Busà Photography/Moment via Getty Images

Busà Photography/Moment via Getty Images

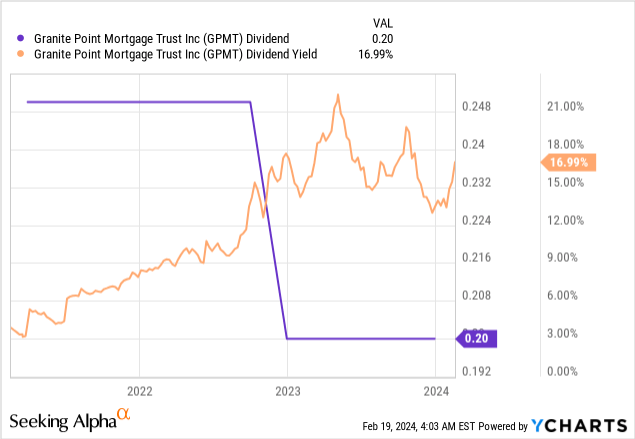

Granite Point Mortgage Trust's (NYSE:GPMT) book value stood at $12.91 per share at the end of its recent fiscal 2023 fourth quarter. This included a $2.71 per share CECL reserve but means GPMT at $4.71 per share is trading at a material 64% discount to book value. This comes as the externally managed mREIT last declared a $0.20 per share quarterly cash dividend, unchanged sequentially and $0.80 annualized for a 17% forward dividend yield. The aggregate of a material dividend yield and a substantial discount to book with the commons going for 36 cents on the dollar form dual reasons for current shareholders to possibly keep their position despite office armageddon. I last covered GPMT in early 2023 to highlight the better stability posed by its floating Series A Preferreds (NYSE:GPMT.PR.A).

Granite Point Mortgage Fiscal 2023 Fourth Quarter Supplemental

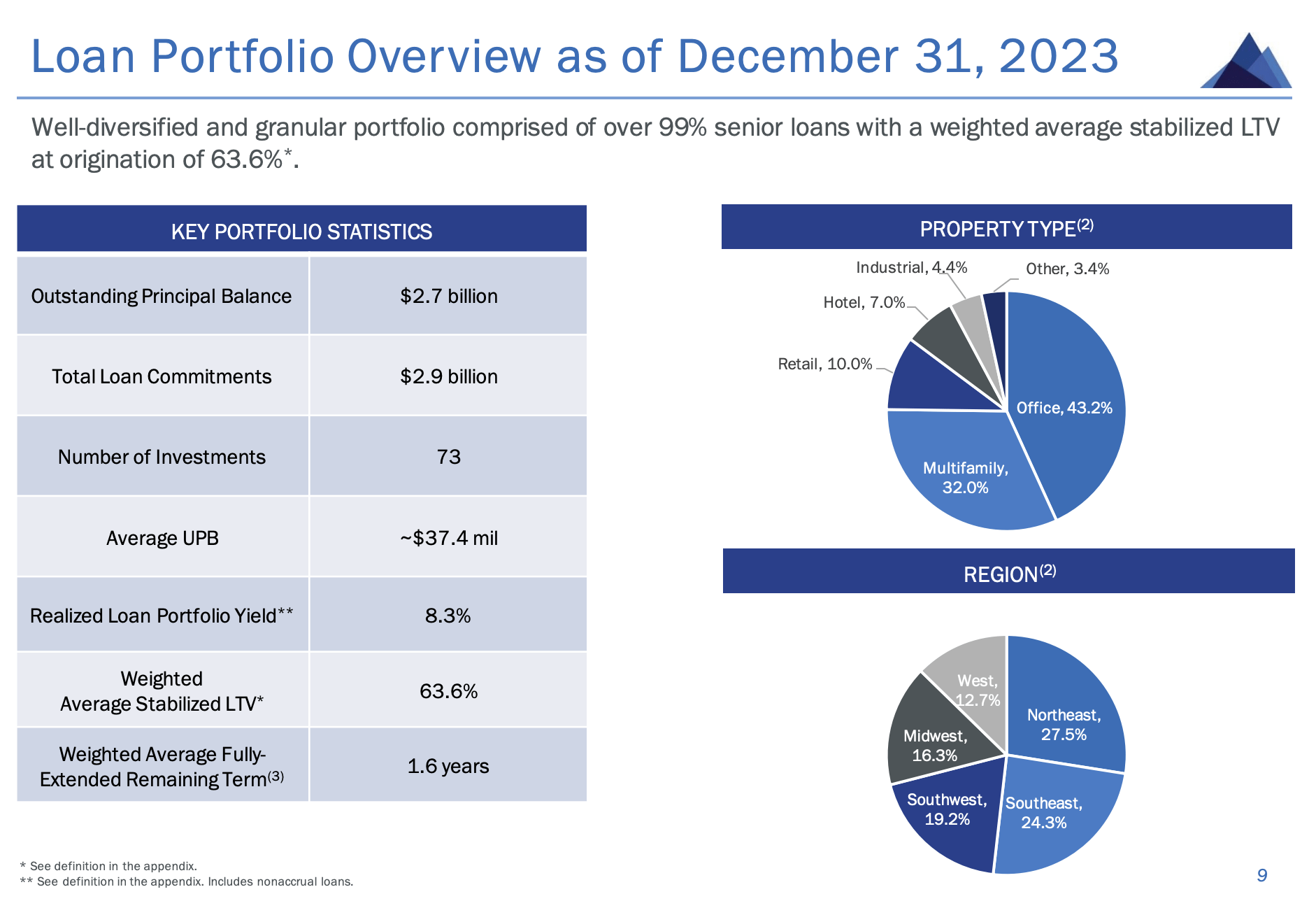

GPMT's loan portfolio had a $2.7 billion outstanding principal balance spread across 73 investments at the end of its fourth quarter. Office properties formed 43.2% of the portfolio's underlying collateral with multifamily as the second largest component at 32%. Critically, the loan portfolio has an 8.3% realized yield and a weighted average fully extended remaining term of 1.6 years. This short-dated remaining term would have been a tailwind pre-pandemic but borrowers will likely find it hard to refinance their loans with the Fed funds rate currently sitting at 22-year highs of 5.25% to 5.50% and against rising office vacancies. Rate cuts are coming with the market pricing in at least 100 basis points of rate cuts exiting 2024.

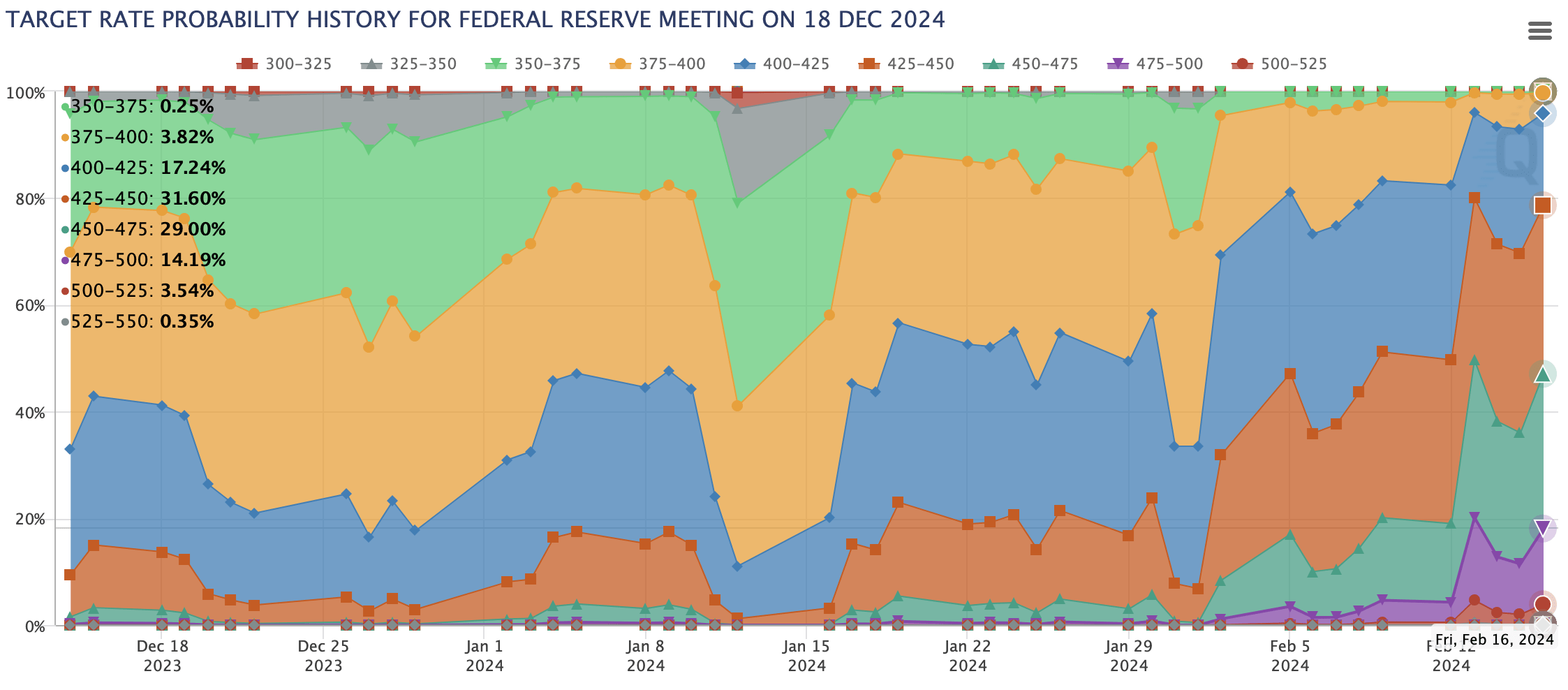

CME FedWatch Tool

GPMT's credit quality forms the most critical factor for a long position as the current discount reflects deep market angst around the impact of rising office vacancies on defaults. The market essentially thinks the current book value should be impaired by as much as 64% to reflect the currently bleak macro backdrop for CRE against a US national office vacancy rate that hit a record high of 18.3% at the end of December, up 180 basis points from its year-ago comp.

Granite Point Mortgage Fiscal 2023 Fourth Quarter Supplemental

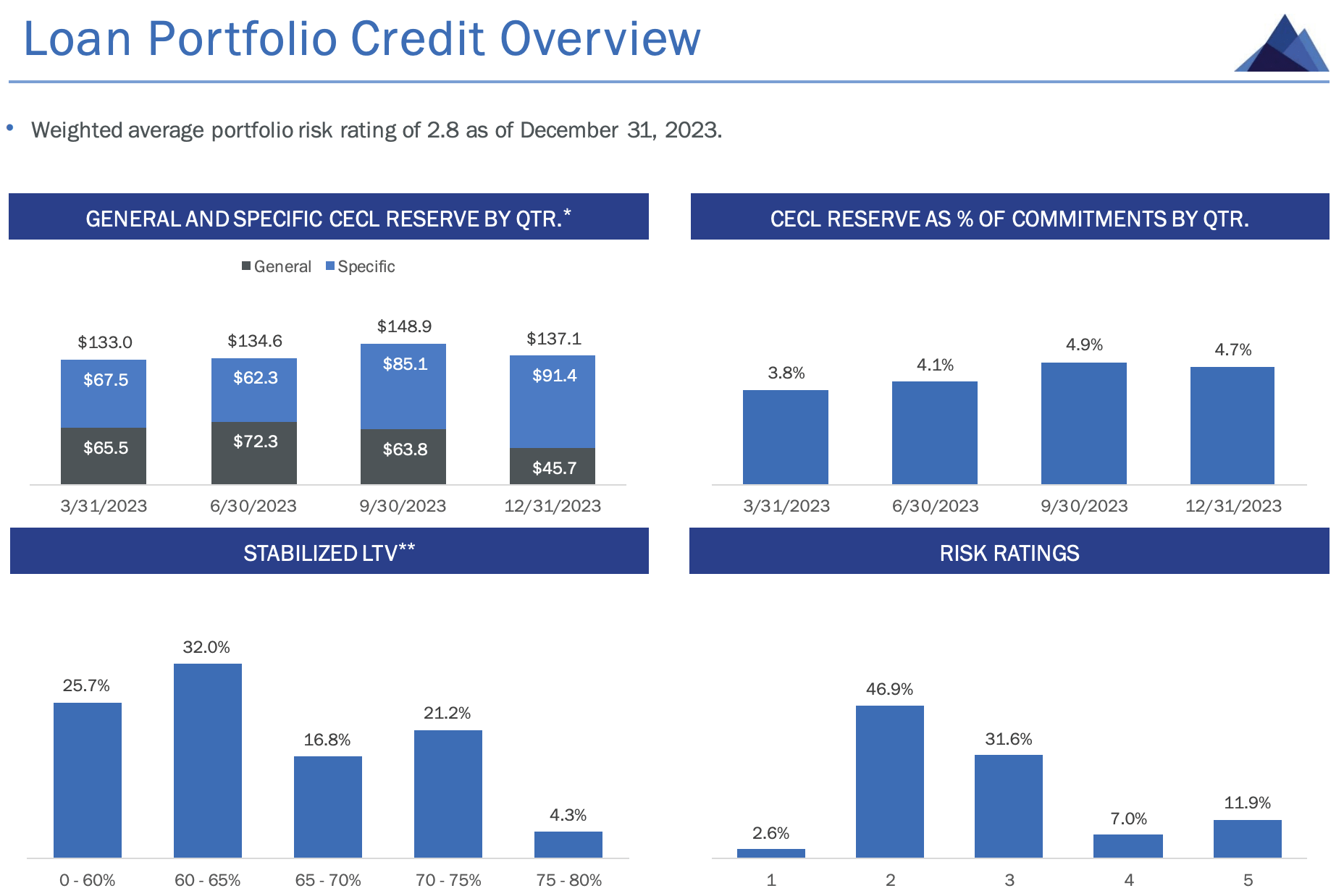

GPMT could see a material amount of its unpaid principal balance due for repayment against this backdrop slip into nonaccrual status as its borrowers face headwinds with refinancing against elevated base interest rates. The mREIT held five loans on a risk rating of "5" and a principal balance of $323.9 million at the end of the fourth quarter. This formed 12% of GPMT's principal balance and came as CECL reserve as a percentage of loan commitments dipped by 20 basis points sequentially to 4.7%. GPMT's weighted average portfolio risk rating exited the fourth quarter at 2.8, up from 2.7 in the third quarter.

Granite Point Mortgage Fiscal 2023 Fourth Quarter Supplemental

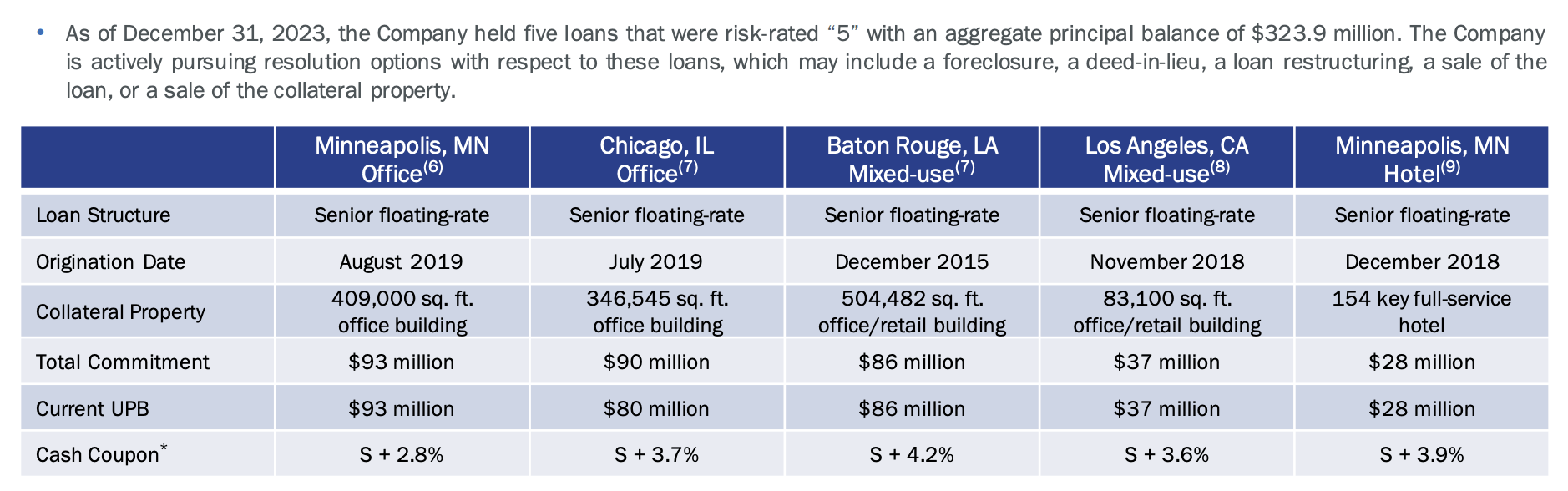

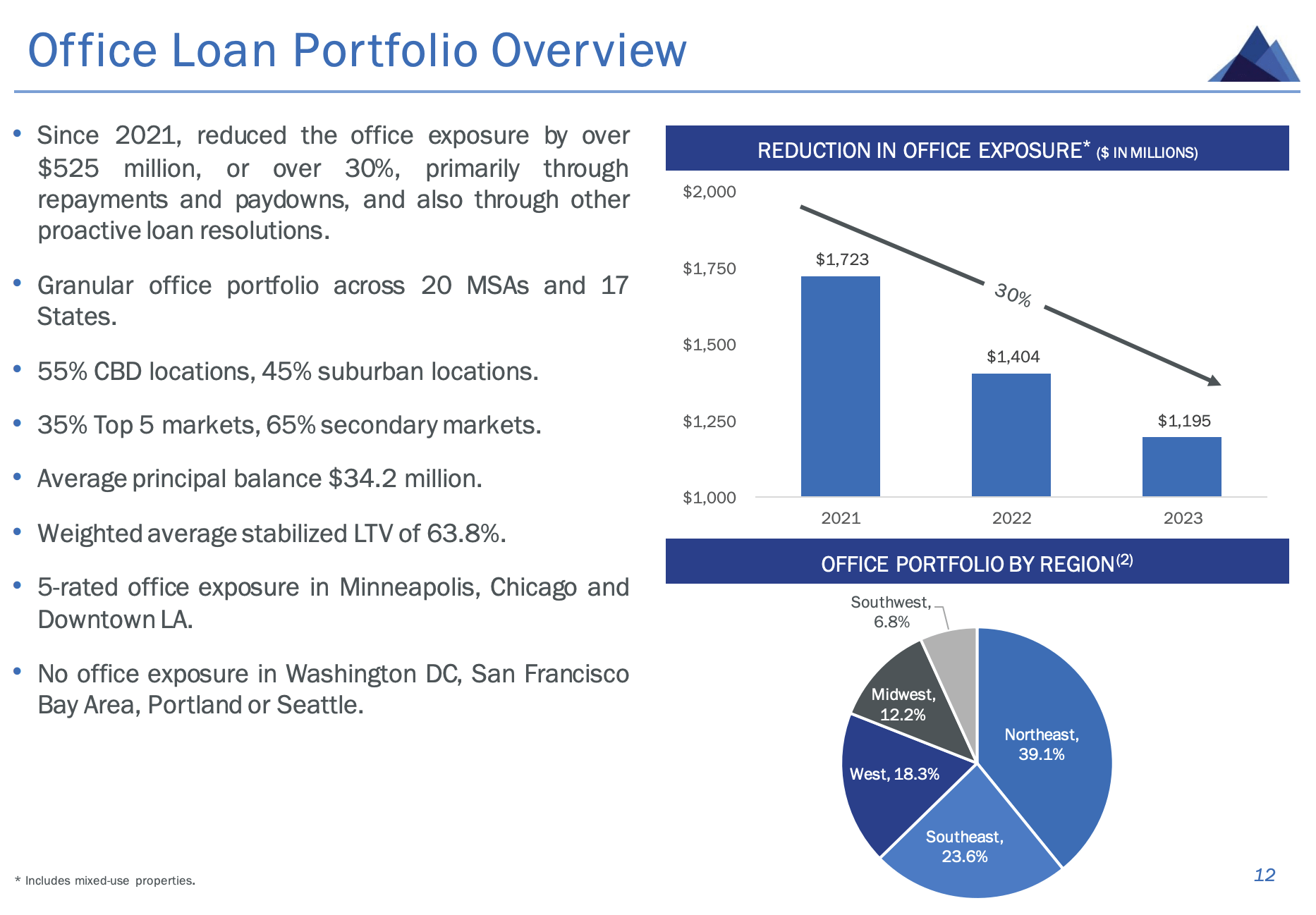

The five problem loans are either office or mixed-used office and retail buildings with a 153-room full-service hotel in Minneapolis also included. GPMT's office exposure has dipped significantly from where it used to be two years ago. There's been a roughly 30% reduction in the unpaid principal balance of office loans from $1.72 billion in 2021 to $1.2 billion in 2023. These properties also had a weighted average loan-to-value of 63.8% with borrowers putting in a decent level of equity.

Granite Point Mortgage Fiscal 2023 Fourth Quarter Supplemental

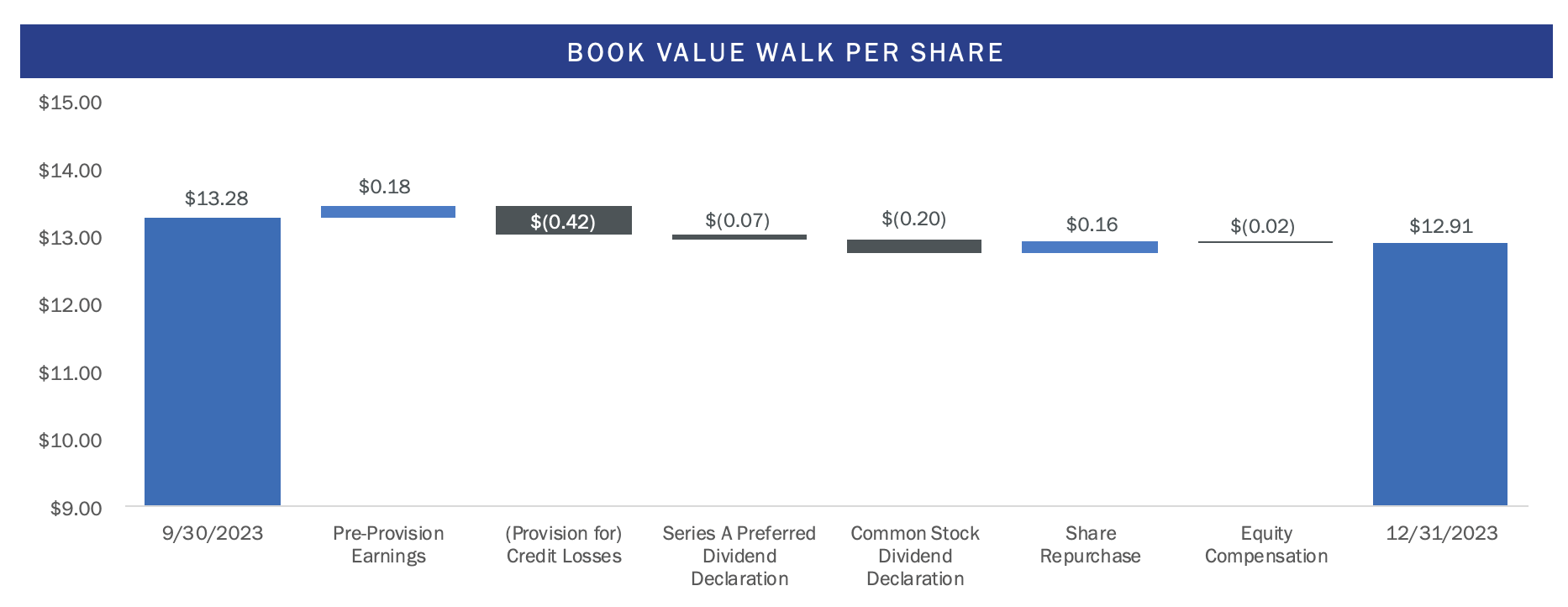

There was around $255 million in loan payoff during the fourth quarter, around $725 million for the full year 2023 with 35% of this repayment volume from office properties. That office repayments were lower than its net office exposure highlights the headwinds being faced by the segment. The discount is essentially the market baking in expectations of a continued deterioration in US office fundamentals. This in the interim will demand high provisions for credit losses and form a $0.42 per share hit to fourth-quarter book value.

Granite Point Mortgage Fiscal 2023 Fourth Quarter Supplemental

GPMT recorded fourth-quarter net interest income of $17.33 million, down 17.4% versus its year-ago comp and a miss by $2.74 million on consensus estimates. The mREIT realized a GAAP net loss of $17.1 million, around $0.33 per share, on the back of its provision for credit losses. Critically, this meant a distributable loss of $26.4 million, around $0.52 per share with a $33.3 million loan write-off, around $0.65 per share, driving the negative inversion.

Adjusting this loss to remove realized losses would have seen distributable earnings of $7 million, around $0.14 per share to mean the mREIT is currently not covering a quarterly distribution. There could be another dividend cut and the outlook for near-term book value growth remains negative. Hence, I'm not immediately attracted to the commons even against the 64% discount to book and 17% dividend yield but will keep GPMT rated as a hold.