Kokkai Ng/iStock Unreleased via Getty Images

Kokkai Ng/iStock Unreleased via Getty Images

Over two years ago, when I heard about Grab Holdings Limited (NASDAQ:GRAB) going public at a $40B valuation, my initial reaction was that the company was probably overpriced.

Looking back, I was right about this.

Without even doing any research, I also made the uneducated conclusion that the on-demand business model in Southeast Asia might just be unsustainable and would remain unprofitable for all eternity.

As it turns out, I was dead wrong about this — in Q4, the company turned GAAP profitable for the first time ever.

Seeking Alpha

So after a flip to GAAP Net Income positivity and after an 80% decline in the stock price, I figured there might be some value in the stock — so I looked into it.

After doing some research, I realized that Grab is a tech giant in hibernation.

With that being said, grab (pun intended) a cup of coffee and get cozy, because this is a deep dive into Southeast Asia's superapp. Enjoy!

A little over a decade ago, two Malaysian-born Harvard Business School students — Anthony Tan and Tan Hooi Ling — teamed up to pitch a business idea for the HBS New Venture Competition in July 2011.

Anthony Tan, having grown up in a family that owned one of the largest automobile businesses in Malaysia, and Tan Hooi Ling, having experienced Malaysia's nightmare taxi industry while working at McKinsey, decided to replicate Uber's (UBER) ride-hailing service in the U.S. and bring it to their home, Malaysia.

As it turned out, the pair finished second place in the competition, winning $25,000. With that prize money, they launched the taxi-hailing mobile app, MyTeksi, in June 2012.

MyTeksi quickly gained traction in Malaysia, as it offers safer and more reliable taxi rides. Eventually, the two founders realized that they could offer the same service in neighboring countries where ride-hailing technology is still nonexistent.

Without hesitation, they rebranded the company as GrabTaxi and entered other Southeast Asian markets over the next few years, including Singapore, Indonesia, Thailand, the Philippines, Vietnam, Cambodia, and Myanmar.

In addition, in 2014, GrabTaxi secured its first major funding of $65M from outside investors, enabling the company to launch additional services and more importantly, compete effectively against other ride-hailing platforms that have just launched as well — including Uber, which Grab ended up acquiring in 2018.

In 2016, the company rebranded to Grab. Fast forward to 2021, Grab went public in the U.S. through a SPAC merger with Altimeter Growth Corp., valuing the company at $40B, which, at that time, was the largest-ever U.S. equity listing by a Southeast Asian company.

App Store

Today, Grab is the leading superapp in Southeast Asia, offering deliveries, mobility, financial, and enterprise services, connecting millions of consumers, merchants, and partners across 500+ cities and 8 countries — all in a single platform.

Grab 2022 Investor Day Presentation

In essence, Grab is the everyday app for everyday consumers — the company focuses on everyday transactions such as transportation, eating, paying, and more.

Grab wants consumers to live and breathe within the Grab ecosystem.

More importantly, through these transactions and interactions within the ecosystem, Grab aims to drive Southeast Asia forward by creating economic empowerment for everyone — that includes consumers, drivers, and merchants.

That's what a superapp is all about — and Grab might just be the only company that has a chance of achieving and maintaining "superapp" status in Southeast Asia.

Why?

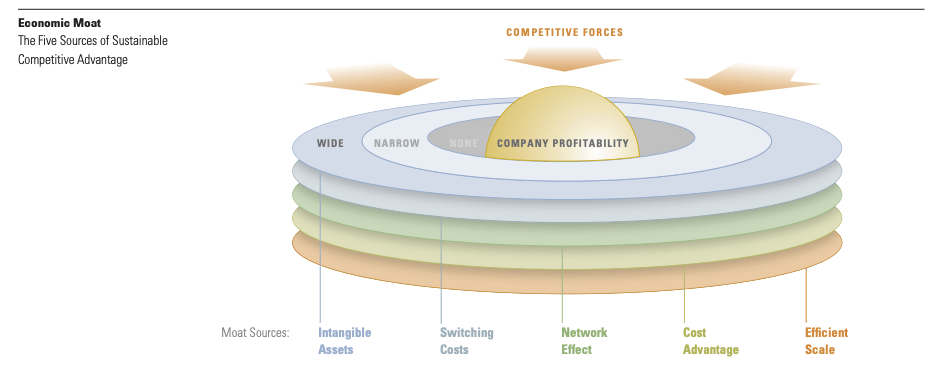

Because Grab has some of the most impenetrable moats I've ever seen in a business.

According to Morningstar, there are five sources of sustainable competitive advantages.

I believe Grab has all five.

Morningstar

Intangible Assets

Per Morningstar:

Intangible assets are things such as patents, government licenses, and brand identity that keep a company ahead and competitors at bay.

Without a doubt, Grab is one of the most powerful brands in Southeast Asia. Just like Uber, it is a household name — a verb.

"I don't have a car but I can just Grab later on."

"I'm hungry. You wanna Grab some food?"

"I can't meet you tonight. I'll just Grab the documents to you".

It's very difficult for companies to become a verb — only the best do.

And Grab is the best.

Everywhere you go in Southeast Asia, you see Grab's green logo embossed on its fleet of cars, on the jackets of its riders, and at the checkout point of its merchants.

I can say this confidently because I'm a user myself who lives in Indonesia and travels frequently to Singapore — two of Grab's largest and most important markets.

Southeast Asia is literally turning greener by the day because of Grab.

That speaks volumes about its brand identity and power.

Switching Costs

According to Morningstar:

Switching costs are obstacles that keep customers from changing between products, like from one company’s product to a competitor’s.

Imagine having a state-of-the-art everyday app with all the features and services that fulfill your daily needs — all at your fingertips. Furthermore, you get the most complete catalog of transportation types, merchant providers, and food items. Service quality — including speed of execution, ease of use, customer service, etc. — is also top-notch.

Now why would you use a different app that offers fewer services or lower quality?

Price is one reason, but other than that, I don't see any other reason why you would switch out of the platform.

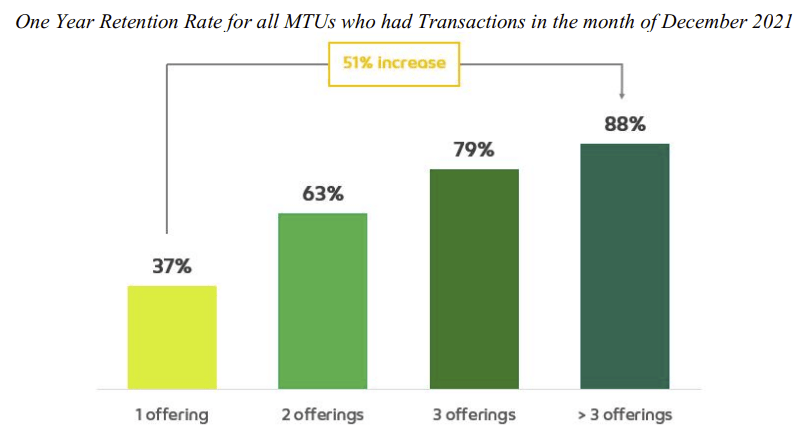

Moreover, as Grab introduces additional products and services on its platform, the more offerings consumers use. And the more offerings consumers use, the more loyal they become.

As you can see, retention rates increase meaningfully as consumers use more offerings, from as low as 37% for one offering, to as high as 88% when they use more than three offerings.

Grab FY2022 Annual Report

Additionally, subscription services such as GrabUnlimited and rewards programs such as GrabRewards are driving even higher engagement within the platform, further amplifying Grab's switching cost moats.

For instance, GrabUnlimited subscribers now account for one-third of Deliveries Gross Merchandise Volume (GMV) with subscribers spending 4.2x more on food deliveries than non-subscribers.

Not only that, Grab sees similar trends in its financial services segment (emphasis added):

We continue to see strong ecosystem uplifts from our payments and lending business, with users from GrabPay spending 4 times more and having 1.5 times higher retention rates than cash users. Our driver partners who take on a loan with us also recorded 1.5 times higher retention compared to drivers without a loan.

(COO Alex Hungate — Grab FY2023 Q3 Earnings Call)

More offerings drive higher cross-sell rates. Higher cross-sale rates drive higher retention rates. Higher retention rates drive higher spending, which ultimately leads to higher quality, more stable Revenue generation.

That, my friend, is high switching cost moats at play.

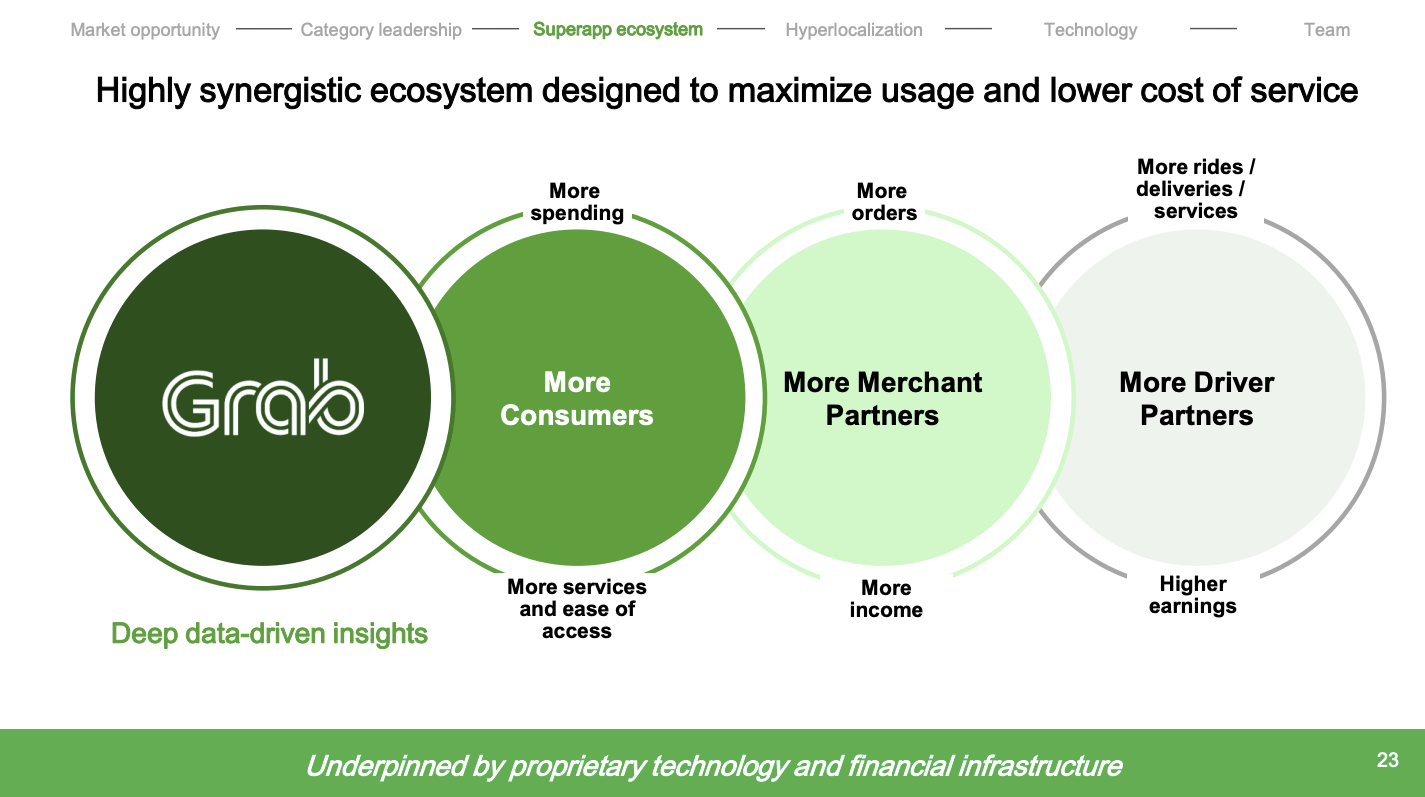

Network Effect

As described by Morningstar:

Network effects occur when the value of a good or service increases for both new and existing users as more people use it.

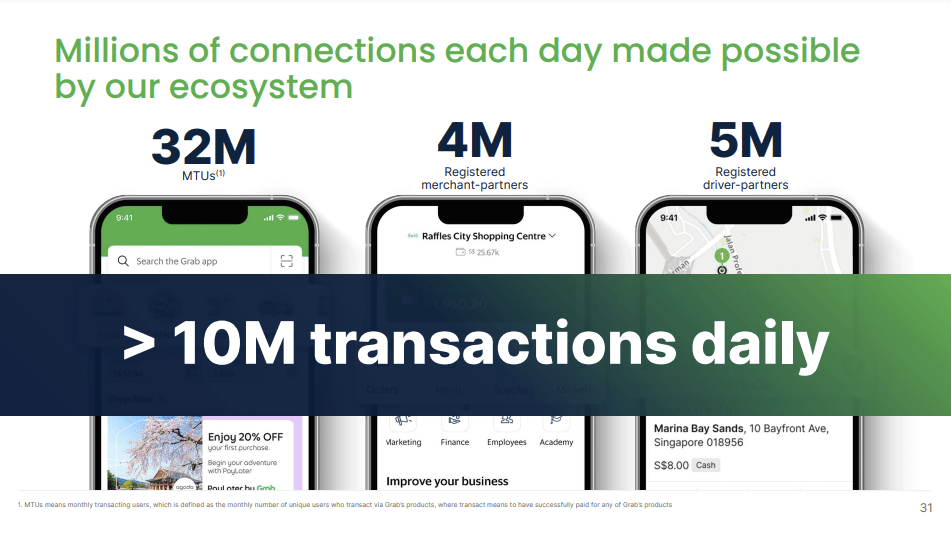

In Grab's case, the more users join the platform, the more valuable the platform becomes. Suffice it to say, the Grab ecosystem is massive:

Grab 2022 Investor Day Presentation

At the same time, Grab's enormous network also makes cross-selling incredibly efficient. For example, following the launch of GXBank in Malaysia in November 2023, GXBank was able to attract 100K+ depositors within two weeks, with 79% of GXBank depositors being existing Grab users.

According to ASEAN, there are 680M people in Southeast Asia, which means Grab has a market penetration rate of about 5.5%. This also means that Grab has so much more room for growth.

As Grab adds more offerings, more consumers should join the platform. This should increase overall platform engagement, which will eventually lead to more income opportunities for drivers and merchants. Consequently, more drivers and merchants will also join the platform, which ultimately leads to even more consumers.

This is the Grab ecosystem flywheel in motion which creates powerful network effects for the business.

Grab Investor Presentation April 2021

Cost Advantage

Looking at Morningstar's definition:

A company with a cost advantage can produce goods or services at a lower cost, allowing it to undercut its competitors or achieve higher profitability.

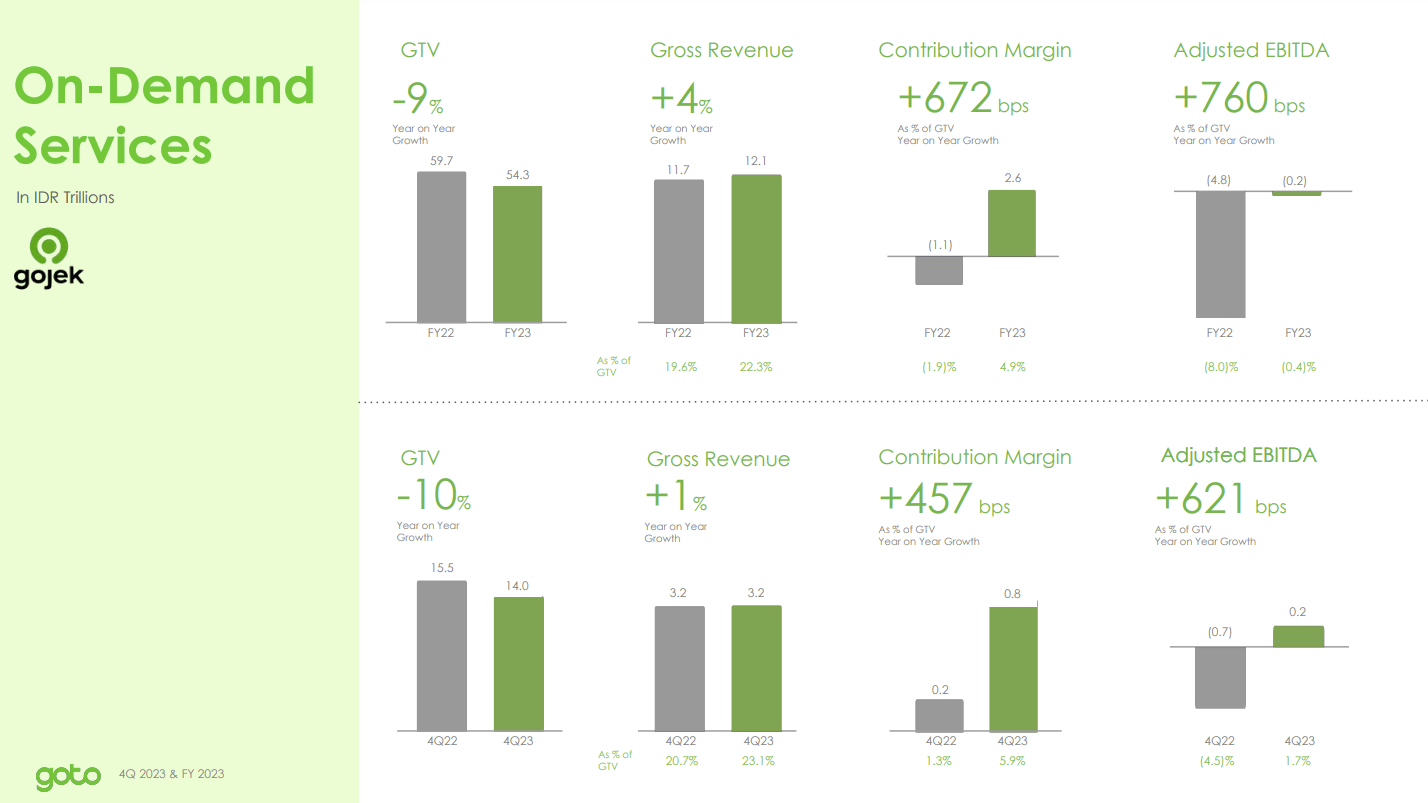

GoTo — the parent company of GoJek and Tokopedia, Indonesia's largest mobility and e-commerce companies — is the closest competitor to Grab.

If we take a look at GoTo's On-Demand Services segment, we can see that GoTo has an Adjusted EBITDA Margin of 1.7% (as a % of Gross Merchandise Volume) in Q4 of 2023.

GoTo FY2023 Q4 Investor Presentation

In contrast, Grab's On-Demand segment produced $278M of Adjusted EBITDA in Q4 last year, at an Adjusted EBITDA Margin of 6.7% (as a % of GMV).

In other words, Grab has a huge cost advantage over GoTo — I'm not even going to compare it with smaller competitors since they most likely have much worse unit economics.

Why?

Because Southeast Asia is a highly competitive market and the only way to achieve profitability is to have a large enough scale to gain operating leverage — Grab has the scale, and subsequently, the cost advantage to defeat its competition.

This brings us to the last moat...

Efficient Scale

... which is the most important of all:

Efficient scale benefits companies operating in a market that only supports one or a few competitors, limiting rivalry.

Much like how the US ride-hailing and food delivery industries are dominated by a few players like Uber and DoorDash (DASH), the Southeast Asian market is also a winner-takes-most market.

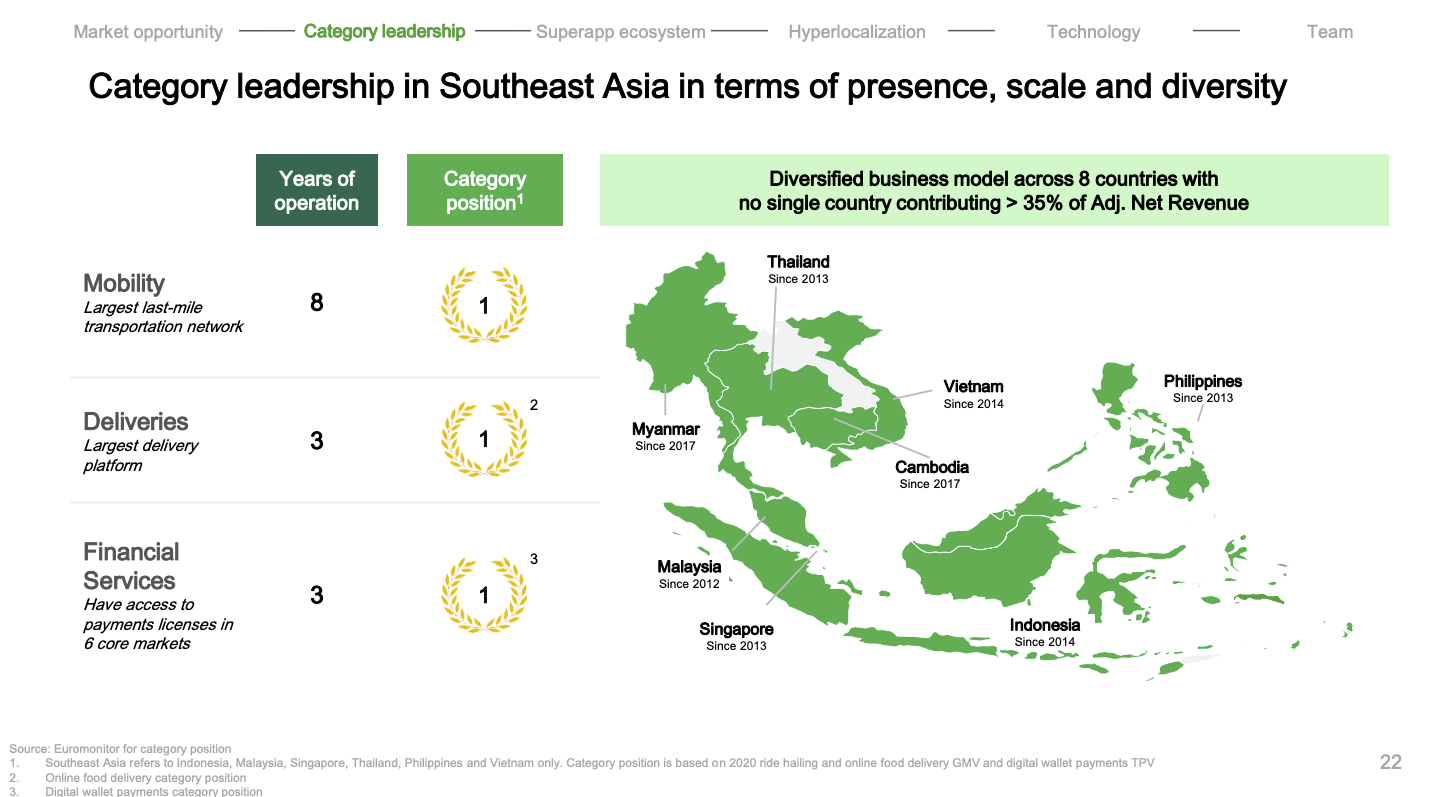

As it stands, Grab is the largest player in Mobility, Deliveries, and Financial Services in Southeast Asia.

Grab Investor Presentation April 2021

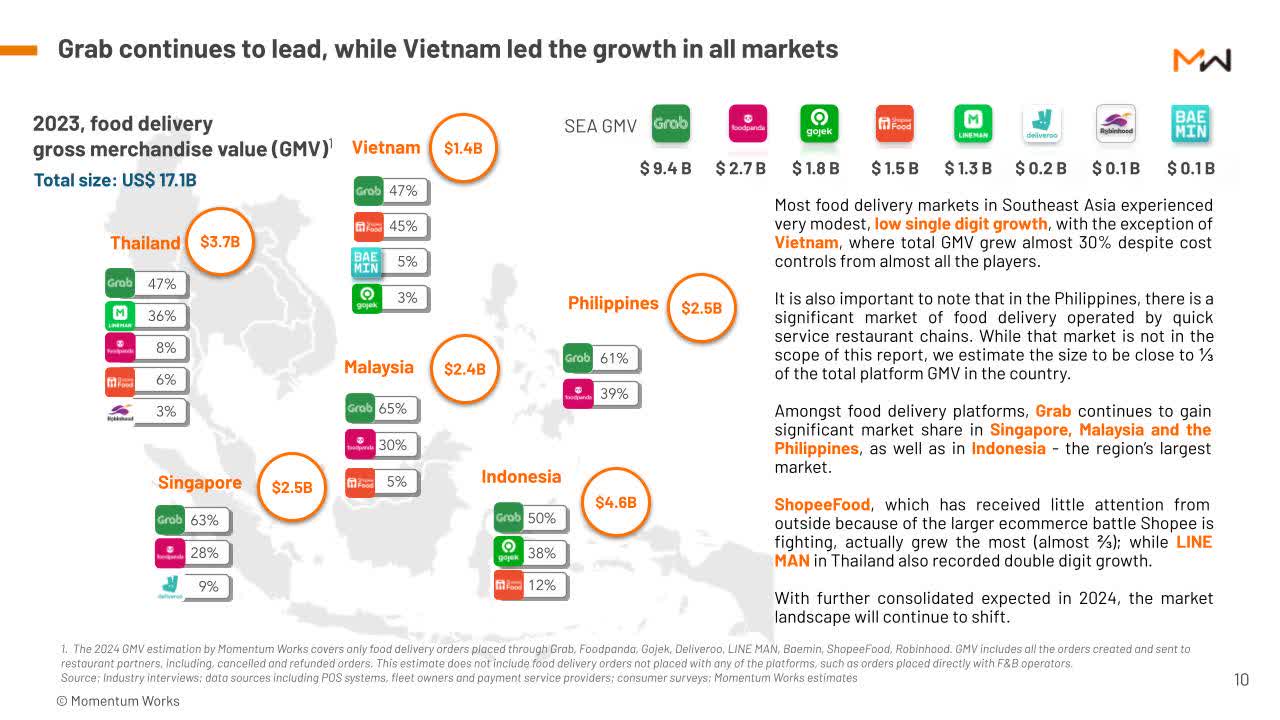

Below, we can see that Grab has the lion's share in the food delivery market in each of the Southeast Asian countries. In 2023, Grab processed $9.4B of food deliveries GMV, which is many times larger than its closest competitor, Food Panda, which has an estimated GMV of only $2.3B.

Southeast Asia is a fertile ground for us. We're now the largest on-demand platform in the region at a scale that is over three times larger than our next closest competitor and yet, there's still a lot for us to achieve for our partners in this region.

(CEO Anthony Tan — Grab FY2023 Q4 Earnings Call.)

Momentum Works

As far as I know, Grab is also the most capitalized player in Southeast Asia. Being the most funded business enables Grab to take market share and expand even more aggressively than competitors. This is one of the major reasons why Uber failed in Southeast Asia.

According to INSEAD, Grab overtook Uber as the leader in Southeast Asia due to its massive funding of $4B. Uber, on the other hand, only spent $700M in the region.

Basically, scale is the most important competitive moat because it reinforces the other four moats:

That being said, I believe Grab has all five of Morningstar's moats, which makes it one of the most durable businesses in modern times — its moats will ultimately allow Grab to not only crush competition but also sustain profitability and capture growth opportunities.

Before we dive into the financials, let's talk about how Grab generates and recognizes Revenue.

Grab operates four business segments, namely: Deliveries, Mobility, Financial Services, and Enterprise.

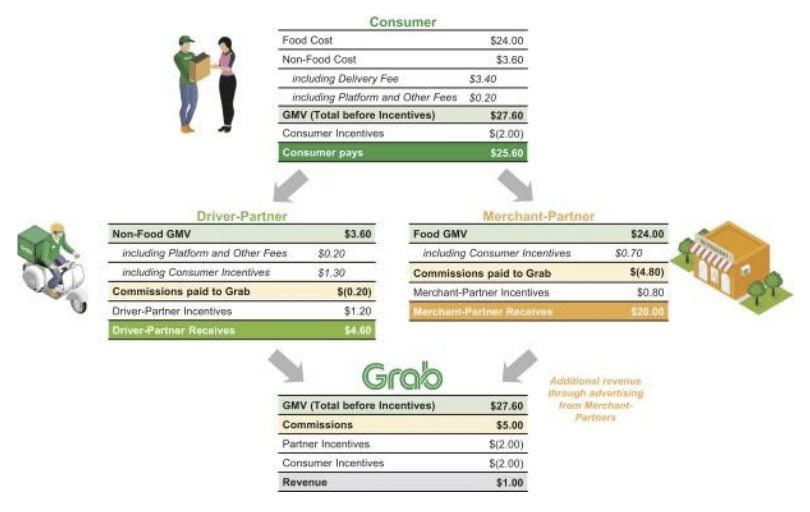

Below, you can see what a typical food Delivery transaction looks like.

Grab FY2022 Annual Report

As you can see, Grab acts as the middleman that connects three different parties: consumers, drivers, and merchants.

Grab also generates Mobility Revenue in a similar fashion, just that merchants are not involved in the transaction.

So, Deliveries and Mobility make up the On-Demand segments of the company.

In addition, Grab also generates Financial Services revenue through transaction fees. The segment also earns non-transaction fees through services such as lending and insurance.

Finally, Grab generates Enterprise Revenue mainly through advertising services.

With that out of the way, let's take a look at Grab's growth trajectory.

In 2023, GMV was $20.1B, up 5% YoY. In Q4, GMV was $5.4B, up 9% YoY. Growth was primarily due to the expansion of its Mobility and Deliveries segment, which I'll go into more detail later on.

That said, growth has accelerated for three straight quarters, which is a good sign that the company is gaining momentum and market share.

Author's Analysis

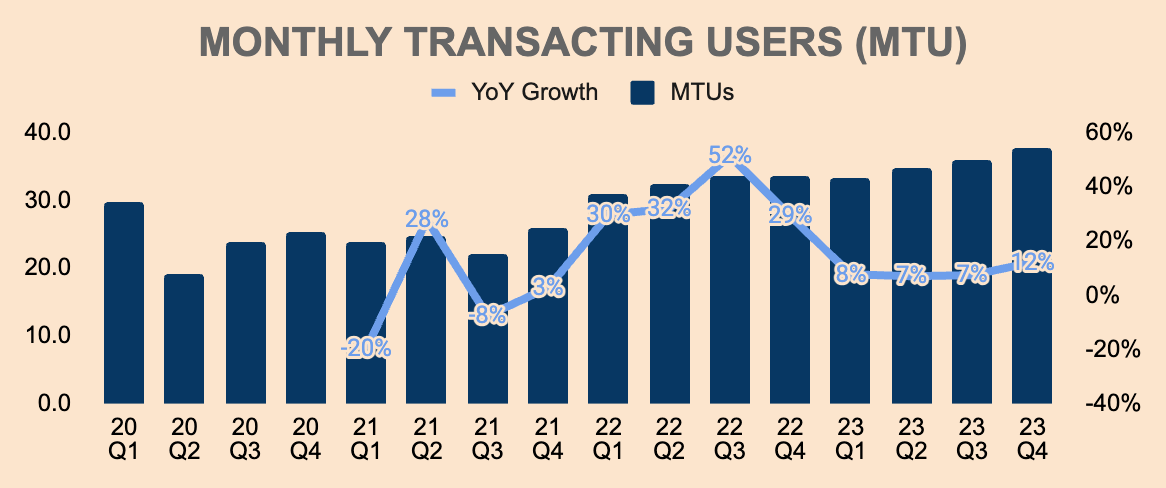

GMV was also driven by increasing MTUs in the platform, which was 37.7M as of Q4, up 12% YoY. The number of users on a platform is one of the most important metrics to track since users are a leading indicator of future Revenue growth. In addition, user growth is an indication of strong platform engagement and increasing network effect moats.

Author's Analysis

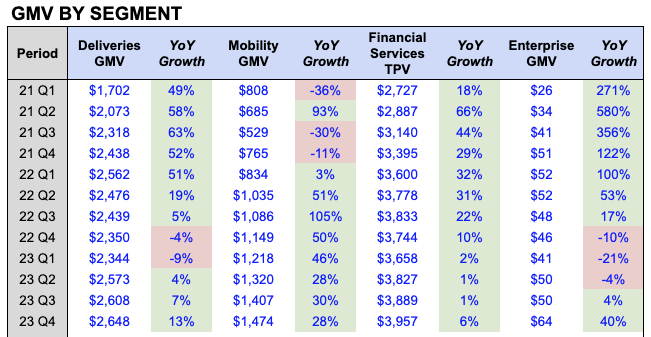

That said, let's look at GMV by segment.

As you can see, all segments are showing robust growth.

Author's Analysis

Q4 Deliveries GMV was $2.6B, up 13% YoY, due to higher spend per user and higher Deliveries MTUs, which reached an all-time high in Q4.

Greater affordability of Grab's services also contributed to growth. For instance, Saver deliveries — which offer a lower delivery fee in exchange for a longer delivery time — increased average order frequency by 1.6x, as compared to non-Saver users. Saver was first launched in Q1 last year and has now accounted for more than 23% of Deliveries transactions.

Moving on, Mobility GMV grew strongly in Q4, which was $1.5B, up 28% YoY. Of important note, the Mobility segment was heavily impacted by the pandemic but has now fully recovered with GMV exceeding pre-covid levels for the first time in Q4. This was driven by higher Mobility MTUs, higher average order frequency, and the rebound in the travel industry.

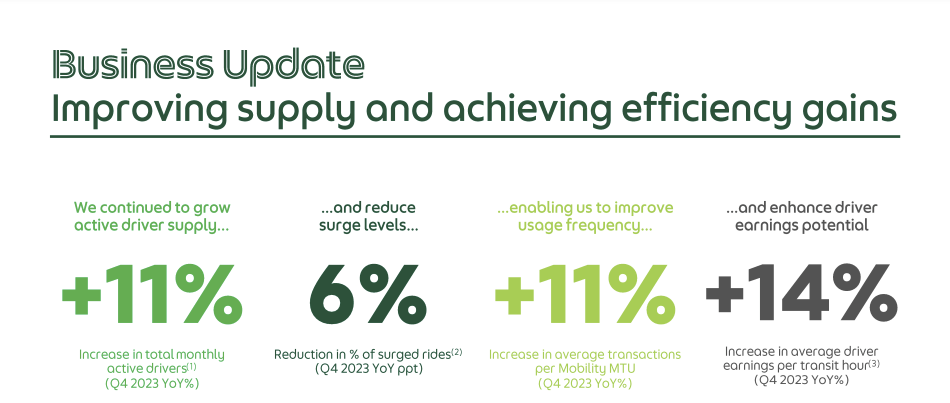

Grab is experiencing strong demand for its Mobility services which is why management is focusing on expanding its driver supply and improving driver efficiency. As you can see, Grab managed to increase its driver supply by 11% YoY in Q4, which consequently reduced surged rides by 6% YoY and increased average transactions per MTU by 11%.

Grab FY2023 Q4 Investor Presentation

Next, the Financial Services segment grew Total Payment Volume, or TPV, by 6% YoY in Q4, to nearly $4B.

The growth in On-Grab Volume and decline in Off-Grab Volume reflect management's focus on driving ecosystem transactions, as the unit economics for Off-Grab transactions were not as attractive:

You'll remember going all the way back to September 2022 when we had the Investor Day, we talked about moving away from the off-platform payments business where the transaction margins were not contributing to our path to profitability.

That's been ongoing. Off-platform transactions continue to fall. And that means that the margin mix improves for our payments business.

(COO Alex Hungate — Grab FY2023 Q3 Earnings Call, emphasis added.)

Finally, Q4 Enterprise GMV was $64M, up 40% YoY, due to the growth of Grab's advertising business. This is still a small segment so growth will likely be volatile in the short-to-medium term.

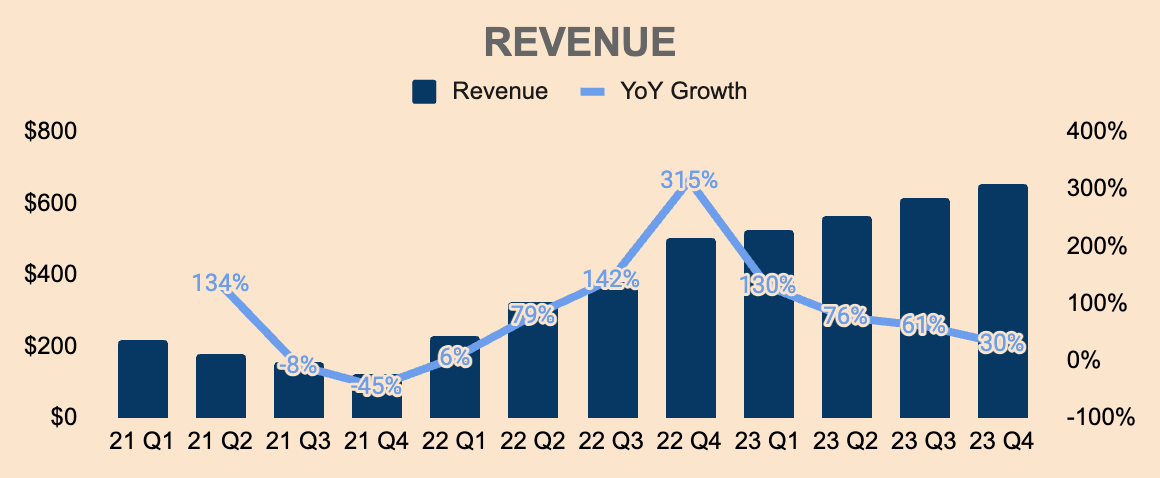

That being said, Revenue for the full year was $2.4B, up 65% YoY. This beat management's initial guidance of $2.2B to $2.3B.

In Q4, Revenue was $653M, up 30% YoY. This beat analyst estimates by $20M.

Great to see Grab outperform expectations.

Growth was mainly due to GMV growth across all segments, a change in business model for certain delivery offerings, and the reduction in incentives.

Author's Analysis

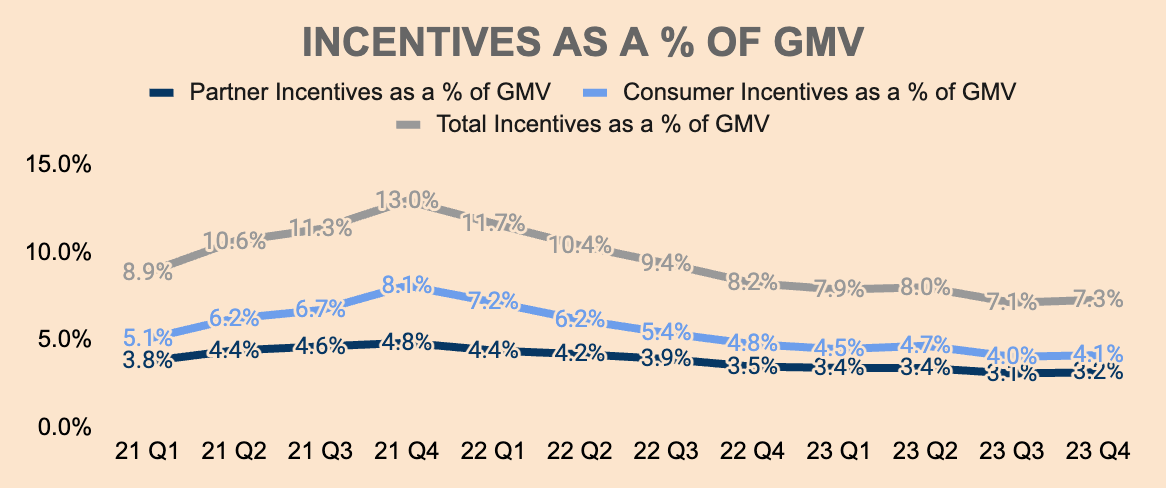

If you haven't realized, Revenue grew much faster than GMV, and this is due to the reduction of incentives.

As a reminder, Grab's Revenue is equal to the commissions and fees it collects from drivers and merchants, minus any incentives it gives out to these partners and its consumers.

As you can see, Grab's Total Incentives as a % of GMV was as high as 13% in Q4 of 2021. This was an effort to defend against competition as well as mitigate consumers and partners from churning during the pandemic.

However, as market conditions stabilized, Grab was able to reduce incentives without jeopardizing the company's growth. As of Q4, Incentives as a % of GMV was 7.3%, down from 8.2% last year, which led to robust Revenue growth.

Ideally, we want to see this metric continue to decline.

Author's Analysis

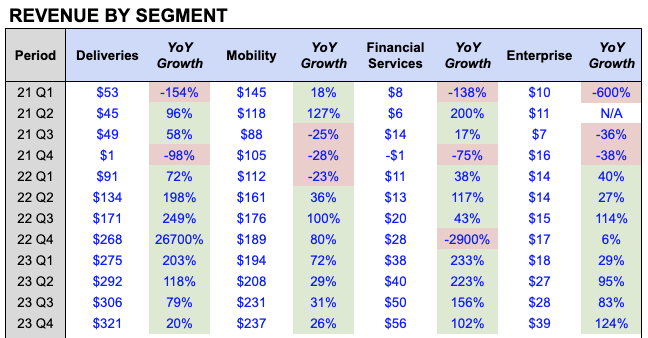

Below, you can see strong Revenue growth for each of Grab's segments, driven by platform monetization and incentive reduction.

Author's Analysis

Of particular note, the Financial Services and Enterprise segments grew triple-digits YoY. I believe these smaller segments could be major contributors to growth in the coming years as Grab continues to monetize its user base.

For instance, Grab is ramping up investments in its Financial Services segment.

Grab FY2023 Q4 Investor Presentation

In addition, Grab's Enterprise segment — which consists primarily of advertising — is still in its early innings. The segment is quickly gaining traction with self-serve active advertisers increasing 54% YoY and average spend by active advertisers growing 129% YoY.

All in all, Grab is showing strong growth as it recovers from the economic shock left by the pandemic.

All its segments are generating record-high GMV (and TPV), and I don't see any signs of slowing down given Grab's durable competitive moats.

What's more, platform monetization and incentive optimization are improving, which should lead to robust Revenue and earnings growth moving forward.

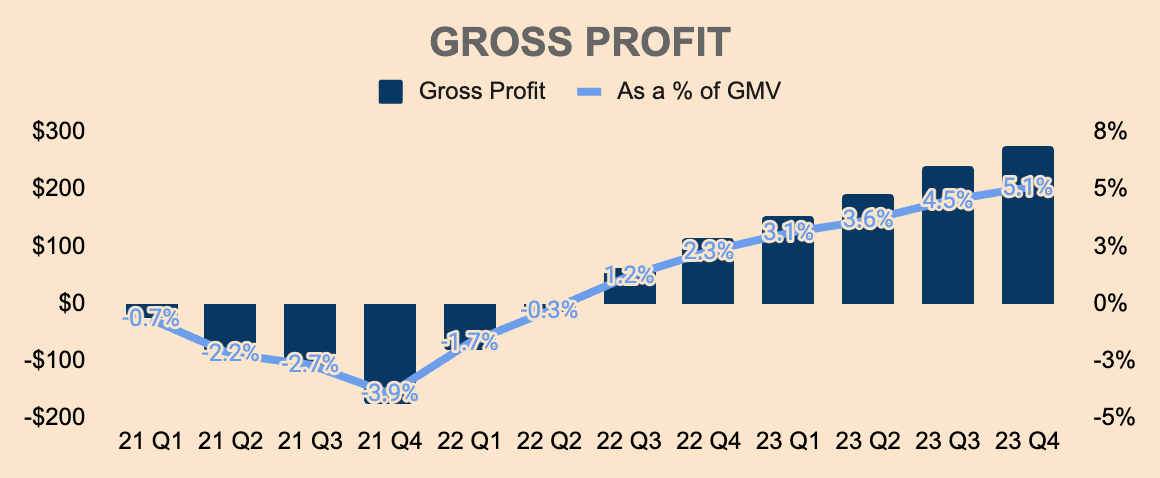

In this section, I will analyze Grab's profit margins by using GMV as the denominator (instead of Revenue). This way, we can see how margins are trending without the volatility of Revenue since Revenue is largely affected by total incentives paid.

That said, Q4 Gross Profit was $276M, which was 5.1% of GMV. As you can see, Grab was Gross-Profit-negative a couple of years ago due to the company pumping massive amounts of incentives to consumers and partners. However, Gross Profit has turned positive as the company focuses on profitable growth.

Author's Analysis

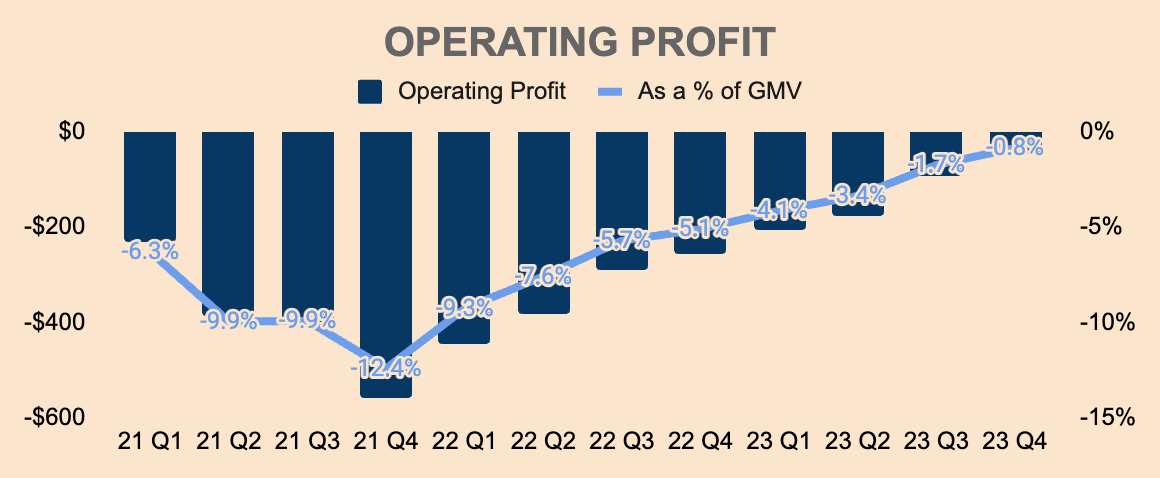

On the other hand, Operating Profit is still negative at $(46)M in Q4, which was (0.8)% of GMV. On the bright side, Grab is showing strong operating leverage and a clear path towards profitability — Operating Margin improved by 430 basis points YoY and 90 basis points QoQ, which means that Operating Profit is on track to turn positive as early as Q1 this year.

Author's Analysis

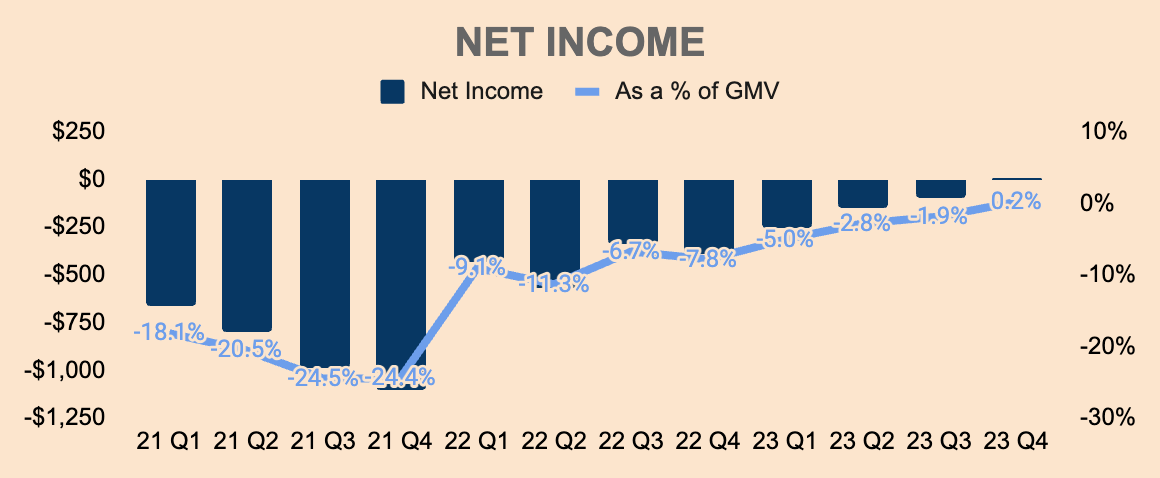

In terms of the bottom line, Grab turned profitable on a Net Income basis for the first time ever. In Q4, Net Income was $11M, which was 0.2% as a % of GMV. Net Income was better than Operating Profit due to improvement in fair value changes in investments as well as higher net interest income.

Author's Analysis

Increases in Adjusted EBITDA also contributed to income growth.

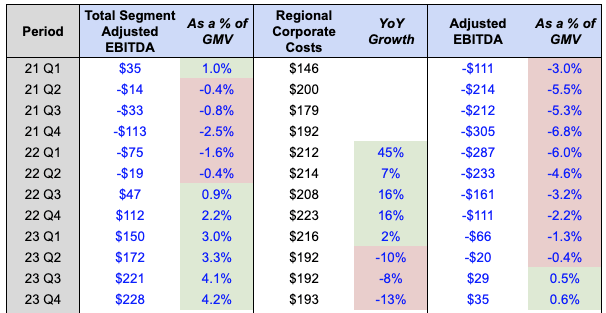

As you can see, Total Segment Adjusted EBITDA has been increasing with each passing quarter with $228M in Q4, which is 4.2% of GMV, up 200 basis points YoY.

Subtracting Regional Corporate Costs, we get Adjusted EBITDA, which has been improving as well. In Q4, Adjusted EBITDA was $35M, which is the eight consecutive quarter of improvement. This represents 0.6% of GMV, up 280 basis points YoY, due to lower Regional Corporate Costs as the company began layoffs in June last year.

Author's Analysis

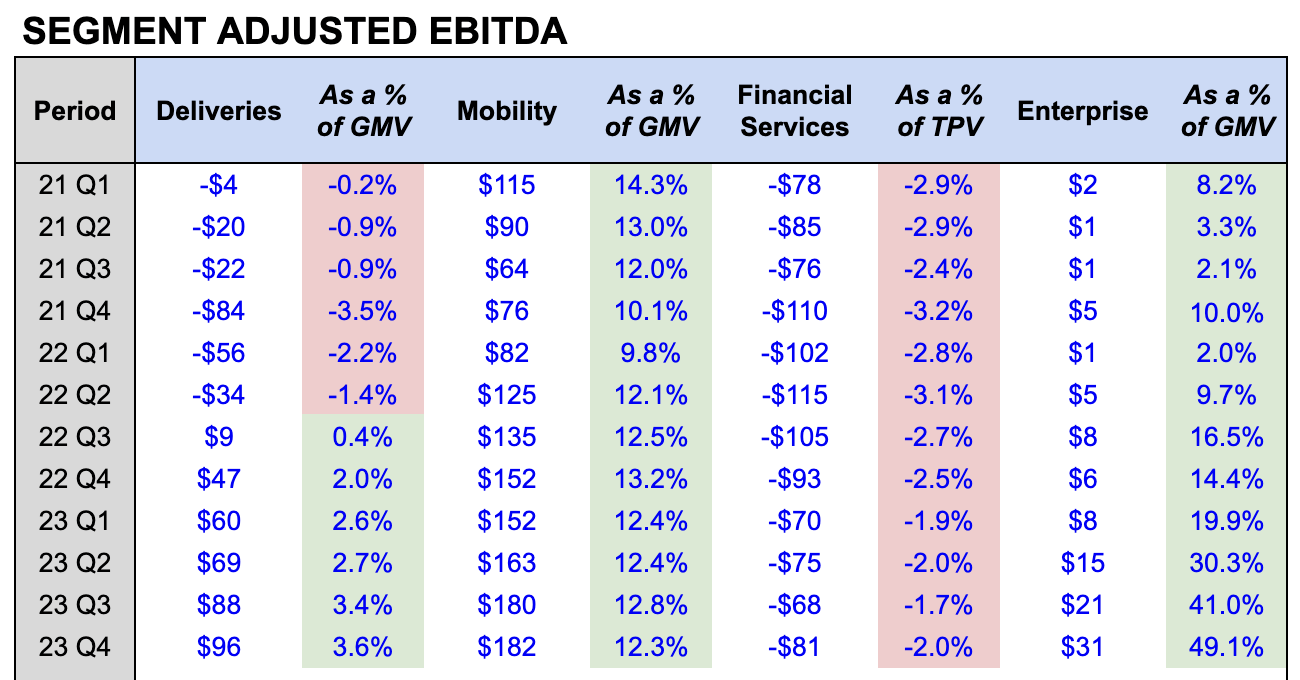

Looking at Segment Adjusted EBITDA, we can see the profitability of each segment:

Author's Analysis

As you know, Grab has been operating at massive losses in the first decade of its existence, due to heavy investments to acquire users, launch new products, and expand geographically.

But recently, the company has just turned Net Income profitable as the company focused on optimizing incentives, improving its cost structure, and scaling Revenue.

As we've seen, Grab's profitability metrics are all trending in the right direction, showing strong economies of scale over the last few quarters.

This will not only make the company self-sufficient but also strengthen its cost advantage and efficient scale moats, leading to an even stronger competitive positioning.

All things considered, this is just the beginning of Grab's profitability journey.

Along with improving profitability, Grab also has a fortress balance sheet.

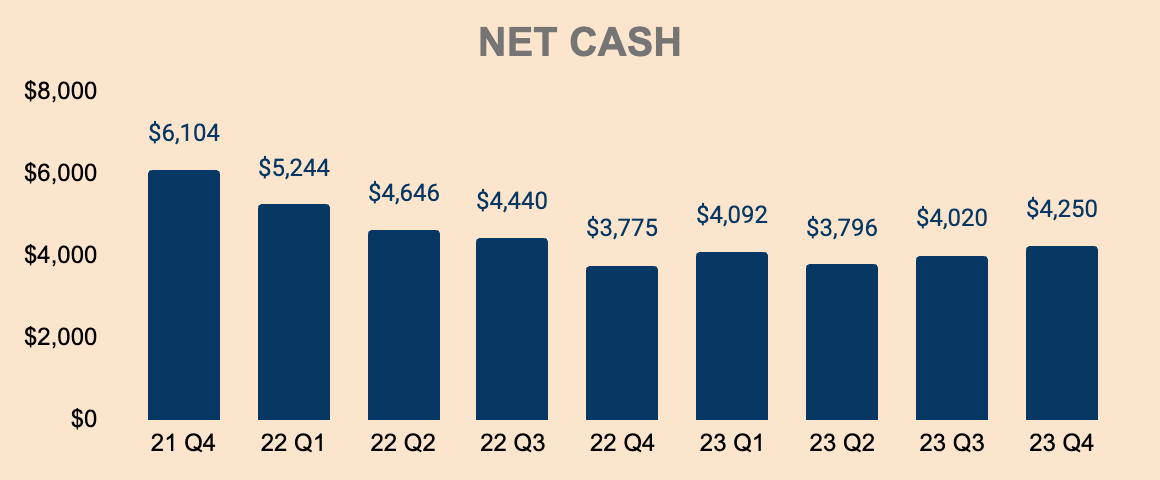

As of Q4, Grab has a Net Cash position of about $4.3B, which is over 30% of its current Market Cap of $12.4B. Net Cash has been on a downfall, but that's understandable given that the company is still in investment mode. However, Net Cash balance should grow over the next few quarters as Grab continues to improve profitability.

Management also plans to repay their Term Loan B debt facility, which is expected to reduce annual interest expenses by $50M, further improving profitability and cash flows.

Author's Analysis

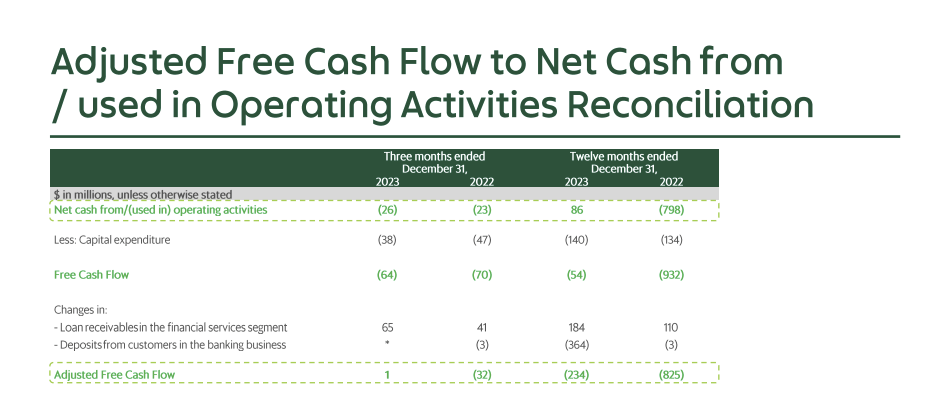

In terms of cash flow, Grab is still cash flow negative on an annual basis.

In 2023, Free Cash Flow was $(54)M, a major improvement from $(932)M in 2022. However, this includes $184M of Loans Receivables and $364M of Customer Deposits — adjusting for this, Adjusted FCF was $(234)M in 2023, still a decent improvement from $(825)M in 2022. This was mainly driven by higher Cash Flow from Operations, which turned positive in 2023 — great to see but still a lot of work to do.

Grab FY2023 Q4 Investor Presentation

Nevertheless, in light of Grab's improving profitability and strong balance sheet, Grab announced a $500M share buyback program, which reflects not only management's confidence about the financial health of the company but also how attractive the valuation of the company is at current prices.

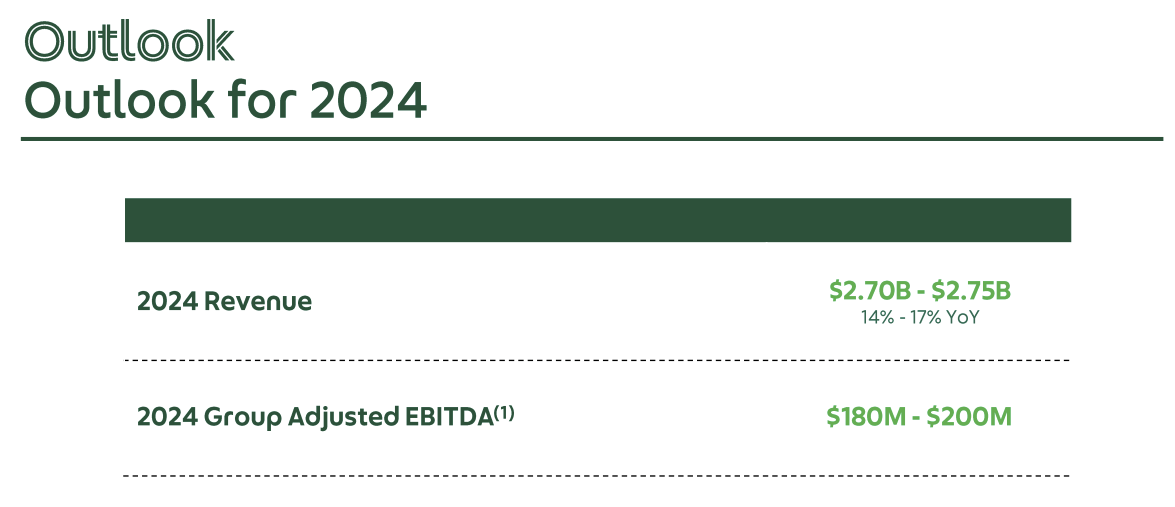

Turning to the outlook, management provided the following guidance:

Grab FY2023 Q4 Investor Presentation

The CFO also gave out more details about their outlook:

In short, growth is expected to remain robust as Grab pulls multiple growth levers across its four segments. In addition, profitability is only going to get better from here which should accelerate earnings growth in the coming years.

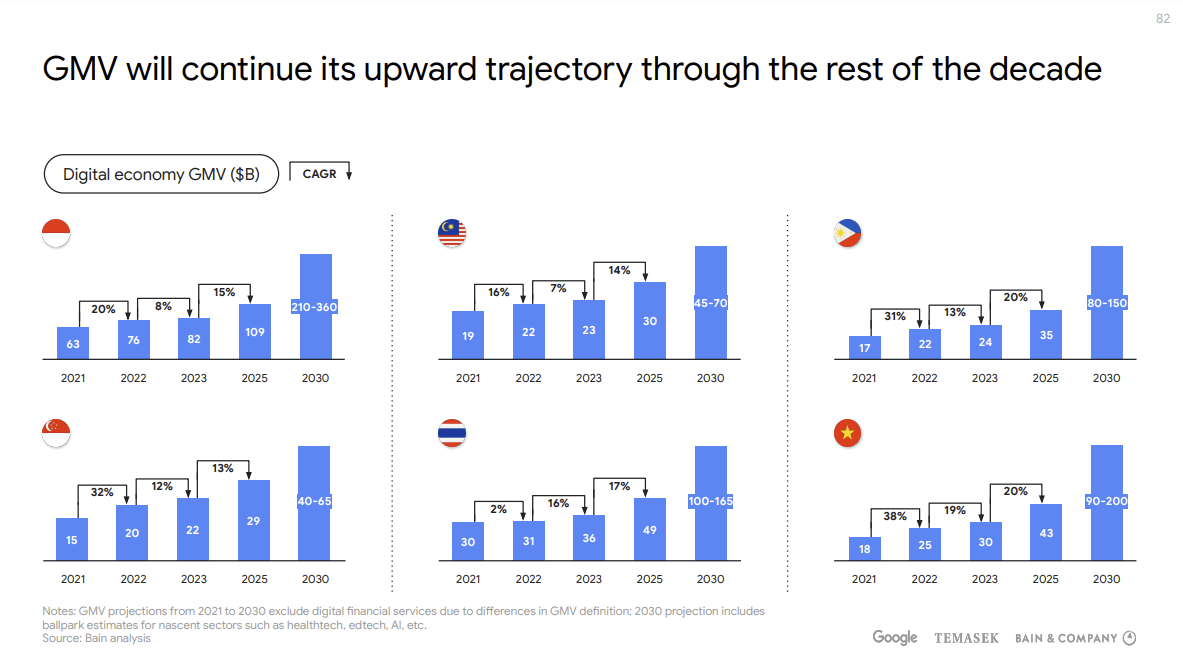

Whatever it is, Grab — although more than a decade old — is still in its early stages of growth, due to the undergoing digital transformation in Southeast Asia.

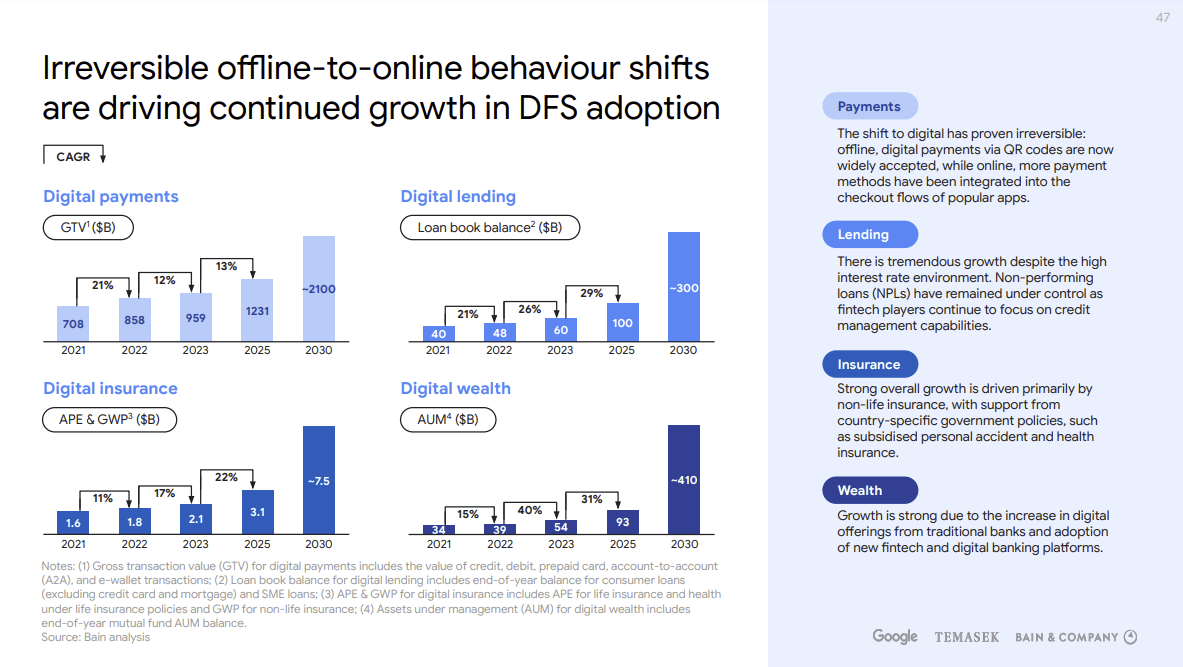

According to the e-Conomy SEA 2023 report, food delivery GMV and mobility GMV in Southeast Asia are expected to grow at a 12% and 18% CAGR, respectively, from 2023 to 2025. In addition, digital advertising GMV is set to expand by 15% through 2025.

But the most exciting growth opportunity for Grab lies in the fintech sector. According to the report, digital financial services adoption in Southeast Asia is deemed irreversible. As you know, Grab offers digital payments, lending, and insurance services currently, and these subsectors are expected to take off in the next few years as you can see below.

e-Conomy SEA 2023

Given the underbanked and unbanked majority in Southeast Asia, I believe Grab's Financial Services has a long growth runway ahead. Scaling its financial products should be seamless as Grab can distribute them through its superapp — Grab has the luxury to rapidly cross-sell its products by tapping its massive scale and network.

For these reasons, I believe the full potential of Grab's digital Financial Services segment has yet to be realized.

That being said, Grab has a massive growth runway ahead as the regional leader in deliveries, mobility, and financial services — the growth of the digital economy in Southeast Asia will be a massive tailwind for the superapp.

e-Conomy SEA 2023

Valuing Grab is quite a challenge since the company just turned profitable and that management has not issued long-term financial targets.

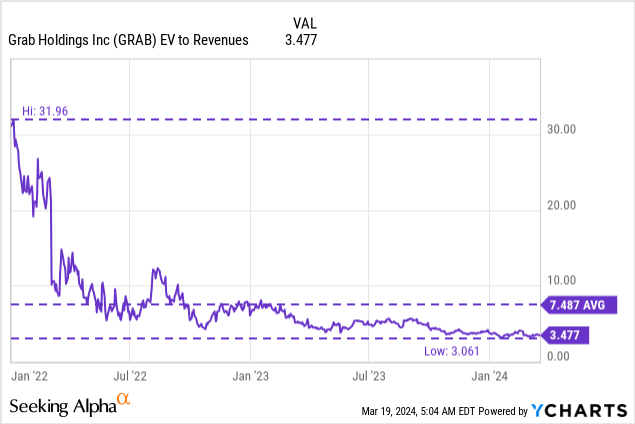

That said, Grab currently trades at an EV to Revenue multiple of just 3.5x, which is quite cheap relative to its peak multiple of 32x and average multiple of 7.5x.

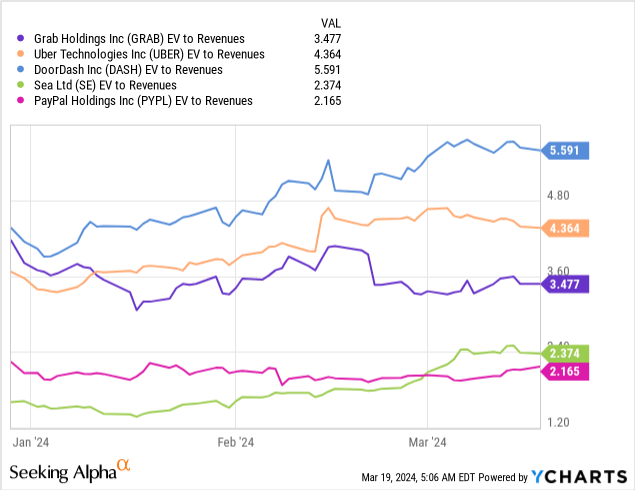

Given the complexity and uniqueness of Grab's business model, there's no direct competitor that we can compare with. Still, it's interesting to see Grab trading cheaper than its US peers Uber (4.4x) and DoorDash (5.6x) — perhaps, US stocks get a premium over Asian stocks.

On the other side, Grab is trading more expensively than fellow Southeast Asian conglomerate Sea Limited (SE), which is trading at 2.4x. And just for fun, I've thrown in PayPal (PYPL) as well, which trades at 2.2x.

In my opinion, Grab should be trading at higher valuations compared to its peer group considering that Grab is essentially Uber, DoorDash, and PayPal mashed together.

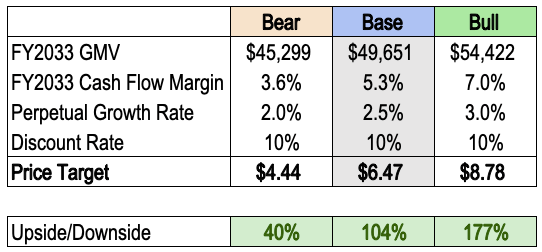

Performing a discounted cash flow ("DCF") analysis on Grab is quite a redundant exercise, but I'm going to attempt it anyway — using very conservative assumptions, of course.

I will be using Adjusted EBITDA as a proxy for Cash Flow from Operations, and then subtract Capital Expenditures and Income Tax to arrive at a figure close to the company's Adjusted FCF.

That said, here are my key assumptions:

Author's Analysis

Based on the assumptions above, I project a GMV of nearly $50B by 2033 at a Cash Flow Margin of about 5.3% of GMV.

Author's Analysis

Based on a perpetual growth rate of 2.5% and a discount rate of 10%, I arrive at an intrinsic value per share of $6.47 for Grab stock, which represents an upside of more than 100% at its current price of $3.17.

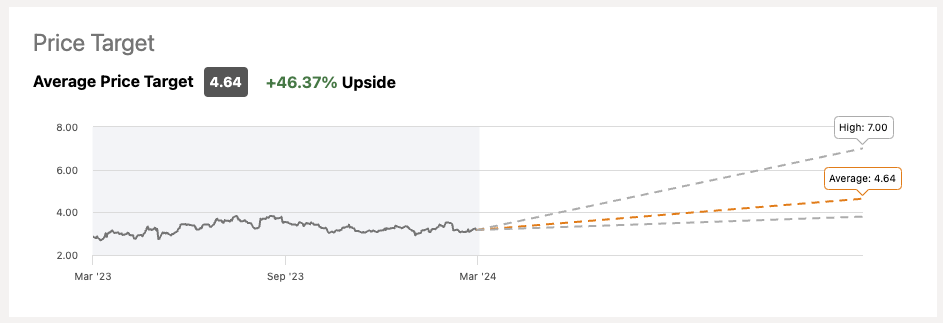

As a reference, analysts have an average price target of $4.64 for Grab stock with a street high of $7.00. As of this writing, there are 21 Strong Buy and 6 Buy recommendations, with ZERO Sell ratings.

Seeking Alpha

I've also included my bear and bull cases below.

Author's Analysis

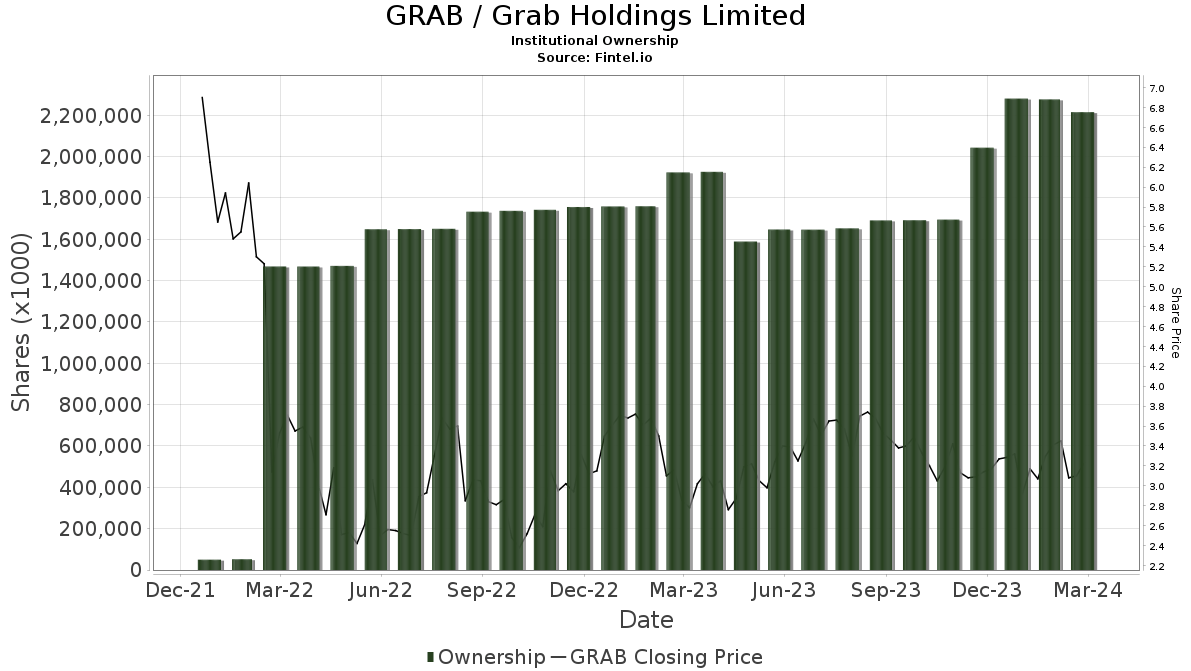

Institutions have also been piling on Grab stock, which could lift the stock higher.

Fintel

To summarize, I believe Grab stock is significantly undervalued.

While Grab has established itself as Southeast Asia's most dominant on-demand services company, competition remains its biggest risk.

This includes GoJek, InDrive, and Bolt in the mobility space. Other international players may also enter Southeast Asia, including India's Ola Cabs and China's Didi Global.

In the deliveries segment, Grab faces competition from GoJek, ShopeeFood, Foodpanda, Deliveroo, Line Man Wongnai, and more. Other large delivery companies may also enter Southeast Asia, including San Francisco's DoorDash and India's Zomato.

In the fintech space, Grab is already dealing with strong opposition, including GoPay, ShopeePay, Dana, Google Pay, and so on.

All this competition may lead to a price war, forcing Grab to deploy more incentives to maintain market share. In addition, the services that Grab offers have the risk of being commoditized, which could mean lower profit margins and cash flows for the company.

However, I believe competition is more of a temporary issue than a permanent one. In my view, competition is unlikely to have the capital resources to compete with Grab on price. They may be able to undercut Grab for a while, but as I've discussed earlier, they are incapable of doing so for a long period of time given Grab's cost advantage, network effects, and efficient scale moats. Not to forget, Grab has $4.3B of Net Cash at its disposal.

I think it's foolish to undercut Grab — it's like digging your own graves.

Other risks include regulations that could increase compliance costs as well as gig worker unions which could lead to lower commission rates for Grab.

In a nutshell, Grab is the baddest superapp in Southeast Asia — its strong brand, high switching costs, powerful network effects, low-cost advantage, and efficient scale moats solidify its status as the undisputed king in the region.

As the company turns profitable and focuses on profitable growth, Grab is in a prime position to capitalize on the growing digital economy in Southeast Asia.

Despite being a fundamentally stronger company today than it has ever been, Grab stock is still down 80%+ from its all-time highs. Moreover, Grab stock has been trading sideways for almost two years — it's essentially in hibernation.

With business momentum back in full force and with fundamentals improving with each passing quarter, it won't be long before the sleeping giant awakens.

With all this in mind, I have started a position in Grab stock.