murat4art

murat4art

I give a buy rating for Heico Corporation (NYSE:HEI) as I am very positive about the near-to-medium term growth potential as air travel continues to grow, more planes become older that require more maintenance, and the acquisition of Wencor expanded HEI’s SKU range significantly. I also think that HEI is pricing its products where they should be; hence, it should be able to continue increasing prices, driving top-line growth.

HEICO is a diversified aerospace and defense component supplier. The business has two key segments: Flight Support Group [FSG] and Electronic Technologies Group [ETG]. In the FSG segment, HEICO manufactures, distributes, and repairs component systems or platforms. It develops and certifies parts for sale directly into the aftermarket via third-party Parts Manufacturer Approval [PMA]. It sells these parts direct to airlines and MROs, through owned distributors, and through its own repair shops, providing a lower-priced alternative to the OE-made aftermarket part. As for ETG, it is a specialized defense component manufacturer for airborne defense applications. HEICO owns distributors and MRO shops to sell parts through, leveraging existing customer relationships to offer a discounted aftermarket product.

1Q24 revenue grew 44% y/y on a reported basis and 7% organically to $896 million, 2% ahead of the consensus estimate of $891 million. By segment, FSG saw revenue of $619 million. Sales were up 12% organically and 3% sequentially. The organic growth was driven mainly by increased demand for commercial aerospace parts and services. For ETG, revenue grew 12% to $286 million, driven by the benefit of M&A contributions as well as increased demand for commercial aerospace products, partially offset by decreased demand for other electronics, medical, and commercial space products. Operating earnings saw $180 million, 9% above the consensus estimate of $177 million. That said, operating margins compressed by 70bps to 20.1%. The compression was due to dilution from Exxelia at ETG, while FSG margins of 22% fell 50 bps on dilution from Wencor acquisition costs.

I expect FSG to continue seeing strong revenue growth in the near to medium term. The main driver of this growth expectation is that air traffic has recovered very nicely when compared to pre-covid (2019 level). In fact, 2024 is going to be such a strong year that it is expected to be record-breaking for airlines. According to IATA, there would be 200 million more passengers than pre-COVID levels. This demand will drive up the utilization of aircraft, which will increase the demand for aftermarket parts. In addition, the average age of aircraft (airline-owned passenger planes) is getting older, increasing from an average of 14 years in 2019 to 16 years in 2024. This suggests a larger pool of addressable planes for HEI. An important point to note here is that the older the plane, the greater the need for repair and maintenance (especially with the recent Alaska incident, I reckon airlines will be more tight on maintenance). Hence, I think the outlook for growth in this segment is very positive. Apart from organic volume growth, I also expect HEI to continue benefiting from price increases, as HEI seems to be underpricing compared to peers.

So I honestly, I think that our pricing has been a lot more conservative and gentle than it could be. Our competitors are substantially raising price. Company 1Q24 earnings

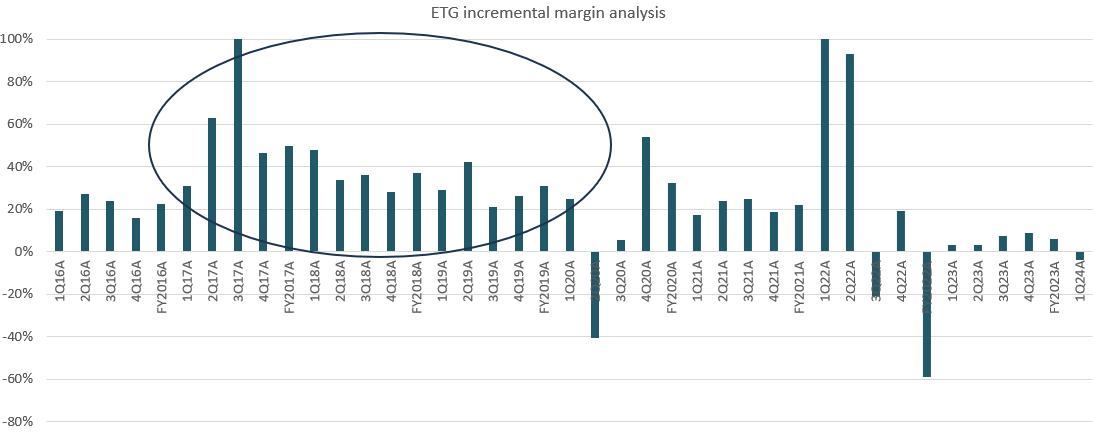

Regarding the ETG segment, my focus is on its margin expansion potential. In 1Q24, ETG margins went below the 20% level, which is a negative sign on a headline basis. However, I think it should rebound easily, as the decline was largely due to the 5% revenue decline seen in defense revenue (50% of ETG segment revenue), reflecting the pulled-forward earnings over the past few years. Looking ahead, the timing of shipments should support a rebound in organic growth in the next couple quarters. Management has already signaled the beginning of a turnaround in the defense segment; hence, I think we should see a recovery from here, growing back to mid-single digits. Attaching the same incremental margin that HEI historically generated, my analysis shows the margin expanding back to a low 20 percent. Another thing to note is that HEI stepped up on research and development [R&D] in the quarter (130 bps headwind) by 22% to work on certain development programs. As this R&D tapers down over time, margins should also improve.

May Investing Ideas

I am also very positive about the Wencor acquisitions. In my opinion, the combined HEI and Wencor can go to market as a larger supplier, which is attractive to airline customers. HEI had ~13,000 PMA part SKUs (3Q22 earnings call) prior to the transaction vs. Wencor ~6,000, or a combined ~19,000. The combined company targets 350–550 new parts per year (vs. 300–500 prior). Importantly, Wencor extends the HEI SKU range to include bearings. The combined scale makes HEI an even more attractive “vendor” to work with, as customers are able to get hands on what they need via one channel, making their lives easier. More importantly, the cost savings are real (it can easily save up to 25% with its parts). In addition, with HEI's wide distribution capabilities, I expect HEI to easily cross-sell the new range of SKUs to its entire customer base. If we look back at the operating history of HEI, it has worked with many airlines over the decades. Its distribution capacity has also expanded to include network carriers, low-cost carriers (LCCs), and regional airlines. Moving forward, I think the important aspect to monitor is the integration of both HEI and Wencor sales forces, such that both can cross-sell each other's products seamlessly.

And then likewise in distribution, we focus in different areas Wencor is, for example, has a very large position over in the bearings area, whereas HEICO basically doesn't, isn't involved in the bearings business. Company 1Q24 earnings

May Investing Ideas

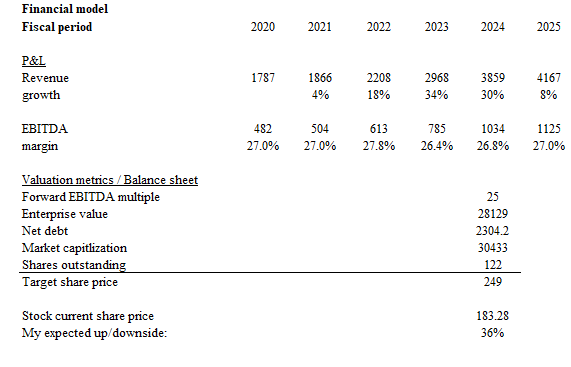

Based on my research and analysis, my expected target price for HEI is $249.

I think the biggest risk to HEI, which has just happened recently, is a major lockdown. This will literally wipe the utilization of aircraft to near zero, which was what happened during the pandemic. If that happens, no matter the size of the HEI-addressable market, demand will be decimated. As we saw in FY20, the HEI share price fell from $120 to $60 in just a few weeks.

I hold a bullish view on HEI. My belief is that HEI has a very positive outlook, driven by growing air travel. Also, many of the planes in operations are also getting older on average, which translates to more maintenance needs. Plus, it seems HEI has been undercharging compared to the competition, so I expect continuous price increases, boosting their top line. The recent acquisition of Wencor is another big win for HEI. With a bigger, more attractive product portfolio and a wider distribution network, I expect HEI to reap positive synergies from this deal. For valuation, I got a target price of $249 for HEI based on my projections for revenue and EBITDA growth, along with a premium valuation that reflects HEI's positive outlook.