skodonnell

skodonnell

Gold Royalty Corp. (NYSE:GROY) – a Vancouver-based gold-focused royalty company – appears to be well-positioned to benefit from the robust gold price rally that may be coming in 2024.

The company's financials are gaining positive momentum, indicating a turning point in profitability in 2024 and renewed growth in 2025 and beyond through organizational streamlining and greater revenue contribution from expected higher attributable production of gold equivalent ounces.

This outlook fits well with retail investors' expectations of achieving significant appreciation through this asset, so GROY was among the “Top Gold Stocks for 2024”, although the investment risk on this stock is far from negligible.

With 39 royalties generated since 2021 through the acquisition model, which comes with a low cost to manage mineral interests, the company has historic potential working in its favor. The retail investor, who now feels a greater aversion to riskier assets such as US-listed stocks, will remain rational, knowing that past events are no guarantee of future returns.

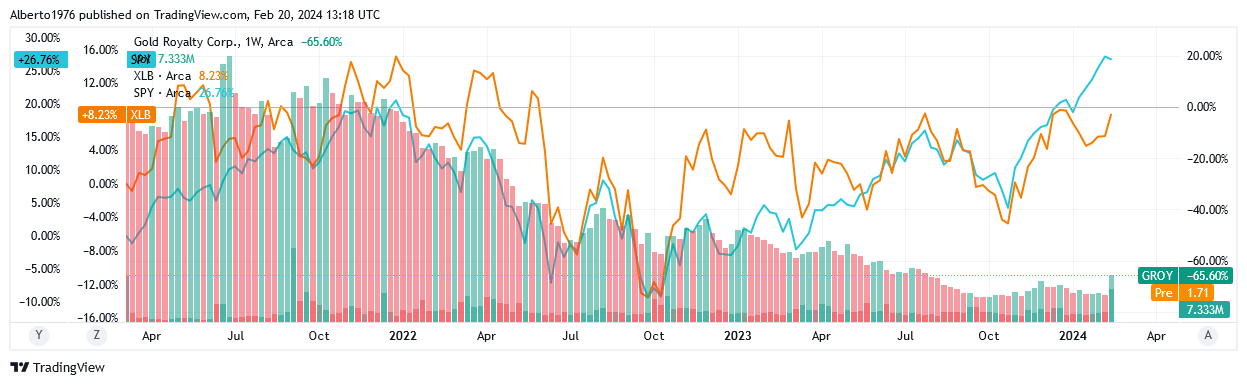

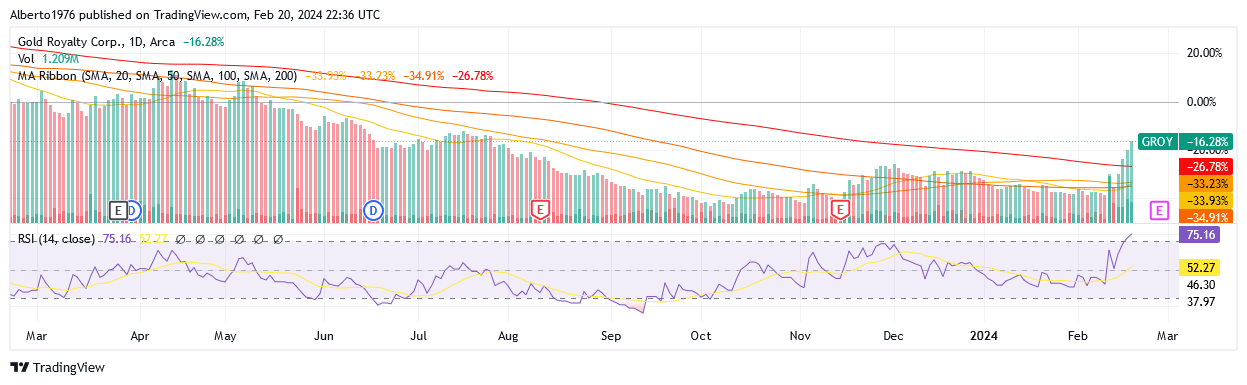

This sentiment was reflected in the following chart: Since initial trading on the NYSE American in March 2021, GROY share price has fallen by more than 50%, while the largest US-listed stocks and the materials sector have instead gained, leaving GROY shareholders quite behind.

Source: TradingView

In addition, the financial market offered an average yield of around 3% for 10-year US Treasury bonds, which rose from 2 to 4% and reached a peak of 4.9% at the end of October 2023, which undoubtedly reshaped most of the market's attention for risk-free investments. Against this background, GROY is still unable to pay a dividend.

The highly uncertain outlook due to the ongoing macroeconomic situation and major conflicts in Ukraine and Gaza is contributing to particularly stubborn core inflation and increased risk aversion to investments in riskier assets. In these very treacherous investment waters, risk-free bonds are still preferable to gold, as long as central banks keep interest rates high to counterbalance the actual economic situation and thus keep demand away from gold royalty stock GROY. Plus, until the company has demonstrated the inflection point proposed by the market, the shares will also continue to be considered quite speculative and therefore exposed to all relevant risks.

The retail investor still has the opportunity to mitigate this risk if he succeeds in taking advantage of a decline share price for GROY stock, which is possible as a result of an economic recession gaining momentum over time. Time will be the retail investor's ally, freeing him from having to rack his brains to understand if and when the company will be able to generate positive returns and be profitable. Exactly what banks do in this particular cycle of expensive loans to offset the increased risk of insolvency when assessing the feasibility of an investment project. They assess companies' resilience to adverse economic conditions before granting further financing or refinancing for a larger project. This is the scenario just described and a high interest rate is a measure of how reluctant banks are in lending, as they place a much higher value on liquidity today than in times of economic expansion. Fed Chairman Jerome Powell and US Treasury Secretary Janet Yellen are urging banks to preserve their liquidity instead of investing money during this difficult time for the economy. Currently, banks are being proposed to cut their dividends, postpone buybacks, and use higher profits to increase provisions for the high risk of losses due to weakness in the commercial real estate sector and others.

Given the uncertainty surrounding GROY's prospects, compounded by the current economic and geopolitical turmoil, why shouldn't retail investors exercise the same caution shown by financial institutions?

Staying on the sidelines for now also helps, because before the economic slowdown leads to a drop GROY share price, the company will undergo an important test where it will have to demonstrate further expansion of its gold royalty portfolio and, more importantly, achieve a positive net income that the market is hoping for. This will insulate GROY stock from gold price volatility, which has great appeal for retail investors with its rapid upsides, but these alone are not enough to guarantee that GROY will develop into a profitable company.

A lower level of share price represents an effective buffer against the risk that the desired growth target will not be achieved. It minimizes the loss if the investor exits or reduces the position and provides a greater chance of a strong upside in the event of a sustained recovery in gold prices.

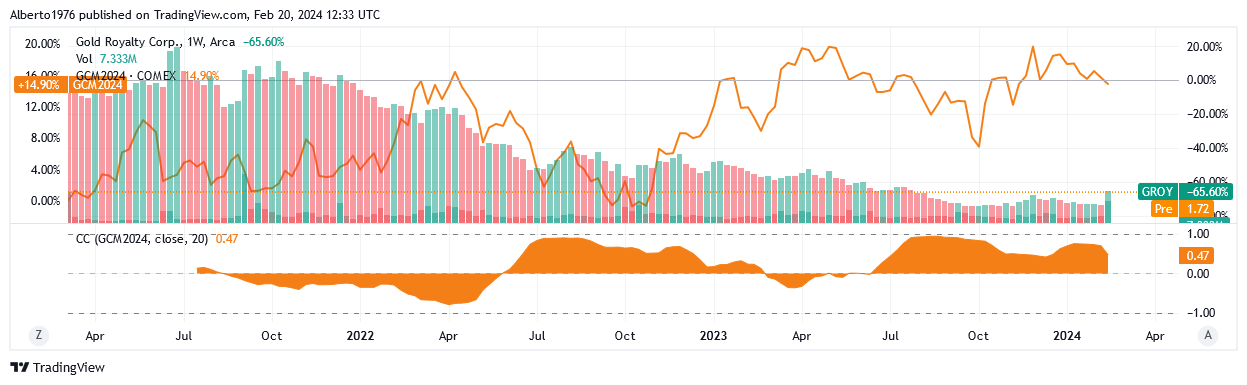

Should there be an economic downturn in the cycle, the hunt for safe-haven gold is the red carpet for a gold bull market in 2024. Analysts at Trading Economics point to a higher 12-month price of $2,112.48/oz compared to the $2,029/oz at the time of this article, a boost to GROY's prospects and stock price.

Source: TradingView

The dynamic illustrated is driven by the positive correlation between GROY and the price of gold or the benchmark of the gold futures (GCM2024), represented by the yellow area in the bottom section of the chart above. A positive correlation means that when gold prices are affected by bullish sentiment, GROY shares are also driven by positive winds.

These 3 indicators predict a recession:

a) Duke professor and Canadian economist Campbell Harvey's inverted yield curve for the spread between a 10-year yield of 4.273% and a 3-month yield of 5.378% US government bonds. Under normal circumstances, shorter terms mean thinner returns than longer-term loans because the risk of the borrower defaulting is remarkably lower. When shorter-term returns instead exceed longer-term returns, it indicates an abnormal condition determined by the short-term future considered riskier and highly uncertain than in calm times. Subsequently, the shift warns of difficult times for the economy.

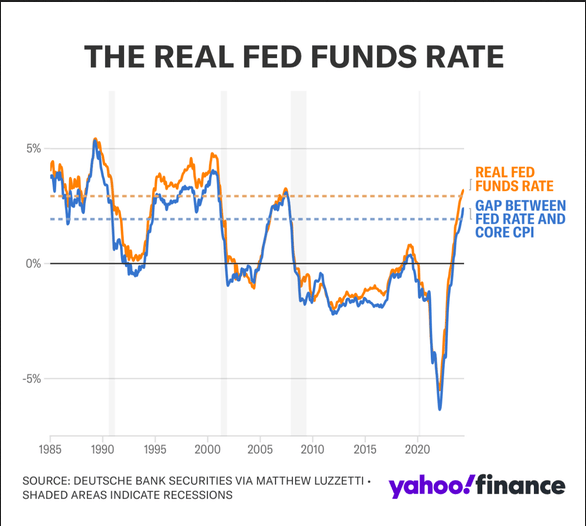

b) The postponement of the Fed's first interest rate cut causes the Fed's real interest rate to reach high levels that have often previously been associated with a subsequent economic slowdown or recession.

Source: Deutsche Bank Securities via Matthew Luzzetti - reported by Yahoo Finance

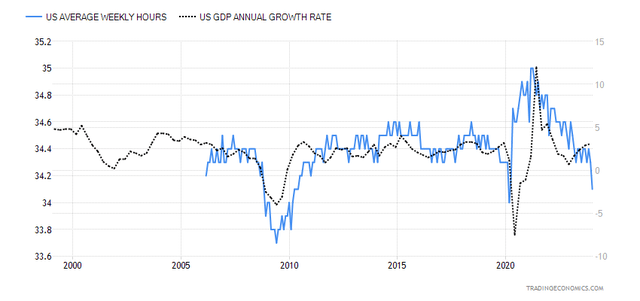

c) The labor market still appears resilient to most market participants, but the decline in average working hours leads Lakshman Achuthan, co-founder of the Economic Cycle Research Institute, to suggest that this trend may herald a recession based on similar comparisons in the past.

Source: Trading Economics

However, it will take some time for the market to recognize the recession as a problem for the business cycle. Presumably, the first rate cut by the markets can be seen as a signal that the Fed is starting to counteract the more negative consequences of the economic slowdown. Last week's inflation data, which turns the near certainty of rate cuts in March into the hope of rate cuts in June among rate traders, shows that the Fed is right to be cautious and not rush its first-rate cut. At present, judging by economic data as it comes in, it cannot be ruled out that the Fed will start reducing interest rates from the second half of 2024, as a generally robust labor market does not allow the disinflationary process to advance smoothly toward the 2% target. However, the economic cycle will inevitably fall into recession, as this is the aim of restrictive monetary policies to reduce high inflation.

As mentioned, the recession is the driving force behind the bullish sentiment around gold, but initially, the financial market will not move rationally, so with GROY in the headwind too, its shares will not be differentiated from other US-listed stocks in the market. In line with the 24-month beta of 1.10x, the share price could deviate significantly to the downside from where it is as of this writing, and retail investors may want to maintain a Hold rating for the time being. As of this writing, shares traded at $1.80 per unit, giving it a market cap of $250.64 million and a 52-week range of $1.18 to $2.48. Shares are slightly closer to the lower limit than the upper limit of the 52-week range.

Source: TradingView

The stock is also above the 20-, 50-, 100- and 200-day simple moving averages. These levels are elevated relative to recent trends, but shares may well revert to a downtrend mode under negative pressure as an earlier (very irrational) consequence of the recession.

The 14-RSI of 75.16 indicates that shares have exceeded overbought levels, suggesting an impending price correction, which could be gaining momentum as the “higher-for-longer” interest rates policy remains effective, and the first cut is postponed. The situation does not bode well for gold and gold stocks such as GROY as these assets face the issue of a higher opportunity cost of holding the zero-yielding yellow metal rather than appealing fixed income on U.S. bonds.

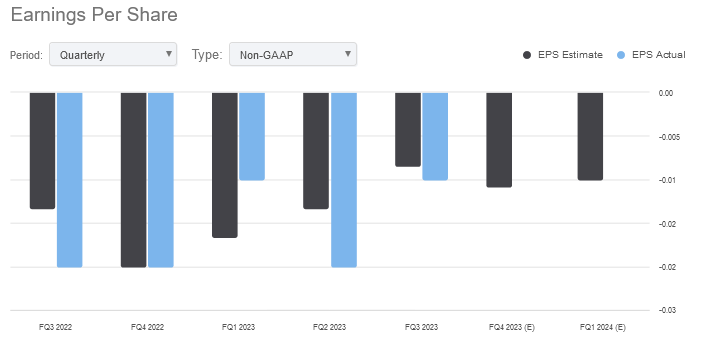

GROY reported a 48% year-over-year increase in total revenue and land agreement proceeds to $1.4 million in the third quarter of 2023, while pure revenue fell 8% to $797 million. Total revenue and land agreement proceeds were driven primarily by new revenue from a one percent-net smelter return royalty for Cozamin, a copper-silver mine in Mexico, which is operated by Capstone Copper Corp. (OTCPK:CSCCF) (CS.TO). For the full 2023, Cozamin reported copper production of 24,340 tonnes, supported by recoveries and grades in line with previous periods. For the full year 2024, production should be consistent with 2023, as cut-and-fill mining methods provide better returns than long-hole stoping methods, while the asset has mine life until 2030, and activities now focus on resource estimate updates.

Driven by higher top line and as the company streamlines its organization and eliminates unnecessary costs (in fact, total costs fell 40.5% year-over-year to $2.2 million), cash flow from operating activities, before working capital movements, improved year-over-year by 67% to $0.9 million in the third quarter of 2023. Despite higher sales and more affordable costs, adjusted net income per share was still a loss of one cent in the third quarter of 2023, although it improved from the adjusted loss of 3 cents per share in the comparable period.

Source: Seeking Alpha

The market is pointing to a positive net income for this year, with revenue and land agreement proceeds expected to be in the range of $5.5 million to $6.5 million.

The positive turnaround in the bottom line (the main driver of the share price), will be a consequence of significant investments and acquisitions made by the GROY company in the past, supported by a robust gold price.

In addition to Cozamin, GROY has secured a 2% net smelter return royalty and a royalty-convertible gold-linked loan on the Borborema gold open pit project in Brazil, operated by Aura Minerals Inc. (OTCQX:ORAAF), with a targeted annual production of approx. 66,200 ounces of payable gold over an initial 11.3 years of operations from early 2025. Recently, Aura said the ongoing improvement in the overall performance of the business is helping to advance the construction of Borborema.

Also, GROY will acquire a Québec-based royalty portfolio from SOQUEM (Société Québécoise d'exploration minière) in exchange for C$1 million of its common stock (≈411,242 common shares out of total shares outstanding of 145.72 million), while the following in its pipeline of mineral projects represent the best progress:

a) The Odyssey open pit gold/silver project (3% NSR over the northern part of the project), located in the heart of the Abitibi Gold Belt in Quebec, Canada, is enjoying strong quarterly gold production. Agnico Eagle Mines Limited (AEM) indicates that at Odyssey 20,000 ounces were produced in the fourth quarter of 2023 and are believed to continue to be produced in the years from 2024 to 2026.

b) Côté Gold Project (0.75% NSR royalty for the southern part of the project), 112 km southwest of Timmins, Ontario, Canada, begins initial production early this year. At a consistent production rate of 220,000 and 290,000 ounces per year, according to IAMGOLD Corporation (IAG):

“Côté Gold will be Canada's third largest gold mine with a life of operations of more than 18 years and significant growth potential”,

Commercial production is expected to be achieved in the third quarter of 2024.

c) Granite Creek Mine Project (10% NPI) underground mining in Nevada will continue to ramp up through 2024, with the South Pacific Zone - high-grade gold mineralization north of the underground mining - being the mine's primary horizon given its potential to be an important deposit in the future.

Gold Royalty Corp. (GROY) is a Canadian gold-focused royalty company that appears to be well-positioned to benefit from the robust gold price rally likely in 2024.

The market expects the company to have an inflection point as it converts net loss into net profit this year due to the rosy outlook for gold prices and a corporate model that increases royalty revenue at a low cost.

If the retail investor is rational, he will take advantage of the market uncertainty and wait for the stock price to retreat below current levels while the company gives evidence that it is on track to deliver earnings. In this way, the retail investor reduces the risk of investing in GROY stock.