FG Trade

FG Trade

I am updating my previous analysis on HCA Healthcare, Inc. (NYSE:HCA) in light of a continuous run-up in the stock price since my last article.

Following Q2 and Q3 earnings, I rated HCA a buy with price targets of $315 and $313, respectively. My thesis was summarized as follows:

Since my last analysis, HCA has been up more than 16% with essentially continuous growth.

HCA Price Trend (Seeking Alpha)

Incorporating 2023 full-year performance, 2024 guidance, and industry trends my DCF-generated price target is largely unchanged at $312 so HCA is now slightly ahead. In addition, I see balanced opportunities from the strategic growth plan and risks from industry headwinds. With that in mind, I lower my rating from buy to hold as I believe the stock is fairly priced.

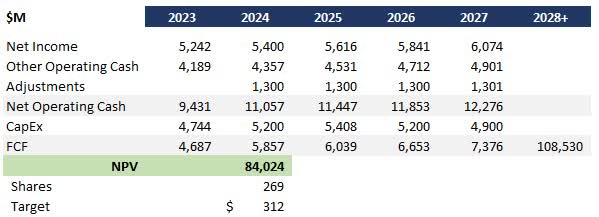

I updated my ongoing DCF analysis to incorporate new guidance and 2024 financials and actually came within $1 of my previous model and $3 of my first model showing how stable this business and the guidance has been. I made the following underlying assumptions in the model:

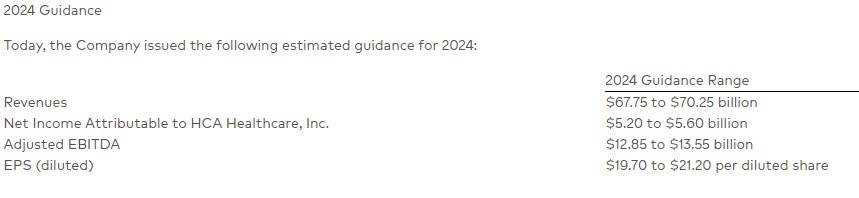

2024 Guidance (HCA Investor Relations)

This model yielded a price target of $312, a 4% downside from today's pricing but within the margin of safety, especially for a dividend stock.

HCA DCF (Data: SA; Analysis: Mike Dion)

Wall Street is just slightly higher at a price target of $332, 1% upside from today's pricing and within the margin of safety.

Wall Street Rating (Seeking Alpha)

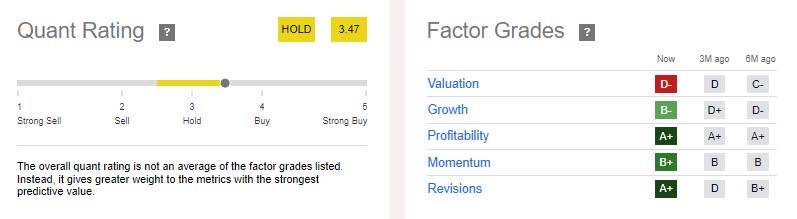

The quant rating also signals a hold, with strong momentum, growth, and profitability offset by high valuation multiples.

HCA Quant Rating (Seeking Alpha)

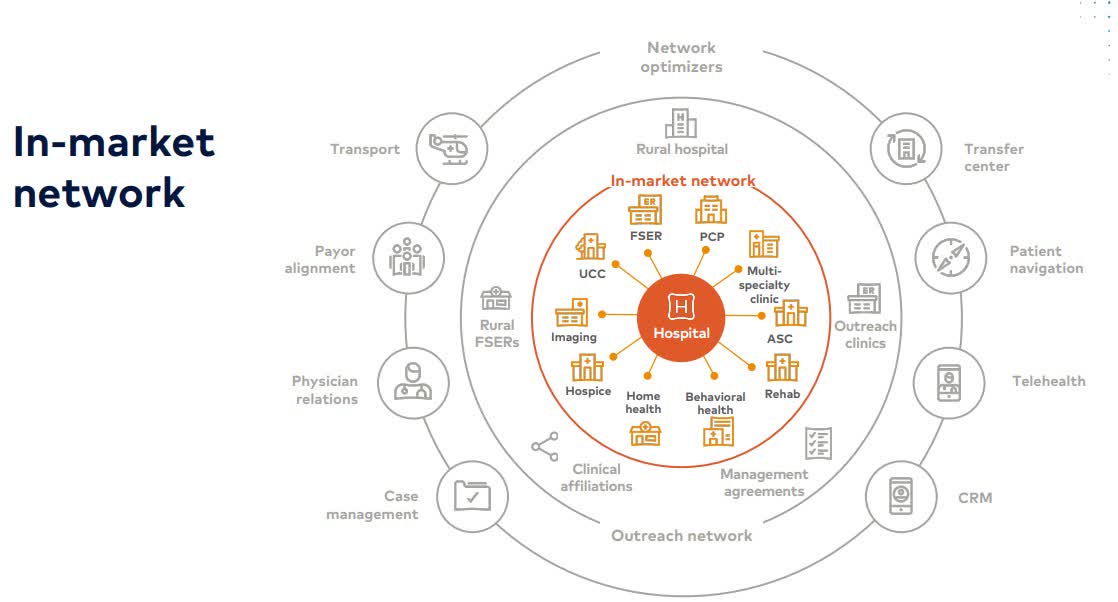

First, HCA has laid out a clear strategy to integrate patient care and thereby capture more healthcare dollars while moving patients through higher-margin services. By expanding their in-network services and building partnerships with out-of-network clinics (especially in rural areas) and "network optimizers," as they call them, HCA is able to increase utilization and admissions in the hospitals that are the core of their business.

HCA Network (HCA Investor Relations)

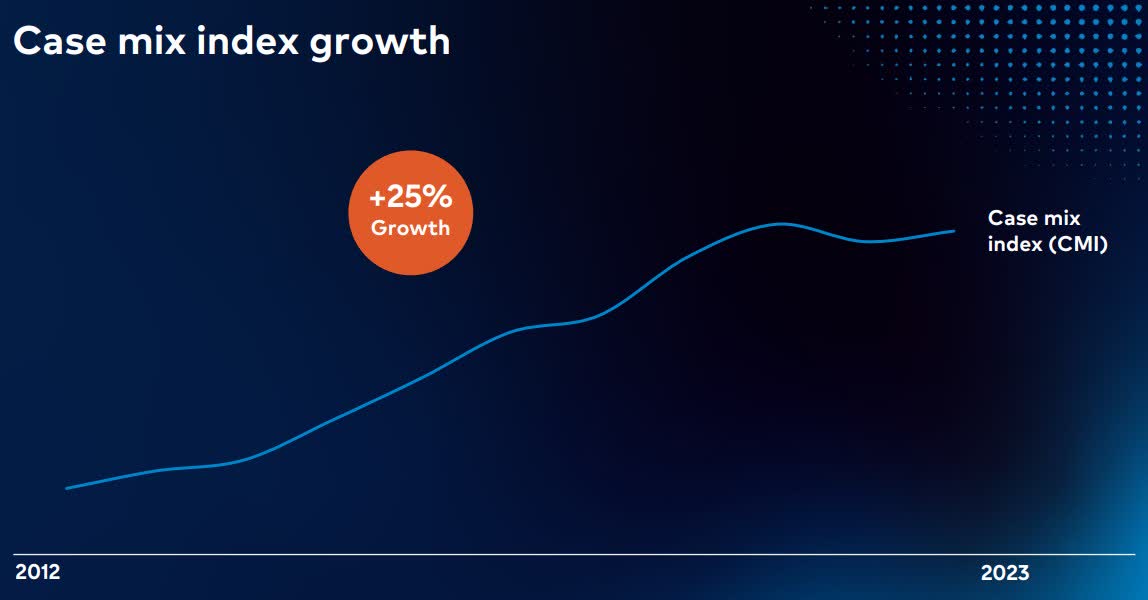

Second, HCA has been focusing on expanding scope and mix of services to drive higher-margins and lower volatility. This is measured using the case mix index which is up 25% and nearly continuously over the past 10-years. HCA noted recently that no single service makes up more than 14% of their inpatient revenue.

Case Mix Index (HCA Investor Relations)

Lastly, HCA has an unprecedented scale for a for-profit hospital provider. They have been laser focused as of late on using this scale to drive efficiencies and lower cost of service. The stated goal is to drive $600-800 million is savings over the next five years using benchmarking, shared services, and analytics.

HCA Scale And Efficiency (HCA Investor Relations)

On the other side of the equation, HCA is facing the downside from three key headwinds: staffing challenges, squeezed profit pools, and regulatory pressure.

Staffing challenges were a major topic of discussion during the earnings call after challenges with professional services fees earlier in the year. While HCA has staffing under control at the moment, the availability of skilled nursing and physician candidates is expected to continue declining. According to a recent report from the American Hospital Association, there will be over 3 million vacant healthcare roles by 2026. And lower supply with consistent demand equals higher cost of labor.

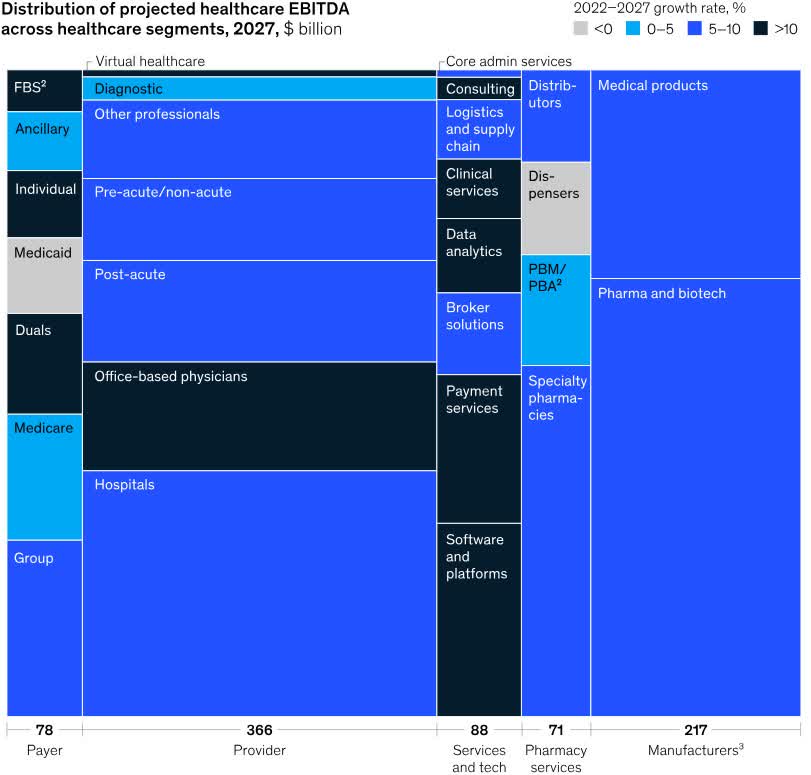

Squeezed profit pools will also challenge profitability. McKinsey expects the most rapid growth over the next few years to come from physician offices and medical technology, neither of which is core to HCA's business. In a surprise twist, Medicare is also expected to slow relative to previous analysis and HCA has been pursuing this business.

Healthcare Profit Pool (Seeking Alpha)

Lastly, regulatory pressures continue to mount on consolidated healthcare companies. HCA is facing a major lawsuit related to antitrust violations, and a court has said they must go to trial. Pharmacy benefit managers are wary of potential legislation that may significantly reduce their profits. Pricing transparency laws, along with the No Surprises Act, have squeezed hospital profits, even causing the joint venture challenges faced by HCA.

HCA Healthcare has had a fantastic run, up more than 32% over the last year. This price increase is well deserved, given solid margin growth and healthy cash flow. That said, this is a great stock to own but not a great stock to buy.

Multiple valuation methods signal that the stock is fairly valued, with my DCF-generated price target of $312 within the margin of safety. Wall Street and Quant ratings concur with a fairly valued stock.

In addition, risk and reward are balanced as an aggressive (and so far well executed) growth strategy and cost containment effort are balanced against industry headwinds on several fronts.

With all of the above in mind, I lower my rating from buy to hold as I believe HCA Healthcare is fairly valued at the current price.