cherdchai chawienghong/iStock via Getty Images

cherdchai chawienghong/iStock via Getty Images

GitLab Inc., (NASDAQ:GTLB), the Dev Ops pioneer, offers a streamlined Development Operations platform for software engineers or developers, where quality assurance and operations work together, ensuring both quality and timely delivery. This is an essential utility and backbone for any software or platform development, especially in a fully connected world, far away from the legacy approach of a) a developer team storing code in one program, b) quality assurance engineers using a second to track bugs and c) A third program to put it all together.

As the cobbler putting it all together, it has saved customers the cost and pain points of dealing with several vendors since it started 10 years ago.

I've highlighted a few large competitors such as Microsoft's (MSFT) GitHub and Amazon (AMZN) AWS's Cloud Platform below. The list, among others, includes Atlassian's (TEAM) Jira - there is no shortage of alternatives and competitors ranging close to each other.

GitLab competitors (Gartner)

GitHub is owned by Microsoft, bought over for $7.5Bn in 2018 and has been GitLab's closest competitor since the beginning. The language Git emanates from open-source GIT, started by Linus Torvalds. Like all its products, Microsoft has the advantage of bundling, and discounting, which can hurt GitLab.

Why buy GitLab then in a crowded field with two 800-pound gorillas?

Let's take a deep dive.

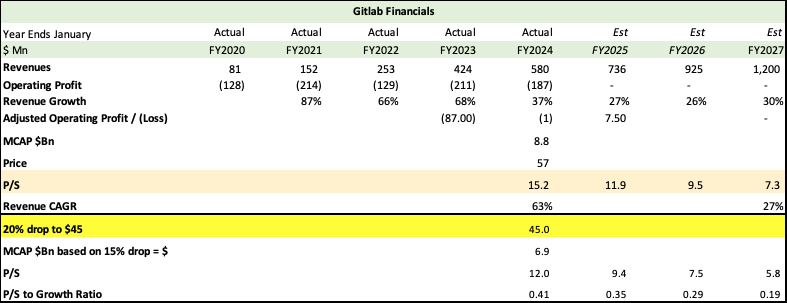

In the last 4 years, GitLab grew revenue at a frenetic pace of 63% from $81Mn to $580Mn. However, growth slowed down to 37% this year with management guiding to 27% in FY25 and consensus analyst estimates forecasting 26% and 30% in FY2026 and FY2027, for a 3-year CAGR of 27%. This is still very healthy growth, especially as GitLab focuses on larger customers with longer and more difficult sales cycles.

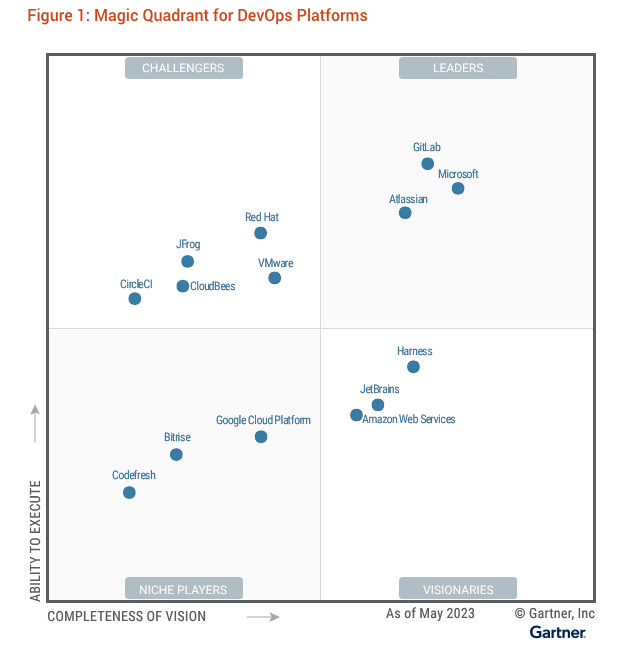

GitLab prides itself as the most comprehensive platform with a wide array of tools for security and compliance such as dynamic scanning, container scanning, API security and compliance management, which then gives them a leg up in getting more artificial intelligence or AI from their platform. No surprise that Gartner placed GitLab at the top as a leader for DevOps platforms, along with GitHub and Atlassian.

As CEO, Sid Sijbrandij stated on their Q4-FY2024 earnings call, emphasis mine.

I think us and GitHub are the only true platforms today where it's a single application, single code base, single data store. And the big advantage of that is you get a faster cycle time. You don't have to switch applications. You can do very intelligent things with AI, for example. We wouldn't have been able to add so many AI functions, the most in the market, if it was across different applications. We have the broadest platform, because the more point solutions our customers can replace, the more they save on licensing, the more they save on integration costs. The better they can up their compliance, the more efficient they get.

We're talking to a CSO and it compares to GitHub, they see we can do a lot of things that they need and that GitHub can't do. GitHub doesn't have dynamic scanning. GitHub doesn't have API security. GitHub doesn't have fuzz testing. Even better, we can prove that they are compliant. With GitLab, they can tag every project, note the security framework, say what that security framework consists of and prove that. The auditors can walk in, point to any environment, and they have the reports ready. We're unique in that capability.

DevOps Magic Quadrant (Gartner)

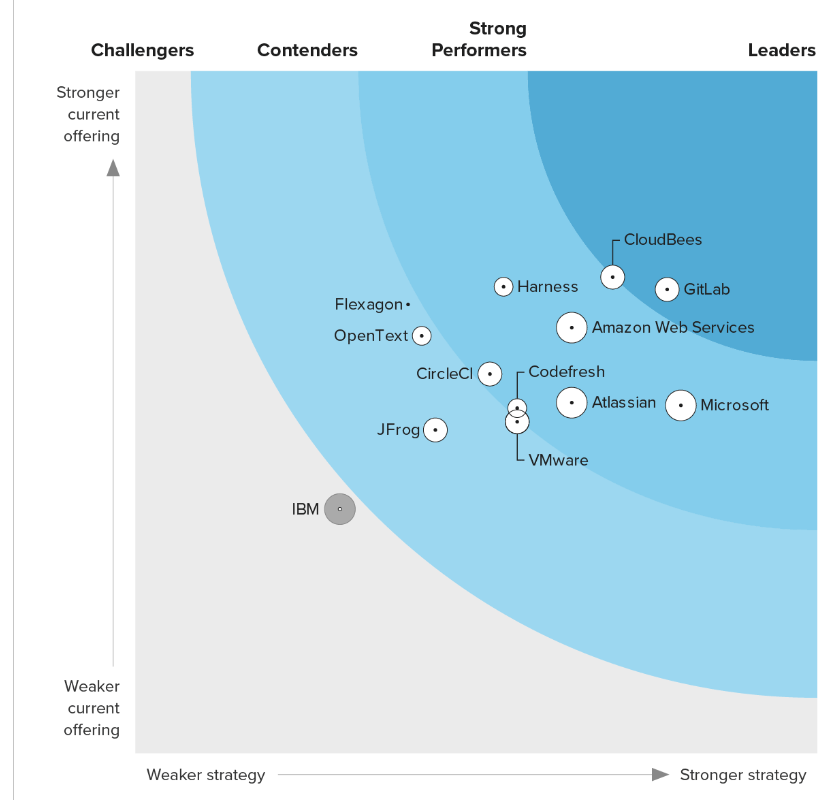

Forrester too seems to love GitLab, naming it as having a stronger current offering than Amazon and Microsoft.

Forrester Integrated Delivery Platform (Forrester)

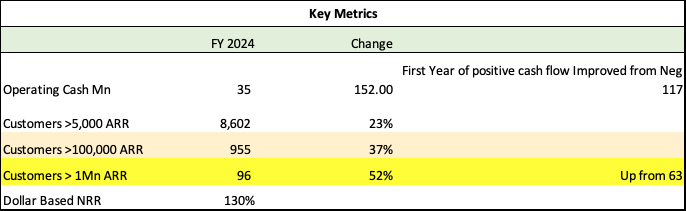

For Q4-FY2024, GitLab had an excellent Dollar based net retention rate or NRR of 130%, indicating a larger wallet share of customers, a solid rate for a SaaS / licensing company.

For Q4-FY2024 it had adjusted gross profit margins of almost 90% even with a SaaS component of 25% of revenues, which has lower margins than licensing revenue. This led to the first year of positive cash flow with $35Mn in operating cash, improving $152Mn from negative $117Mn.

As we can see below, it had strong growth in the top tiers with customers over $1Mn in ARR growing 52% and customers over $100,000 in ARR improving 37%.

GitLab Metrics (Seeking Alpha, GitLab)

Stronger offerings led to better pricing for GitLab, with GitLab Ultimate, their most expensive offering, becoming the fastest growing across the company, and now represents about 44% of the total ARR. And even though it was the highest priced, customers bought it because of improved cycle times leading to a better ROI for their clients.

GitLab has positioned itself as a DevSecOps player and is firmly increasing its share of compliance and security features within the Dev Ops platform with security features like dynamic scanning, fuzz testing, API testing and, providing certification for auditors, again circumventing the need to look for other software programs just for security. For example, T-Mobile recently moved 25,000 projects into GitLab in two months and increased their security scans to hundreds of thousands per month - using GitLab's integrated solution to reduce friction and fix vulnerabilities that would have arisen with two different solutions. As another example, one of their clients, CACI, found it easier to comply with federal regulation working in their integrated and agile environment.

GitLab is also offering a single tenant cloud environment via GitLab Dedicated for clients that need one for security, residency, and compliance regulation, and acquired a seven-figure deal from a US airline in Q4.

I believe providing security and compliance within the DevOps platform is and will become an even bigger competitive advantage as will the single tenant offering. They're the only DevOps platform that offers the single tenant SaaS right now with the first mover advantage. They've also seen growth from customers replacing point solutions like Checkmarx, Snyk, Veracode and Black Duck.

GitLab is also seeing growth and promise from their planning offering, Enterprise Agile Planning, which lets customers bring software planning into the DevOps platform, and they've seen customers switching from Atlassian's Jira. Having a planning component integrated into DevOps reduces the need for planning tooling and software creation tooling.

Another big opportunity is using its large platform to build and charge for AI capabilities, and they're charging $19 per month per user for GitLab Duo Pro. This integrates AI throughout the software development life cycle, which allows them to explain and address vulnerabilities all throughout and improve engineering productivity. The Duo Pro offering, according to an Omidia report, had the best AI features in the market. They had 38 out of the 43 areas where you could provide AI features in the DevOps platform, the best coverage amongst their competitors.

Along with Ultimate, GitLab can get a larger security and AI wallet share by adding value, which would further lead to brand loyalty. This is a virtuous cycle of the broadest platform, providing the best data for AI solutions, further increasing the reach of the platform. In addition to code generation, AI also helps with other work streams in addressing use cases, summarizing issues

According to CEO Sid Sijbrandij from an investors conference, the total market size for DevOps platforms is estimated to be a $40 billion revenue a year market, with GitLab and GitHub together comprising less than 5% of the market.

Given the necessity of having a DevSecOps platform for software build outs, growth shouldn't be a problem for GitLab at all, especially if the AI market is going to grow at 16% through 2030.

Management on its Q4-FY2024 earnings call spoke a lot about normalization of customer behavior, indicating that they're seeing trends they saw 6 quarters back when growth was at its peak, they've seen reduced churn and tremendous customer interest in products not being offered by competitors.

Microsoft offers a similar product, a small fraction of their entire product line, which they can easily bundle or discount to GitLab' detriment. While GitLab has competitive advantages of best features, and a broad array of products there is no single moat to fend off the likes of Microsoft and Amazon, which as hyperscalers and CSP's can easily bundle their DevOps platform with other products.

Over 70% of the business is still licensing and not SaaS, which while enjoys greater margins, does precious little to Land and Expand, increase Net Retention Rates or increase adoption, upselling of other modules, and then you have worry about customers dropping seats, leading to more uneven revenue instead of steadier larger multi year contracts with greater chances of upselling.

The current price of $57, equates to 12x FY 2025 sales. With a growth rate of 27% it is too rich for a company that has little visibility towards cash flow or adjusted operating profits. Management has guided to only $7.5Mn in FY2025 adjusted operating profits. Given that GitLab is getting more revenue from large clients, a single quarter with a revenue miss could easily chop off 10 % of its price as it did post Q4-earnings.

GitLab Revenue Growth (GitLab, Seeking Alpha, Fountainhead)

As we can see from the table above, this is still only a revenue story with 27% YoY growth. Management has guided to about 26% growth in revenues for FY2025, and even with that they expect adjusted operating profits to be only $7.5Mn, a very minuscule margin.

The normalization of customer behavior, price tailwinds, lowering of churn and acceptance of new products for compliance, security, and AI, should be bigger factors for FY2026 than FY2025, as management suggested, providing it good growth momentum for the next 2-3 years.

GitLab has a lot of good things going for it:

Best in class products and industry recognition from Gartner and Forrester.

A large TAM with low penetration.

Emphasis on growth markets such as security.

Excellent Net Retention Rates and lower churn.

Growth with large clients.

GitLab has dropped over 20% from its 52 week high of $78, but given the lack of visibility of even adjusted operating profits, I would still like to wait for a price of $45, or another 20% drop to buy. Till then it's a show me story and not enough margin of safety to counter the risks of competition from Microsoft and the lack of a moat.

At the current price of $57, this equates to 12x sales, which is too expensive especially in the absence of adjusted profits or even a decent cash flow margin. I ran the same exercise with a price of $45, resulting in a much better 9X FY25 sales, which is a P/S growth ratio of 0.35.

My usual benchmark is 0.33. At $45 I'm a buyer, till then it's a hold.