Luke Sharrett

Luke Sharrett

In my previous article, I indicated that I was selling CONSOL Energy (CEIX) and re-deploying the capital towards met coal companies instead of thermal coal companies. One of the companies that I have been buying this week is Warrior Met Coal (NYSE:HCC). If one is bullish on the met coal industry, one can start establishing a position in the coming months while prices should languish in the "shoulder season."

Warrior Met Coal is an Alabama-based exporter of Australian Premium Low-Vol hard coking coal to the global steel industry. The company has two major mines that produce 7.6 million short tons annually with reserves of over 20 years.

HCC has been a standout performer over the last three years. Shares have tripled over the last three years on the back of higher coal prices.

Trading View

The company boasts some of the highest coal assets in the United States with a mix of coking coal grades that allow the company to achieve premium prices in the export market.

The main catalyst is the Blue Creek Mine that is currently under development. Once this mine is completed in 2026, the company should generate $647-800 mm of free cash flow. Generating that type of cash flow against a $2.3 billion enterprise value should propel the shares much higher.

Shoulder season in the coal markets refers to the period between the peak and the off peak season. More specifically, in the coal markets, investors have been conditioned to sell in February and buy back later in the summer. It's worked the last three years.

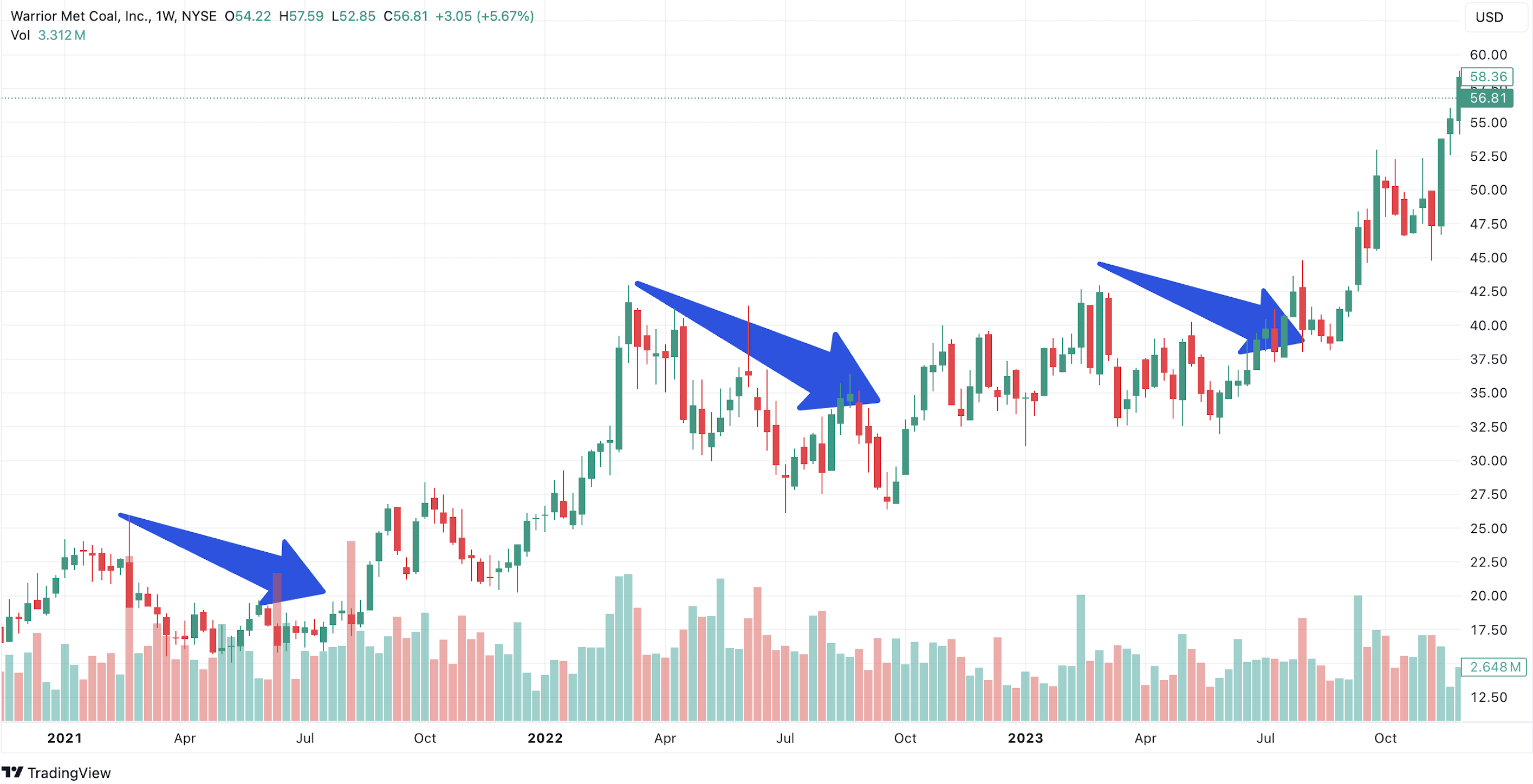

Trading View

I've highlighted with the blue arrows the weakness of the share prices over the past three shoulder seasons.

Usually, I build a position incrementally by adding 20% of my total position each month until August 15 or so. If I'm trying to establish a 1,000 share position in HCC, I would buy 200 shares per month until mid summer. I expect that I will get a chance to buy HCC in the range of $45-55 during the shoulder season.

There has been some unexpected weakness in the coking coal markets since October 2023. The futures market is also pricing in weakness in to late spring.

Australian Coking Coal Prices (Trading View)

It appears that there is some demand weakness out of China. Local Chinese coke producers passed their fifth round of price cuts in March. This month, China’s coking coal and coke production fell due to weak steel demand and a decline in pig iron production.

HCC shares do not have the support of share buybacks like other coal companies, particularly Alpha Metallurgical Resources (AMR). Since HCC is focused on growth and is investing heavily in the Blue Creek Mine, the shares do not have buybacks that can support the share price through the weak shoulder season.

Since coal companies are under represented in ETF's and passive fund flows, many coal investors have focused on share buybacks as a way to unlock value.

Since HCC is using most of its free cash flow for CapEx at the Blue Creek mine there is little hope of any buybacks until 2026.

Without the buyback machine scooping up 7-10% of the float every year, it is likely that HCC will underperform until investors start focusing on how much free cash flow will be generated with the Blue Creek mine.

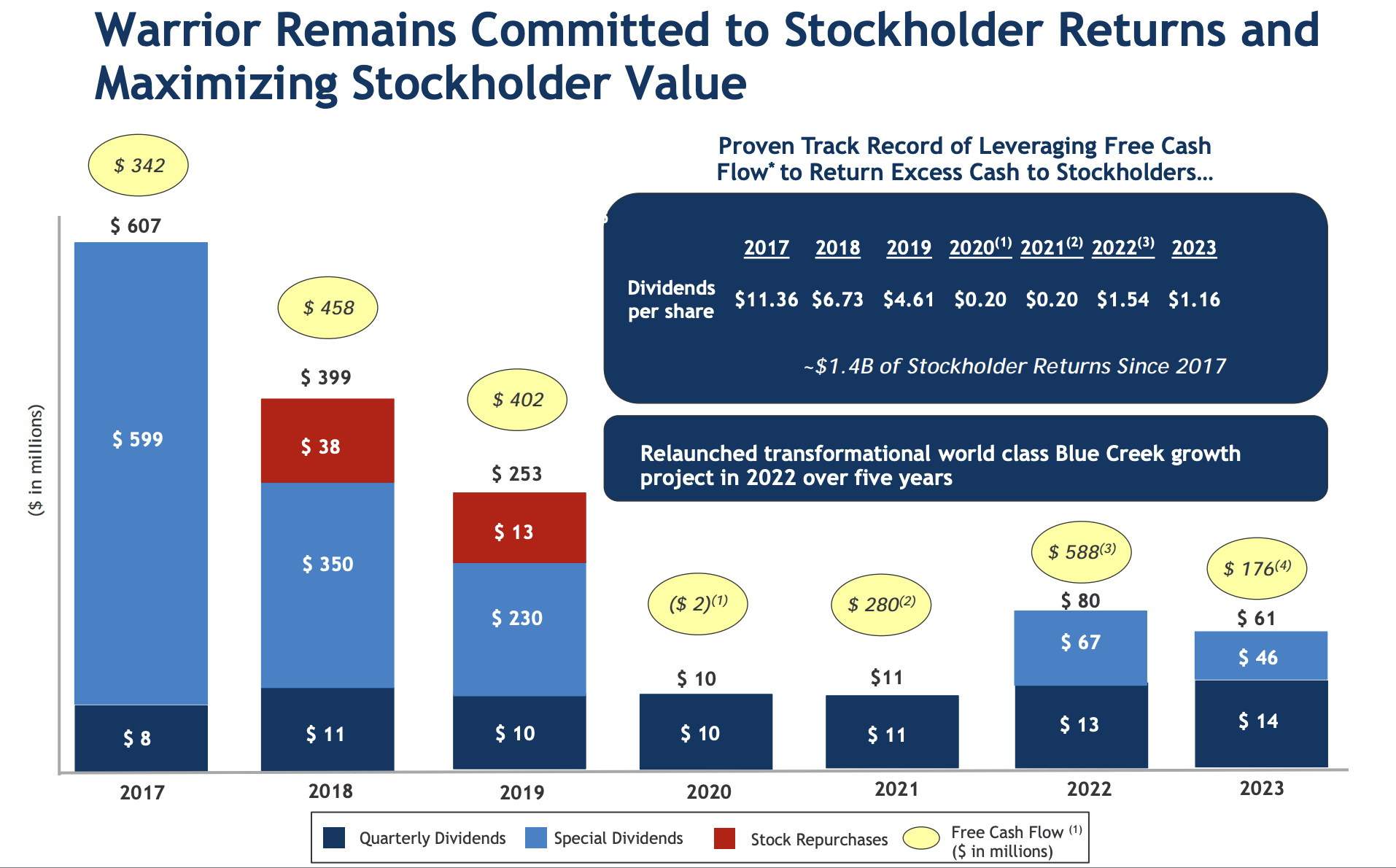

HCC Investor Presentation

Interestingly, Warrior has never been a buyback machine. In the 2017-2019 time period most free cash flow was returned to shareholders via dividends. However, once the Blue Creek mine is completed, HCC can either issue special dividends or initiate buybacks.

The Blue Creek mine is one of the largest untouched metallurgical coal reserves in North America. It is a staggering resource with a reserve base of 69.8 million short tons of recoverable reserves and 49.5 million short tons of coal resources (excluding reserves).

It is estimated that Warrior will generate $647-800 mm of free cash flow in 2026 once the Blue Creek Mine is up and running.

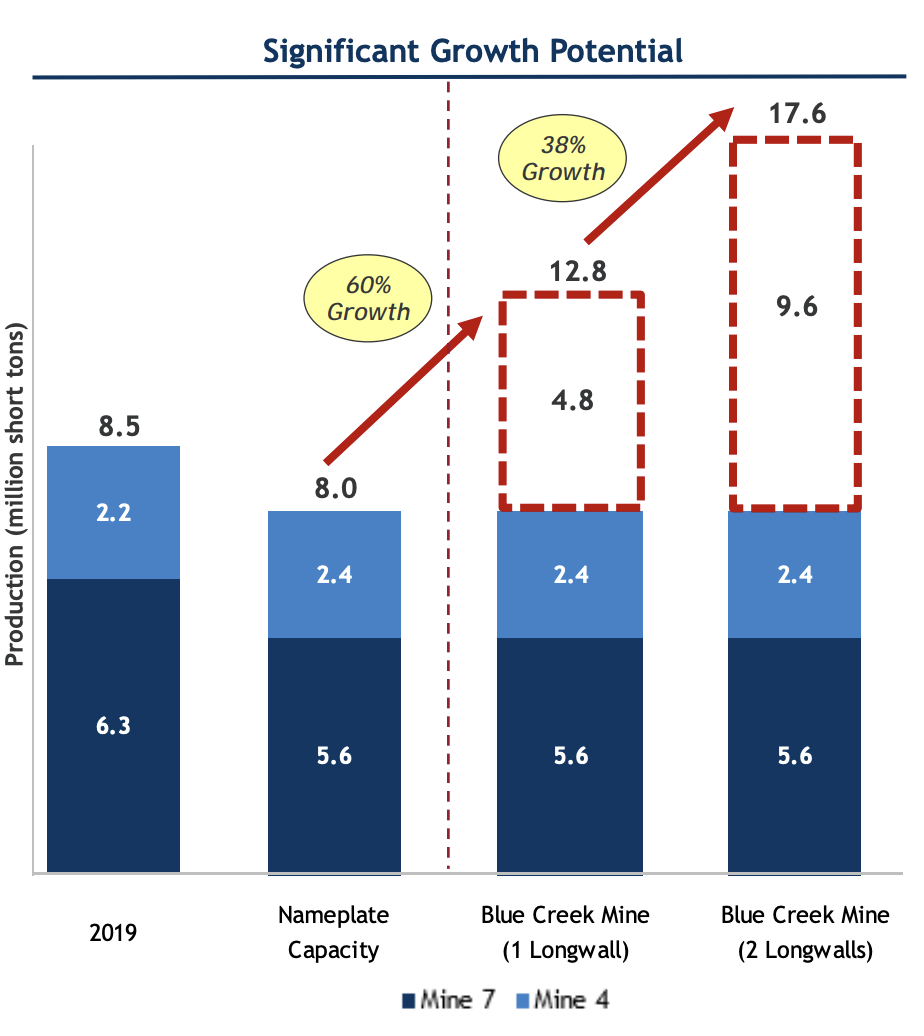

As you can see from the chart below production is estimated to increase from 8 million short tons to 17.6 million short tons.

HCC Investor Presentation, February 2024

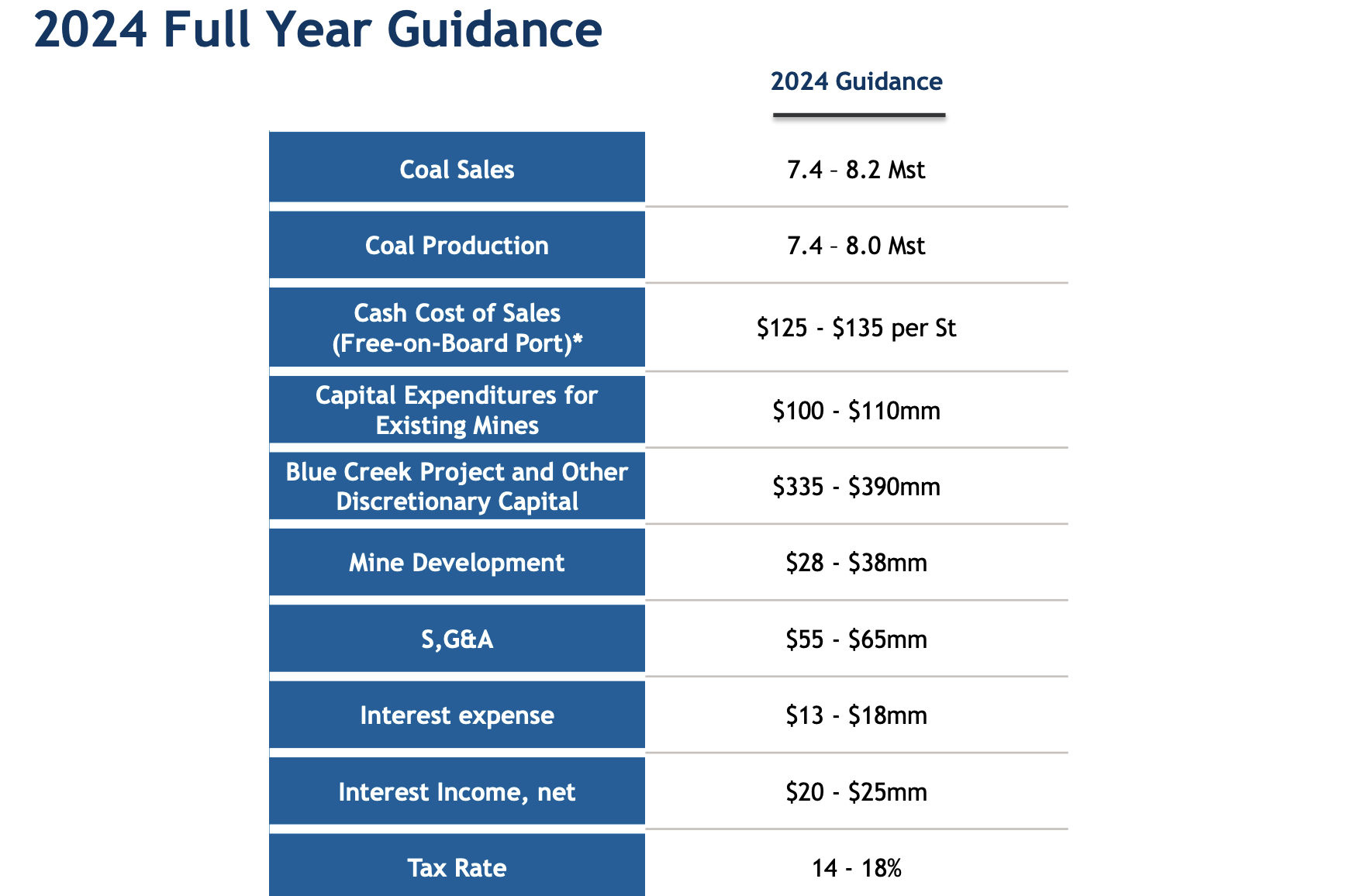

For 2024, company has earmarked $335-390 mm for the continuing development of the Blue Creek Mine. Investors need to be aware that this is a billion dollar project and these types of projects have a tendency to run into cost overruns and delays. The total capex estimate has already moved up from $700 mm to over a billion dollars. One of the big risks to the investment thesis are construction delays and cost overruns. The other big risk is a collapse in coal prices. We all remember coal prices getting cut in half in 2019-2020.

First of all, Warrior Met Coal is a conservatively financed company. The company has $173 mm of debt against an asset base of $2.3 billion. In 2023, the company retired 50% of their senior debt.

Last month the company provided estimates for 2024.

HCC Investor Presentation February 2024

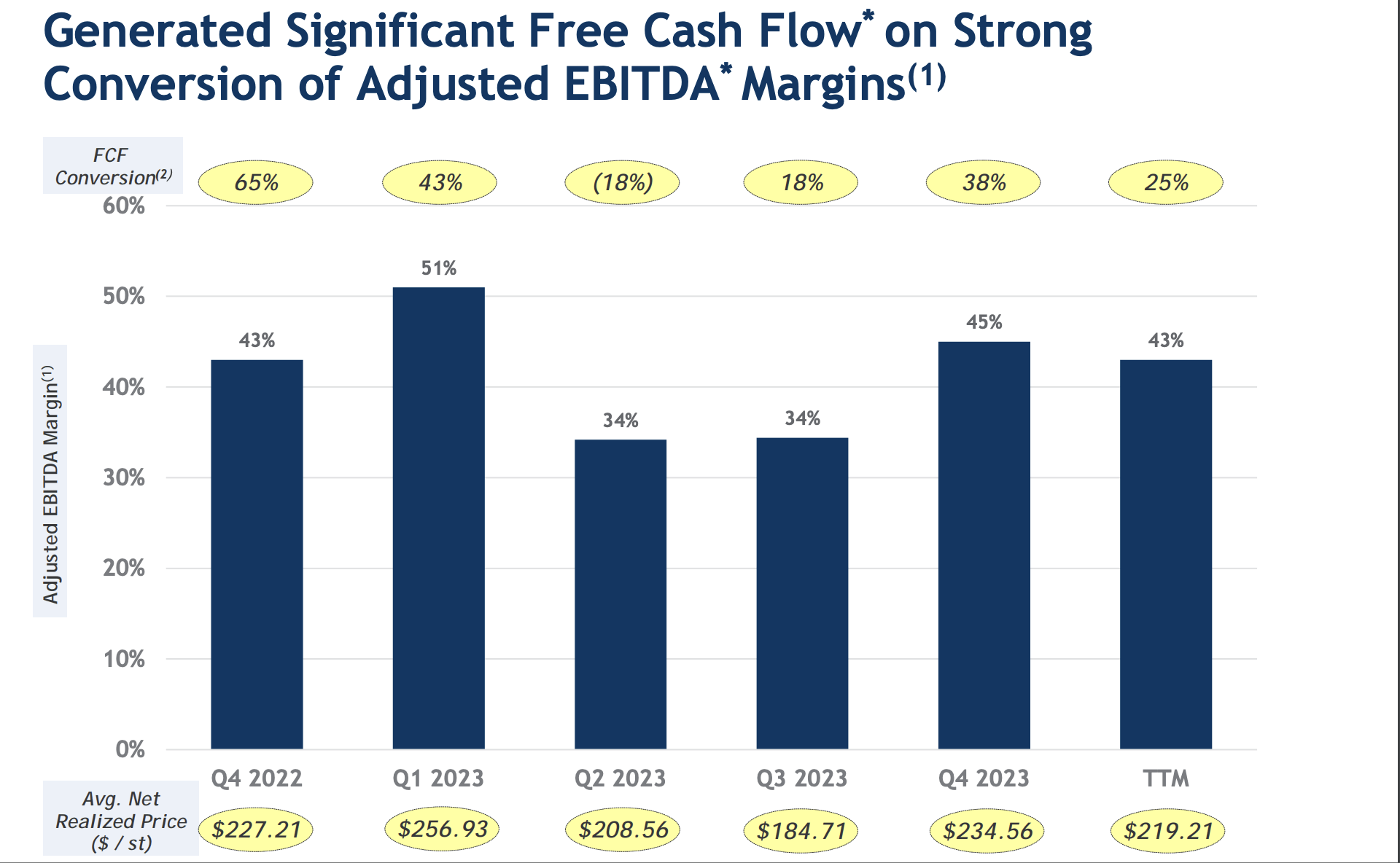

In 2023, the company generated $701 mm of operating cash flow. Similar numbers are expected for 2024. The company has an enterprise value that is only 3.3X cash flow. The shares are cheap based on current production levels.

In addition, the company is able to generate significant free cash flows as long as realized coal prices stay in the $200-250/st price range.

HCC Investor Presentation

However, once you factor in the growth with Blue Creek, the shares become quite bargain if you're able to look forward to 2026 and beyond. Production will almost double to 17.6 million short tons. This alone should result in ~$400 million of free cash flow. Once you add in the $335-395 mm of savings from mine costs you are left with $647-800 mm of free cash flow.

I own Warrior Met Coal with an eye towards 2026. When the Blue Creek Mine is up and running, I expect the company to generate $647-800 mn of free cash flow annually. It is important to note that the company will also not be spending $335-395 mn annually on the mine construction. There will be a boatload of cash available via special dividends or buybacks. With a $2.3 billion enterprise value, HCC will either issue special dividends as they did in 2017-2019 or follow the example of other coal companies and initiate significant buybacks.