coldsnowstorm

coldsnowstorm

Hibbett, Inc. (NASDAQ:HIBB) maintains a dense network of stores in underserved communities in the U.S. and has a close working relationship with Nike, Inc. (NKE) which provides the company to access with highly desirable apparel and footwear products. This story hasn't changed since I last wrote about the company, but the market's perspective of the business has shifted. In August 2023, HIBB was trading around 6x FY2024 EPS, and the stock was priced for an imminent collapse in earnings. The market's view seemed to be that Hibbett would not have the ability to navigate the very difficult retail environment with an overstuffed inventory channel and waning demand.

The stock now trades at around 10x FY2025 EPS after earnings did not collapse and Nike reiterated that it views Hibbett as an important business partner. The main concerns now center around when or if same store sales will grow again (specifically brick and mortar comps), and the sustainability of Hibbett's gross margins, while the terminal value issue relating to Nike's ambitions to control all of its distribution remains in the back of investors' minds. It's difficult to pinpoint when comps will turn, but given the huge supply/demand shocks stemming from the pandemic, the past two years of negative comps is a bit more forgivable. Management guided for brick and mortar comps to be flat to down low single digits and investors will be watching this closely while hoping for positive comps once again in FY2026.

The gross margin concerns are backed by commentary from JD Sports Plc (OTCPK:JDSPY), Foot Locker, Inc. (FL), and Nike. All of these businesses spoke on the unexpectedly promotional environment towards the end of the year, citing lack of product innovation, consumers that are too accustomed to previously promotional pricing, and a weaker consumer that is still being hurt by inflation. Hibbett is guiding for gross margins to improve as the year goes on.

In the face of negative comps and falling margins, HIBB may struggle to attract investors over the course of the next year. However I still believe a bet on HIBB comes with very attractive long-term upside as the company believes there is room to double its store count and as the company continues to repurchase shares at a rapid rate. The caveat is that this must occur with growth in same store sales and expanding gross margins.

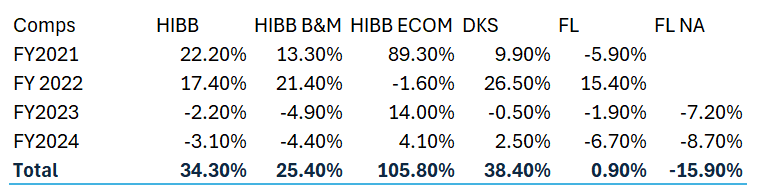

While Hibbett's sales grew in FY2024, comps declined by 3.1%. Specifically, brick and mortar comps declined 4.4% while ecommerce comps rose 4.1%. Gross margin for the year declined by 1.4% from 35.2% to 33.8%. SG&A expenses as a percentage of revenue rose from 22.8% to 23%. EPS for the year declined from $9.62 to $8.17.

HIBB FY2024 Results (HIBB Q4 Earnings Presentation)

These headline numbers show a clear decline from the previous year's results. This is made worse by the fact that last year's results were a decline from the previous year, and that next year's guidance doesn't indicate much improvement. However the pandemic related demand boom, supply shortage, and subsequent supply glut has created a retail environment of extremes. Put in the larger context of the past 4 years and in the context of the performance of other retailers, Hibbett's comps don't look quite as bad.

Retailer Comps (Created by Author)

It's fair to view these comps as either normalization or deterioration because the correct perspective isn't clear. But given how unprecedented the FY2021 and FY2022 comps were, I think it is reasonable to think that a normalization period would be longer than usual.

Hibbett's declining gross margin over the past few years is also a concern. Gross margin has declined from its peak of 38.2% in FY2022 to 33.8% in FY2024. This can be explained by the pandemic supply/demand dynamic but more recently it can be explained by promotional activity across the industry. JD Sports provided some commentary on this in their interim update in January:

In terms of the US, promotional activity was widespread across the entire market and different players participated. I believe Nike referred to this when they last update the market in December which is a contrast to their September statement…within apparel the lack of innovation, combined with the consumer being more price sensitive affected the category, especially now that many brands are tapping into the casualisation trend.

I can't confidently make the short-term bet that these trends will improve or deteriorate over the course of the year but based on evidence from other retailers, I think there is a good chance these concerns end up being temporary concerns.

A longer term view comes with concerns about Hibbett's partnership with Nike. I am personally confident that it will hold up primarily because of the replacement cost of Hibbett's store network, which I estimate to be between $1bb and $1.5bb. This is based on my estimate of Hibbett's maintenance capex, new stores openings, and Hibbett's total store count. This would equate to over a year's worth of capex for Nike and doesn't take into account Hibbett's local knowledge of these communities. If brick and mortar stores remain important for Nike going forward, which I think they will be, Nike will be forced to work with Hibbett. Despite Hibbett's small size when compared to Nike, I do think they have some bargaining power.

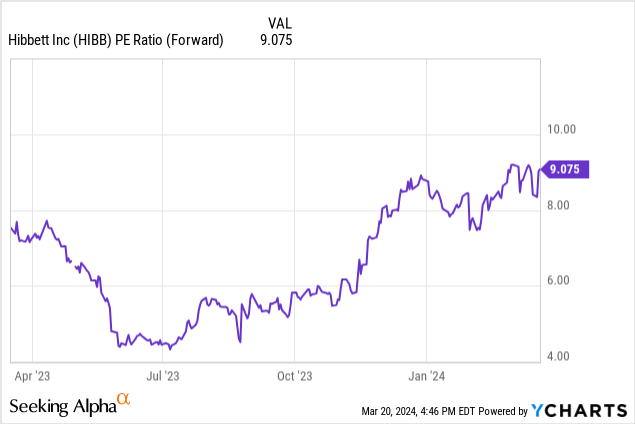

The valuation work for Hibbett is quite simple. The stock looks cheap optically, but the low multiple makes sense given recent comp and gross margin trends. If the company continues to open stores and those poor trends continue, returns on incrementally invested capital will be low or negative and the stock deserves a low multiple.

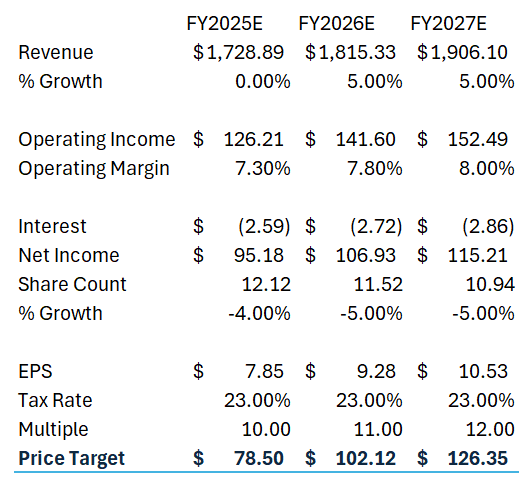

I think that potential upside if things go well outweighs the potential downside. If revenue increases 5% in FY2026 and FY2027 after a flat year in FY2025, and operating margins expand to 8% when operating leverage kicks in from back office and tech investments, I estimate FY2027 EPS may be around $10.50. If comps have turned around in this scenario and the Nike partnership remains solid, a 12x multiple would put the stock at around $125. This would provide a 20-30% IRR depending on an exit date.

HIBB Bull Case (Created by Author)

If comps don't return to growth and gross margin continues to decline as industry supply/demand dynamics remain poor, I see a credible case for a price target of around $60 over the next 2 years based on slower revenue growth, 7.5% operating margins, and a 6x multiple. Given the company's low debt and consistent profitability over time, I don't see much risk of permanent loss of capital.

HIBB Bear Case (Created by Author)