BlackJack3D

BlackJack3D

GSI Technology, Inc. (NASDAQ:GSIT) is a stock we continue to hold as part of our speculative, mad money-style exposures. The stock has started to express some meme qualities these last couple of weeks, and the price has risen very substantially from its level around $2 as of mid-February. We think the main reason is that markets are going a level deeper in their research for artificial intelligence (AI) plays, and have come across GSIT in the process, which is absolutely an AI play, albeit one that is far from being demonstrated commercially.

We've been covering GSIT for years now, and its technologies have the potential to be relevant in broad AI applications, whether they use sparse structures or not. The issue is that GSIT is still very far off from being ready with its APU. They are only now talking about Gemini-III, which is the chip design that is going to be meant for their commercial push at data centers, from what we understood.

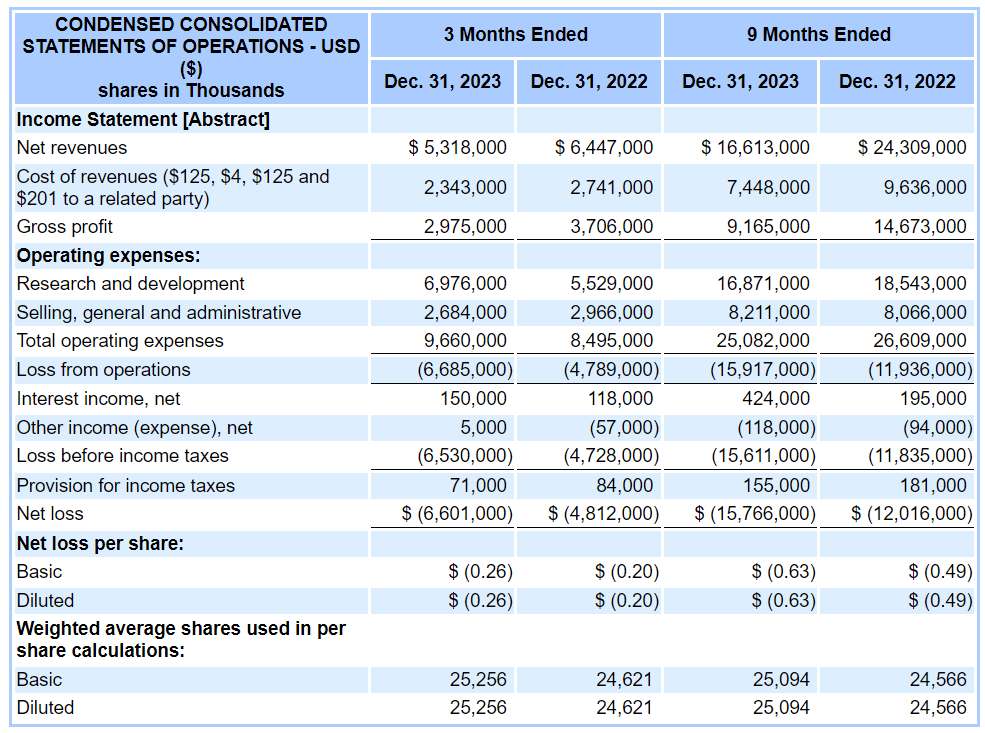

They burned around $6 million in cash in the last 9 months. R&D continues to grow to support the Gemini R&D and revenues on SRAM are falling. The Rad-Hard revenues that were supposed to significantly grow revenues came in, but way too late. Therefore, the SRAM performance continues to be pretty underwhelming. Better late than never, as it still at least offsets some of the development burden, which has always been the fundamental appeal of GSIT - that it's an option with a mitigated premium.

They did claim that they managed to win some new contracts that should be able to start producing a 10% kick to revenues, but only starting in 2025. However, due to a pretty weak record on delivering on promises, we wouldn't put too much faith in it.

GSIT IS (SEC.gov)

The current cash position is around $21 million. They expect cash burn to rise from current run-rates.

This year we'll be around $13 million to $14 million. Yes, we have one kind of extraordinary expense coming up this fiscal year that requires about $2.4 million cash outlay.

Doug Schirle, CFO of GSIT, during the Q2 Call.

This should give them almost a 2-year runway as a base case, based on that disclosure. GSIT also reports that they are planning on selling a building they own for around $10-13 million, which would further defer any needed action in equity capital markets for another year, although given the recent position of prices, an opportunistic small-scale issuance they can do would be great.

On the Gemini front, apparently they're getting their Gemini-II in February from the fabs and are going to start to do some alpha tests on it with limited customers. They actually delivered here on timelines for when the Gemini-II was supposed to exit the design phase. Now they are going to produce and sample some to see where they stand in terms of performance. It has enough in-chip memory to hold more information, including specialized algorithms, and is a major step-up in performance from Gemini-I. They have some SBIR contracts now with the USAF Research Laboratory that's going to support establishing the performance of the Gemini-II and pave the way for Gemini-III, which they are already beginning to talk about.

The development of Gemini-III, which is the next step, will be another pretty big R&D burden, but it's also the product that's supposed to be a hit among hyperscalers. So, they are looking to possibly do some customer partnerships or other industrial partnerships in order to lessen the burden for developing it and bringing the actual manufacturing of it to scale if they get some major orders. They are also reserving the possibility of licensing out the IP, but having made some progress already on the Gemini-III development and with a view on what's possible, they are leaning towards bringing it forward themselves. The stronger price action may contribute to this IP idea being less likely if they can do any sort of financing for themselves. We should mention that there's no timeline yet for Gemini-III, and there is still work to be done with Gemini-II

Hyperscalers are an important market because there is economic value in reducing the intensity associated to work with large and sparse matrices, as well as in search applications. We are already confident in that proposition, but we also note that there are a lot of applications in NLP, too. We have discussed this a little in the past, as NLP models use architectures that could benefit from the Gemini. Also, models that try to approximate human activity and thinking usually work on data that follow the Hebbian principle, and NLP models use a lot of sparse data and produce a lot of sparse layers since language will follow Hebbian principles. To bring it into the most relevant context with large language models, APUs from GSIT may have especially useful applications in searching for context to inform responses to prompts.

We really like the GSI Technology, Inc. long-term proposition, but we are wary about current price increases. It is more likely that GSIT is going through a phase of being a trading stock right now rather than gaining more permanent following. When it no longer is a trading stock, liquidity should fall and the only people who'll keep holding are the ones who are in it for the very long haul. Prices will likely settle down to previous level at which holders were taking their long-standing wait and see approach on Gemini-II performance and the next announcement of timeline ambitions for the final commercial push.

GSIT already popped last year when the major revelation of ChatGPT started affecting markets, so whatever case there is behind GSIT is already known. Nothing company-specific or new is going on, and the real measure of the success of the APU is still far off - it'll have to be after an industrial plan is established and commercial agreements become reached.

We think the stock remains in a position where something meaningful and commercial needs to happen on the APU side before more long-lasting moves are possible. At that point, GSI Technology, Inc. stock could be worth multiples of what it is now. With a genuinely innovative technology, it could take outsized share of the $327 billion or so AI semiconductor TAM estimated by 2027 from current valuations of $127 million.