popovaphoto/iStock via Getty Images

popovaphoto/iStock via Getty Images

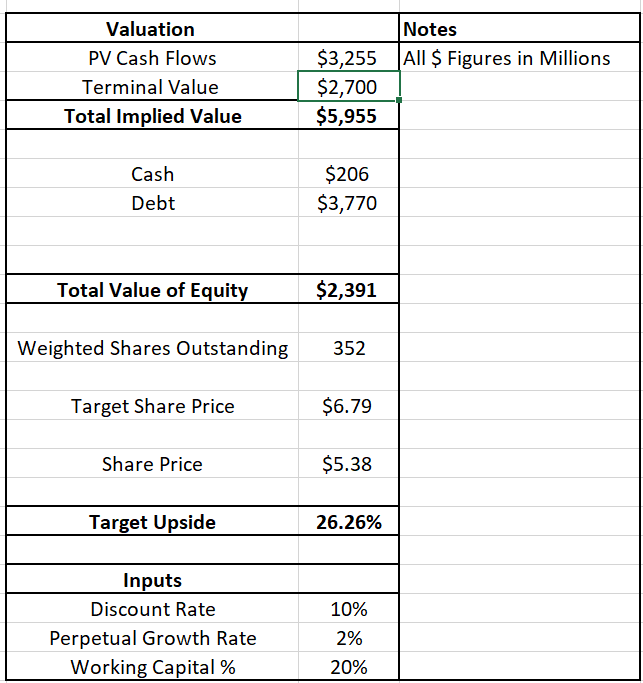

I am placing a BUY rating on Hanesbrands Inc. (NYSE:HBI) primarily because it is looking evermore likely that HBI might turn around the business operations of its Champion brand due to a rather expensive "Champion performance enhancement plan". If HBI can successfully turn Champion around and stop spending hundreds of millions of dollars in a revitalization program for the brand it would likely steer HBI into profitability. Hanes gave a time frame of 2024's fall/winter season to begin to see the full results of this turn around. If Hanes can pull this off and get the company back on track to just a 2.0% year over year revenue growth I believe you would be looking at a value per share of approximately $6.79.

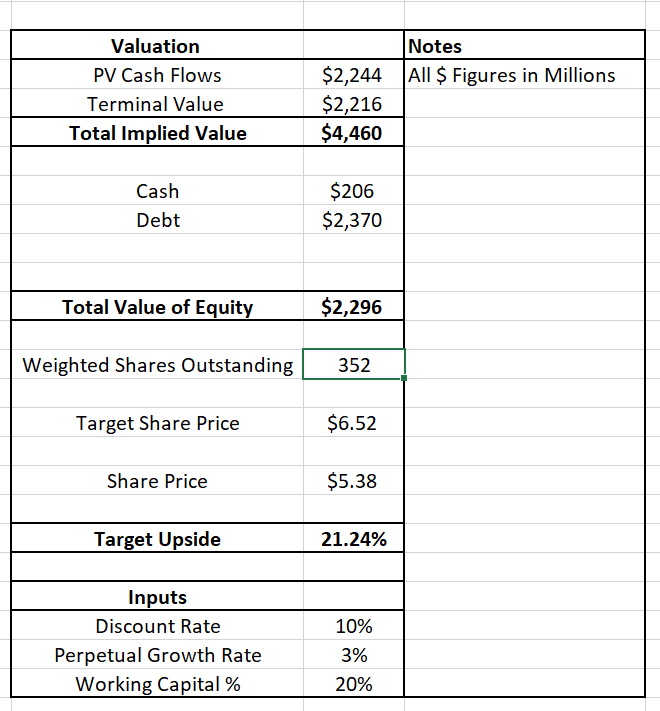

Management has also announced it is looking into the possibility of selling off the brand entirely so it can pay down debt. In this scenario I think that HBI's share price may be worth $6.52 at least.

Hanes was founded in 1901 and is headquartered in Winston-Salem, North Carolina. I doubt you'll be able to find many American's who don't know this iconic American clothing brand. Some Hanesbrands products that probably come to mind when you mention the company to the average American are underwear, socks, plain T shirts, and maybe innerwear tank tops. The company offers many more products other than this however and also owns brands such as Playtex, Bras N Things, Wonderbra, Maidenform, JMS Just My Size, Champion, and has a license agreement with Polo Ralph Lauren.

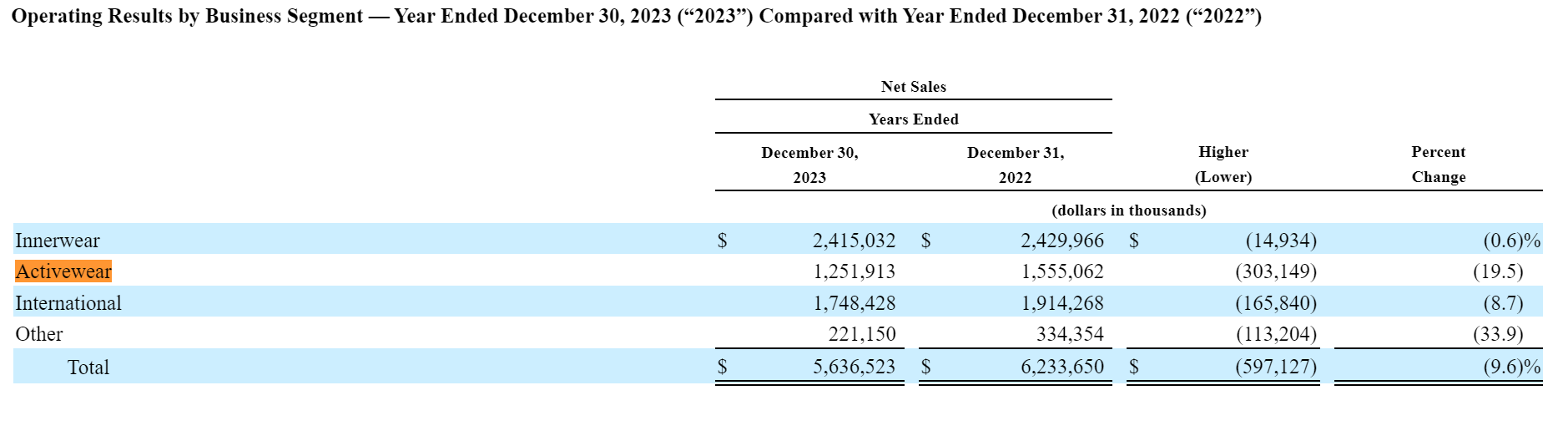

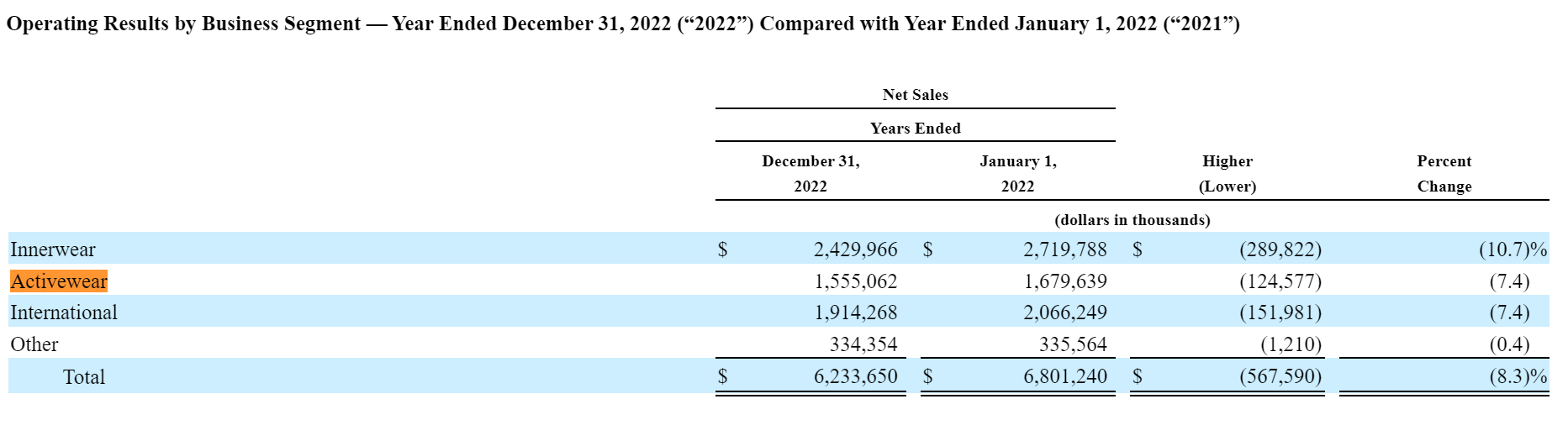

Champion saw a 23% decline in net sales in HBI's most recent quarter and HBI's activewear category, of which Champion plays a very large role in, saw a 19.5% decrease in net sales in 2023. In 2022 HBI saw its activewear segment take a 7% decrease in net sales.

HBI's Operating Results By Business Segment 2023 (HBI's 2023 10-K) HBI's Operating Results By Business Segment 2022 (HBI's 2022 10-K)

In an attempt to revitalize Champion Hanes has and continues to inject a lot of capital into the brand. In HBI's most recent earning's call CEO Stephen Bratspies has noted that Hanes continues to "aggressively implement our Champion performance enhancement plan to strengthen the brand and position Champion for long-term profitable growth." Bratspies also noted that the large decrease in net sales earnings was due to HBI's performance enhancement plan and that he expects these downward pressures on Champion's net sales figures to extend into Q1 of 2024.

In order to implement this performance plan for Champion Hanes has spent a considerable amount of money. $60 million was spent in 2022 and $116 million in 2023 for a total of $176 million spent thus far to revive Champion. Hanes said in its 2023 10-K that it intends to spend another $70 million in 2024 to continue their Champion enhancement plan.

All of that adds up to $246 million that Hanes has said it plans to spend on reviving Champion. On HBI's most recent earnings call management did sound excited about introducing Champion's fall/winter line-up and hopefully that begins an important inflection point with the brand. Even after injecting this much money into Champion however, management is currently leaving the door open on a potential sale of the brand.

Hanes hired help of Goldman Sachs & Co. and Evercore to look at "strategic alternatives" for the company's Champion brand. These alternatives include the possibility of selling off the company and using the proceeds to pay off debt. Hanes actually set its deadline for its first round of bids to end this past February. Authentic Brands Group and G-III are among the companies that have shown interest in potentially buying Champion. Hanes is rumored to have set the minimum bid at $1.4 billion and could likely receive more should management decide to sell.

Hanes managed pay off $500 million in debt last year. This year they forecast another $300 million or more in debt paydowns. This $1.4 billion could easily help Hanes take another large chunk out of its $3.77 billion in outstanding debt which would in turn help Hanes bring down its annual interest expenses which in 2023 reached $278 million.

I ran several growth model discounted cash flow analysis scenarios for HBI in an attempt to figure out what the company's finances would look like if they made a recovery back towards a modest revenue growth. For every DCF scenario I assumed a 10% weighted average cost of capital and a 20% working capital as a percentage of revenue figure. On all DCFs I assumed that in 2024 HBI would first see a further 2.9% decrease in their revenue (the average drop in revenue from 2019-2023). Afterwards I have HBI's revenue growing at a modest rate of between 2.0% and 3.0% depending on the specific DCF model. I also assumed HBI's EBIT margins would make a modest recovery to 10% of revenues. This EBIT margin is likely lower than it would be once HBI becomes profitable again as their historic pre 2021 EBIT margins hovered around 13% year after year.

When running my first DCF under these assumptions I got an 26% upside to the current stock price of $5.38 per share for a price target of $6.97 per share. This DCF assumes Hanes holds onto its Champion brand and that through its revitalization program it is able to steer the company back to a modest 2.0% revenue growth rate. This also assumes HBI continues to pay an effective corporate tax rate of 10%.

HBI Discounted Cash Flow If HBI Keeps Its Champion Brand And Returns Revenue Growth Around To A 2% Growth Rate (Leland Roach)

Other distressed retailers such as Reebok have sold off in recent years at approximately 1X sales. Unfortunately HBI leaves us in the dark on just exactly how much of its revenue comes from its Champion brand because it only reports its revenues for three segments innerwear, activewear, and international but doesn't give many individual details for specific brands. Unfortunately we are left to assume revenues are at 1X of HBI's starting bid for Champion and therefore assume that Champion's predicted sales are to be around $1.4 billion. If we subtract that $1.4 billion from HBI's future revenues and use the cash from the sale to pay down HBI's $3.77 billion in debt HBI is left with $2.37 billion worth of debt. Freeing themselves of Champion and not having to continue to pour money into a struggling brand would also improve Champion's revenue growth therefore I boosted HBI's revenue growth to a steady 3.0% rate. The sale of Champion may also increase HBI's effective tax rate as they may lose large tax write offs from losses associated with Champion and therefore I assumed Hanes would have to pay a normal 21% tax rate after it sells off Champion and returns itself back to profitability.

HBI Discounted Cash Flow If HBI sells Champion And Returns Revenue Growth Around To A 3% Growth Rate (Leland Roach)

Under my assumptions HBI's target price actually decreases after selling off Champion to $6.52 per share compared to our previous DCF but still offers an ample upside of 21%. One thing I must mention about my DCF is that selling off Champion would allow HBI to use more of its free cash flow to pay down its existing debt at an increased rate as it would no longer have to fork out as much cash on interest payments or put cash towards its Champion revitalization plan. This alone could further increase the future upside HBI is likely to experience if they successfully sell Champion.

By far the biggest risks HBI faces is that it may be unable to sell Champion or unable to steer the company into profitability. If Champion continues to bleed money despite having hundreds of millions of dollars pumped into it then HBI's stock price would likely retreat back down to the low $4.00 range or even further. This recent excitement in the market is predominantly made up of investors excited about the prospects of Hanes ditching a troubled brand that has dragged down earnings and the stock price since 2021. If those investors see Champion's prospects of turning a new leaf or being sold off to someone dwindle then I would fully expect them to exit their positions.

I think that Hanesbrands Inc. is a BUY. This buy rating is predicated specifically on HBI's ability to either sell off its troubled Champion brand or to complete its "Champion performance enhancement plan". If Hanes fails to do either of these things the stock price will likely fall back down into the low $4.00 range. If HBI is able to successfully sell off Champion and achieve a 3.0% revenue growth starting in 2025 I think the fair value of the stock will be $6.52 a share. If HBI instead is able to turn around its Champion brand and generate a modest 2.0% revenue growth rate I believe the value of the stock to be $6.79 a share. This stock is a bit riskier than I would normally be comfortable with but I think that the very modest turn around HBI has to achieve should be doable.