JHVEPhoto

JHVEPhoto

The Goodyear Tire & Rubber Company (NASDAQ:GT) is a tire manufacturer in the United States. Over the years, the company has undergone a tumultuous period but I believe there seems to be signs of a turnaround. While shares have underperformed the market by a wide margin, the company has been undergoing a restructuring and has been making significant investments that should position it to be a market leader in the future. With higher revenue growth and margin expansion ahead, I believe that the market is sleeping on this forgotten and unloved stock at a depressed valuation.

Goodyear Tire & Rubber Company is a household name that many might already be familiar with. They're a world-class tire manufacturer that's been around since the 1800s. Tires make up 86% of the company's sales and they sell to a wide range of customers. Along with your standard automobiles, they also make tires for buses, aircraft, industrial equipment, and other vehicles. The remaining 14% is made up of its services business which includes retreading and the sale of chemical and rubber industrial products.

With 57 manufacturing facilities and a presence in over 23 countries, the company has a significant market share selling under the Cooper, Dunlop, Kelly, Debica, Sava, Fulda, Mastercraft, and Roadmaster brands, in addition to its flagship Goodyear brand. It has nearly a thousand company-owned retail outlets that provide repair and other services for customers.

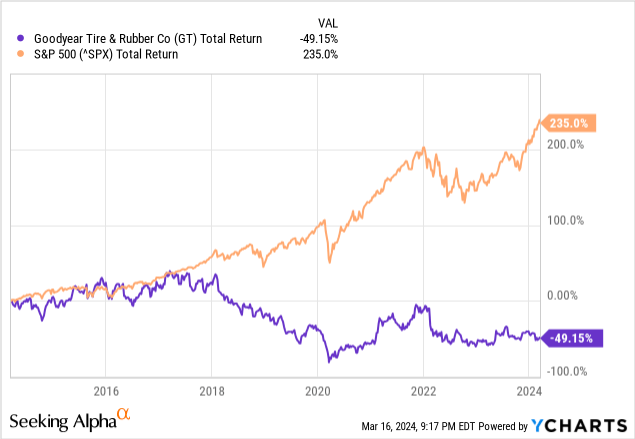

When looking at the historical price performance of Goodyear tires, it's been somewhat of a dud. In the last ten years, while the S&P500 has delivered a total return of 235%, investors in Goodyear have essentially lost half their investment. While this is obviously not great, I think there are reasons to believe things at Goodyear may be turning around.

Over the last decade, the global tire market has been increasingly more competitive as new entrants from Asia enter the market. That's caused most domestic manufacturers in the U.S. to lose market share, so barriers to entry have been somewhat eroded over time which has caused margins to contract.

As part of the company's strategy, Goodyear aims to combat this through a few primary areas including 1) innovation excellence (2) leveraging partnerships (3) Goodyear Forward Plan.

As part of the innovation excellence part of the strategy, Goodyear has been investing a lot in new technologies and product lines that will appeal better to customers. This is so that the company can maintain its competitive advantage against low-cost overseas competitors and position itself as a technological innovator in the space.

A primary example of this SoundComfort, a technology that reduces road noise generated by tires without sacrificing grip and performance. Even with minor improvements, small changes to safety and performance can have a major influence on customer buying habits that make Goodyear's products stand out in the face of rising competition. In the end, the company should be able to regain market share and expand into higher margin areas as it becomes the premier product that consumers and manufacturers want.

When it comes to leveraging partnerships, Goodyear has been making inroads with several companies to tighten the technology and innovation around its products. A good example of this is the company's collaboration with ZF, which specializes in hardware and software systems for passenger and commercial vehicles. Through the partnership, Goodyear is able to contribute to better control, comfort, and efficiency in the driving process. Another partnership, with TDK Corporation, offers similar benefits where Goodyear is using intelligent hardware and software in its tires to create a robust tire sensing system. This may not be the next generative AI story here, but it's things like this in a boring, relatively undisrupted industry that will maintain Goodyear as a market leader in the space.

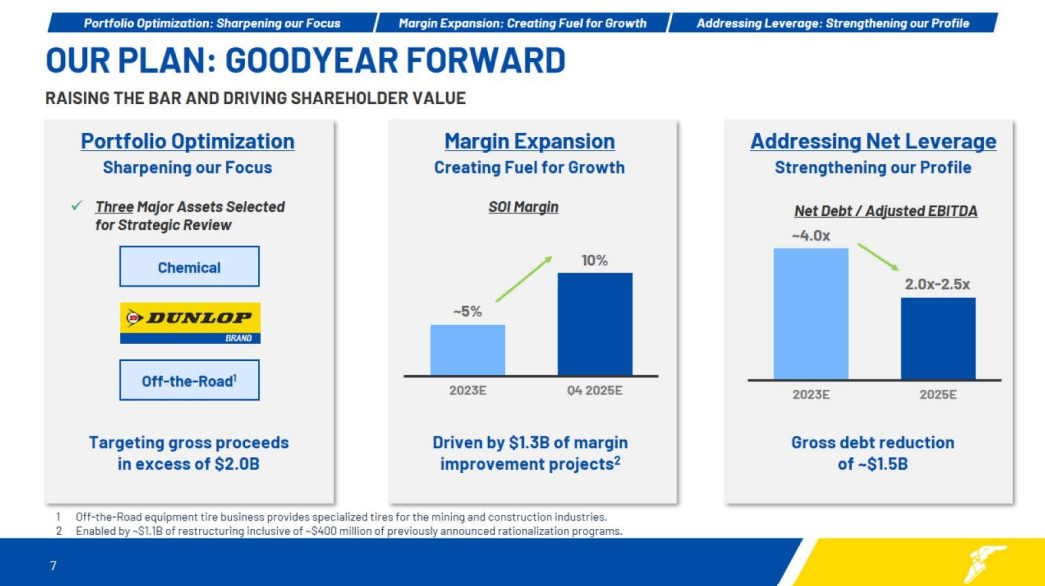

Finally, regarding the Goodyear Forward Plan, the company has become a lot more shareholder-friendly with plans to restore better margins and return cash to shareholders. A lot of this comes after an activist investor got involved with the company. In the Spring of last year, activist investor firm Elliot Management bought 10% of the outstanding shares of Goodyear. When it was announced that the Board was implementing many of the changes, the company's share price jumped nearly 20%. Since then, shares have been basically flat, despite improvements already and a solid medium-term plan in my view. Under the new plan, the company is exploring strategic alternatives for its Chemical business, Dunlop brand, and off-the-road equipment tire business. In addition, by 2025, Goodyear expects that it should double its operating income margin by 2025. This would put it at 10% and would restore profitability so that it can de-lever down to 2.0-2.5x by that time.

Investor Presentation

Goodyear reported its Q4 and full year 2023 results on February 13, and while the company did miss on the revenue figure with sales clocking in at $5.12 billion, down 4.8% year over year (a miss by $239.5 million against analysts' estimates), the company did beat on earnings per share by 11 cents with Q4 EPS coming in at $0.47.

So far, it's been the market view that Goodyear has been undergoing weakness as the automotive market has been recovering in the back half of last year. This has been supplemented by a gradual recovery in auto volumes since the pandemic period of 2020-2021. In my estimation, the volatile swings in both EPS and margins have been enough to keep most investors away from Goodyear.

But I think there are two primary reasons to believe that the market and consensus view is wrong and that the company's shares don't deserve to be down 30% since the Spring of 2020.

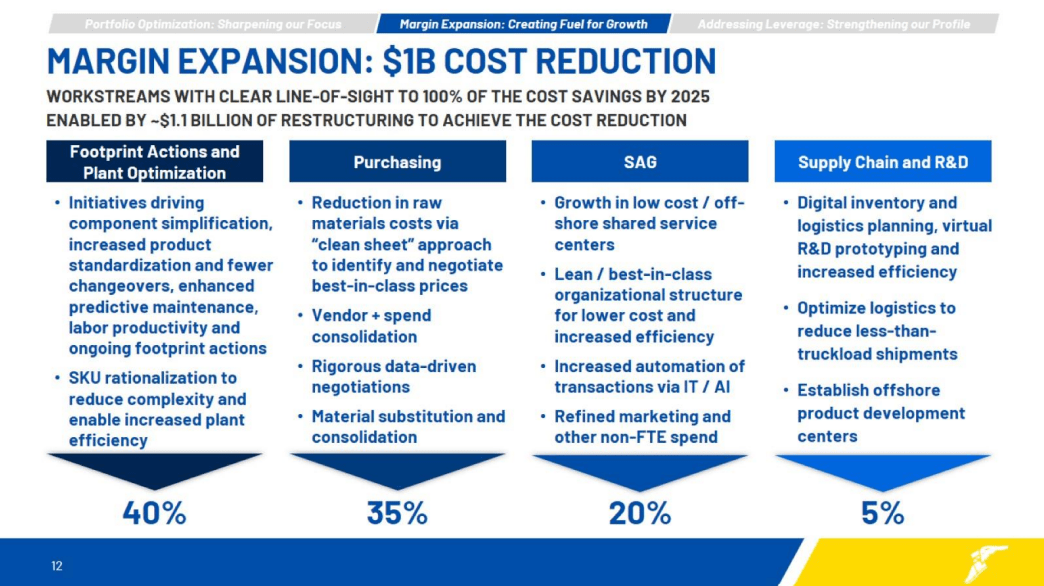

Firstly, through the Goodyear Forward plan, the company has been targeting higher-margin segments of the business that are not only more profitable but also faster growth. So in my view, if the business is able to generate strong free cash flow and pay down quite a bit of debt, we could see over $500 million saved in interest expenses in the next two to three years. The consensus view is that revenue growth will not be large enough to fully realize the debt reductions and margin expansion but I believe the company's strong brand reputation in the market as well as its investments in product innovation should mean that it will. For example, on the earnings call, Goodyear's management discussed product innovation at length, yet there were no analyst questions related to this. This indicates to me that analysts are likely asleep at the wheel here.

Investor Presentation

Secondly, the notion of electric vehicles, sustainability, and eco-friendly driving capabilities have been major shifters in the automotive industry. So far, the tire industry hasn't really kept up with this, but Goodyear, as a market leader has. One example of this is a partnership that the company did with Gatik, a company that's been revolutionizing the autonomous driving industry and has made partnerships with several companies now. Goodyear and Gatik have been partners for a few years and Goodyear has essentially integrated its technology so that tires are smart enough to send road information to a driverless car.

This is important because Goodyear will be able to integrate this technology and work on it before the competition gets involved. Goodyear's knowledge of the manufacturing process combined with Gatik's technological expertise makes this a worthwhile partnership with synergistic benefits to both parties. In my view, it's difficult to quantify a number of how much margin expansion and revenue growth we are talking about. But it nonetheless speaks to the company's ability to be at the forefront of innovation and invest for the future at a time when most competitors are not.

In terms of my outlook for the company going forward, I would expect continued partnerships with innovative technology companies. There's likely more that the company can do in the EV and autonomous driving space and continue to make their tires safer on the road.

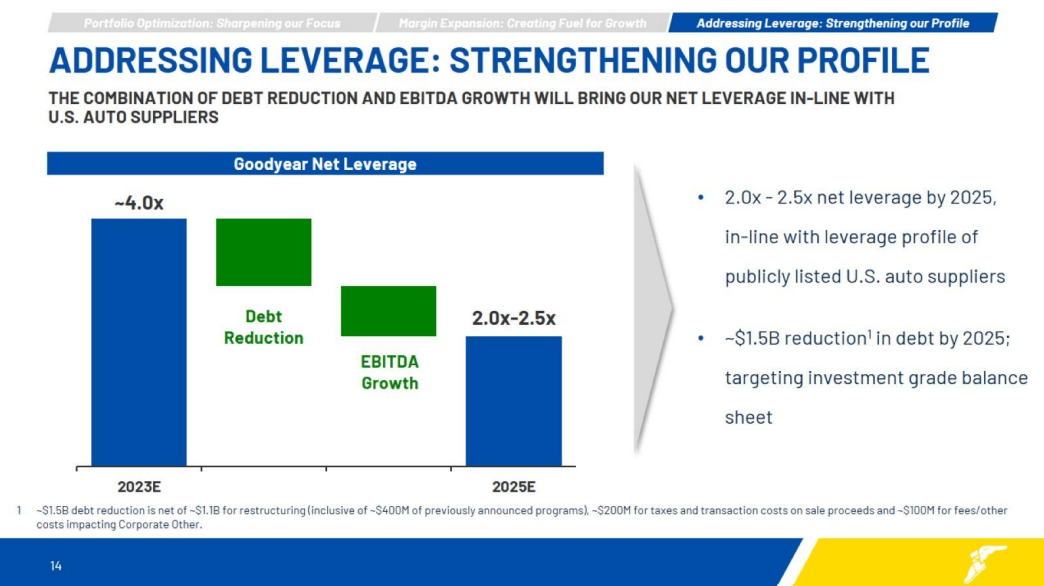

Another major catalyst would be the company paying down debt. Goodyear is somewhat highly levered and has about $7.7 billion of long-term debt on its balance sheet while having a market capitalization of $3.5 billion and a cash position of just $902 million (source: S&P Capital IQ). So clearly, debt makes up a substantial portion of the company's capital structure. As most of this debt bears interest above 7%, Goodyear is looking to bring its leverage down by half (2.0-2.5x) from the 4.0x it sits at currently. With half of that being funded by paying down debt (and the other half EBITDA growth), I estimate that about 30% of its debt could be paid by 2025, resulting in a $100+ million savings in interest expenses.

Investor Presentation

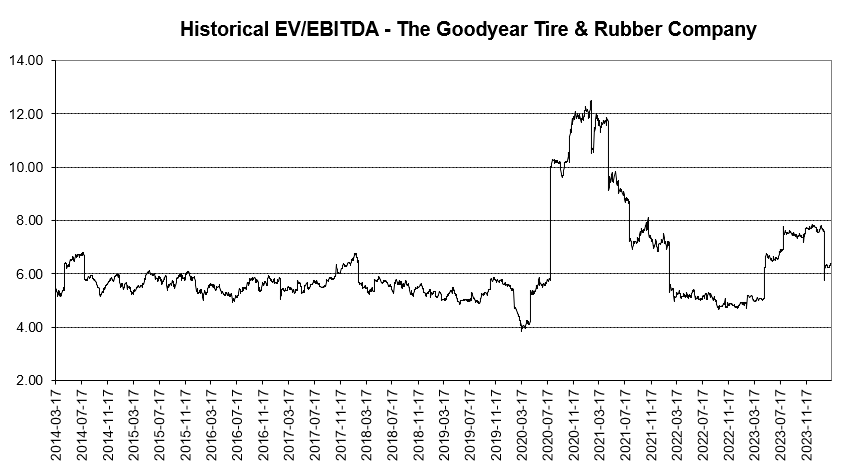

When it comes to valuation, Goodyear trades at a very attractive valuation, likely due to the fact that it has a substantial amount of debt. At 6.3x EV/EBITDA, the market has not adjusted its multiple higher to account for any of its investments or revenue potential going forward. According to Custom Markets Insights, the global tire market is expected to grow at a CAGR of 3.7% until 2030 so I would keep this as a base case despite the company's potential to grow at least twice this rate.

Author, based on data from S&P Capital IQ

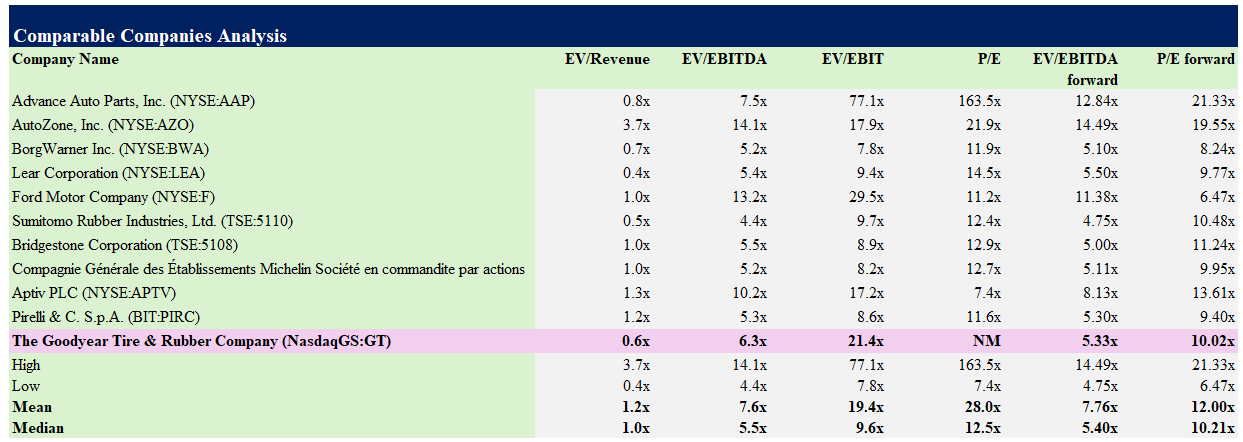

Comparing to peers in the tire industry, Goodyear trades at 5.3x forward EBITDA while the peer group trades at 7.8x EBITDA (Source: S&P Capital IQ). In my view, as the company de-levers the balance sheet and proves that it can meet the targets of its Goodyear Forward plan, then shares should re-rate higher closer to the average multiple. At 7.8x EV/EBITDA, shares of Goodyear would be at least 50% higher than what they trade for today.

Author, based on data from S&P Capital IQ

In terms of the risks to the investment thesis, I've discussed the company's debt position, but another risk would be labor. Goodyear has about 72,000 employees globally with about a third of them who are unionized. We've already seen Goodyear make cuts to its workforce in 2023 so unfavorable relations with unions or an increase in the number of employees under a union would be a negative headwind for Goodyear.

To summarize, I think Goodyear presents a compelling investment opportunity that has strong upside potential. Despite some messy financials in the past and swings in margins that looked like they were out of control, I think Goodyear is back on track and has positioned itself to restore profitability and steady growth. As the company begins to de-lever the balance sheet and make investments and partnerships that strengthen its product portfolio, the company seems poised for a re-rating in its valuation much higher. As it strategically makes inroads in the EV and autonomous driving space, the combination of a strong brand and revamped product portfolio makes this an exciting story with high free cash flow growth potential. As such, I rate shares of Goodyear as a buy today.