PM Images

PM Images

Written by Nick Ackerman.

Schwab U.S. Dividend Equity ETF™ (NYSEARCA:SCHD) recently went through its annual reconstitution on March 15th, 2024. We had already seen a preview of what changes there would be, as this is a passively managed fund based on the Dow Jones U.S. Dividend 100 Index. Therefore, the news posting for the changes in that index was already available earlier in the month, and that gave us a good idea of several of the changes. Several of the largest allocations of the fund have remained the same.

SCHD has been treating us well after we took a position last year thanks to taking assignment of some puts. Since then, we've looked to double down and add to the position opportunistically by writing more puts. Further, we even had a chance to write some covered calls through last year, bringing in even more option "income."

One of the reasons I find utilizing options writing on SCHD as attractive is that the fund is mostly what I already hold, but just adding even more diversification.

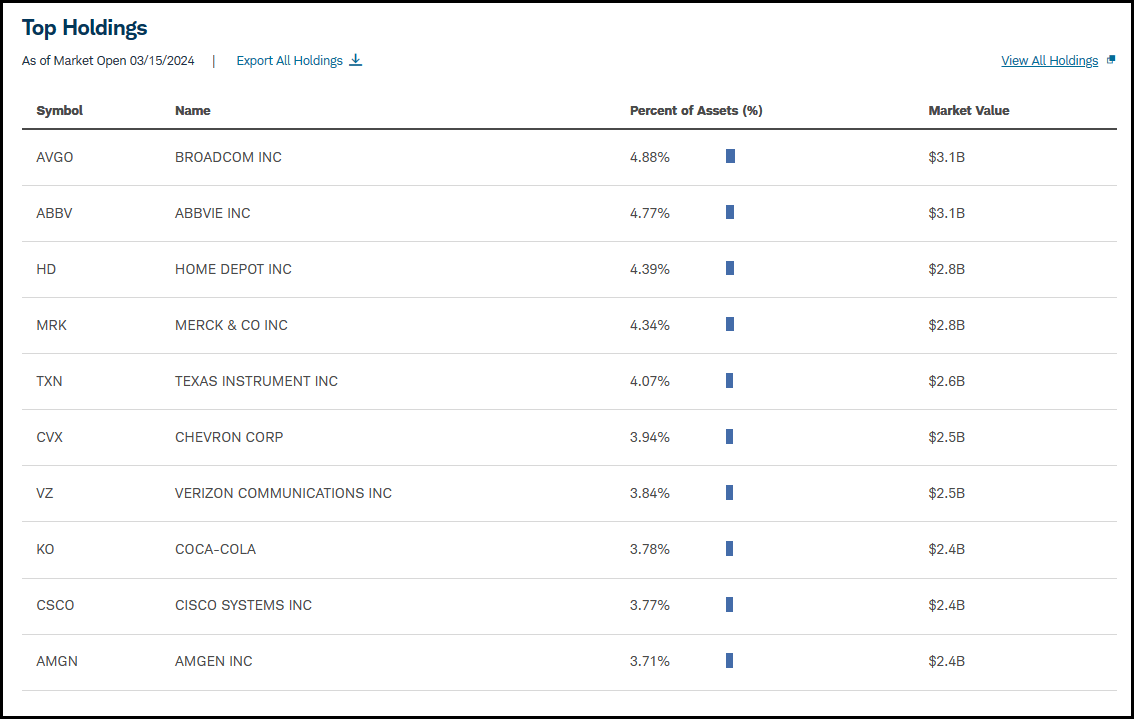

Here is the latest top ten, as of last Friday - note the "market open 03/15/2024."

SCHD Top Ten 3/15/2024 (Schwab)

I own individual positions in AbbVie (ABBV), Home Depot (HD), Merck (MRK), Texas Instruments (TXN), Chevron (CVX) and Verizon (VZ).

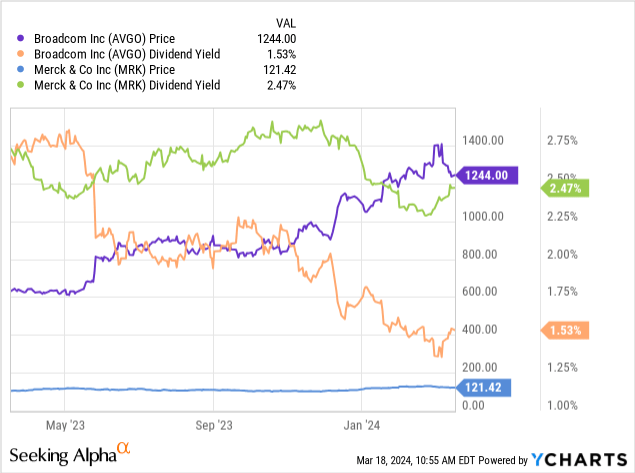

I don't own Broadcom (AVGO), but it is at the top of my watchlist. It's the big one that got away, and I kick myself to this day. I passed on it when it was trading at just over $600 a share as I remained stubborn with my sub-$600 price target. Since then, I've moved up my buy target to $900. We've seen shares correct from the peak quite a bit now as shares fall just over 14% from their all-time highs. That said, I'll probably once again remain stubborn in waiting for my buy target - and perhaps curse myself all over again in another year.

On the three other names here, I don't have Coca-Cola (KO), Cisco Systems (CSCO), or Amgen (AMGN) in my portfolio—at least not directly—but I do through SCHD and other funds. That said, I could easily see owning positions in KO or AMGN.

Maybe not CSCO so much, but they are still checking the box to pay a growing dividend. They are still earning plenty of free cash flow and trading at a reasonable valuation, too. Perhaps their future will be a bit brighter, and they can return to earnings growth - which would likely provide more enthusiasm for the company's stock.

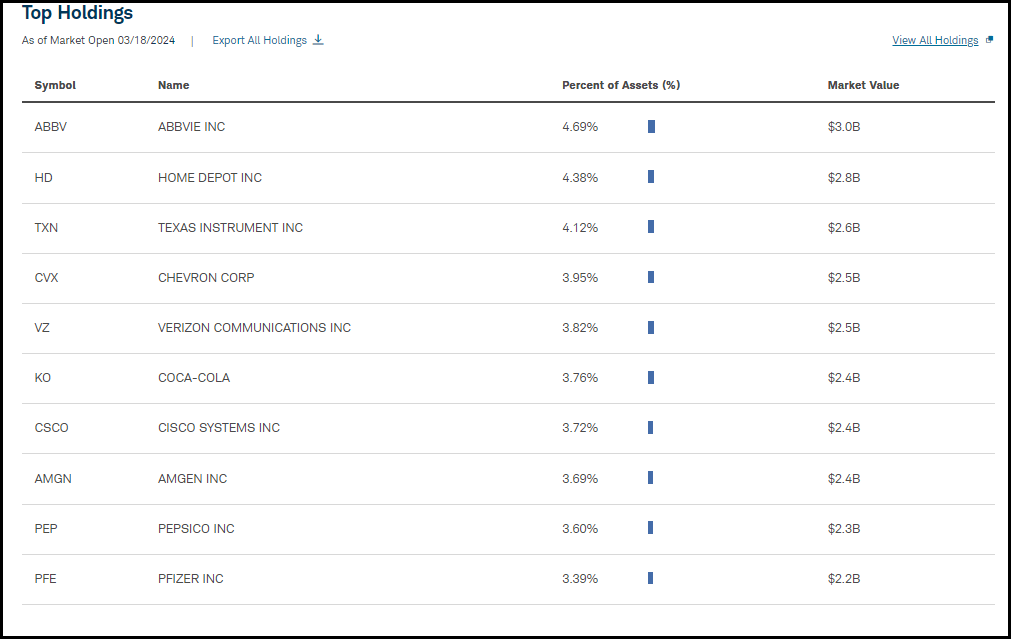

With all that being said, let's take a look at the top holdings now after the reconstitution. Again, we can note the "market open 03/18/2024" at the top.

AVGO Top Ten 3/18/2024 (Schwab)

ABBV, HD, TXN, CVX, VZ, KO, CSCO, and AMGN are all retaining top positions. That only means PepsiCo (PEP) and Pfizer (PFE) are new names that slid into the top holdings. That said, PEP and PFE were actually positions number 11 and 12 for the fund previously anyway; they just slid to now higher allocations.

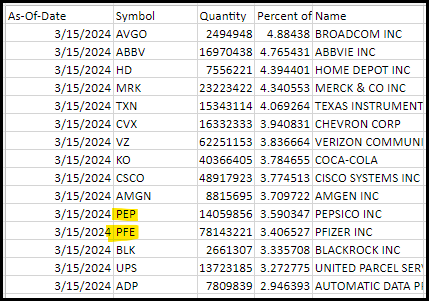

SCHD 3/15/2024 PEP and PFE Holdings (Schwab (highlights from author))

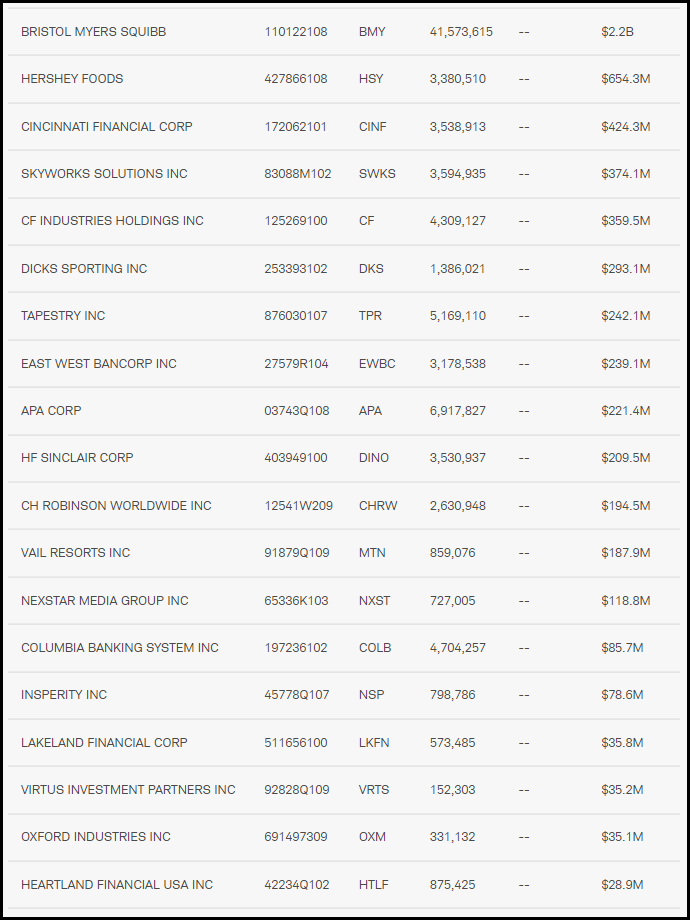

Interestingly, we should also see Bristol-Myers Squibb (BMY) in a top spot now, as this was a meaningful addition to the fund. Instead, the new names for the fund haven't been given allocations in terms of percentage yet.

SCHD New Names (Schwab) SCHD New Names (Schwab)

So, for the fund's largest allocations, we've just seen an overall general slide up with several familiar names. The main material difference for the fund's largest allocations is BMY, which is now going to be making an appearance as well.

Of course, that means there were some removals from the top spots. It resulted in AVGO and MRK being removed from the fund. Both of these names have now been completely removed.

While that might be a bit of a shock, considering those are definitely solid names, it comes as these names have performed quite well. Trimming winners can make sense, and this is one of the ways that an investor can take the emotion out of it, letting a passively managed index cull those names.

The appreciation in these is to the point where the yield on these names has come down considerably - particularly for AVGO. Given that the ranking process has IAD yield as part of its process and limits sector representation, this played a role in those names being excluded.

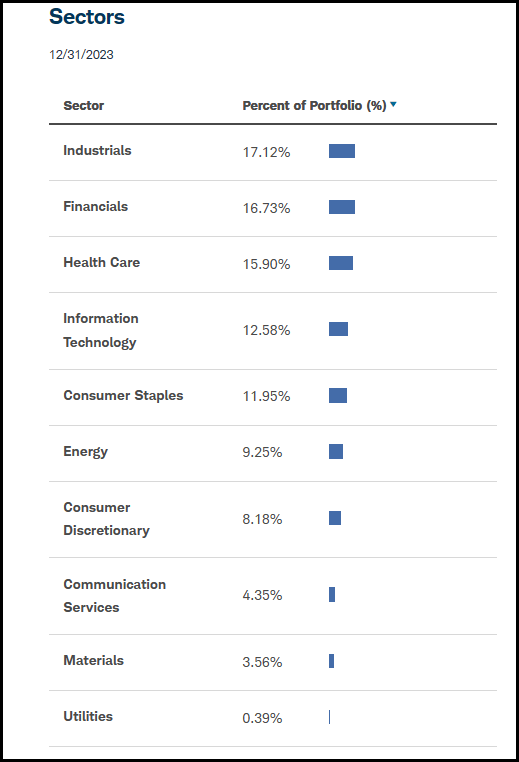

A portfolio like this provides another appealing feature of the fund, in my opinion. It provides more exposure to a value-oriented portfolio rather than going so tech-heavy as the S&P 500 Index (SP500) has become. As of the end of December 2023, the fund listed that the average P/E was 16.09x.

SCHD 12/31/2023 Sector Allocation (Schwab)

However, this table has not been updated as of the writing of this piece. Given the many similarities of the portfolio names during the reconstitution, there likely will not be a dramatic shift.

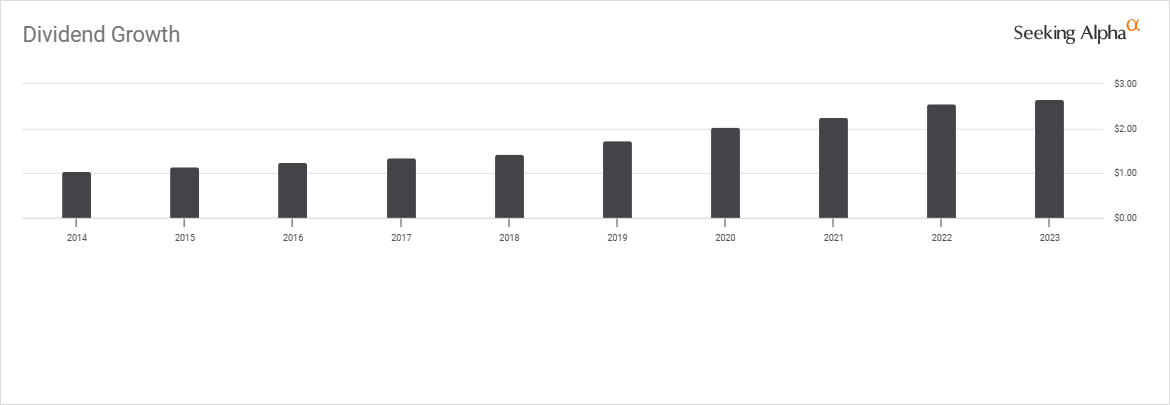

With this portfolio's dividend focus, we've also seen SCHD deliver an attractive yield. Currently, the yield is 3.37% based on the last four dividends paid. Even better, though, it's grown year over year since the fund's launch. Last year's increase was relatively shallow, at 3.77% year-over-year growth. However, in the prior four years, the average annual increase was a sizzling 15.55%.

SCHD Dividend History (Seeking Alpha)

As we've covered in the past, we've been able to generate additional income by collecting option premiums from writing options on this name.

On February 16, 2024, we wrote the $75 puts and collected $0.27. The actual premium received may not appear too appealing, but when considering it's over 28 days, the potential annualized return comes out to 4.69%; plus, with cash-secured puts, one is receiving around 5% these days on the cash that's just otherwise sitting there. The PAR itself is also higher than the dividend yield of SCHD, so if one is comfortable just sitting and holding shares of SCHD for the dividend, then one could find earning 4.69% plus the interest on cash quite appealing.

That said, over the last month, the shares continued higher, and taking assignment never really came close.

Ycharts

What it did allow us to do is what I also did with this trade, and that is to write more puts even before these ones expired. That's why, on the Friday expiration day, I turned around and wrote another batch of puts for next month's expiration, April 19.

As a quick reminder, I already hold some shares of SCHD due to taking assignment of puts last year. That was at $76, and throughout the year, my idea was to write covered calls - that did end up occurring. However, the share price also came under pressure throughout the year, and writing more puts also became an attractive endeavor.

Then, I ultimately decided that holding a consistent position in SCHD rather than using the options wheel strategy sounded appealing. This is where we are today, where I've decided to hold onto the shares I have but write more puts to implement the options wheel strategy still.

Here is a full recap of all the selling options we've done since initiating our original trade.

| Ticker | Expiration Date | Upper Strike | Lower Strike | Current Price | Type Sold | Date Initiated | Premium Collected | Date Closed | Closing Cost | Gain/Loss |

| SCHD | 03/15/2024 | $75.00 | - | Expired | Puts | 02/16/2024 | $0.27 | Expired | - | $0.27 |

| SCHD | 02/16/2024 | $73.00 | - | Expired | Puts | 12/21/2023 | $0.50 | Expired | - | $0.50 |

| SCHD | 12/15/2023 | $65.00 | - | Expired | Puts | 10/25/2023 | $0.50 | Expired | - | $0.50 |

| SCHD | 08/18/2023 | $76.00 | - | Expired | Calls | 07/19/2023 | $0.43 | Expired | - | $0.43 |

| SCHD | 06/16/2023 | $67.00 | Expired | Puts | 05/15/2023 | $0.40 | Expired | - | $0.40 | |

| SCHD | 05/19/2023 | $76.00 | Expired | Calls | 04/03/2023 | $0.52 | Expired | - | $0.52 | |

| SCHD | 03/17/2023 | $76.00 | Assigned | Puts | 02/17/2023 | $0.90 | Assigned | - | $0.90 | |

| SCHD | 02/17/2023 | $76.00 | Expired | Puts | 01/13/2023 | $0.62 | Expired | - | $0.62 |

This doesn't include the latest puts that we wrote just last Friday, but we did collect another $0.40 for those efforts. For the trades that did expire, we netted $4.14 in options premium. Being long a position since March 17, 2023, we've also collected all of 2023's dividends, which amounted to $2.658. We are also going to be due the next upcoming dividend, as the fund goes ex-dividend on March 20 this year for the Q1 payout.

By writing more puts, I believe the worst-case scenario is I end up holding an overweight position in a diversified dividend-paying ETF. Being that it is diversified over 100 names, it technically wouldn't even be overweight any individual position. It just further complements my own individual positions quite well. In fact, it is mostly more of what I already hold and generally dividend-paying names I wouldn't mind holding either.

Overall, the Schwab U.S. Dividend Equity ETF has provided a solid and growing dividend for investors holding the shares. The passive nature based on a screening process keeps investors disciplined, even if it means selling out what appear to be solid winners. The fund complements my portfolio well by bringing even more diversification to the table. Being able to generate further meaningful option income from this name has been a bonus for us.

Editor's Note: This article covers one or more microcap stocks. Please be aware of the risks associated with these stocks.