FatCamera

FatCamera

G1 Therapeutics, Inc. (NASDAQ:GTHX) is a commercial-stage biopharmaceutical company specializing in developing and commercializing advanced oncology treatments. Its flagship product, Cosela (Trilaciclib), is an FDA-approved drug for reducing chemotherapy side effects like myelosuppression in patients with Extensive-Stage Small Cell Lung Cancer (ES-SCLC), an aggressive form of lung cancer. Furthermore, the company has a research pipeline exploring new Trilaciclib indications, such as solid tumors in breast and bladder cancer. GTHX reported a 29% increase in Cosela's net revenues in Q4 2023, and it remains well-positioned for continued growth as clinical trials continue. Hence, despite inherent dilution and cash burn risks, I consider GHTX a good speculative “buy” in oncology biotech.

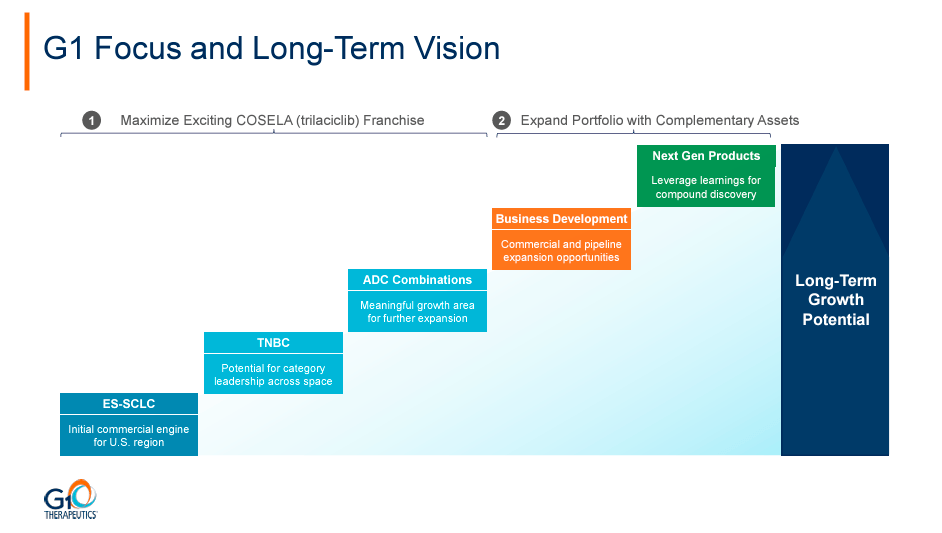

G1 Therapeutics is a commercial-stage biopharmaceutical company based in Research Triangle Park, North Carolina, primarily focused on developing next-gen cancer therapies. GTHX was founded in 2008, and its leading product today is Trilaciclib, a first-in-class treatment for certain types of cancers. GTHX’s Trilaciclib IP is currently commercialized under COSELA and is the company’s main revenue contributor. Moreover, Trilaciclib is also undergoing further clinical trials to expand its potential use cases into breast and bladder oncology applications. Today, GTHX is a bet on the Trilaciclib IP and its future development.

Source: GTHX’s website.

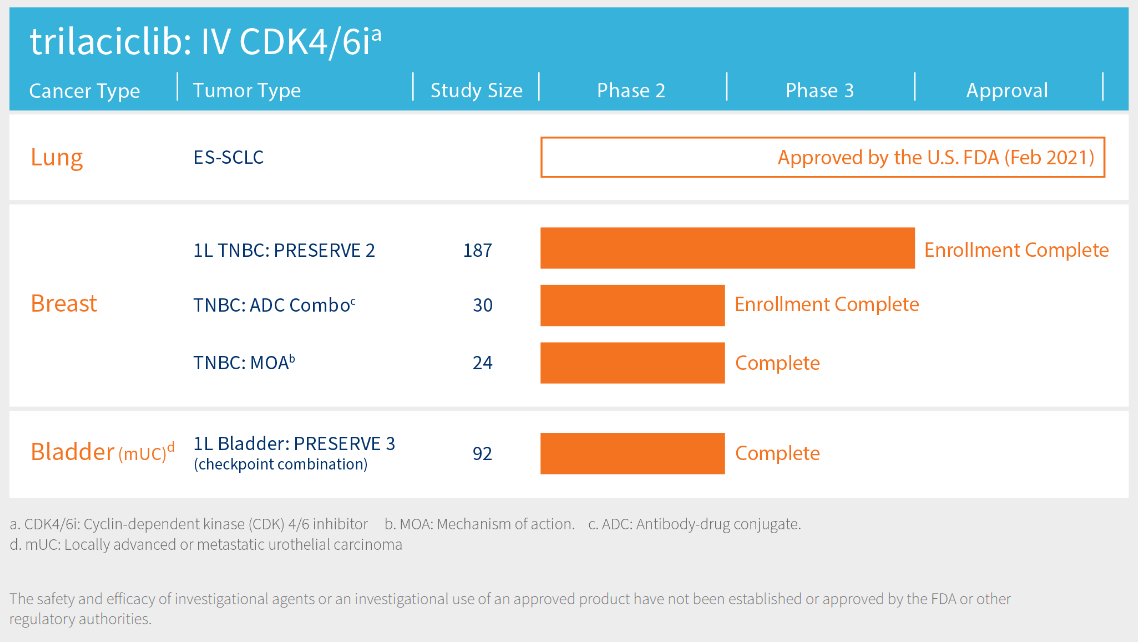

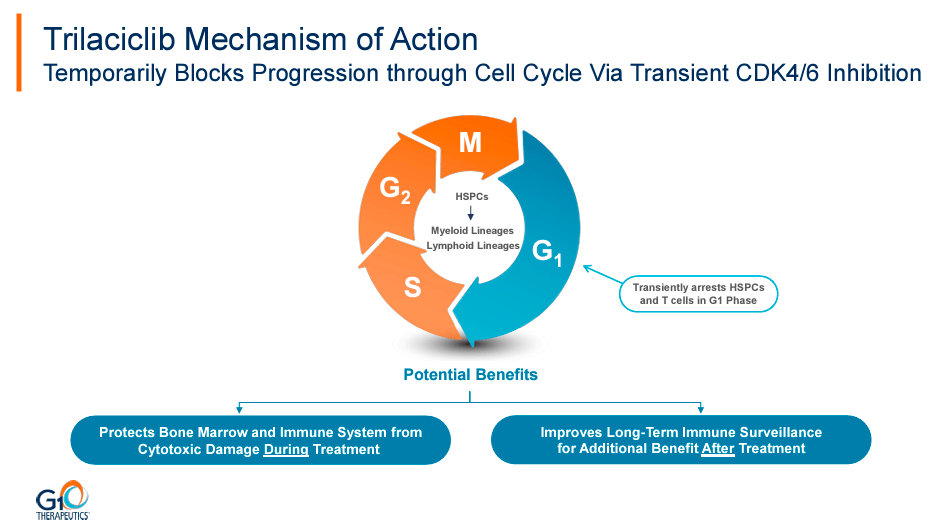

Thus, essentially, GTHX’s main commercial product is Cosela (Trilaciclib for injection), which is indicated for chemotherapy against lung cancer. The interesting part about Cosela is that it protects the bone marrow against the effects of chemotherapy, decreasing the incidence of myelosuppression. Myelosuppression is a concerning side effect of traditional chemotherapy treatments and reduces blood cell production, increasing the risk of infection, anemia, and bleeding. The FDA approved GTHX’s Trilaciclib for a specific type of lung cancer called Extensive-Stage Small Cell Lung Cancer [ES-SCLC] in February 2021. ES-SCLC is a particularly aggressive lung cancer where the malignant cells spread extensively within the chest or to other body parts.

Moreover, GTHX's research pipeline contains new Trilaciclib applications targeting solid breast and bladder cancer tumors. There are three different study types for breast cancer: 1) first-line triple-negative breast cancer [TNBC], with the study PRESERVE 2 in phase 3 of the clinical trials; 2) triple-negative breast cancer: antibody-drug conjugate combination [TNBC: ADC Combo], which is in phase 2; 3) triple-negative breast cancer: mechanism of action [TNBC: MOA] also in phase 2. For context, TNBC is a type of cancer denoted by the absence of the following three common receptors that fuel most breast cancer growth: estrogen receptors [ER], progesterone receptors [PR], and human epidermal growth factor receptor 2 [HER2]. Treating TNBC is challenging because it does not respond well to hormonal or HER2-targeted drugs, and it has a higher likelihood of spreading and recurrence.

Source: February 2024 Corporate Presentation.

Consequently, GTHX’s first-line denomination implies a clinical trial where patients receive their initial cancer treatment. The antibody-drug conjugate is a targeted cancer therapy that combines an antibody specific to cancer cells with a delivery instrument to bring a cytotoxic drug directly to cancer cells. Hence, GTHX’s study on TNBC is MOA and aims to uncover how Trilaciclib’s immune mechanism acts in the tumor microenvironment. So far, GTHX’s clinical trials on this potential application of Trilaciclib show the beneficial effect of a single dose to enhance antitumor immune response.

Additionally, Trilaciclib’s potential application for locally advanced or metastatic urothelial carcinoma, a type of bladder cancer [mUC], is also promising. GTHX is conducting its Preserve 3 study, a completed phase 2 clinical trial involving first-line treatment patients. Early clinical trial data in this signal-finding study suggest improved survival odds for patients using Trilaciclib plus an immune checkpoint inhibitor such as Avelumab. Immune checkpoint inhibitors help the immune system recognize and attack cancer cells, so in conjunction with Trilaciclib, it could potentially lead to significantly better results than other standalone therapies.

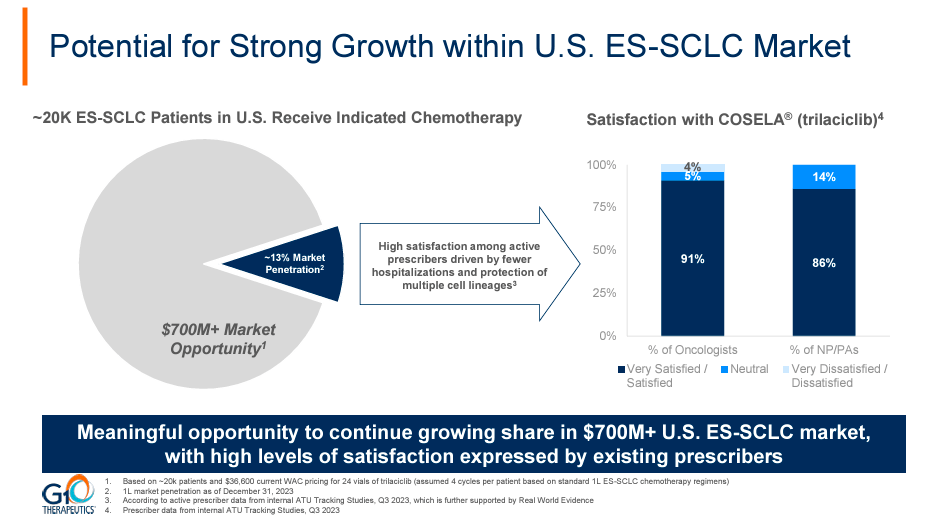

It’s also worth noting that GTHX’s latest earnings call in February 2024 discussed the company's Q4 2023 and full-year 2023 company’s performance, where executives provided an update on Cosela's commercial progress, reporting significant volume sales growth with a 29% increment in revenue in Q4 2023. These results underscore the importance of Cosela for GTHX’s business model and financing. Indeed, Cosela’s value lies in reducing chemotherapy's negative effects, which is undoubtedly vital for patients' lives, making this IP a particularly promising value driver.

Source: February 2024 Corporate Presentation.

Moreover, the reports included the announcement of phase 3 for the Preserve 2 study of Trilaciclib in TNBC, which is expected to present final results in Q3 2014. Likewise, GTHX’s executives highlighted the promising results from phase 2 for TNBC: ADC Combo, which showed tolerability and survival benefits. Mid-year 2024 expectations for the ADC blend data include persistent monitoring of survival advantages compared to historical data, which could lead to collaboration opportunities for further development.

Management also noted that the shortage of platinum chemotherapy drugs such as cisplatin and carboplatin in 2023 slowed commercial execution. However, in 2024, Cosela patients' share is expected to continue growing, with an estimated 13% in the first-line market, a broader base of adoption, and 55 new accounts. In Q1 2024, GTHX continued to pursue new contract customer opportunities. Moreover, management suggested that the platinum shortage shouldn’t be a factor in the future, which, if true, should be another tailwind for Trilaciclib comps in 2024. After all, this shortage likely led to reduced use of platinum-containing chemotherapies, which probably decreased Cosela’s demand as an adjunct therapy.

Source: February 2024 Corporate Presentation.

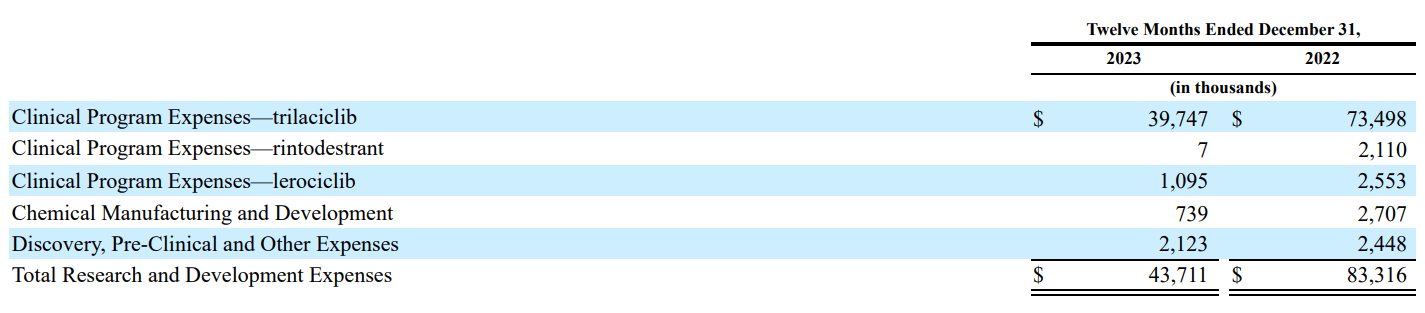

From a valuation perspective, GTHX is undoubtedly a bet on the Trilaciclib IP at this stage. In fact, the company’s latest 10-K report revealed that Trilaciclib accounts for roughly 90.9% of the company’s R&D expenditures. Also, Trilaciclib’s product sales and licensing revenues account for essentially all of the company’s revenues today.

Source: GTHX’s 2023 10-K report.

This simplifies our analysis as Trilaciclib revenues should continue to grow at a decent clip, particularly if the ongoing clinical trials for TNBC applications show compelling data. For context, in 1H2024, we should get updates on the Phase 2 trials of Trilaciclib in combination with TROP2 ADC for TNBC, and then by Q3 2024, the Phase 3 results for the PRESERVE 2 trial for metastatic TNBC. If both of these clinical trials are successful, they could quickly position Trilaciclib as a category leader in TNBC and corroborate its effectiveness indirectly in its currently approved SCLC application. These catalysts could certainly position Trilaciclib as a credible oncology treatment overall, and I believe this will only catalyze further revenue growth. In fact, SCLC alone already has more than enough market potential for sustained growth of Cosela since it accounts for roughly 15% of all lung cancer cases today.

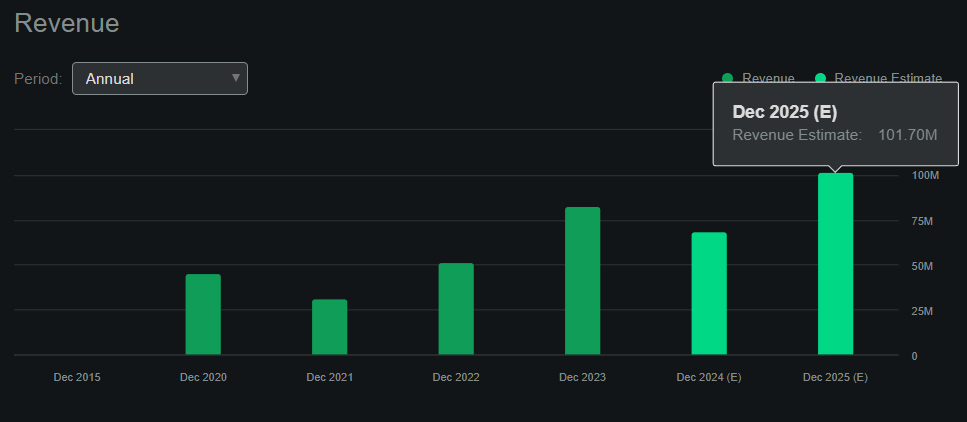

Seeking Alpha’s GTHX dashboard suggests that 2025 revenues should reach $101.7 million, implying 47.7% YoY revenue growth. Such estimates likely don’t include possible added revenue verticals from Trilaciclib applications on TNBC and Bladder applications, as these don’t have FDA approvals yet. Hence, I think it’s reasonable to conclude that GTHX’s revenue growth curve is still in its early stages.

Source: Seeking Alpha.

Using the 2025 forecasted revenue figures, I estimate a 1.68 forward P/S ratio for GHTX since its market cap is $171.2 million today. By comparison, the median sector forward P/S multiple is 3.63, which suggests that GTHX’s valuation is cheap relative to its peers. Moreover, the company holds approximately $82.2 million in cash and equivalents against just $57.2 million in total debt. I estimate GTHX’s latest quarterly cash burn figure was $38.3 million, which annualized implies $153.2 million in cash burn per year. I obtained this figure by adding the latest quarterly CFOs and CAPEX. This is the main risk on GTHX at this point, as the implied cash runway as of December 2023 is just about half a year. This means that dilution or more debt is virtually inevitable in 2024, which could lead to valuation headwinds for the stock.

Nevertheless, even though dilution is possible, rapid revenue growth could quickly offset operating costs and significantly reduce GTHX’s cash burn. For context, the company’s latest quarterly operating expenses amounted to about $22.5 million, or about $90.0 million per year. By 2025, GTHX’s revenues are anticipated to increase by roughly $32.8 million compared to 2024, and most of that delta in revenues would decrease by $153.2 million of yearly cash burn. Plus, such revenue projections likely don’t even include potential added revenue verticals from Trilaciclib applications for TNBC and Bladder treatments, which could cut future cash burn even quicker if successfully developed. But more importantly, dilution is unnecessary as debt is perfectly viable given Trilaciclib’s promising revenue streams. So overall, a mix of debt and stock is the most likely outcome, and the amount needed shouldn’t be unsurmountable. Hence, I think it’s reasonable to lean bullish on GTHX, so I give it a “buy” rating at these levels for investors aware of the inherent risks.

First, regulatory and approval risks remain, and my investment thesis on GTHX partially hinges on the assumption that added revenue verticals will come down the road as the Trilaciclib IP is successfully developed and commercialized. This assumption is uncertain, even though I think it’s reasonable. If GTHX fails to get FDA approvals for the previously discussed additional applications of Trilaciclib, then its upside potential could suffer. Moreover, even if FDA approvals happen, competitive risks remain. Oncology is a field of intense study, and competitors are researching multiple angles, so the Trilaciclib IP could suffer if a superior alternative is developed.

Lastly, I think it’s undeniable that the current cash burn rate is unsustainable, and I do expect such cash burn will decrease as revenues pick up. However, if revenues disappoint and management’s cost controls fail, margins could remain deeply negative, and its cash burn might not improve significantly. If we couple this risk with the company’s need to raise funds in the short term, it quickly becomes evident that GTHX is not without its risks. Yet, I think that on balance, Trilaciclib has proven effective so far in its Lung applications, and future revenue verticals are reasonable given the early clinical trial data. Plus, I think GTHX itself already seems to trade at a discount relative to peers, as implied by its forward P/S ratio, so there’s also some margin of safety embedded in its valuation today. Hence, it’s reasonable to consider GTHX as a good speculative “buy,” given the overall context.

GTHX’s stock has rallied significantly over the past six months. (Source: TradingView.)

Overall, GTHX’s leading IP, Trilaciclib, is undoubtedly promising with an already proven use case for Lung oncology applications. GTHX has also demonstrated that it can get FDA approvals for Trilaciclib, and it’s reasonable to expect that it’ll succeed in successfully developing adjacent FDA approvals for Trilaciclib down the road. Even though I recognize there are cash burn and dilution risks in the near term, I believe these are largely offset by GTHX’s discount relative to peers and promising revenue growth. Hence, on balance, I rate GTHX a good speculative “buy” for investors looking for exposure in the oncology biotech sector.