Hamilton Beach Brands Holding (NYSE:HBB) Could Be Struggling To Allocate Capital

If you're not sure where to start when looking for the next multi-bagger, there are a few key trends you should keep an eye out for. Ideally, a business will show two trends; firstly a growing return on capital employed (ROCE) and secondly, an increasing amount of capital employed. Put simply, these types of businesses are compounding machines, meaning they are continually reinvesting their earnings at ever-higher rates of return. Having said that, from a first glance at Hamilton Beach Brands Holding (NYSE:HBB) we aren't jumping out of our chairs at how returns are trending, but let's have a deeper look.

Understanding Return On Capital Employed (ROCE)

For those who don't know, ROCE is a measure of a company's yearly pre-tax profit (its return), relative to the capital employed in the business. To calculate this metric for Hamilton Beach Brands Holding, this is the formula:

Return on Capital Employed = Earnings Before Interest and Tax (EBIT) ÷ (Total Assets - Current Liabilities)

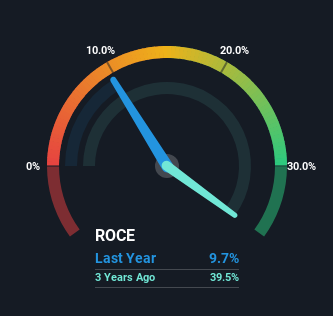

0.097 = US$22m ÷ (US$379m - US$152m) (Based on the trailing twelve months to September 2023).

So, Hamilton Beach Brands Holding has an ROCE of 9.7%. In absolute terms, that's a low return and it also under-performs the Consumer Durables industry average of 15%.

Check out our latest analysis for Hamilton Beach Brands Holding

While the past is not representative of the future, it can be helpful to know how a company has performed historically, which is why we have this chart above. If you're interested in investigating Hamilton Beach Brands Holding's past further, check out this free graph covering Hamilton Beach Brands Holding's past earnings, revenue and cash flow.

How Are Returns Trending?

When we looked at the ROCE trend at Hamilton Beach Brands Holding, we didn't gain much confidence. Around five years ago the returns on capital were 41%, but since then they've fallen to 9.7%. Meanwhile, the business is utilizing more capital but this hasn't moved the needle much in terms of sales in the past 12 months, so this could reflect longer term investments. It's worth keeping an eye on the company's earnings from here on to see if these investments do end up contributing to the bottom line.

On a related note, Hamilton Beach Brands Holding has decreased its current liabilities to 40% of total assets. That could partly explain why the ROCE has dropped. Effectively this means their suppliers or short-term creditors are funding less of the business, which reduces some elements of risk. Since the business is basically funding more of its operations with it's own money, you could argue this has made the business less efficient at generating ROCE. Keep in mind 40% is still pretty high, so those risks are still somewhat prevalent.