RiverNorthPhotography/iStock Unreleased via Getty Images

RiverNorthPhotography/iStock Unreleased via Getty Images

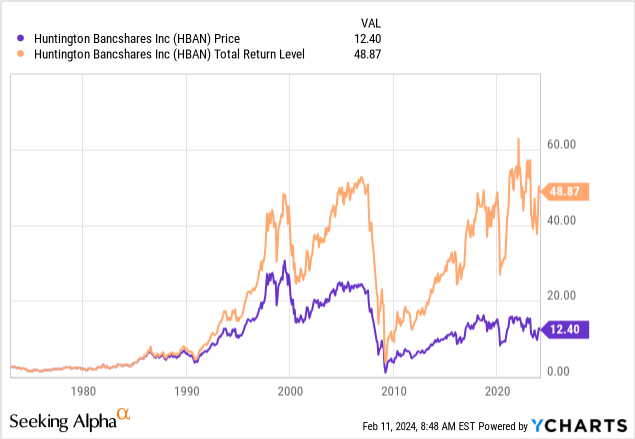

A year after the US banking system was shaken by bank failures that were compared to the collapse of Lehman Brothers, the GFC that that caused was averted this time, despite the FOMC inflation fight resulting in more rate increases. Last fall, just as "higher for longer " was losing steam, I wrote Huntington Bancshares: Evaluating Its Available Preferred Stocks, which reviewed the three preferred offered by this Ohio-based bank. The timing couldn't have been better as preferreds bottomed about then.

With the FOMC tossing water on the idea they would start cutting rates in March, prices have retreated from recent peaks. Here, I focus on the Huntington Bancshares Incorporated 6.875% DEP PFD J (NASDAQ:HBANL), the one with the best coupon and longest Call protection. Compared to other HBAN preferreds and a competing major bank's floating preferred stock, I find HBANL is attractively priced, thus I would give HBANL a Buy rating, though with a high expectation it could be Called in 2028.

Seeking Alpha describes this bank as:

Huntington Bancshares Incorporated operates as the bank holding company for The Huntington National Bank that provides commercial, consumer, and mortgage banking services in the United States. The company operates through four segments: Consumer and Business Banking; Commercial Banking; Vehicle Finance; and Regional Banking and The Huntington Private Client Group (RBHPCG). Huntington Bancshares Incorporated was founded in 1866 and is headquartered in Columbus, Ohio.

Source: seekingalpha.com HBAN

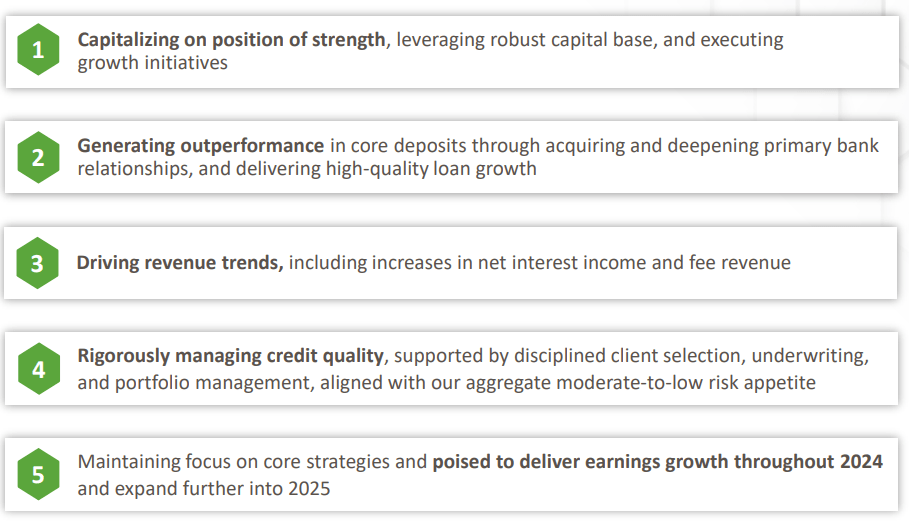

The recently released 4Q-23 earnings presentation opened with the following slide which highlights how the bank defines its mission.

d1io3yog0oux5.cloudfront.net 4Q23 PDF

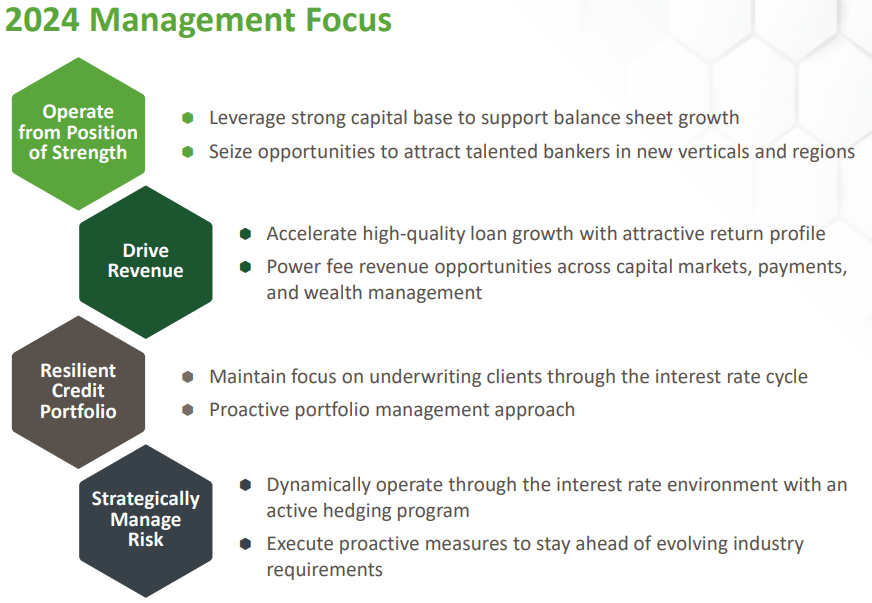

That was followed by what the bank's goals and strategies are for this year.

d1io3yog0oux5.cloudfront.net 4Q23 PDF

I read a key objective from the first listed point to be expanding their footprint in this challenging time for mid-size banks. The second point, that while expanding is a goal, maintaining high-quality loan standards will stay in place. Key points listed in the presentation included:

In reviewing the Income and Balance Sheets, the key point in each was:

There are potential clouds not only for HBAN, but all banks; two being:

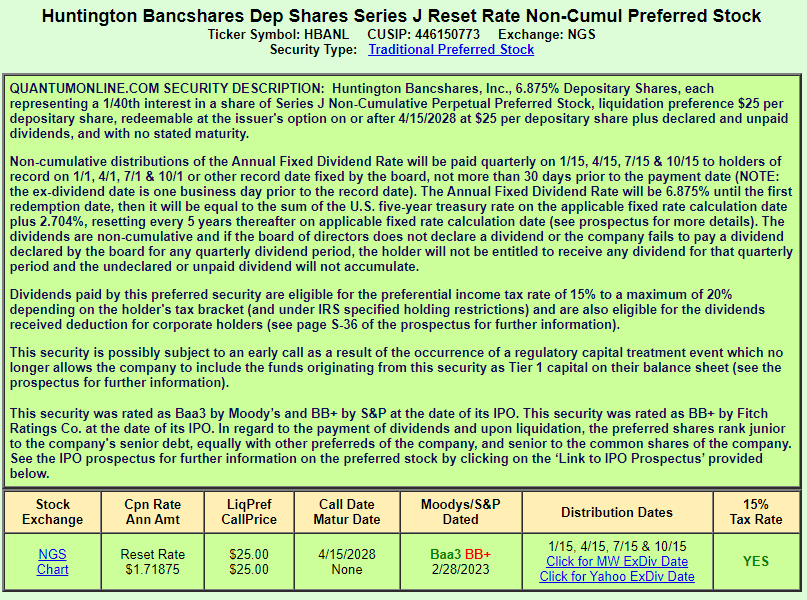

seekingalpha.com HBANL homepage QuantumOnline.com

Important features of HBANL include:

The current yield is 7.04%, compared to 6.25% for Huntington Bancshares Incorporated 5.7% DP SH PFD I (HBANM) or 5.93% for Huntington Bancshares Incorporated 4.500% DEP PFD H (HBANP). HBANL provides the longest Call protection with two years over HBANP; HBANM is already Callable. The low fixed coupon on both of the other preferreds, in my view, would make HBANL more likely to be Called if the 5-Yr UST Note rate is above 3% at that time. HBAN has shown an ability to replace existing preferreds with a lower yielding one. From what I see, HBANL is the first time that HBAN issued a preferred stock with a floating, not fixed rate. I read its higher current yield as a sign that investors think HBANL will be Called and want compensation for the reinvestment risk they are accepting.

There are several comparisons investors can make in deciding if HBANL belongs in their portfolio. First is comparing HBANL's yield to a CD that matures near HBANL's Call date. The extra yield comes to about 3%, or a bonus rate of 70% over the risk-free CD. If Called, investors in HBANL get a higher 7.55% return. Compared to its sister preferred stocks, HBANL provides between 70 to 111bps in extra yield. A slightly higher rated bank floating-rate preferred stock is the MS.PR.A Morgan Stanley PFD A (MS.PR.A), which is yielding about the same as HBANL. The MS issue uses a much less generous floating formula. Translation, HBANL is attractively priced, thus I would give HBANL a Buy rating, with a high expectation it could be Called.