peangdao/iStock via Getty Images

peangdao/iStock via Getty Images

No doubt about it, following the news that housing starts and permits are down early in the year, this is a time few people are looking at home-builders to invest. It's understandable, but as a contrarian, when there's blood in the streets, there's time to start looking for gems.

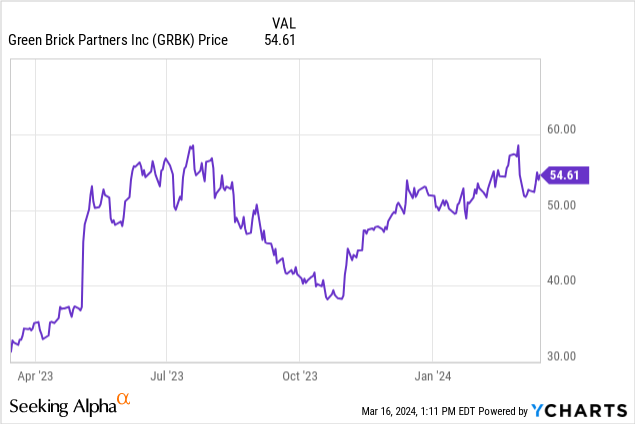

Today's diamond in the rough is Green Brick Partners (NYSE:GRBK), a Texas-centric homebuilding and land development company. In spite of a comparatively down market, they managed to break a lot of new records this most recent quarter and fiscal year, and all indications are that's going to continue going forward. With a very value-friendly P/E ratio, there's a lot to like here.

Green Brick builds homes in a very selective marketplace, centering heavily on Dallas-Fort Worth (DFW), and Austin, Texas. They have carefully selected desirable locations and are building an inventory of lots and even of backlog housing units ready to be sold.

Perhaps the most exciting market is the one they're just about to enter: Houston. With the first transaction made in Huffman, TX, just outside of downtown Houston, they are prepared to start construction in Q2 of 2025, putting them in the market which saw the largest number of new home constructions in 2023.

Beyond Texas, Green Brick is very selective in where to build, mostly centering on metro Atlanta and Florida's Treasure Coast. All locations have one thing in common, a strong economy and younger than average population, which means plenty of new home-buyers to court.

2023 saw record home-closing revenue for the company, and record gross margins in the range of 30.9%. New orders increased 70% year over year, and a record 3,356 homes were sold. All told, Green Brick not only grew fast, but had the highest growth among its peers.

Green Brick builds around subsidiaries, like Trophy, which they own 100% in. Trophy grew admirably, founded in 2018, selling its first 33 homes in 2019, and today managed a full 1,378 home closings for 2023. Needless to say, that's the kind of growth we like to see.

| 2021 | 2022 | 2023 | |

| Residential Revenue | $1.31 billion | $1.7 billion | $1.77 billion |

| Cost of Revenue | $964 million | $1.2 billion | $1.22 billion |

| Diluted EPS | $3.72 | $6.02 | $6.14 |

(source: most recent 10-K from SEC)

Here we can see growth at Green Brick overall, with residential revenue steadily climbing and diluted EPS hitting a new record in 2023. Estimates show $6.84 and $7.41 in the upcoming years, both of which keep the P/E well into the value range, and with Houston's market likely to come online thereafter for them, it's only a bright future to look forward to.

| Cash and Equivalents | $180 million |

| Inventory | $1.5 billion |

| Total Assets | $1.9 billion |

| Total Liabilities | $549 million |

| Shareholder Equity | $1.3 billion |

| Price/Book | 1.85 |

(source: most recent 10-K from SEC)

Financially, we can see a very high inventory and a secure amount of cash on hand, keeping the company responsibly financed. The price/book value is also a decent value figure, particularly when the company is experiencing such growth and profitability, and seems well lower than the median for the sector.

Oh, and the book value is growing too, with 2023 enjoying a book value increase of 26% over the prior year. If this growth continues, and the earnings estimates suggest it will, it should serve as a catalyst once investors stop being so scared of the homebuilders.

One number that stands out as a possible risk is the backlog units, with the year ending in 770 unsold homes worth around $555 million, up from 537 and $369 million in 2023. That's a fair lot of inventory that's starting to build up, and Green Brick is so prolific you can't help but wonder if they are building them faster than they can sell them, even in their desirable markets.

Already, inventory is in excess of stockholder equity, and while that's not entirely uncommon for the company given what they do, if the growth continues in that direction they may start to have an unbalanced book.

Other risks include vulnerability to inflation or deflation, and the possibility of negative changes in their operating markets. Obviously, neither Dallas nor Austin nor Atlanta is due for a precipitous economic downturn, but growth in sales is continued to be based around the theory of growth in the metro communities. The move into Houston should allow them to diversify a bit more, and be less vulnerable to a single event.

Seasonality is also something to be aware of. In general, the sales are highest in the spring and summer, and lowest in the rest of the year. This means keeping a particularly close eye on the company in the high-end parts of the year, and being ready for sales to be a lot lower in the autumn and winter.

Green Brick lays out its strategy pretty plainly in the 10-K, focusing on acquiring and developing land in desirable locations, and holding an extensive inventory or parcels that can sell in 24-72 months.

I already talked about the importance of growing economies in the regions they operate, after all, people will be more ready to buy first homes if they have good jobs and economic opportunity. The cities seem to have been well selected in this regard, and Houston, the one glaring omission in their Texas-heavy portfolio, is only going to underscore that.

With a P/E ratio in the single digits and analysts projecting solid growth in the years to come, things are looking up for Green Brick. I understand the reticence about investing in a homebuilder after the news, but metro areas aren't created equal, and homebuilding in DFW and the other markets is a lot different than, say, building in marginal areas in the northeast.

With market sentiment being what it is, this is a perfect time to consider adding Green Brick to a portfolio, though keeping in mind that Houston won't be fully online for a few years and that means a need to be patient.

Being patient never hurts with investments like this, however, and going forward I would expect big things to come. There is no obvious external catalyst with this stock, however the low P/E and better than sector price/book should eventually shock investors back into treating Green Brick as it always deserved.