bluebay2014

bluebay2014

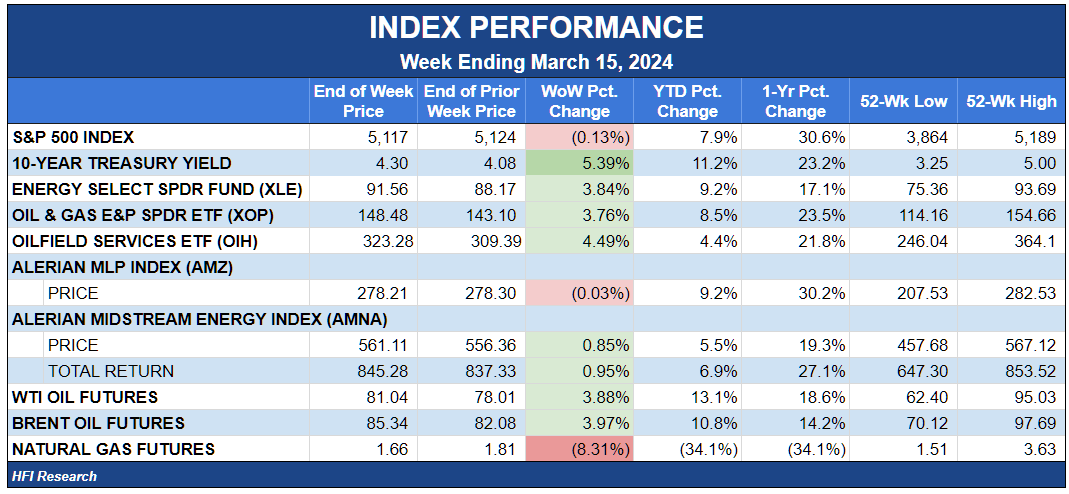

The energy sector is finally getting the respect it deserves. After oil prices and energy stocks failed to reflect the energy market’s supply and demand fundamentals, we’re finally seeing an improvement. After this week’s 3.9% increase, WTI prices (CL1:COM) of $81 per barrel now reflect the reality of today’s low inventory levels and generally tight physical market conditions.

The bullish oil backdrop favored oilfield services (OIH) and E&Ps (XOP), which gained 4.5% and 3.8%, respectively. The high-yielding midstream sub-sector fared worse, ending the week flat after Treasury yields leapt higher. The 10-year Treasury yield (US10Y) traded to 4.3% during the week, gaining 5.4% due to domestic economic strength, a lower likelihood for Federal Reserve interest rate cuts, and Federal deficit spending that is excessive—to put it mildly—in the absence of a recession.

HFI Research

Meanwhile, natural gas can’t get a break. Prices declined by another 6.3% this week, though gas-weighted equities continue to read through today’s conditions. Gas-weighted E&Ps have held up far stronger than would be expected with prices plumbing generational lows.

The cause for gas equities outperformance the commodity is that natural gas prices for delivery further out in time trade at elevated levels, so investors are comfortable assuming that today’s low prices will give way to higher prices in the future. If, however, their expectations prove to be wrong, due perhaps to another warm winter later this year, natural gas equities have a long way to fall.

We recommend being selective when choosing natural gas equity investments. Investors seeking exposure to gas should stick with the highest-quality names, such as Tourmaline Oil (TOU:CA), Spartan Delta (SDE:CA), and Peyto Exploration (PEY:CA).

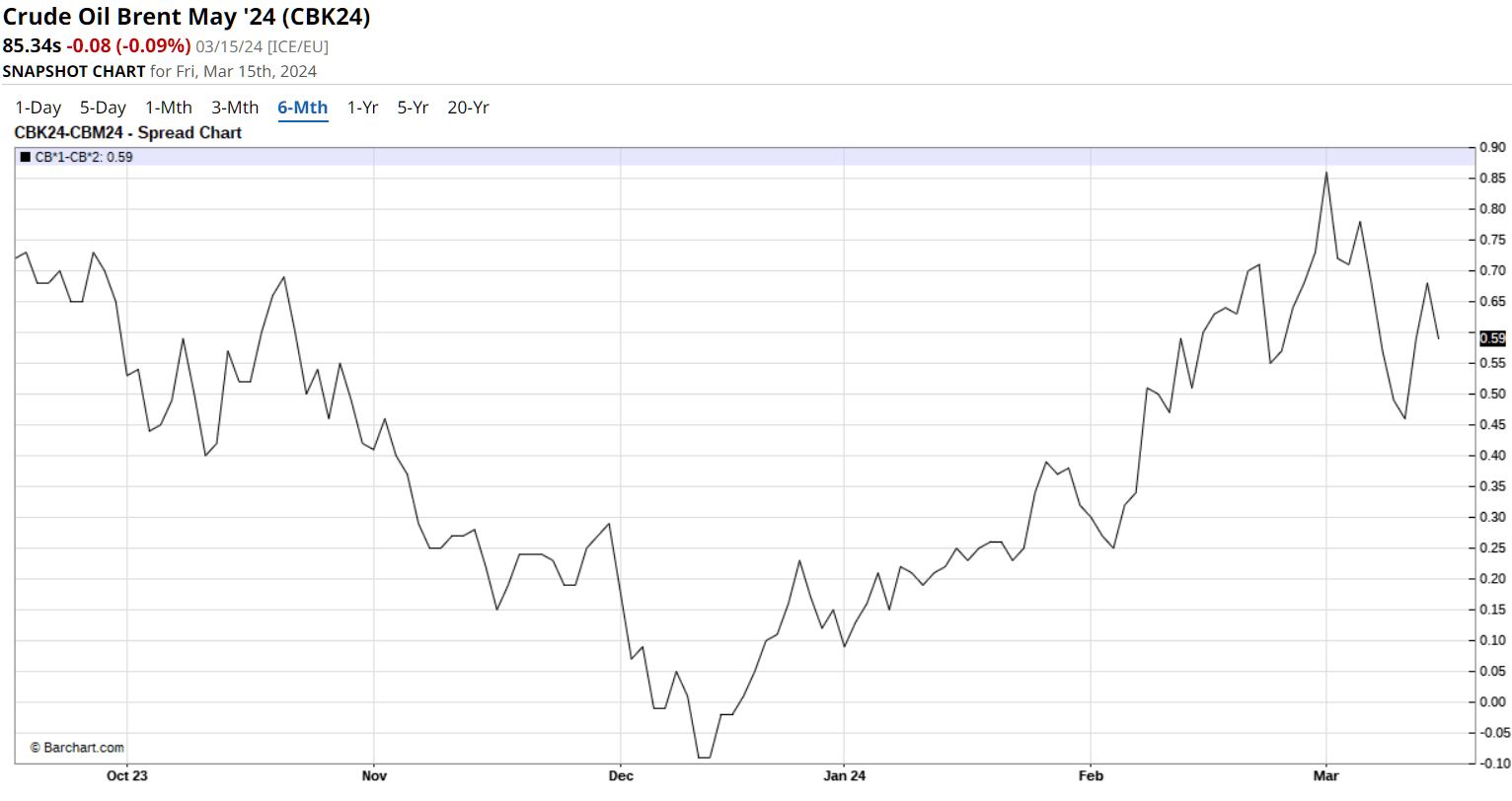

For oil, we expect the physical market to remain tight. As we’ve expected, U.S. production growth is coming in disappointingly low versus consensus expectations, Saudi Arabia and the U.A.E. extended their supply cuts through the end of the second quarter, global inventories remain significantly lower than last year, U.S. inventories indicate an ongoing supply deficit, refining margins remain strong, and Brent backwardation is holding up despite marginally weakening this week. Brent’s backwardation is shown below.

Barchart.com

The U.S. and global economies have remained stronger than expected by many economic commentators, as lower interest rates and massive fiscal stimulus create Goldilocks conditions for the economy and stock market. Fears of a recession are now ebbing, which is translating into better-than-expected corporate earnings and higher stock prices.

All these macro factors bode well for the energy sector. We expect the bullishness to continue over the coming months. Energy Aspects now forecasts 2.3 million barrels per day of oil inventory draws in the third quarter. This would market the largest quarterly draw rate since the third quarter of 2023, when oil prices shot up well past $90 per barrel.

This year will feature the added benefit of inventories entering the summer at lower levels than last year, though this bullish factor is offset by large OPEC spare production capacity, which is likely to be phased in beginning in the third quarter. We don't expect OPEC to increase production so as to send oil prices below $80 per barrel.

Downside risk to a bullish second half stems more from a U.S. strategic petroleum reserve (SPR) release than fundamentals, though the administration will be limited in the volumes it can release. Furthermore, Saudi Arabia will be in control of the supply situation, and we'd expect the Kingdom to adjust its oil market policy to accommodate at least part of the additional SPR volumes.

But if Energy Aspects’ third-quarter supply deficit estimate is anywhere close to the mark, increasing physical market tightness should begin to make itself seen in the May-June timeframe. Of course, financial oil market pricing will play a role in either undershooting or overshooting the actual state of the physical market. But a tightening physical market will push crude prices higher over a several-month period, irrespective of the financial oil market's sentiment and pricing idiosyncrasies.

The combination of a strong economy, healthy corporate balance sheets, and a constructive commodity price outlook will work to the favor of oil-weighted E&Ps. These stocks are currently discounting high-$70 per barrel WTI. As such, they have mid to high-single-digit appreciation potential on average simply to reflect current commodity prices.

An energy equity investor’s next move at this point depends on his or her risk tolerance and investment objectives. The most risk-averse should stick to the large oil sands producers, such as Cenovus Energy (CVE).

Our estimate of CVE’s intrinsic value stands more than 50% above its current stock price of $18.58. Its shares continue to trade at a discount to CVE’s large-cap Canadian peers. Moreover, the last time oil prices were at current levels, CVE’s U.S. stock listing was sustained above $19 per share. Nothing has changed in the fundamental picture since last year, so a reversion back to that level or above strikes us as reasonable.

Momentum has firmly shifted in CVE’s favor. Its shares’ 5.2% gain this week made them the third-best performing equity in our coverage universe.

CVE’s fourth-quarter results and five-year plan—both of which were announced over the past month—were surprisingly well received by investors. In fact, CVE shares have rallied 14% since fourth quarter earnings were reported on February 15.

CVE’s price action underscores how overly negative investors had become due to management’s poor messaging, particularly after it badly screwed up in estimating the arrival of 100% free cash flow distributions to shareholders. As bad as the snafu was from a public relations perspective, it did nothing to change our appraisal of management’s operational or capital allocation skills, or CVE’s intrinsic value, for that matter.

We now expect the pivot to distributing 100% of free cash flow to occur in the second half of this year, which is likely to serve as a catalyst for a higher stock price. It is also likely to be a boon for income investors, as CVE will probably boost its dividend once it reaches the free cash flow pivot point.

We’d point out that the pivot to 100% free cash flow distribution was clearly a catalyst for Canadian Natural Resources (CNQ) stock, even though CNQ’s pivot came as no surprise. Moreover, the company was already paying out nearly 100% of its free cash flow to its shareholders. It paid out 94% of free cash flow to shareholders in 2023.

With sentiment toward CVE improving and macro fundamentals on an upswing, we believe the shares are the best pick for conservative investors looking to profit from higher oil prices.

Conservative accounts looking for long-term E&P equity investments should also take a look at Suncor Energy (SU). The company’s turnaround is proceeding faster than we’ve even seen in an E&P—and this for a company that sports a US$50 billion market cap. While our estimate of SU’s upside isn’t as large as that for CVE, we expect its shares to do well if its turnaround continues and the commodity backdrop is as bullish as we expect heading into the second half of the year.

Moving up the risk spectrum, the more volatile but fundamentally sound names such as Crescent Point Energy (CPG), Cardinal Energy (CJ:CA), Whitecap Energy (WCP:CA), International Petroleum (IPCO:CA), and Hemisphere Energy (HME:CA) are all attractive candidates for long-term investment. All are well managed, have attractive return of capital profiles, and high-quality assets. Please refer to our writeup of these names for details and valuations.

These stocks offer more upside than CVE and SU due to their cash flow torque to oil prices and inherent volatility. And in the worst-case scenario that our macro outlook for a strong oil market is wrong and/or shorter-term investors end up holding these names longer than expected, each of these E&Ps will be able to either maintain or grow their intrinsic value for shareholders with oil prices in the $70s per barrel. Prices below $70 per barrel for any considerable period would cause a supply reaction that we expect would send prices back into the $70s per barrel in short order.

Our portfolio gained 0.1%, essentially flat with its benchmark, the Alerian MLP Index.

We were asleep at the wheel in our tracking of Genesis Energy (GEL) this week. The units—which are always volatile—declined 6.3% on no news. We’re looking to invest our portfolio’s cash and would have done so if we saw GEL trade down to the mid-$10 range, as it did on Wednesday and Thursday. Assuming the units remain there over the coming trading days, we’ll buy more GEL units.

Like GEL, Calumet Specialty Products Partners (CLMT) also drifted lower, ending the week down 6.2%. The only news item was the company issuing $200 million of 9.25% Senior Secured First Lien Notes due 2029 in a private placement transaction. CLMT intends to use the proceeds to redeem all its outstanding 9.25% Senior Secured First Lien Notes due 2024, as well as $50 million of its 11% Senior Notes due 2025. The move is in keeping with management’s previous capital allocation guidance.

The U.S. economy is strong, which bodes well for CLMT’s industrial business. Its Montana Renewables business is presumably running near capacity, thereby paving the way for an IPO as investors get a taste of how much cash flow the unit can generate in a low-margin environment. All in all, there has been no change in CLMT’s macro or company-specific fundamentals to warrant this week’s price action.

The biggest news this week for our portfolio came in Equitrans Midstream (ETRN) shares. The company’s former E&P sponsor, EQT (EQT) reached an agreement to acquire ETRN in an all-stock deal valued at $12.50, which has been our price target for ETRN since we’ve held the name in our portfolio. EQT expects the deal to close in the fourth quarter. It is conditional on the ETRN completing construction of the Mountain Valley Pipeline (MVP).

We plan to hold onto our shares, primarily for tax reasons. We purchased our ETRN shares on July 11, 2023, so we’ll have to wait for July 12 this year to sell and realize a long-term gain. We’d much rather wait for a few months and get favorable tax treatment than sell now and trigger a short-term capital gain.

In the meantime, ETRN’s price moves will track those of EQT. We’re comfortable holding the pricing equivalent of EQT shares. We expect natural gas prices to recover as high-cost production is increasingly curtailed. A move by Henry Hub back above $2.00 per mcf is likely to push EQT shares higher, as the consensus outlook after this year is bullish for natural gas prices. The current natural gas market consensus is calling for a bullish 2025 due to the arrival of LNG facilities in the U.S., which will increase demand and sop up excess supply, at least in the near term.

We’ll decide what to do with our ETRN shares if EQT’s shares recover and our holding period crosses the one-year mark.

By acquiring ETRN, EQT will become a vertically integrated E&P, which we believe is favorable for a gas-weighted E&P like EQT. Natural gas netbacks tend to be slimmer than oil netbacks, making cost control key. We were never particularly fond of ETRN’s management, and its full accountability to a corporation would likely enhance its operations. The MVP is set to be completed in the second quarter. Its completion will bring a valuable asset—and enhanced egress flexibility—for EQT.

The deal was not well received in the market, which sold EQT’s stock down 8% on the day of the announcement. This was a silly reaction, and the EQT’s beatdown got us thinking about investing our cash holdings into EQT shares. What held us back was that EQT wouldn’t be our first (or second, or third) option for a natural gas-weighted E&P holding, even though we consider its long-term prospects to be bright. The company will benefit from its massive scale and ability to sign exclusive long-term natural gas supply deals with utilities and LNG export facilities. Both kinds of deals entail natural gas pricing at a premium to benchmarks.

That said, we’d rather own Tourmaline Oil (TOU:CA), Spartan Delta (SDE:CA), Peyto Exploration (PEY:CA), or even currently out-of-favor Birchcliff Energy (BIR:CA) over EQT.

March 5. Cheniere Energy (LNG) launched an offering of Senior Notes due 2034. Cheniere intends to use the proceeds to retire its $1.5 billion of Cheniere Corpus Christi Holdings senior secured notes due 2025.

March 12. Hess Midstream (HESM) announced the repurchase of $100 million of Class B units from its sponsors, Hess Corporation (HES) and Global Infrastructure Partners. The transaction will mark $1.65 billion of unit repurchases from sponsors over HESM’s life as a public company.

March 13. Kinetik (KNTK) announced an underwritten secondary offering of 11.37 million Class A shares. KNTK will not receive any proceeds from the offering, which will result in Apache Corporation’s (APA) exit as a KNTK shareholder.

March 14. Baytex Energy (BTE) announced the pricing and upsizing to US$575 million of its private placement offering of senior unsecured notes due 2032, which will bear interest at 7.375% per year. BTE plans to use the proceeds to redeem US$409.8 million of its outstanding 8.75% notes due April 2027 and a portion of debt outstanding on its credit facilities. The move reduces risk to shareholders by extending BTE’s nearest maturity by five years.