zhengzaishuru

zhengzaishuru

Gran Tierra Energy (NYSE:GTE) (TSX:GTE:CA) looks to be one of the cheapest oil stocks out there on the market, trading at close to 2x FWD earnings and at about half of book value. Despite some risk coming from Colombia, I believe the market has priced in all the downside making it very attractive for new investors. Given a promising oil market with stable prices, increasing production, and intense buybacks, I believe Gran Tierra is a buy.

The company is "a company focused on oil and gas exploration and production with assets currently in Colombia and Ecuador" (Annual Report). Its revenues comes from the production and sale of oil and market prices. As an exploration and production oil company, they identify promising land with good reserves and then invest in drilling wells to extract those resources. They then sell the extracted oil to buyers and make a profit.

Per the annual report, "For the year ended December 31, 2023, 97% (2022 - 100%) of our revenue was generated in Colombia." Colombia has significant royalties that oil companies must pay, and according to the 10-K, "Discoveries made before the enactment of Law 756 of 2002 have a royalty of 20% and in the case of such discoveries under association contracts reverted to the national government, an additional 12% applies for a total royalty of 32%."

Despite these pretty big royalties, the company is still demonstrably profitable even with these fat checks to the Colombian government. Gran Tierra spots EBITDA margins of 54%, and EBIT margins of 15% for the past 5 years on average. Therefore, the royalties don't seem to be a major dent to profitability and I believe the Colombian government is quite reliant on oil for their exports and GDP numbers. As long as high oil prices exist, I think Gran Tierra will continue to be profitable going forward.

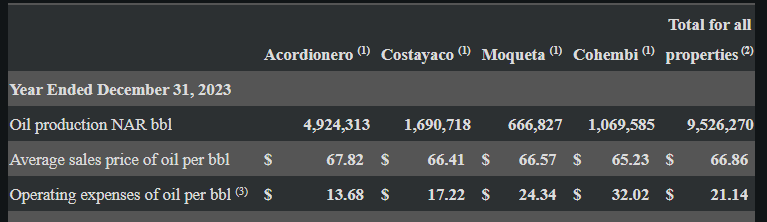

The company has 4 major oil fields that contribute to their revenues, Acordionero, Costayaco, Moqueta, and Cohembi. These hard to pronounce fields for 2023 have a combined production capacity of 9,526,270 NAR barrels, with operating expenses of $21.14 per barrel of crude oil. This seems to me very attractive due to the low-cost operating nature of these oil fields, and at current oil spot prices all of them are immensely profitable.

10-K

Many oil experts predict that oil prices will remain relatively high. According to the EIA, "Because of falling inventories, we now expect the Brent crude oil spot price will average $88 per barrel in 2Q24, up $4/b from our February STEO, and we expect the Brent price will average $87/b this year." Goldman Sachs indicates high stable oil prices, "According to Goldman, the international benchmark Brent Crude will likely remain in the $70-$90 a barrel trading range in the near term amid modest geopolitical premium from the wars in Ukraine and the Middle East." I think that given these predictions oil will probably remain somewhere between $60-$90 a barrel for the next 2-3 years, giving significant profits for Gran Tierra Energy. At almost 2x FWD earnings, it looks like investors can get all their money back so long as oil prices stay relatively high for 2 years.

Given high oil prices, it's no surprise that oil companies want to ramp up production. According to the earnings call, Gran Tierra is drilling well after well to increase production,

All wells from this development program are expected to be drilled, completed and on production before the end of the first quarter of the year. Back down in the Southern Putumayo Basin, Gran Tierra intends to commence development drilling in the Cohembi oil field located in the Suroriente Block during the later half of the year. We plan to expand the block’s production facilities, increased gas power generation, construct new development well pads and make social investments in the area, all with the goal of substantial production growth in 2025 and 2026.

I believe the oil production at Gran Tierra will expand steadily as the company continues to redeploy its cash flow intelligently into very high ROI projects. They have so many reserves, both developed and undeveloped to tap into giving investors significant tailwinds for growth. According to the annual report,

Our base capital program for 2024 is $210 million to $240 million for exploration and development activities. Based on the mid-point of the 2024 guidance, the capital budget is forecasted to be approximately 60% - 70% directed to development and 40% - 30% to exploration activities. Approximately 20% of the development activities included in the 2024 capital program are expected to be directed to facilities to support future production growth and enhance recovery factors.

As investors can see, the company is leaning more towards development to support future production growth. It's a little absurd to me that a company's market cap of $200 million is equal to its capital expenditures for 2024. I believe the company's development activities will be hugely successful in ramping up production, giving more profits and cash flow to investors.

The story here can be quite simple: high oil prices + ramping production = more profits/cash flow. I think both parts of the equation will likely occur, giving investors a good chance for increased profitability. Even with pretty high royalties and Colombian risk, those challenges are unlikely to stop Gran Tierra from growing production.

I believe management has been extremely shareholder friendly by engaging in share repurchases. According to the earnings call,

During ‘23, a combination of our strong reserves growth, ongoing reductions in debt and share buybacks allowed Gran Tierra to achieve net asset values per share before tax of $44.48 1P, up 288% from 2020 and $79.13 2P, up 144% from 2020.

Additionally, in 2023, we showcased our confidence in Gran Tierra’s future prospects by our purchasing 6.8% of our outstanding shares through our normal course issuer bid or NCIB program, demonstrating our dedication to create long-term shareholder value. We’re currently trading at a discount to our proved developed producing or PDP net asset value per share by about 46%. Our average cost per each share purchase was $7 per share.

I believe management has made it quite clear that their stock is undervalued, and their aggressive approach in buybacks will improve net asset value per share and cash flow per share numbers. They even mention that they are trading at around a 50% discount, indicating a potential double for investors.

All in all, continued buybacks serve as a major catalyst for the share price, even if the stock is ignored by the mainstream community. When neglected stocks stay neglected, the management can juice shareholder returns by aggressively buying back shares, which I believe says a lot about management's genuine intention to deliver great shareholder returns.

A conservative valuation estimate still yields potent shareholder returns. Assuming revenues stay at a floor of $500 million going forward, I believe the stock is still dramatically undervalued. A $500 million revenue estimate annually is incredibly conservative given high expected oil prices and ramping production.

Apply a safe EBITDA margin of around 40%, which is below the 5Y average gets me a floor of EBITDA going forward of $200 million annually. Apply a EBITDA multiple of 4.5, which is around the sector median gets me a fair enterprise value of $900 million. Subtracting net debt of $500 million gets me a market cap of $400 million. Divide by shares outstanding of 32 million gets me a fair value of $12, rounded down.

Even with conservative estimates, a margin of safety of 50% still exists in the stock. I believe the company could likely do even better than my above estimates, but even with conservatism the stock is significantly undervalued.

Investors can also see undervaluation with the price to tangible book of .5x, which supports a $12 price target if investors believe the stock ought to trade near book value.

As an oil stock, their revenues and profits are directly impacted by the price of oil going forward. Therefore, any major price drop in oil and gas will likely negatively impact profits for Gran Tierra, which could decrease share prices. Back in the pandemic, Gran Tierra went as low as $2/share as demand for oil plummeted, so if something like that happens again oil stocks may underperform.

The majority of their operations are concentrated in Colombia, specifically in "the Middle Magdalena Valley (“MMV”) and Putumayo Basin" (Annual Report, Page 15). In particular, their largest oil field Acordionero made up "52% of total Company production for the year ended December 31, 2023." If some natural disaster or operational hazard were to disrupt production at Acordionero, production may stall and revenues may falter.

Colombian royalties may increase in the future as the Colombian government does rely substantially on oil for their economy. Colombia's top court recently struck down a royalty measure worth over $700 million to the government from mainly its coal producers. Basically the president wanted to prevent "oil and coal producers from deducting royalty payments from their corporate tax liability". The courts struck this down, supporting oil and coal producers' ability to deduct their royalty payments and thus reduce their tax bill. While the courts seem to be in favor of oil and coal producers, President Gustavo Petro seems undeterred. Petro seems very determined to ditch fossil fuels and reliance on oil for Colombia's economy,

The correct policy, in Petro’s view, is to ditch fossil fuels. And he is positioning Colombia not only as a key advocate for the global energy transition but also as a test case of how a fossil-fuel-producing country can decarbonize.

In the long-term Gran Tierra may be under pressure politically from leaders trying to switch away from fossil fuels, which presents risks for investors.

Finally, oil companies are seen as undesirable by many institutional funds and sovereign wealth funds due to their ESG-unfriendly nature. I think the main reason for why oil stocks continue to be undervalued is the lack of institutional interest in companies that are seen as environmentally unfriendly. As institutions become more ESG-oriented, less and less investors want anything to do with oil and coal companies.

I believe the story here can be quite simple. High oil prices + increasing production = higher profits for investors. As one of the cheapest oil stocks on the market, investors who like cheap oil may want to buy Gran Tierra at bargain prices. Oil will likely remain at attractive prices, production is dramatically increasing, and the risk/reward profile seems favorable at $6. Even if the stock continues to stay neglected, buybacks act as a major catalyst for a higher share price. I think at 2x FWD earnings it is far too cheap and deserves a buy.