deepblue4you

deepblue4you

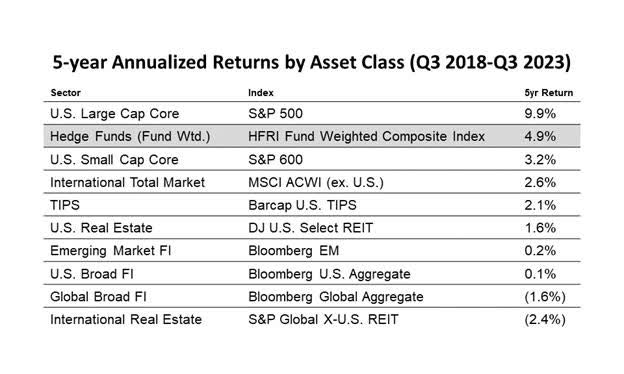

Relative performance of the hedge fund industry has dominated a majority of asset classes over the past 5 years, marking one of the strongest stretches in the history of the industry.

Seen below, the HFRI Fund Weighted Composite Index has outperformed most liquid assets with the exception of the S&P 500. However, this performance has been concentrated in a small number of stocks and most large-cap US active equity investors have significantly underperformed the broader index.

Unlike top endowment funds, which have had significant allocations to hedge funds for decades, most public pension funds did not begin developing direct hedge fund allocations until well after the 2008 financial crisis.

Since then, many of the most sophisticated pension funds have established diversified, uncorrelated asset allocations, primarily funded by reallocating away from fixed income with a goal to enhance overall returns and reduce volatility.

In the past five years, hedge fund indices have not only outperformed fixed income, but have also avoided the extreme declines seen in long-duration fixed income investments.

Hedge fund indices often under-report the performance of the industry because calculations include "full fee" share class performance. This does not take into consideration the vast majority of managers who give fee discounts to large investors.

For example, large institutional investors committing over $100 million to a manager can often receive discounted fees typically ranging from 50 to 100 basis points less than standard fees, which increase their net return.

Hedge fund fee structures have evolved over the years in order to attract and retain large institutional investors. Most managers have adopted one of the 2 structures below:

There is significant potential for increased performance for investors who can identify strategies that will outperform or select top-tier managers within a specific strategy.

Hedge Fund Indices encompass a wide range of strategies, and the Hedge Fund Research (HFR) database tracks over 5,000 funds.

Agecroft Partners estimates that approximately 85% to 90% of these funds may not be of high quality. By focusing on the top 10% to 15% of the highest-quality funds, which are not always the largest managers, investors can aim for significantly higher returns than those provided by the broader index.

A significant challenge in the hedge fund industry arises from the tendency of less sophisticated investors predominantly investing in the most prominent fund managers.

This preference is often driven by the allure of established brand names, endorsements from other institutional investors, and the fame of the portfolio manager.

Regrettably, this excessive concentration of capital within the largest funds leads to their assets growing beyond the point where optimal returns can be achieved for their investors.

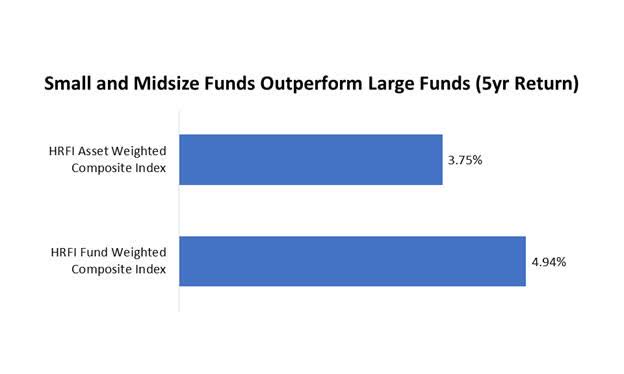

As these funds expand, their ability to enhance performance through security selection diminishes, resulting in declining returns. For example, there are 2 ways to calculate the performance of the HFRI index:

Over the past 5 years, smaller funds have significantly outperformed larger funds as demonstrated by the HFRI Fund weighted composite that was up 4.9% vs. the HFRI dollar weighted composite that was up only 3.8%. Small and mid-sized managers have a distinct advantage in generating returns through security selection, especially in less efficient markets.

Hedge fund absolute returns should improve going forward for 2 reasons:

Original Source: Author

Editor's Note: The summary bullets for this article were chosen by Seeking Alpha editors.