ArtistGNDphotography/E+ via Getty Images

ArtistGNDphotography/E+ via Getty Images

A little over a year ago, in late January of 2023, I found myself researching what kind of investment prospect John Bean Technologies (NYSE:JBT) would make. The company, which largely focused on food technology and providing solutions and services to the air transportation markets, was an interesting opportunity because of the spaces that the firm operates in. Even though I found myself interested from a conceptual perspective, and I concluded that the firm would probably make for a reasonable prospect for investors in the long run, I ultimately decided that it did not make sense to buy into at the time because shares were not yet cheap enough. This led me to rate the business a ‘hold’ to reflect my view that the stock would be unlikely to outperform the broader market for the foreseeable future.

Fast forward to the present day, and my prediction turned out pretty good. While the S&P 500 is up 29.7%, shares of John Bean Technologies have seen upside of only 6.6%. However, it has not just been business as usual for the firm. Management has undergone some significant changes. For starters, the company ultimately sold off its airline service operations, known as AeroTech, in exchange for $808.2 million. Management used some of those proceeds in order to pay down debt. And now, the business is in the process of trying to buy out another interesting firm known as Marel (OTCPK:MRRLF). Although I do recognize that times of significant change like this do offer up some of the best chances to capture attractive upside, I also believe that shares are still not cheap enough for investors to dive on in. So while it may be tempting to consider picking up some units, I am maintaining the ‘hold’ rating I assigned the stock in early 2023.

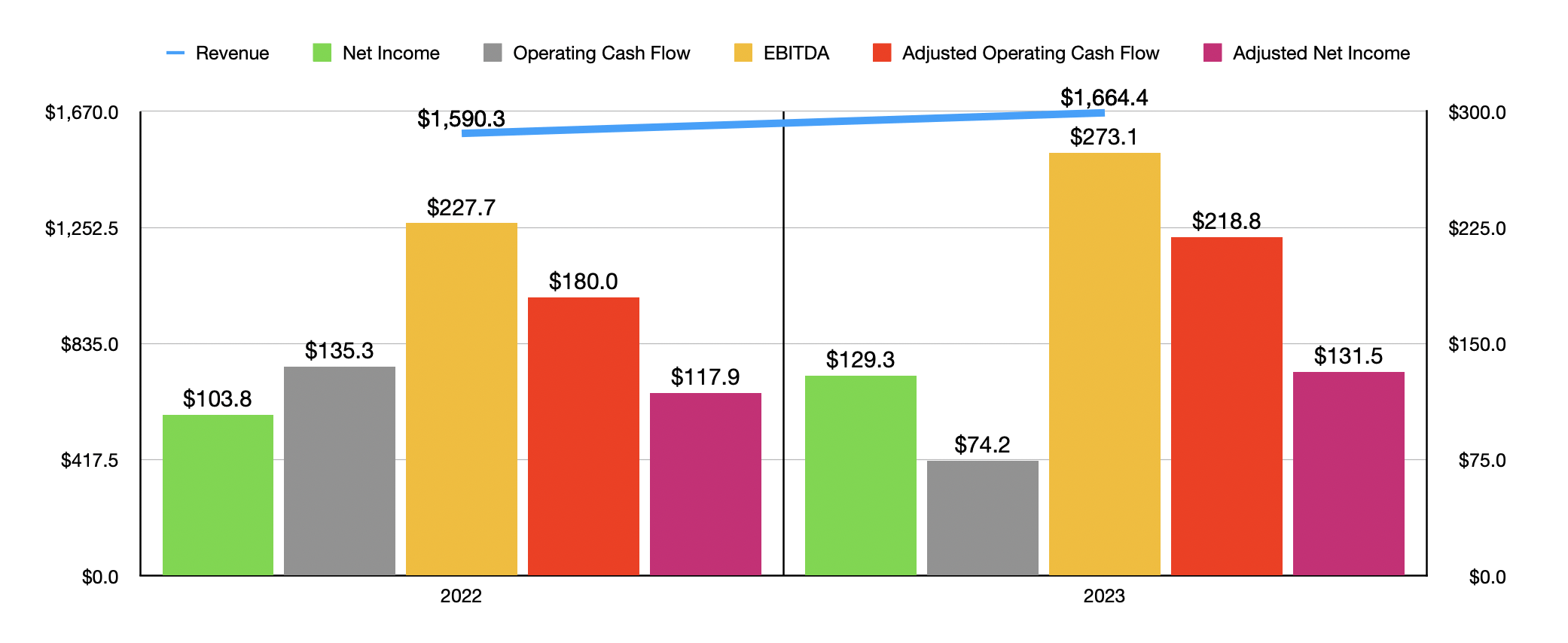

Fundamentally speaking, John Bean Technologies is far from a bad company. But it's also not a great one. For starters, we should touch on how the business performed during the 2023 fiscal year. During that time, revenue came in at $1.66 billion. That represents an increase of 4.7% compared to the $1.59 billion generated in 2022. Acquisitions accounted for most of this increase in sales, about $76.8 million in all. By comparison, organic revenue contributed only $4.7 million to the company's upside. Management attributed that increase to higher pricing and an increase in volume associated with its recurring revenue activities, even as volume for non-recurring activities decreased year over year.

Author - SEC EDGAR Data

With the rise in revenue also came higher profits. If we exclude everything associated with discontinued operations, net profits rose from $103.8 million to $129.3 million. This was in spite of higher restructuring costs, as well as a rise in interest expense. Management attributed much of the improvement to the higher revenue and to an increase in gross profit margin from 33.3% to 35.2%. That increase was driven mostly by higher pricing, combined with savings resulting from the company's restructuring activities. A higher mix of recurring revenue was also to thank for this improvement. Other profitability metrics largely followed suit. Adjusted profits went from $117.9 million to $131.5 million. It is true that operating cash flow fell by almost half, from $135.3 million to $74.2 million. But if we adjust for changes in working capital, we get an increase from $180 million to $218.8 million. And lastly, EBITDA for the business expanded from $227.7 million to $273.1 million.

All things considered, investors have a lot to be happy about. The firm has net debt of only $163.1 million, and management is forecasting additional growth this year. Revenue is expected to come in at between $1.75 billion and $1.78 billion. Adjusted earnings per share of between $5.05 and $5.45 will translate to adjusted profits of $168.5 million at the mid-point. And EBITDA for the company is expected to come in at between $295 million and $310 million. No guidance was given when it came to operating cash flow. But if we assume that it will increase at the same rate that EBITDA is expected to, then a reading of $242.4 million is not unrealistic.

Author - SEC EDGAR Data

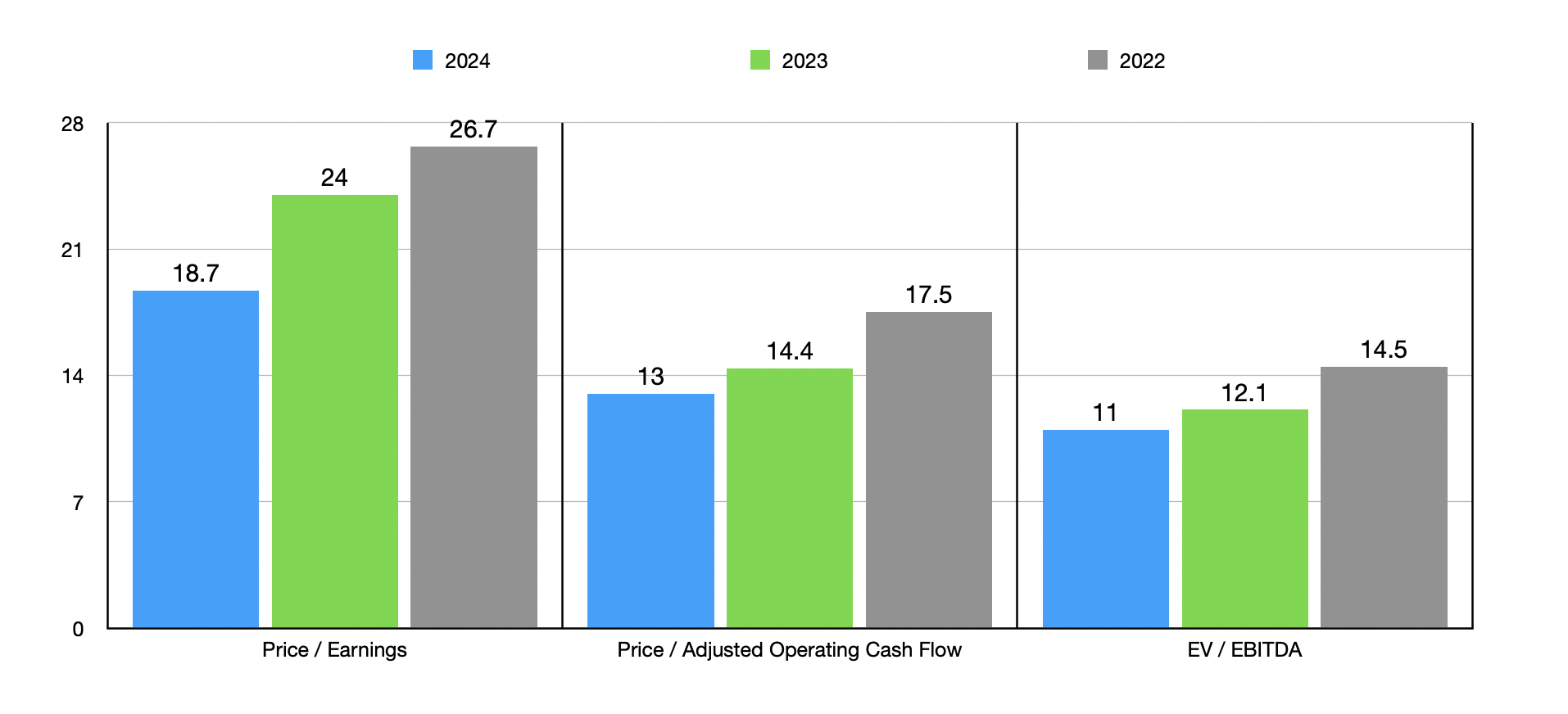

Using these results, I valued the company as shown in the chart above. I show data for 2022 and 2023, as well as estimates for 2024. In the grand scheme of things, shares don't look expensive. But they also don't look cheap. In the table below, I then compared the enterprise to five similar firms. What I found was that, when it comes to both the price to earnings approach and the EV to EBITDA approach, three of the five businesses end up looking cheaper than it. This number drops to two of the five when we look at the price to operating cash flow multiple. Although none of this is bad, it does make me feel as though this is just a decent play surrounded by similar firms. It doesn't strike me as an opportunity that should capture market beating returns.

| Company | Price / Earnings | Price / Operating Cash Flow | EV / EBITDA |

| John Bean Technologies | 24.0 | 14.4 | 12.1 |

| SPX Technologies (SPXC) | 171.3 | 91.5 | 27.9 |

| Hillenbrand (HI) | 6.1 | 17.5 | 11.8 |

| Albany International Corp (AIN) | 29.3 | 21.4 | 13.2 |

| Gates Industrial Corporation (GTES) | 17.1 | 8.3 | 8.9 |

| Mueller Industries (MLI) | 9.5 | 8.6 | 4.9 |

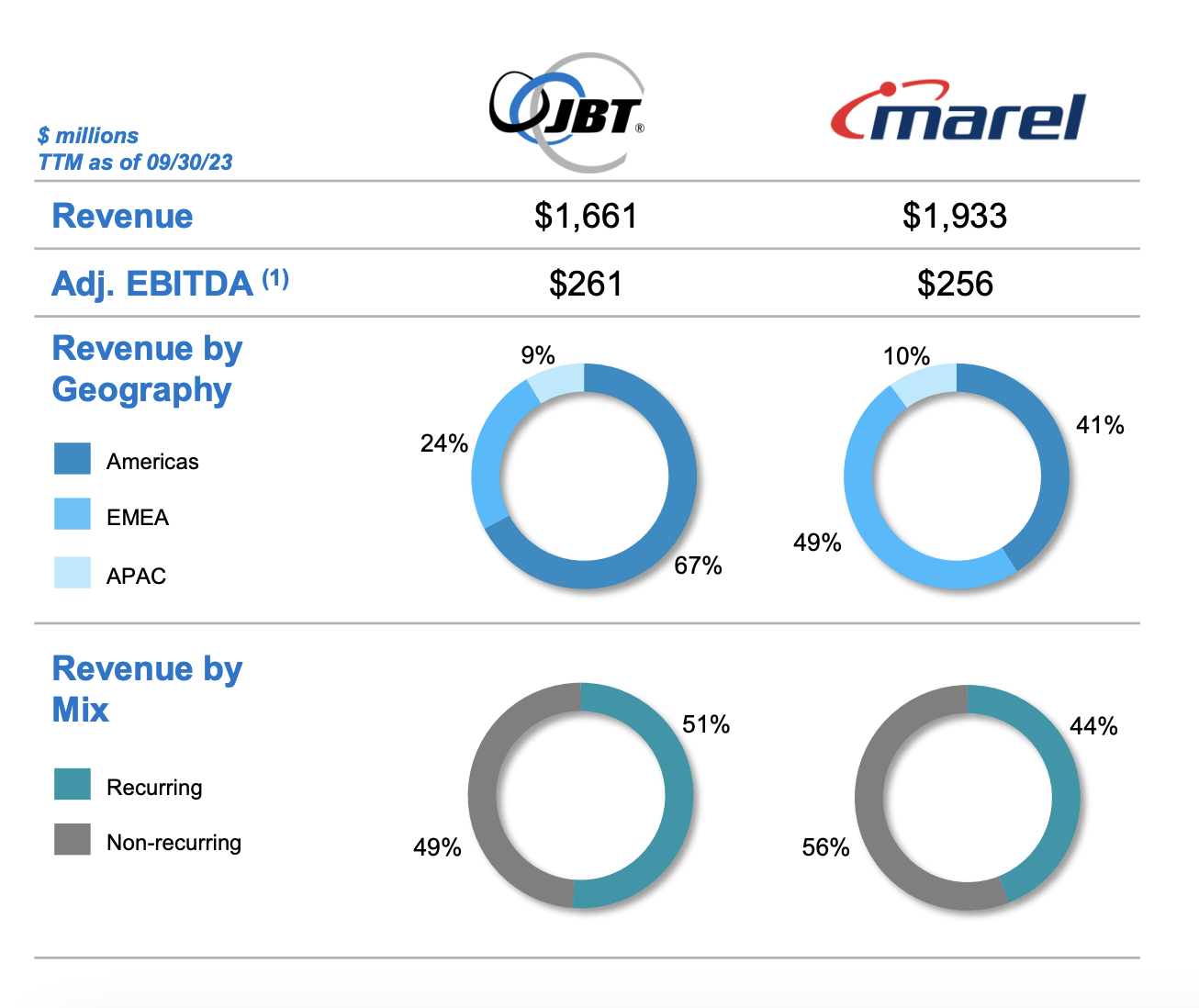

Back in late November of last year, the management team at John Bean Technologies announced that they had issued a non-binding proposal to acquire Marel. For those not familiar, Marel is a rather sizeable player in the food space that was established back in 1983. It operates today in over 30 different countries spread across six different continents. The company has four different operating segments. The first of these is the Poultry segment, which provides a range of poultry processing solutions for its customers. This includes automated inline solutions, software, and various services. Its Meat segment supplies customers with equipment and systems for the purpose of processing, cutting up, deboning, and providing other related services, for the red meat industry. The Fish segment includes equipment, software, and more, for processing whitefish and salmon, including those that are farmed or that are wild. And lastly, the Plant, Pet and Feed segment provides processing solutions centered around the pet food, plant-based proteins, and aqua feed markets.

Author - SEC EDGAR Data

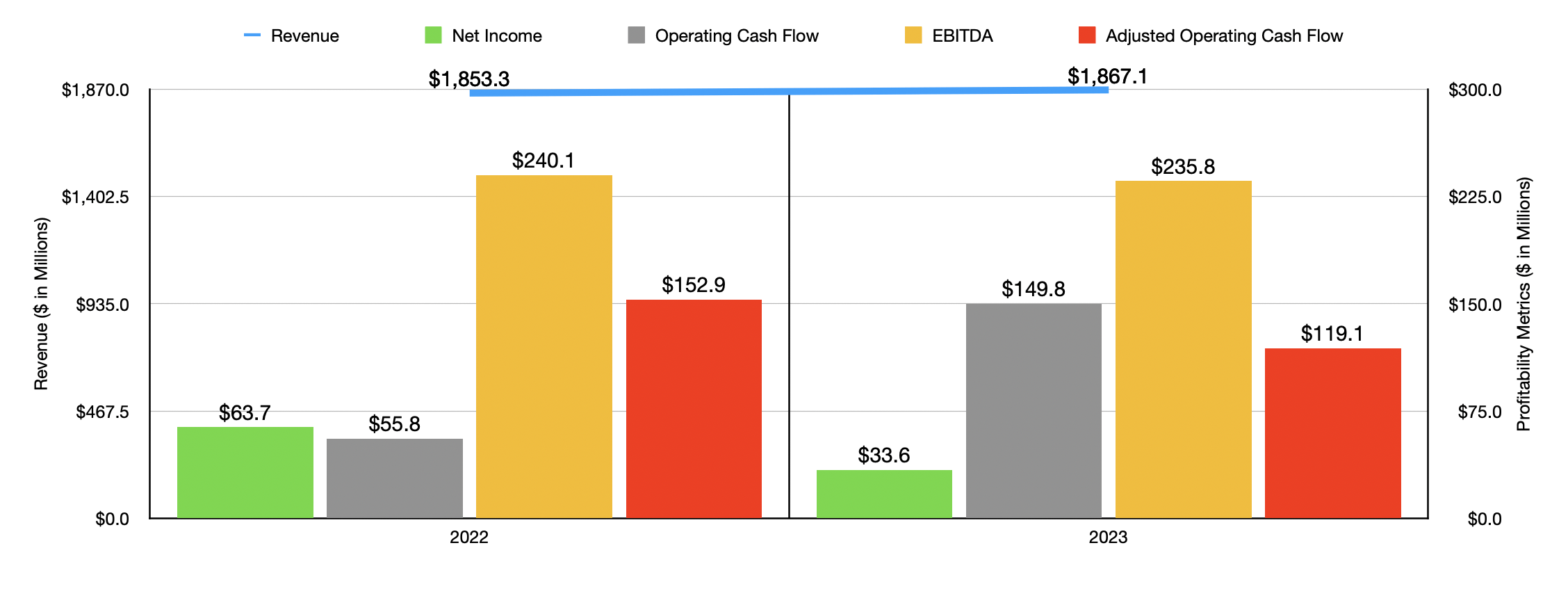

Actually speaking, the picture for Marel has also been a bit mixed as of late. Using constant currency for translating from euros to dollars utilizing current exchange rates, the company did manage to see revenue rise from $1.85 billion in 2022 to $1.87 billion last year. Sadly, net profits fell from $63.7 million to $33.6 million. This was offset by the fact that operating cash flow nearly tripled from $55.8 million to $149.8 million. But as the chart above illustrates, the adjusted figure for this and EBITDA, both showed a year over year decline.

John Bean Technologies

Recognizing an opportunity, the management team at John Bean Technologies decided to pursue a purchase of Marel in the hopes of creating what it describes as a ‘diversified and leading global food and beverage technology solutions company’. Management has offered up a price of €3.60 per share, implying a market value for the company of $2.93 billion. When you factor in existing net debt of $813.4 million, this implies an enterprise value of $3.74 billion. 65% of the deal is going to be in the form of common stock, with the remaining 35% in the form of cash. And upon completion of the transaction, if it is completed, shareholders of Marel will end up with a 38% interest in the combined enterprise.

If this transaction does come to fruition, management expects to generate some rather attractive synergies. The current estimate is to reach $125 million in annual run rate synergies within the first three years following the completion of the merger. That completion is currently targeted for the end of this year. But of course, it does require shareholder approval and the firms must meet other conditions as well. There are multiple reasons besides the cost savings to consider this an attractive opportunity.

John Bean Technologies

For instance, while 67% of the revenue generated by John Bean Technologies comes from the Americas, only 24% comes from the EMEA (Europe, Middle East, and Africa) regions. By comparison, 49% of the revenue generated by Marel comes from the EMEA while 41% is attributable to the Americas. Another benefit is that there is the potential for John Bean Technologies to capture attractive value by pushing more of the revenue generated by Marel to be recurring in nature. Only 44% of its sales are currently recurring, compared to 51% for John Bean Technologies. Their increased size and geographic diversity could allow additional cross selling to generate additional revenue opportunities. The list of benefits goes on.

Author - SEC EDGAR Data

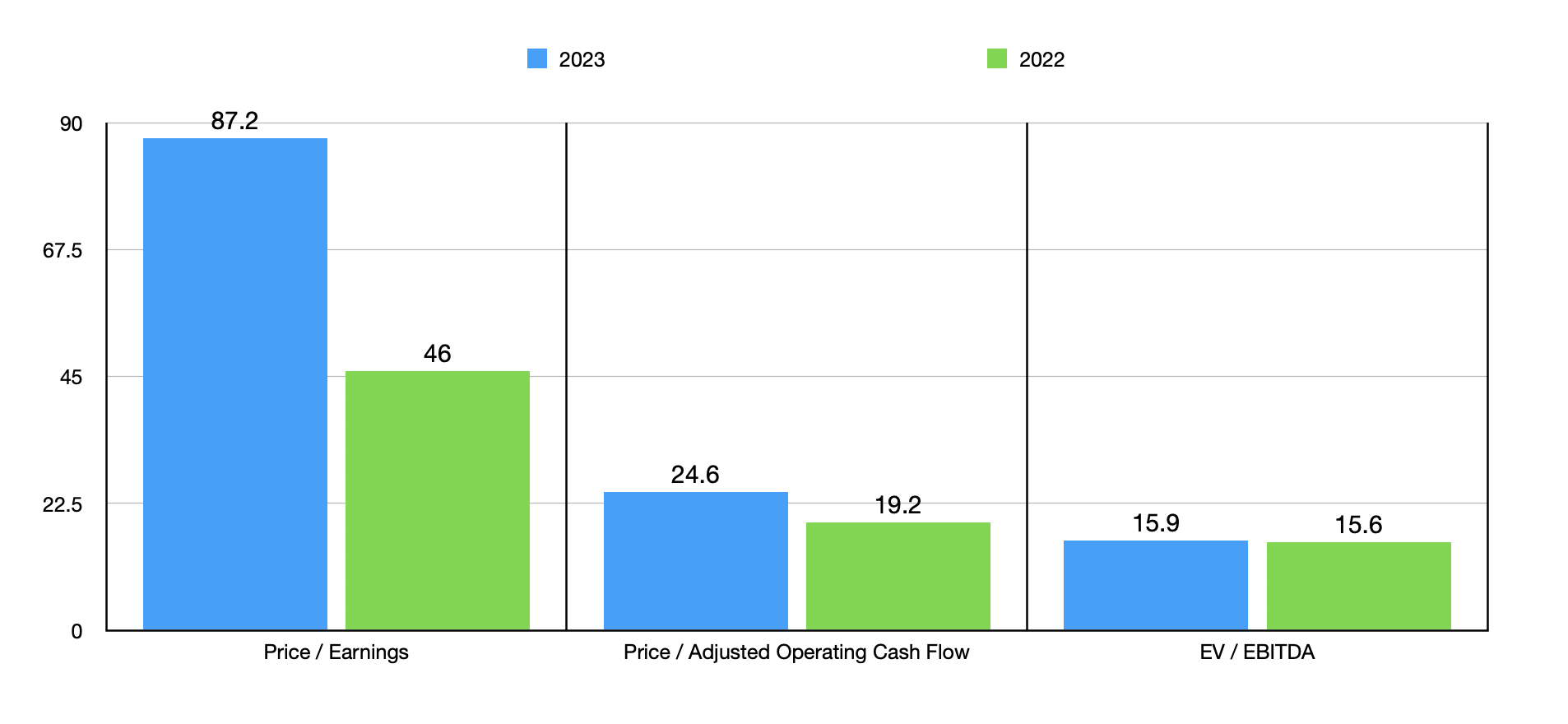

The only problem I have with this transaction is that, if synergies don't come out at full force, it appears as though John Bean Technologies is overpaying for Marel. Using the $3.74 billion of enterprise value that I calculated for the purchase and the 2023 EBITDA that Marel generated of $235.8 million, we end up with an EV to EBITDA multiple of 15.9. And if we use the adjusted operating cash flow generated in 2023, we end up with a price to adjusted operating cash flow multiple of 24.6. And this assumes that management does not need to take on any debt that would result in a material amount of interest having to be paid. It would be different if John Bean Technologies was using high-priced stock in order to pick up shares of Marel at a cheaper multiple. But the exact opposite is what is occurring.

Although I am interested in John Bean Technologies from a conceptual standpoint, the stock is only now getting close to the point of being worth considering from an investment perspective. But then when you add on to this the rather expensive Marel acquisition the company is pursuing, the stock looks mediocre at best. Of course, if new data comes out suggesting that the picture will be better, my mind could change. But for now, I believe that there are still better opportunities to be had in the market at this time.

Editor's Note: This article discusses one or more securities that do not trade on a major U.S. exchange. Please be aware of the risks associated with these stocks.