Chris Hondros

Chris Hondros

This article focuses on Goldman Sachs BDC (NYSE:GSBD), a Goldman Sachs Group (GS) entity that deals with direct lending. Global credit markets are heating up as volatile interest rates and credit spreads have coalesced, creating a speculative environment. As such, we decided to communicate our latest findings on Goldman Sachs BDC.

Without further delay, let's discuss our findings.

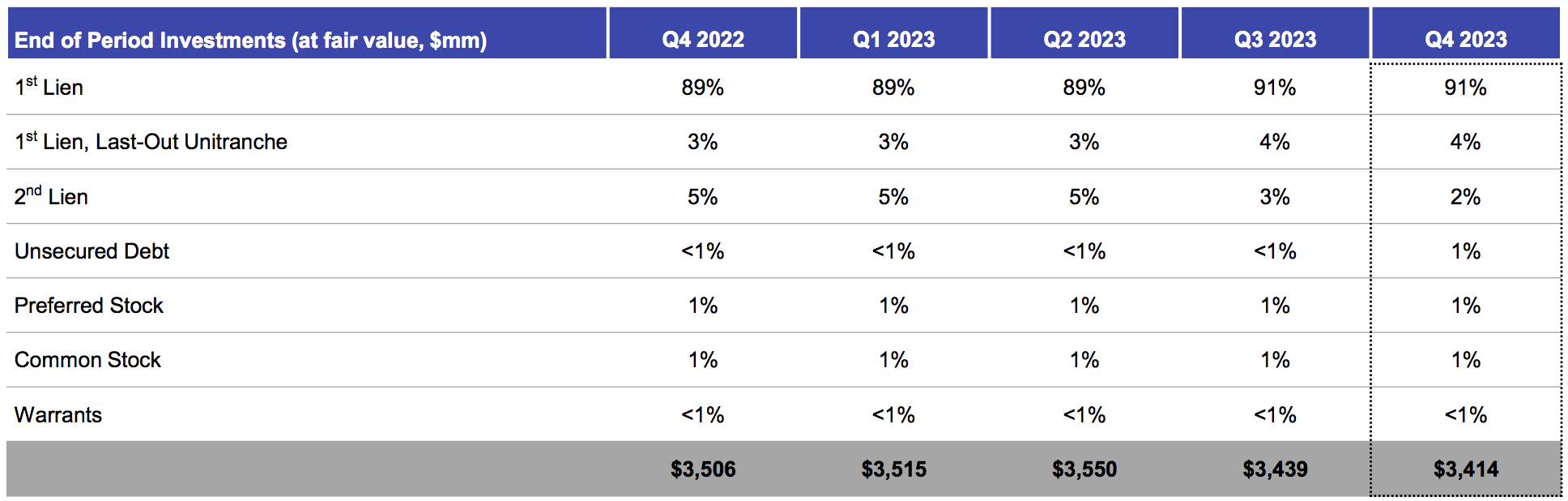

Goldman Sachs BDC is a direct lender primarily targeting U.S. middle-market first-lien loans. The firm's portfolio does contain other tranches of debt, but it's quite clear from the diagram below that its main focus is first-lien loans. Moreover, Goldman BDC partners with firms to improve their capital structures and uses its network to access favorable capital.

Goldman Sachs BDC

I just wanted to touch on the secondary component of Goldman BDC's business. We honestly have very little input regarding this business component. Instead, we decided to focus on the hard facts conveyed by Goldman Sachs BDC's portfolio data.

Let's take this analysis from the bottom upward.

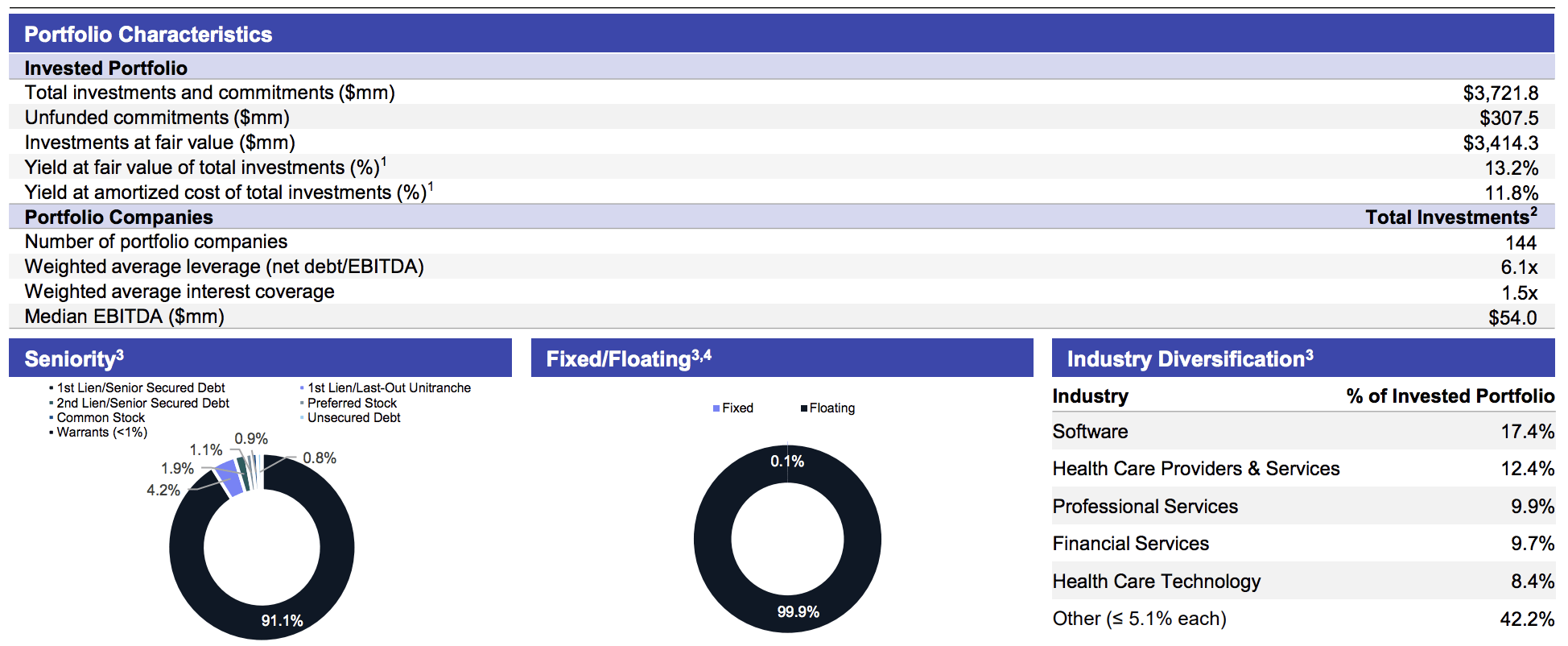

A look at the fund's portfolio shows that its 144 constituents have a weighted average interest coverage of 1.5x and a weighted average net debt/EBITDA of 6.1x. We consider these numbers extremely flimsy, especially given the uncertainty baked into the economic environment.

Nonetheless, having said the above, we don't think floating interest rates add fundamental risks for the time being because we strongly believe that future interest rates will be lower. In addition, Goldman Sachs BDC is sector diversified, with its main holdings spanning cyclical (Financial Services) and non-cyclical (Health Care Providers & Services) industries, phasing out some of its flimsy multiplier risks.

Goldman Sachs BDC

The following diagram shows a time series of Goldman Sachs BDC's asset value and earnings. Below the figure, I discuss our outlook on the components.

Goldman Sachs BDC

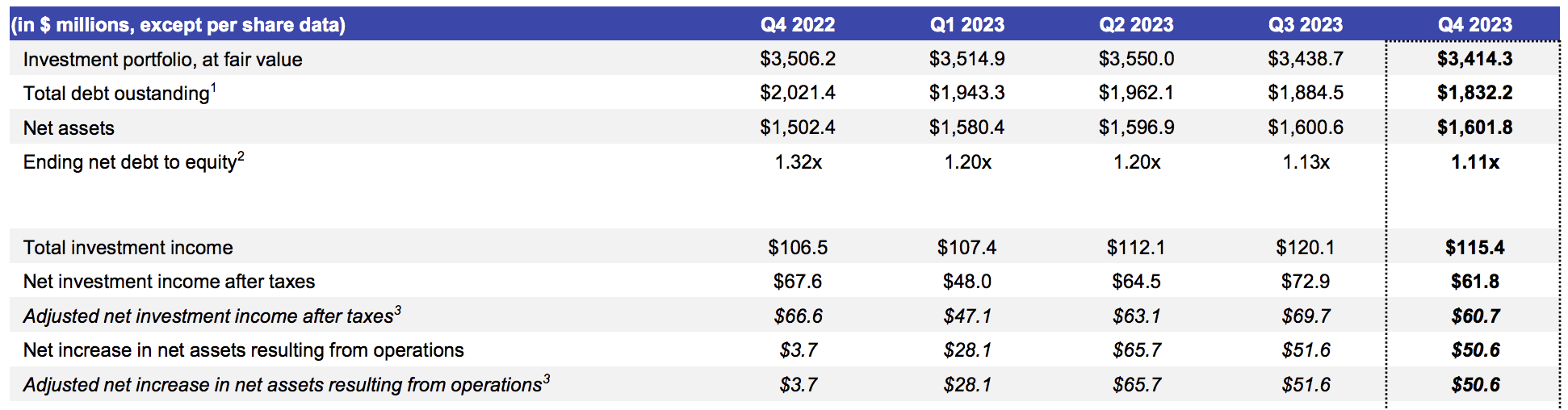

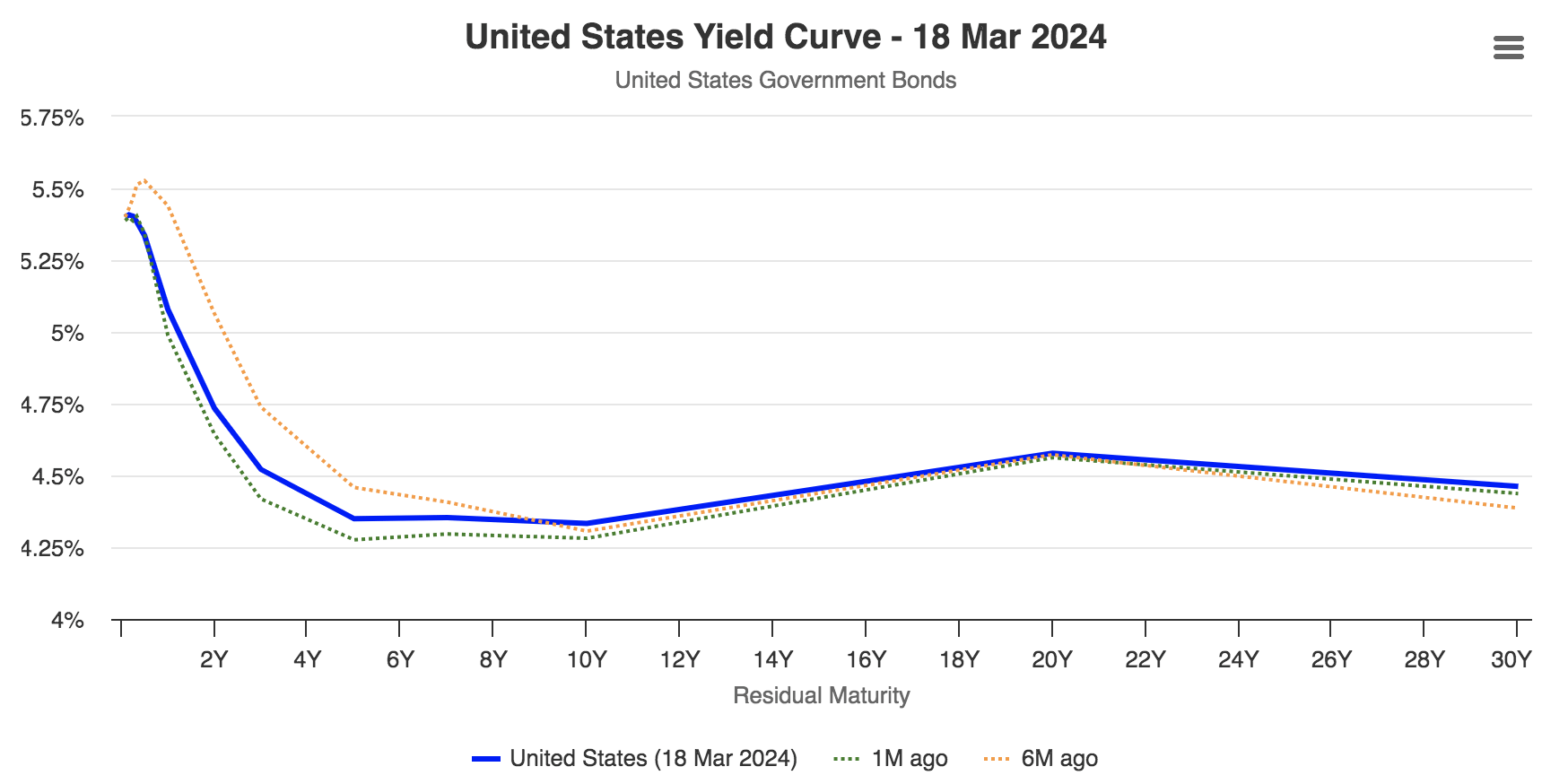

Goldman's results present a few interesting talking points. The U.S. yield curve and credit spreads maintained their usual inverse relationship during the past year, which is reflected in Goldman Sachs GSBD's results.

The fund's earnings from investments increased by 8.35% year-over-year, reaching $115.4 million. In addition, Goldman Sachs BDC's net asset value reached $1.602 billion, expanding by 6.6% year-over-year. A positive correlation between fixed-income asset value and income may seem unusual, but 90.9% of Goldman Sachs BDC's portfolio is floating-rate instruments, meaning negative or zero interest rate duration instruments are likely salient to the firm's portfolio.

worldgovernmentbonds.com

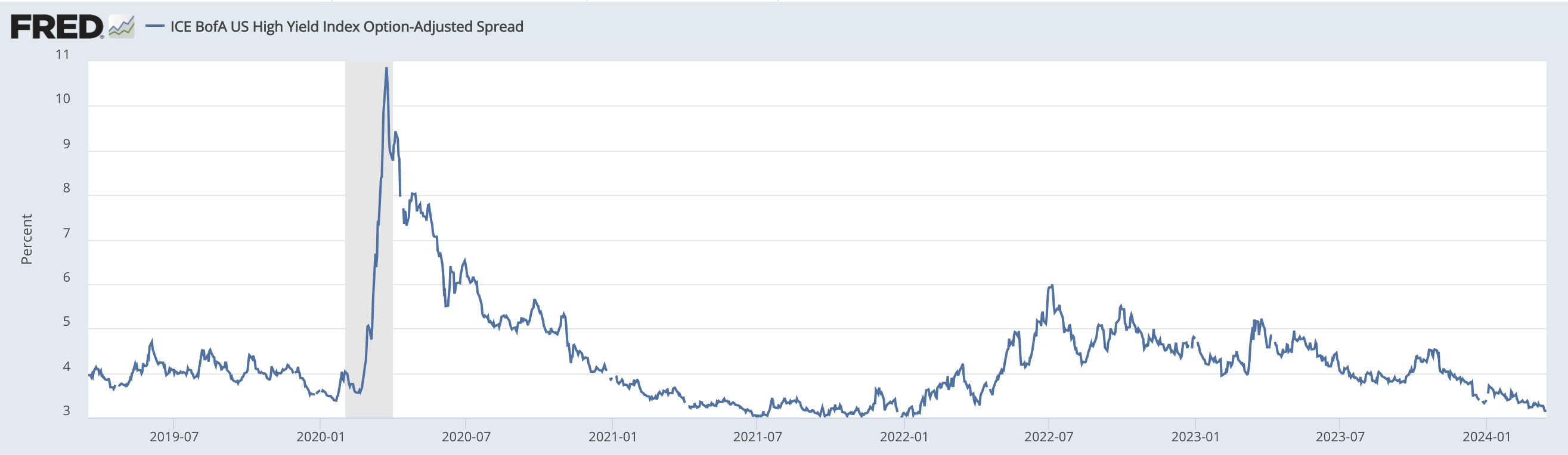

Despite its asset base showing arguably no negative sensitivity to interest rates, Goldman Sachs BDC's net asset value expansion and concurrent credit spread softening is no coincidence. We think the fund's first-lien exposure means it possesses a lot of positive credit spread duration (In other words, its asset value and spreads have an inverse relationship). However, the simultaneous income enhancement phases out much of the validity of our argument, as lower credit spreads would usually lower direct lending income.

St.Louis Fed

Our analysis leads us to the conclusion that this vehicle's income-based prospects are based on interest rates. However, credit spreads may have more of an impact on its net asset value. By assuming such a relationship, we think Goldman Sachs BDC's prospects may soften in the coming quarters. Our basis is that lower interest rates will eventually occur as year-over-year inflation shows softening. A drop in interest rates will likely send credit spreads higher due to the natural inverse relationship between the yield curve and the credit curve.

Unless the fund improves its funding costs by a significant amount (which is a possibility), we foresee lower net asset value and lower net income occurring during the latter stages of this year and into 2025.

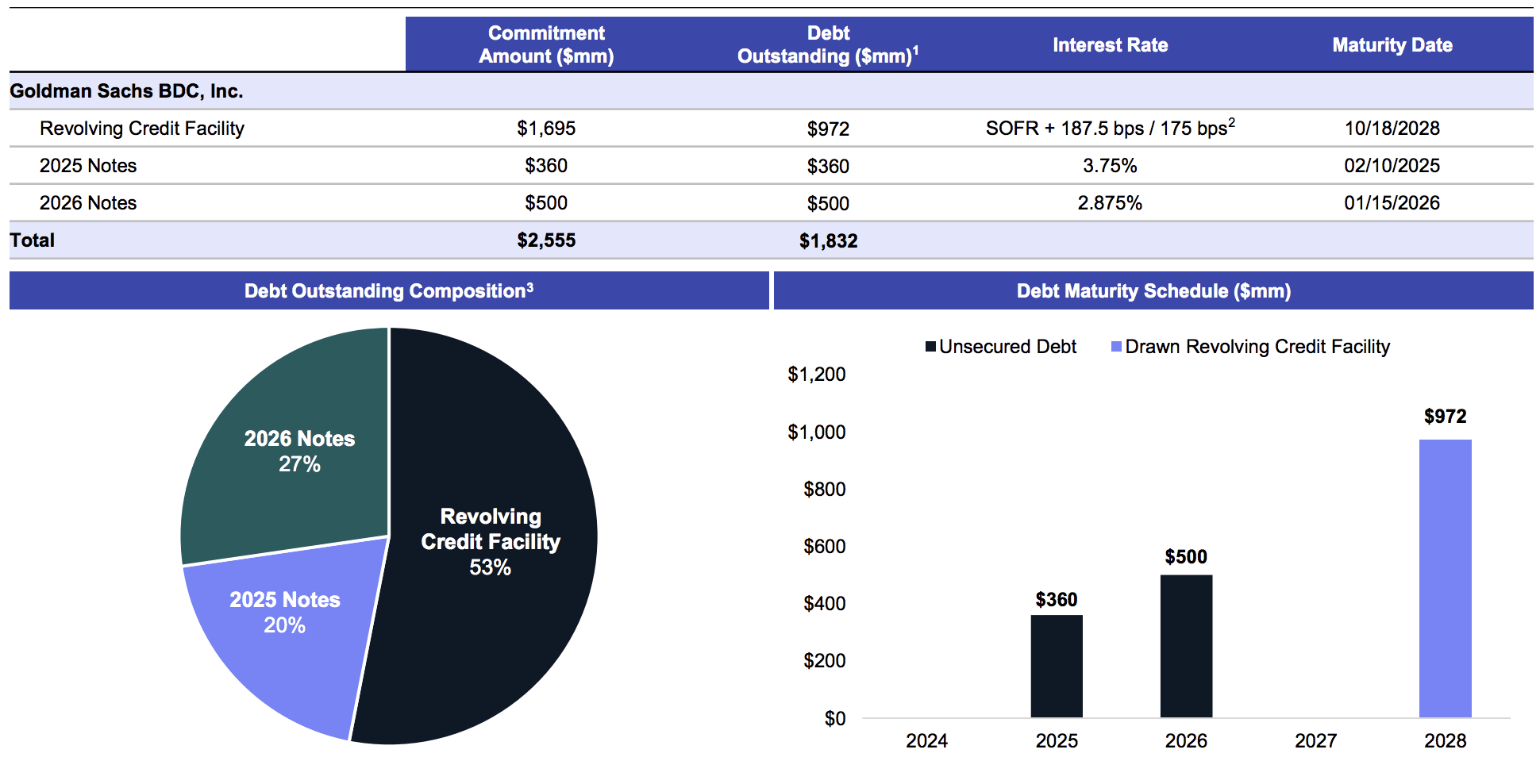

The Fund's Capital Structure (Goldman Sachs BDC)

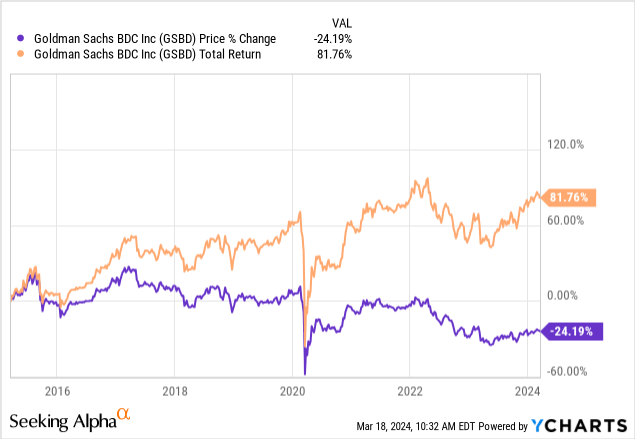

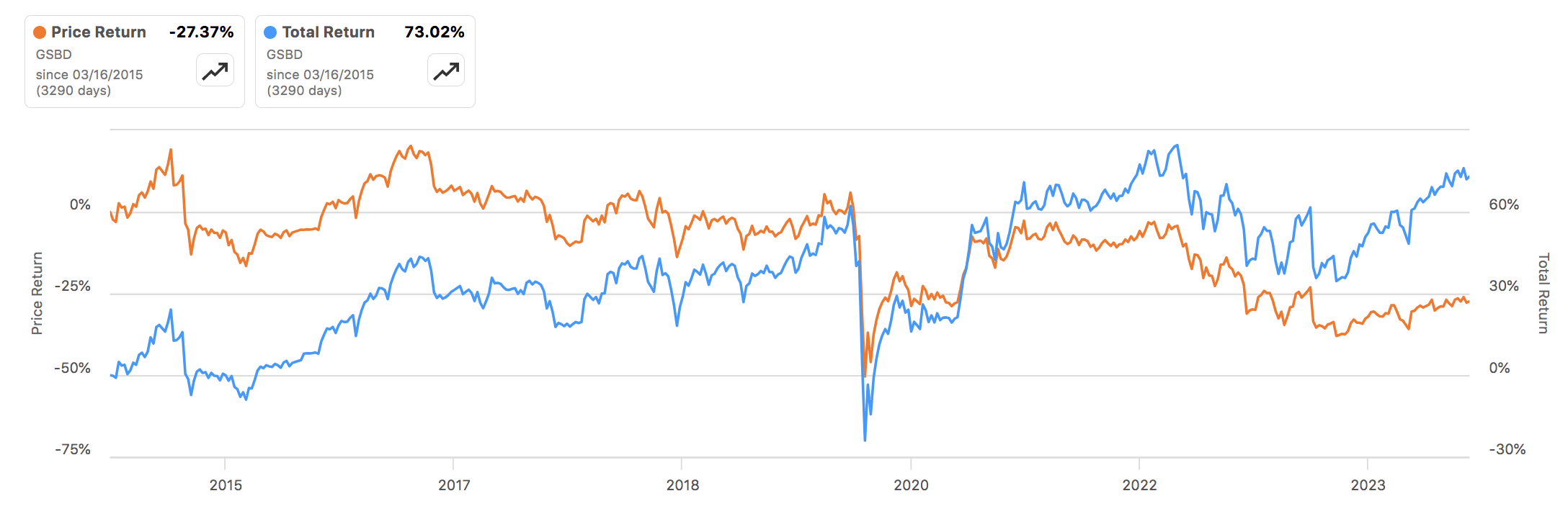

Most of Goldman Sachs BDC's past returns stemmed from income. In fact, investors have experienced negative price returns since inception. Therefore, we think a valuation analysis of the fund functions as a risk assessment more than anything.

Seeking Alpha

An intraday market price on March 18 divided by Goldman Sachs BDC's latest measured net asset value per share translates into a P/NAVPS of 1.04x. We don't see much relative under/overvaluation in this and deem the asset fairly valued on a trailing basis.

| Metric | Value |

| NAVPS | $14.62 |

| Market Price | $15.15 |

| P/NAVPS | 1.04x (rounded) |

Source: Seeking Alpha

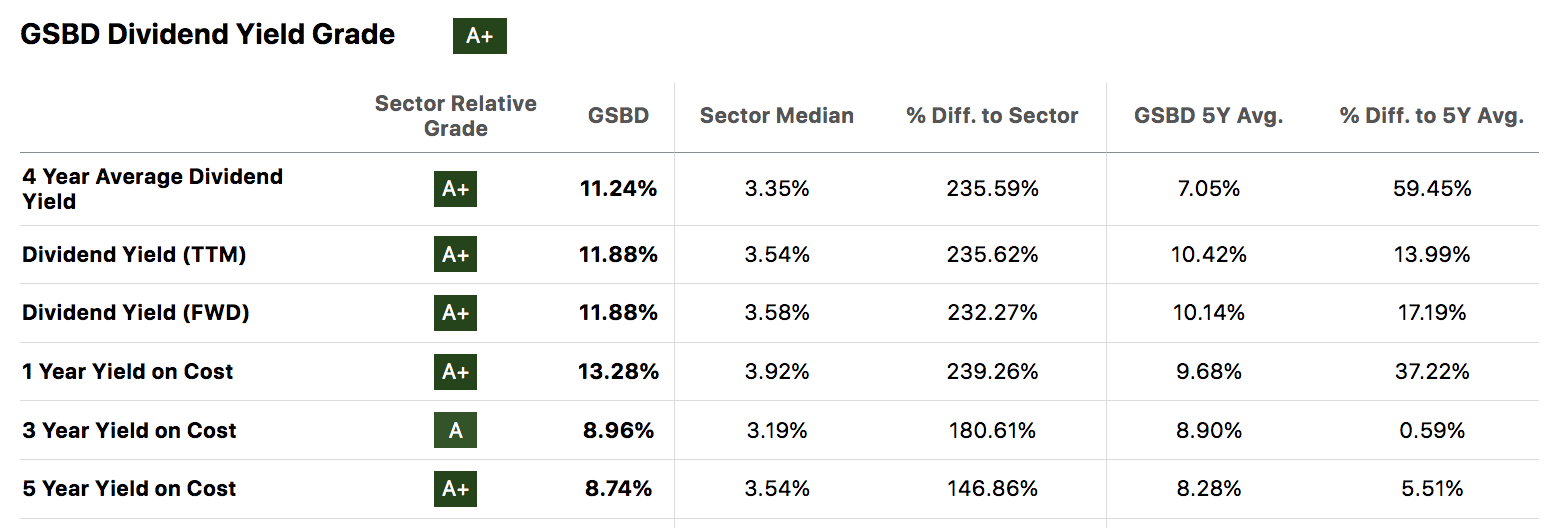

Goldman Sachs BDC's dividend profile raises another conversation altogether. Key metrics suggest the security has best-in-class dividend attributes. For example, Goldman Sachs BDC's yield on cost metrics suggests investors can enter a position at any time and still receive a good dividend. However, we do encourage considering that its dividends are cyclical in nature.

Seeking Alpha

Our view is that Goldman Sachs BDC could experience soft performance for the remainder of 2024. We think a changing interest rate and credit spread environment will dent its portfolio's net asset value and interest income. Moreover, we are worried about the fund's interest coverage and debt/EBITDA ratios, given the uncertainty baked into the economy.

Despite our worrisome outlook, we don't think the asset is a hard sell. Therefore, we assign a hold rating to Goldman Sachs BDC.