Wong Yu Liang/Moment via Getty Images

Wong Yu Liang/Moment via Getty Images![]()

Written by Nick Ackerman, co-produced by Stanford Chemist.

The last time we touched on the Western Asset High Income Fund II (NYSE:HIX), I noted that the fund looked to be unappealing due to valuation. I highlighted a couple of potential opportunities that seemed a bit more attractive. That included funds from the same investment sponsor family, Western Asset High Yield Defined Opportunity Fund (HYI) and Western Asset Diversified Income Fund (WDI). Either of those alternatives would have been significantly better, thanks to HIX having a rights offering.

HIX's investment objective is "high current income with capital appreciation as a secondary objective." The fund will attempt to achieve this by offering "a leveraged portfolio of high-yield corporate debt securities from both the U.S. and non-U.S. corporations, with strategic allocations to emerging markets and derivatives."

The managers at HIX themselves fixed that issue by pulling a rights offering. Rights offerings often put immediate price pressure on the funds and become dilutive to NAV. That isn't always the case, as there are a couple of exceptions where funds have been able to have a rights offering become accretive due to selling shares at a premium.

In this case, though, since the fund slipped to a discount shortly after announcing the rights offerings, it will be dilutive to the NAV. Fortunately for investors, there is a floor in this offering at now lower than a 10% discount to NAV. That means dilution can be kept to a maximum, and the deeper the discount the fund trades at, the less that should participate. This rights offering also wraps up with an expiration set for February 26, 2024.

The Subscription Price will be determined based upon a formula equal to 92.5% of the average of the last reported sales price per share of the Fund’s common stock on the NYSE on the Expiration Date (as defined below) and each of the four preceding trading days (the “Formula Price”). If, however, the Formula Price is less than 90% of the net asset value per share of common stock at the close of trading on the NYSE on the Expiration Date, then the Subscription Price will be 90% of the Fund’s net asset value per share of common stock at the close of trading on the NYSE on that day. The estimated Subscription Price has not yet been determined.

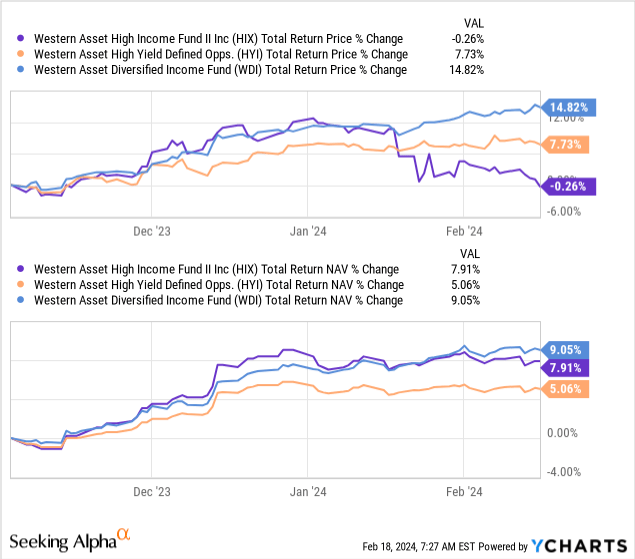

This announcement ultimately then resulted in both HYI and especially WDI performing significantly better on a total share price return basis since our prior update. I do believe this would have ultimately played out either way, at least for WDI relative to HIX, but the rights offering sped the process up quickly. HYI was even able to outperform despite HYI's underlying portfolio not performing as strongly. That's represented by the total NAV results seen below, which weren't as strong as HIX's in this relatively short period.

Ycharts

One of the appeals of HYI is that it is a term fund that is set to liquidate later next year in 2025, barring any sort of announcement for a vote to go perpetual. That means that HYI's discount should naturally decline as its share price moves towards its NAV. Whether that ultimately ends up in the share price moving higher or the NAV moving lower is yet to be determined.

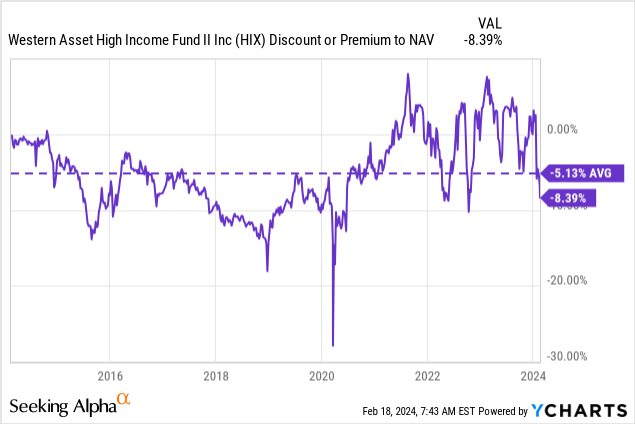

Given the HIX's current discount, it's looking much more appealing now than it was previously. However, historically, we've seen that the share price pressure from a rights offering doesn't let up until the expiration of the offering. In most cases, waiting until the rights offering dust settles after the expiration has tended to be the best time to pick up a fund.

Therefore, despite the fund having a deep discount on an absolute and relative basis, one may want to wait a couple more weeks before jumping in. Admittedly, the 1-year z-score coming in at -2.74 is certainly tempting, though.

Ycharts

On a bit of a side note, this was also a transferable rights offering. We've often observed that investors who wish not to participate in a rights offering but receive the rights should sell them as soon as possible. In this case, it is quite late in the offering already.

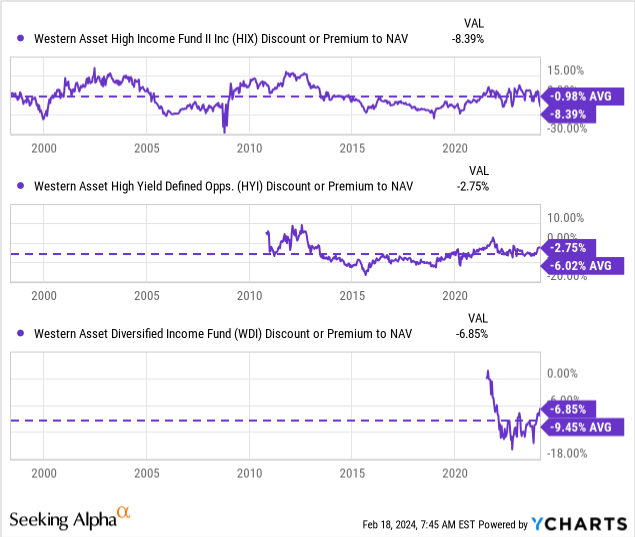

Looking back since inception, HIX's discount is even deeper relative to that average. Times can change, and this fund goes back a couple of decades, so make of that what you will. At this point, HIX is certainly more appealing on a relative basis compared to HYI and WDI.

Ycharts

That said, we already noted the term structure of HYI and WDI, which is also a term structured fund. That feature of WDI is less of a concern at this time as the fund's potential term date isn't until 2033.

With that being said, it still does look like HIX is the best value at this time. I'd still personally wait before adding because of the expected dilution of the NAV, which can put a bit more pressure on the share price until the expiration. I currently hold WDI with no plans to sell, but it certainly isn't the bargain price it once was

HIX is going through a rights offering, and that made the swap potential we highlighted last time into its sister funds, HYI or WDI, play out extremely well. It played out much better than I would have anticipated, thanks to the management team correcting their own overvaluation problem.

Going forward, HIX does look like the best candidate in terms of valuation at this time. However, we've tended to see share price pressure on funds until the expiration date of the offering. At that point, it could be worth revisiting for either a tactical play or if one is looking to invest in a high-yield fund.

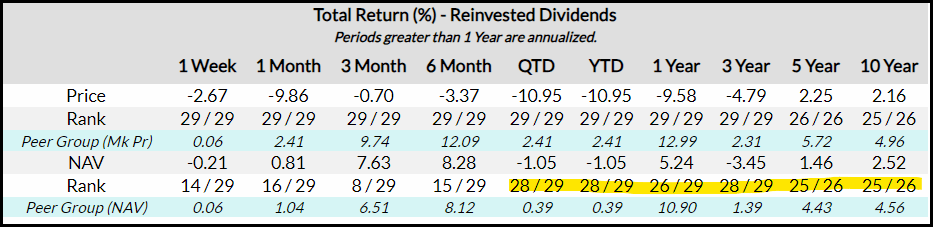

Further, I'd want to reiterate a point we highlighted last time. HIX actually doesn't have a great historical track record. According to CEFData, HIX has been almost the worst ranked in terms of total NAV return results of its category. Given that the rights offering has now put pressure on the fund's share price, the fund is ranked 29/29 in several of these periods as well.

HIX Performance Rank Vs. Peers (CEFData)

More recent results seem promising on a 3- and 6-month basis and past results don't guarantee future results, but they are at least worth noting.

Another small point worth noting is that the leaders of the "high yield bond" category that CEFData assigned are Barings Corporate Investors (MCI) and Barings Participation Investors (MPV). Investors familiar with these funds will know that these are largely invested in floating-rate bank loan exposure and are really in a league of their own. I've previously noted this in more depth. HIX owns some floating rate exposure, but it is primarily invested in fixed-rate corporate bonds. Still, whether HIX is ranked 25 out of 26 funds or 23 out of 24 in terms of their performance, it isn't a good look.

Editor's Note: This article covers one or more microcap stocks. Please be aware of the risks associated with these stocks.