Dilok Klaisataporn

Dilok Klaisataporn

After originally turning bullish on Gates Industrial Corporation plc (NYSE:GTES) in May of 2023, we reverted to a 'Hold' rating in early November just before the announcement of the company's third-quarter earnings. We turned bullish approximately 10 months ago due to underlying strength in both the 'Power Transmission' segment as well as improving fundamentals in the 'Fluid Power' area. Furthermore, margin gains and an improving balance sheet were also noteworthy trends in our eyes given the adverse ramifications of the cybersecurity incident in February of 2023.

Gates Industrial stock however failed to gain traction (20%+ contraction over the 6 months between May 2023 & November 2023) post our May'2023 'Buy' rating which made us revisit the company as mentioned in early November of last year. What was affecting the stock at the time was growing uncertainty & bearish forward-looking EPS revisions. At this juncture (given the corresponding bearish pattern of lower lows up to that point) just before the announcement of Gates' Q3 earnings print, we believed it was prudent to downgrade the stock to a 'Hold' until the third quarter report was fully digested.

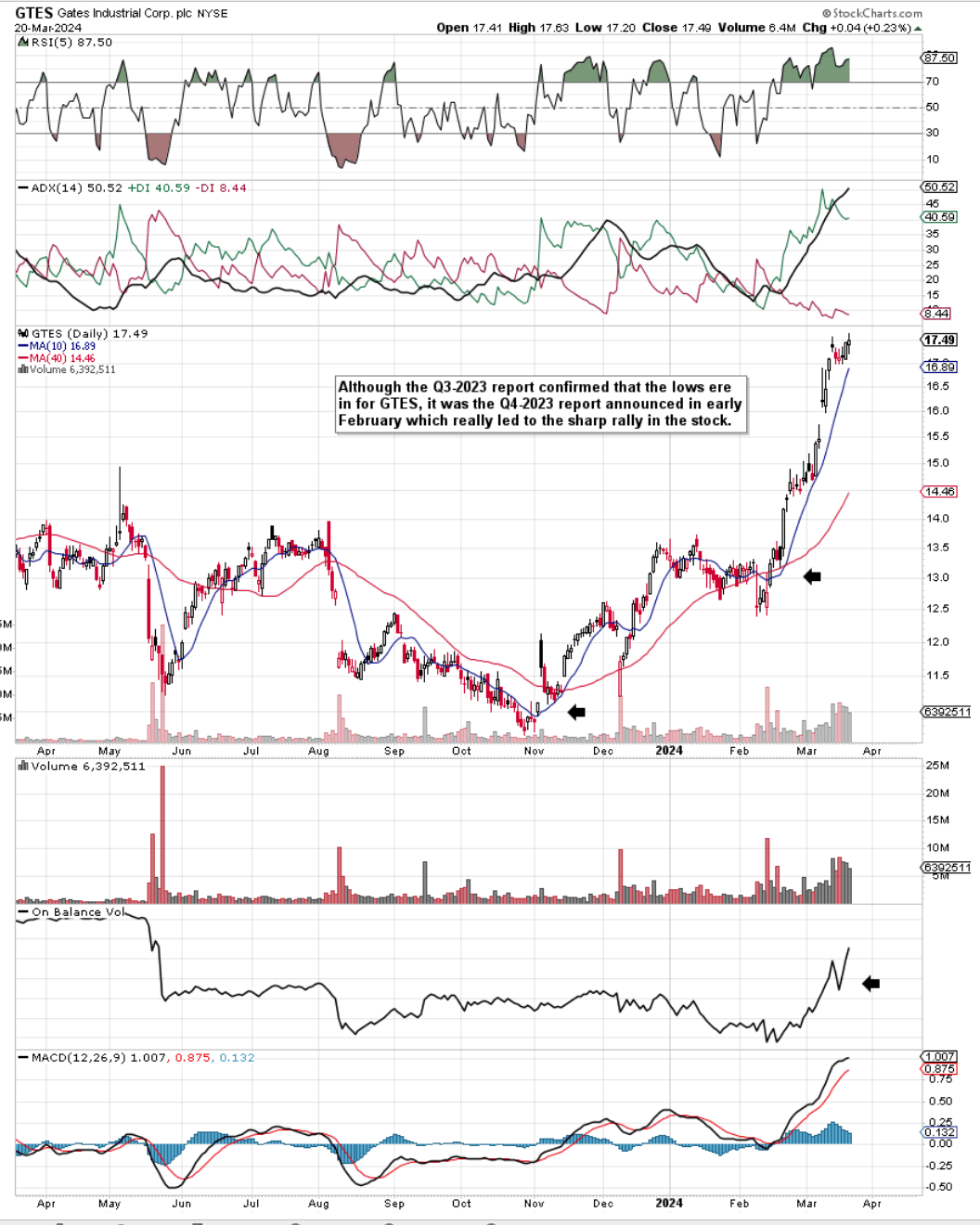

Thankfully, the marginal Q3 earnings beat and the raising of adjusted EPS guidance were enough to stop the pattern of lower lows in earnest. The subsequent Q4 earnings report (announced in early February this year) was a more convincing bottom-line beat ($Non-GAAP EPS of $0.39) resulting in a more aggressive upturn in Gates' shares as we see below.

Gates Technical Chart (Stockcharts.com)

Therefore, given the searing momentum that came off that Q4 earnings report (thus nullifying near-term macro uncertainty to a significant degree), we are upgrading our rating in GTES to a 'Buy' once more. Trends in the company's Q4 numbers & fiscal 2023 in general back up our bullish thesis as we learn below.

Up to now, we have consistently stated that Gates' debt load was a significant factor when valuing the stock. High debt loads invariably lead to below-average interest coverage ratios which can adversely affect cash-flow generation over time. Therefore, we stated that the market needed to see improved forward-looking growth rates to compensate for this leverage. This clarification we believe may have finally come as we see below.

For example, in Q4, the overall company gross margin metric surpassed 39%. This was a meaningful 440 basis point gain over the same period of 12 months prior which was maintained for the most part further down the income statement. Sustained margin strength was confirmed by the impressive $186 million of adjusted EBITDA in the quarter.

However, where investors were probably most impressed was the free cash flow print for the quarter which came in at a very impressive $165 million (158% conversion of adjusted net profit). This brought Gates' full-year free cash flow conversion to 110% of adjusted net income which means shares at present are trading for just under 11 times free cash flow.

The drop in Gates' free cash flow multiple is an encouraging sign as the updated multiple illustrates how much free cash flow investors can attain for every dollar invested in the company. Higher cash-flow generation should also enable management to bring down that balance sheet leverage as alluded to earlier. Furthermore, the recent approval of the share-buyback initiative is an encouraging sign that free cash flow should remain elevated for some time to come.

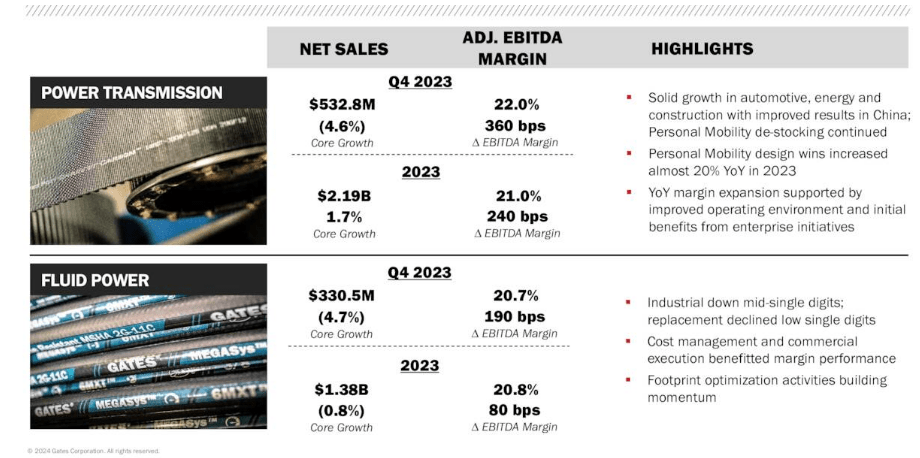

Adjusted EBITDA margin OF 22% in Power Transmission & 20.7% in Fluid Power were well ahead of the prior year quarter plus the fiscal 2023 average. This was down to an improved operating environment and promising signs from enterprise initiatives. Automotive & Energy segments remained strong with the bounce back in automotive in China being a welcome surprise in the quarter. Suffice it to say, notwithstanding Q4 margin improvements, when one goes under the hood of Gates, it can be seen that the company has numerous initiatives that should keep earnings growth elevated.

GTES Q4 Segment Highlights (Seeking Alpha)

Personal Mobility design wins for example jumped by close to 20% in fiscal 2023 and the company's growing footprint concerning its regional manufacturing initiatives (resulting in improved efficiencies & lower costs over time) means the runway for margin expansion is nowhere close to an end. The CEO echoed these promising trends on the recent Q4 earnings call when he made it clear that the company would continue to invest through the cycle.

While we cannot control the timing of improvement in broad-based business activity, we are firmly in control of improving our business operations for the long term. As such, we continue to build the momentum of our enterprise initiatives in the areas of productivity and footprint optimization. Moreover, we are thoughtful about making further investments in our business.

As the business environment evolves, our priority is to stay close to our customers at the commercial front end as well as maintain tight operational proximity to optimize service levels and fill rates of our comprehensive portfolio of highly engineered mission-critical products. We are making investments in innovation, material science, and process engineering to improve the competitive position of our portfolio while equipping our people with better analytics and empowering them to ramp up the execution of our growth initiatives.

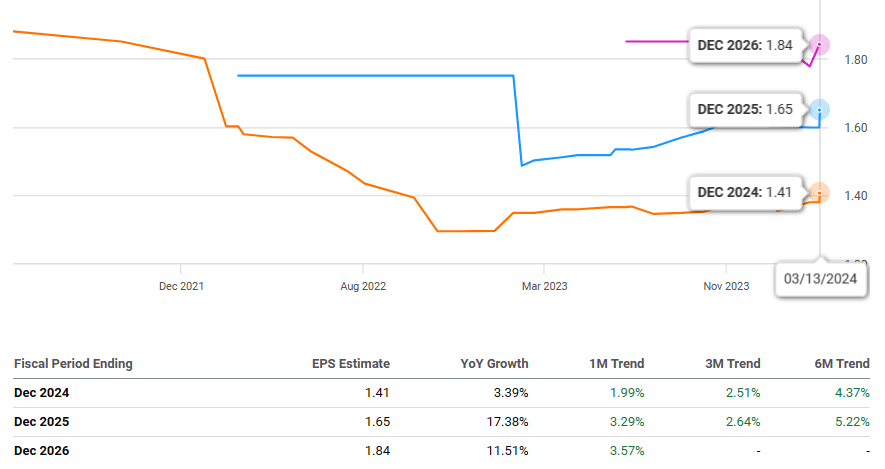

Therefore, as we see below, given the strong Q4 trends and encouraging outlook for fiscal 2024, forward-looking EPS revisions have remained buoyant with the EPS 2024 estimate now coming in at $1.41 per share. Suffice it to say, given the low free cash-flow trailing multiple discussed earlier and management's intention to convert 90%+ of its fiscal 2024 adjusted net profit, Gates should continue to have the wherewithal to keep on investing aggressively, pay off debt & reward shareholders through share-buybacks over time.

GTES Forward-Looking EPS Revisions (Seeking Alpha)

Although as mentioned, Gates' trailing free-cash-flow multiple of just under 11 remains an attractive entry here, one must also be mindful of how investor sentiment can change on a dime here. What we mean by this is that current consensus trends now point to marginal top-line growth along with 3%+ bottom-line growth for Gates in fiscal 2024. The macro picture for industrial growth (in both of Gates' segments) remains sluggish which means further declines here would most likely curtail any significant share-price gains.

Therefore, we would urge investors to keep analyzing Gates' book-to-bill ratios and especially forward-looking consensus trends which will determine if markets are indeed opening up or if the macro picture is becoming even more choppy. Remember, sustained growth (resulting in robust free cash flow numbers) is a prerequisite given Gates' sizable amount of goodwill & intangible assets on its balance sheet as well as its significant debt load. Suffice it to say, Gates' improving but elevated net-leverage ratio (2.3x at the end of fiscal 2023) was not focused on by the market given how margins and free cash flow have been improving. However, if interest rates were to rise once more and/or if EPS revisions were to be revised down over time, investors may be swift to sell their holdings over time.

Nevertheless, based on current trends and the sector's valuation on average, Gates should be worth at least 15 times its free cash flow all things remaining equal. Therefore with fiscal 2023 free cash flow coming in at $419.8 million, if we multiply this number by 15, we get a forward-adjusted market cap of $6.297 billion. Dividing this projected market cap by the current number of shares outstanding (260.12 million), we get an estimated value of $24.20 per share for Gates Industrial.

To sum up, given the improvements in fill rates, margin expansion & free-cash-flow generation in fiscal 2023, we believe Gates' present rally has more room to run here as the company begins to report fiscal 2024 numbers and beyond. Risks as outlined undoubtedly remain but the company looks primed now to begin reporting strong earnings numbers once volumes recover in earnest. We look forward to continued coverage.