Wirestock

Wirestock

Near the end of December 2023, pharmaceutical giant AstraZeneca PLC (AZN) announced a deal to acquire Gracell Biotechnologies Inc. (NASDAQ:GRCL). Gracell is a Nasdaq-traded Chinese company focused on developing cell therapies for cancer and autoimmune diseases.

The terms of the acquisition look like this:

The acquisition should close tomorrow on 22 February 2024. Shareholder approval was received yesterday.

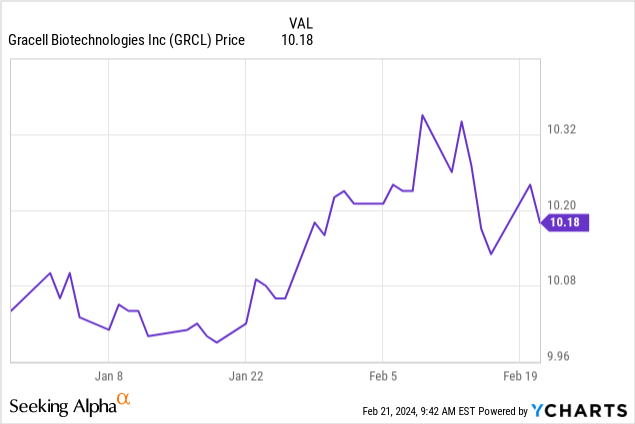

Gracell trades at $10.18, meaning the market is ascribing at least some value to the CVR:

Here is what the CVR agreement says (emphasis added by me):

Each CVR represents the right to receive $0.30, in cash, without interest, subject to any applicable withholding taxes, with such payment conditioned upon the receipt by Parent, any of its permitted assignees, any of their respective affiliates, or any entity that has obtained rights from any of the foregoing entities to file a biologics license application (a “BLA”) with the United States Food and Drug Administration or any successor thereto (the “FDA”) for authorization to market or sell any biologic product that contains the product candidate referred to by the Company as “GC012F”, the composition of matter of which is covered by certain Company patent rights in the U.S. (the “Product”),

or to register, develop or commercialize the Product in the U.S., on or prior to (i) December 31, 2028 of an accelerated approval granted by the FDA of a BLA for the Product for the treatment of multiple myeloma,

or (ii) December 31, 2029 of a regulatory approval (excluding an accelerated approval) granted by the FDA of a BLA for the Product for the first-line or second-line treatment of multiple myeloma.

This appears to be an unusually broad CVR that allows multiple ways to cash in on the full CVR. The milestone payments that I've seen in CVRs are almost always tied to a specific authorization or sales number obtained for a specific cause. Here, the company can keep looking for a problem that needs its solution.

AstraZeneca also said it would expend commercially reasonable effort to achieve the goals of the CVR. I think that's a wise decision; otherwise, they could get stuck in a situation where they would have to throw good after bad money to satisfy the CVR. The time restrictions constrain the CVR as well.

Given the broad CVR, the commercially reasonable effort, although not a very high legal standard for effort, is suitable here. In addition, the CVR doesn't apply to a secondary or tertiary asset. If the CVR doesn't come close to paying out, I think it is unlikely AstraZeneca will make money on this deal.

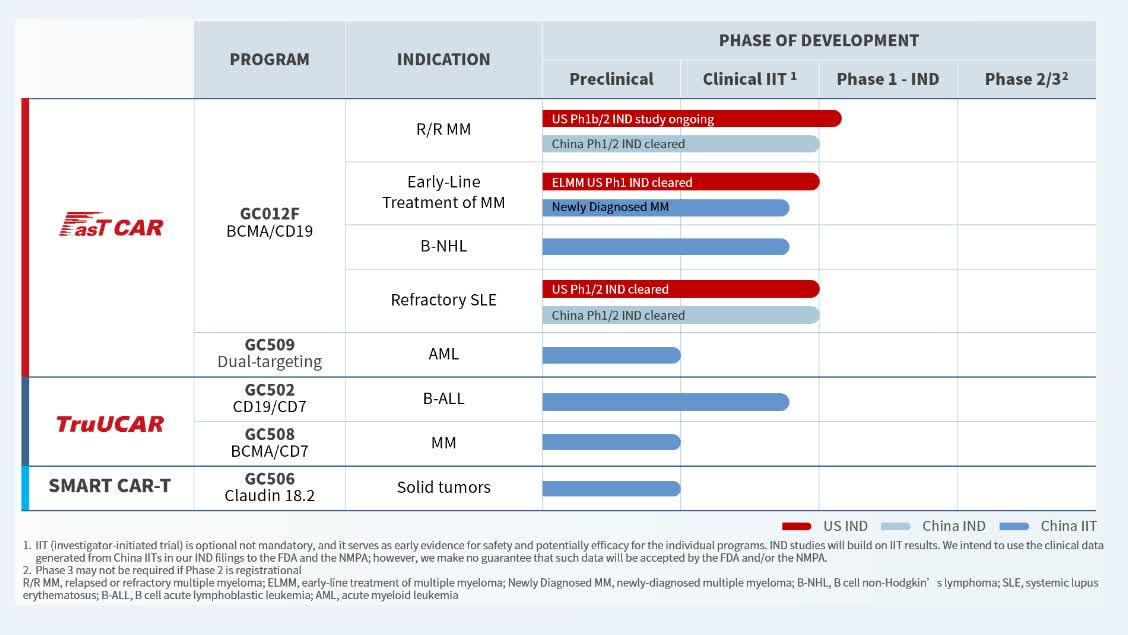

This is what the Gracell pipeline looks like:

Gracell pipeline (Gracell Biotechnology)

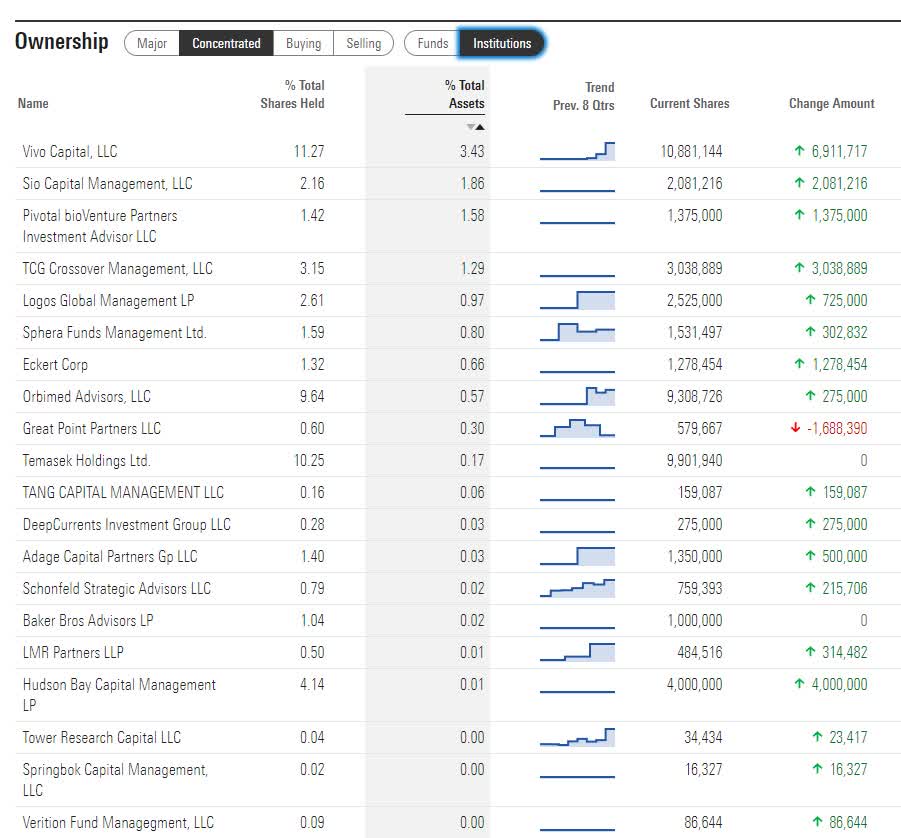

There are quite a few specialist healthcare investors that hold shares in this firm:

Gracell shareholder register (Morningstar.com)

I think that's an essential positive because it increases the odds that this company is developing something with a real chance.

The acquisition was also executed opportunistically with a lot of pressure on biotech as a whole and specifically on firms with links to China. This may also have helped to motivate management to sell the firm. If the company would experience restricted access to U.S. capital markets (in practice, if not regulatory), things can get hairy quickly for cash-burning biotechs.

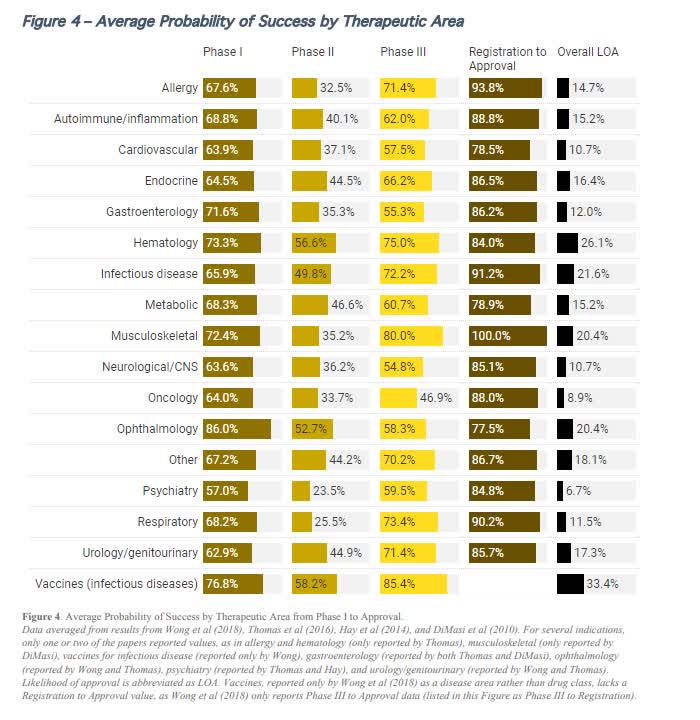

My go-to baseline for probabilities of success for clinical trials is this paper:

Probability of trial success (Alacrita consulting)

Based on this data, phase 2 and 3 trials are very challenging in oncology.

I'm unsure yet how to assess the probabilities here. There are multiple shots on goal, but these aren't strictly independent. There is also a possibility the phase 3 trial isn't necessary (see company slide). However, if it fails a phase 2 trial because it isn't safe, odds likely go down a lot. It seems unlikely it would be safe.

Yet, if I'm extremely bearish here and assume there is one shot of getting something through three phases of trials, using the odds associated with the baseline oncology path (ignoring there are quite a few specialist healthcare investors on the shareholders register), the probability of getting there is 0.64 x 0.33 x 0.47. That means there would still be a 10% chance of hitting the CVR payout. 10% of $1.50 = $0.15. It will be some time before this pays out, so I should consider the time value of money. I like to start out with a very high discount rate. At a 20% discount rate, the present value of the CVR is at least $0.06.

The shares trade $0.18 above the $10 acquisition price. If this bearish scenario is getting me close to the true probabilities, the current share price sets me up for an expected loss of 2/3rds of the capital that gets tied up.

I need an expected payout of around $0.4977 in 5 years to have a present value of $0.20 today using the same 20% discount rate.

Suppose, I'm somewhat less bearish. I'll give credit for two paths to victory. The company also has an application of its therapy for an autoimmune disease. There is a 16% chance that it gets to the end of the line according to the Alacrite baseline odds. That's another $0.24 in expected value. Based on a 20% discount rate over 4 years, the present value of $0.24 today is approximately $0.12.

If I add up $0.06 and $0.12, that's $0.18, and that's exactly where the CVR trades.

If I use a less aggressive discount rate in this less bearish scenario (note that I may be getting myself in trouble here), things quickly start looking quite attractive.

With a discount rate of 12%, the present value of $0.39 in 4 years is roughly $0.2479. This is already well above where the CVR trades.

With a 6% discount rate (could be justified given where AstraZeneca's bonds trade), the present value of $0.39 in 4 years is approximately $0.3089. Which is around 50% above where the CVR trades.

There are myriad ways to create more bullish estimates of the value of this CVR. I could raise the odds of success because of the expert shareholders involved, I could give credit for other ways to achieve the milestones, etc. The company may not need a phase 3 trial (in 1 or multiple paths toward a BLA), which increases the odds by a lot. My confidence in assessing the likelihood of any and all these bullish scenarios is very low.

However, I do think the bearish scenarios are quite punishing. Discount rates are something that can be different for each investor. What I like about these CVR payments is that they're uncorrelated from the market. I can talk myself into accepting lower rates of return if returns are uncorrelated. This leads me to the conclusion that the market values the CVR at worst in the neighborhood of "fair value."

I don't think this is the most fantastic CVR to pick up ever. However, I like it enough to ensure I'll get some in my portfolio. When I test the value using what I consider a mix of bearish assumptions, it appears fairly valued by the market. Yet, there are many circumstances (especially the broad CVR with a multitude of paths to success) and the presence of strong specialist healthcare investors on the shareholder register that allow for more realistic or bullish scenarios.

Editor's Note: This article discusses one or more securities that do not trade on a major U.S. exchange. Please be aware of the risks associated with these stocks.