da-kuk

da-kuk

I recommended a buy rating for HashiCorp (NASDAQ:HCP) when I wrote about it the last time, as there was no fundamental change to the long-term growth outlook, which I believed could support HCP growth recovery back to >30%. Based on my current outlook and analysis of HCP, I recommend a buy rating. While the path to reaching 30% growth is being delayed, I believe the likelihood of it actually reaching 30% has gone higher because of the initiatives that management is rolling out. The fact that management started to buy back its own shares could be a signal that they find the stock undervalued as well.

HCP 4Q24 performance showed enough strength to push FY24 results above my expectations. 4Q24 revenue came in at $156 million, which was above the midpoint of guidance of $149 million. This led to FY24 total revenue performance of $583 million, $6 million above my target, which translates to 150 bps of growth upside on a growth basis. While FY24 ended well, FY25 guidance appears weak on a headline basis. Management guided for FY25 revenue of $645 million at the midpoint, implying 11% y/y growth, which is 400bps lower than my expectations. I believe this slowdown is just a reflection of the strategic initiatives that management is implementing; as such, it is a near-term-pain-but-long-term-good kind of thing. The market appears to be reacting well to these initiatives (as I discuss below), given that the share price went up after that guide.

On the initiatives, the key highlight is HCP’s three prong initiatives to drive sales team productivity, commercial differentiation, and cloud focus, and I am very bullish on this. At a high level, the plan is to improve sale execution, improve commercial differentiation vs. the open-source product, and reallocate resources and compensation toward its cloud product.

As you can see, these are not easy iterations that one can just flip the switch and immediately see results. Hence, I think a slowdown in growth in FY24 is reasonable, and management did very well in managing expectations by setting up the medium-term performance framework that points to 20% revenue growth, reaching PF EBIT breakeven status, and generating positive free cash flow. In the near term, management expects to see a mild U-shaped recovery in its revenue growth rates in FY24, with 2Q24 expected to be the trough in revenue and cRPO growth rates (expected to exit FY25 at around ~20% cRPO y/y growth on a quarterly basis). What is important to note about cRPO performance is that, because of growing cloud penetration, cRPO growth will become a leading revenue indicator, which should give the market better “visibility” into growth, and this really helps in modeling the business.

Finally, I thought the decision to initiate a share repurchase program seemed a bit weird, but it was actually positive. Remember that HCP is still pretty much in the growth zone, and they are not generating positive free cash flow yet. My guess is that they have too much cash on the balance sheet (~$1.3 billion), and management probably thinks that their own shares are cheap, so they are buying them back, which also acts as a way of returning capital to shareholders; hence, it is not a bad decision after all.

Author's work

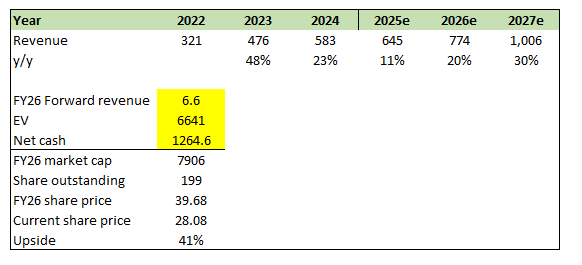

I believe HCP's ability to see growth accelerate to 30% is still within sight; it's just that it is being delayed by 1 year due to the strategic changes being implemented this year. While this is a 1-year delay, I am supportive of those changes because it instills higher confidence that they are achievable. Guidance for FY24 is 11% growth, and I expect growth to accelerate to 20% in FY26, followed by 30% in FY26. At the 6.6x forward revenue multiple that HCP is trading at today, I see an upside of ~41%, but readers should note that if HCP growth accelerates as I expected, there is a very high chance of the market re-valuing the stock upwards because it is still trading below its historical average of 8.5x.

The strategic changes noted by management are positive, for sure, if they work out. If it doesn’t, then growth recovery to 30% could be further delayed, and I think the market will penalize HCP for any misexecution here, given that the stock went up likely due to the guide. Also, management's commitment to allocating capital to share buybacks might restrict its ability to be aggressive about investing in the business when needed.

My recommendation is to maintain a buy rating for HCP despite FY25 revenue guidance slowdown due to strategic initiatives. Specifically, I am positive about management's three-pronged growth strategy which focuses on sales productivity, differentiation, and cloud products, although they will impact term revenue growth. A notable part of this is that, if executed well, the cloud product focus should improve growth visibility as cRPO becomes a leading metric for revenue growth. On valuation, I also see upside potential if growth accelerates as I expected.