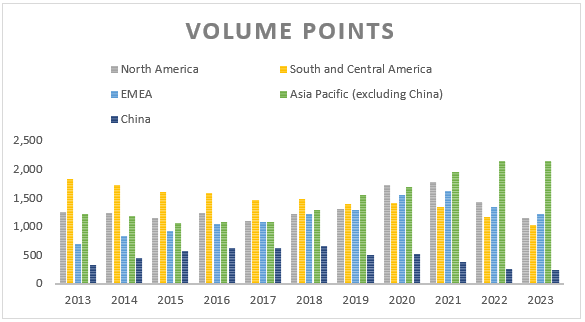

Lower revenues come from lower volume and fewer Sales Leaders and distributors. The only exceptions to the negative trends in the number of Sales Leaders and volume are the EMEA and Asia Pacific (excluding China) regions, which have grown in previous years. However, EMEA Sales Leaders are selling less than what they sold in 2021, which caused a decrease in Sales leaders the last year, I think.

10K Reports 10K Reports

Meanwhile, the North America region seemed to experience a revival during the pandemic; however, in 2023, the volume points and Sales Leaders returned to pre-pandemic numbers, so the boom is over in this region. The rest of America has a persistent downward trend, losing relevance in Herbalife’s revenue.

As I said in my Nu Skin article, MLM companies have significant competitive disadvantages. In the case of Herbalife, the reviews are negative; most customers complain about medical problems after consuming the products, the price, and the lack of effectiveness. The former, alongside legal proceeding involvement with the FTC, the SEC, and the DOJ, have erased consumers' trust in Herbalife products. This situation makes it harder for a turnaround, as even if the company changes, customers will shift their beliefs slowly.

In the last earnings call, management stated that they will strategically focus on North America, China, and Mexico to increase revenue by engaging with distributors, recruiting new distributors, improving conversion rates in the US, and developing new products. Overall, the management objective is to increase sales and reduce costs, allowing the margins to expand.

They already made some progress toward these objectives; first, the company reported a positive YoY revenue growth in 4Q23; second, it decreased SG&A by $115 million, whose effects will take place in 2024; third, 17 new products were released. Nevertheless, the guidance for 2024 isn’t so positive, as the management doesn’t expect a rise in volume, so the company won’t increase its operating leverage, so the gross margin will likely remain flat. However, as the company continues to invest in new technologies, the management expects lower operating margins, which aligns with what analysts expect.

Moreover, as interest rates have risen and a portion of the debt becomes due, management expects to reduce its debt until it reaches a leverage ratio of 3 (currently at 3.9); management was clear in stating that financial deleveraging is a priority over stock buybacks in the last earnings call. Therefore, outstanding shares will likely remain flat until the company reaches the desired leverage ratio. I believe achieving the desired value will take more than one year, as only a portion of the EBITDA turns into free cash flow that can be used to repay debt. For instance, according to my calculations, the 10-year average FCF conversion ratio is 55.4%, using EBITDA and not Adjusted EBITDA (the measure used by the management to calculate the leverage ratio). Thus, it’s plausible that the company will take at least two years to attain its goal if it uses all FCF to pay down debt and doesn’t use any of its cash reserves.

I understand the advantages of attaining an investment grade (or at least a better credit rating than a B+), as it increases the number of lenders and decreases interest rates. However, it comes when the stock trades at extremely low valuations, which would maximize the return on share buybacks. Consequently, I don’t think Herbalife will probably take advantage of the low valuations to buy back many shares, as refinancing debt at current interest rates could significantly increase interest expenses, undermining profits and increasing default risk.

Nonetheless, I think that without share repurchases, the company offers little upside potential as it keeps investing in its MLM model to achieve incremental improvement. Still, it’s the same model that Herbalife has had in the last ten years, showing no positive results as revenue growth was flat, margins shrank, and customers’ trust was erased. I doubt the company will turn around the downward tendency while keeping the same business model. However, at such low valuations, I don’t think the company can go down further, as it keeps being profitable despite macroeconomic headwinds, and most importantly, it has a strong cash generation together with enough cash reserve to meet financial obligations. Furthermore, it seems the worst is behind, as analysts expect higher EPS and revenue to stop falling.

Finally, over the long term, I don’t believe Herbalife is worth something today; however, in the short term, the low valuation offers an appealing opportunity, but without buybacks, I don’t think the upside potential is worth it.

Herbalife's current situation is a complex dance between attractive valuation and concerning fundamentals. While the low P/E and P/FCF multiples might entice value investors, the company faces headwinds from stagnant revenue, shrinking margins, and eroded consumer trust. Management's efforts to revitalize growth offer some hope, but their prioritization of debt reduction over share buybacks limits short-term appeal. Ultimately, I don’t think the company will be neither a winner or loser in the short-term, so I think for now, the company is a ‘Hold.’